Big Tech Earnings Face $600B AI Reality Check Today

1 min ago

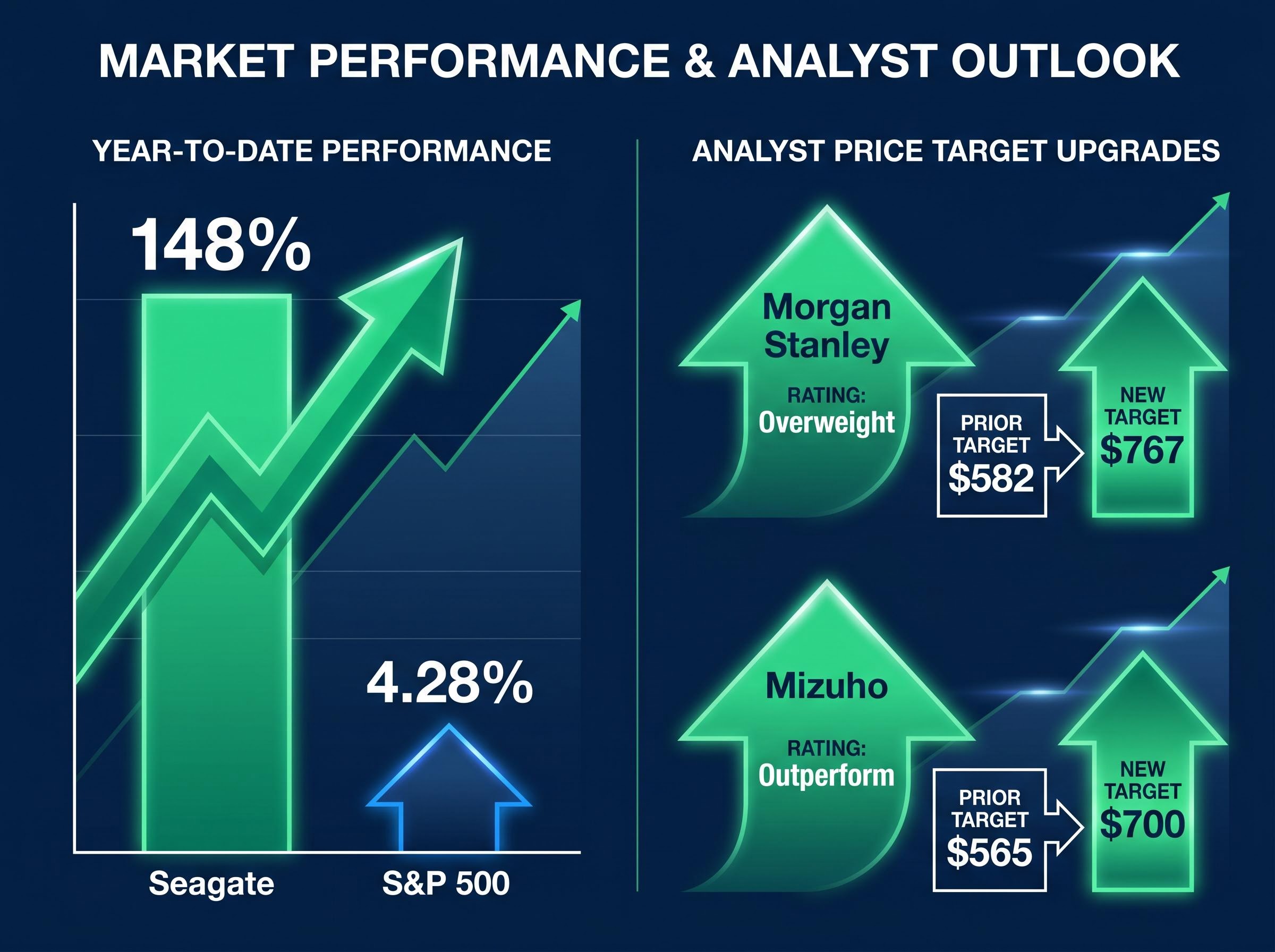

Seagate Technology shares surged more than 18 percent in after-hours trading on 28 April 2026, capping a staggering 148 percent year-to-date climb. The catalyst for this aggressive repricing was a fiscal third-quarter blowout that comprehensively crushed consensus estimates. This immediate market response proves that the artificial intelligence boom is finally delivering material revenue to physical hardware vendors.

Investors watching the Seagate stock price target revisions from major investment banks are witnessing a fundamental reassessment of the company’s earning power. This article breaks down the dual analyst upgrades from Wedbush and Bank of America that followed the earnings release. It dissects the underlying financial metrics driving the massive rally and unpacks the mechanics of nearline storage.

By examining these structural shifts, the analysis reveals why Wall Street believes this hard drive supercycle is only just beginning.

The sheer momentum of the stock triggered an immediate response from institutional analysts on 29 April 2026. Morgan Stanley and Mizuho issued rapid upward revisions to their valuations, cementing a new pricing floor for the data storage giant. Before the earnings drop, the stock closed at $579.03 on Tuesday.

Following the massive 18 percent after-hours pop, shares pushed aggressively toward the $680 to $690 intraday range as markets opened on Wednesday. This explosion in value places the stock’s year-to-date gain at approximately 148 percent. To contextualise the scale of this rally, the broader S&P 500 benchmark has returned just 4.28 percent over the same period.

This aggressive institutional repricing mirrors the upside momentum seen in recent telecom AI infrastructure valuations, where major US providers are similarly outperforming baseline market expectations following strong first-quarter earnings beats.

The aggressive overnight upgrades signal that top-tier analysts view the previous trading levels as significantly undervalued. Readers can immediately grasp how institutional sentiment has shifted overnight, driven by real-world infrastructure spending.

| Firm | Prior Target | New Target | Rating |

|---|---|---|---|

| Morgan Stanley | $582 | $767 | Overweight |

| Mizuho | $565 | $700 | Outperform |

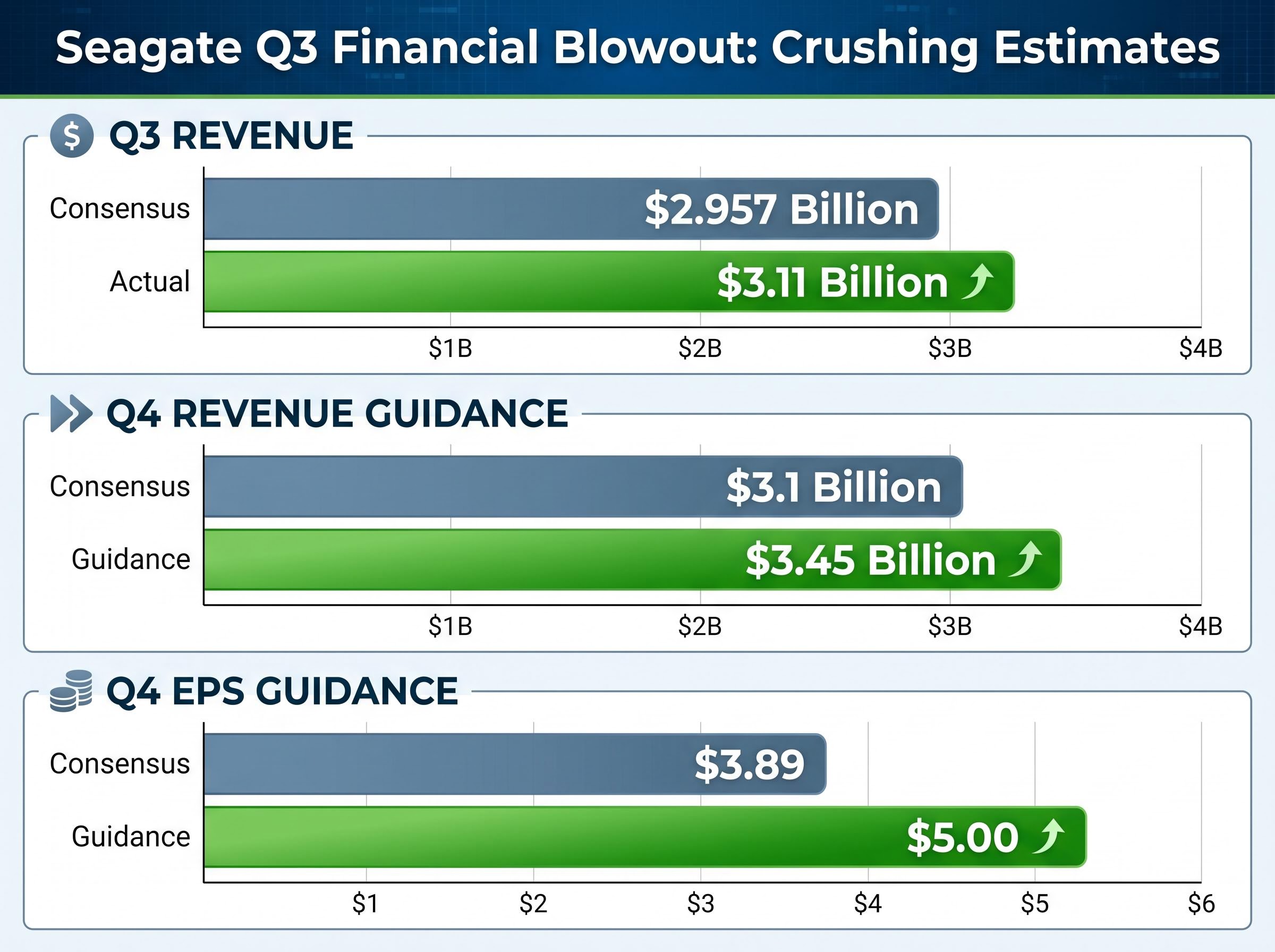

This historic stock surge is anchored by fundamental financial execution, serving as a total vindication of recent market optimism. The company reported fiscal Q3 revenue of $3.11 billion, representing a massive 44 percent year-over-year increase. This top-line result comfortably beat the Wall Street consensus of $2.957 billion, proving that customer demand is accelerating across all major geographic regions.

The profitability metrics proved even more remarkable than the revenue growth. Seagate achieved a record non-GAAP gross margin of 47 percent and generated a decade-high free cash flow of $953 million. Non-GAAP diluted earnings per share hit $4.10, silencing lingering concerns about the sustainability of hardware margins.

The company’s fiscal third quarter financial results confirm that the manufacturer successfully translated raw infrastructure demand into exceptional cash generation and record-setting margins.

Forward guidance for the June quarter indicates management expects this momentum to accelerate rather than plateau. The company projected Q4 revenue of $3.45 billion alongside $5.00 in earnings per share, substantially above prior estimates.

| Financial Metric | Wall Street Consensus | Actual Reported / Guidance |

|---|---|---|

| Q3 Revenue | $2.957 billion | $3.11 billion |

| Q3 Free Cash Flow | Not specified | $953 million |

| Q4 Revenue Guidance | $3.1 billion | $3.45 billion |

| Q4 EPS Guidance | $3.89 | $5.00 |

The sheer margin of these beats proves that software infrastructure hype is finally translating into tangible cash generation.

The financial screens tell the story of a massive quarter, but the real drivers live on the data centre floor. Every artificial intelligence token generated by language models requires long-term, high-capacity retention. This creates a direct pipeline between rising software usage and the urgent need for physical nearline hard disk drives.

Market analysts are already tracking severe nearline HDD shortages across the industry as hyperscale data centre operators aggressively stockpile physical drives to support their expanding language model deployments.

Nearline storage refers to high-capacity drives that balance fast data retrieval times with massive archiving capabilities, serving as the backbone of modern cloud infrastructure. While solid-state drives dominate the high-speed processing layer, they remain too expensive for bulk archiving. As a result, traditional hard disk drives still account for the majority of all cloud storage demand.

The relentless pace of data creation means cloud hyperscalers cannot risk falling behind on physical storage infrastructure. Morgan Stanley observed that new artificial intelligence use cases are fundamentally accelerating the global pace of data creation. This dynamic has pushed infrastructure buyers to secure capacity well in advance.

Seagate reported that its nearline manufacturing capacity is completely booked through calendar year 2026. This extraordinary backlog explains why a legacy hardware provider has suddenly found itself at the absolute centre of the modern technology infrastructure boom.

Wall Street is now looking far beyond the current quarter, constructing euphoric future projections for calendar year 2027. The mechanics behind the newly established $767 base target from Morgan Stanley highlight a mathematical ceiling that retail investors must understand.

The most striking revelation from the firm’s coverage is that its previous bull scenario has transitioned into its baseline outlook for the third straight quarter. This sustained upward pressure demonstrates a massive gap between top-tier analytical models and broader Street consensus.

The firm models two distinct scenarios for the stock: Base Case: Projects calendar year 2027 earnings per share of $42.59, sitting 132 percent above broader consensus, applying an 18x price-to-earnings multiple. Bull Case: Establishes a massive valuation ceiling, assuming a multiple on an earnings per share estimate.

These projections show investors the specific earnings multiples required to push the stock into four-digit territory over the next eighteen months.

This remarkable profitability surge is protected by a structural shift in industry power, driven by disciplined supply mechanics. A highly concentrated group of hard disk drive suppliers is actively managing output to prevent the inventory gluts that plagued previous hardware cycles. This discipline has shifted pricing leverage firmly away from enterprise buyers and back to the hardware producers.

The tangible result of this control appeared in the first quarter of 2026, when the cost per terabyte for hard disk drives rose quarter-over-quarter. This price increase significantly exceeded the anticipated 1 percent baseline that analysts had modelled. These supply mechanics are structurally extending the duration of the current upcycle.

“The highly consolidated hard drive sector is maintaining strict production discipline, ensuring that record gross margins are protected by a structural supply shortfall rather than temporary demand spikes,” according to industry analysis.

Because pricing, gross margins, and earnings power have consistently surpassed above-consensus forecasts, investors are gaining confidence in the longevity of these returns.

For readers wanting to understand the broader ecosystem of hardware constraints, our deep-dive into AI infrastructure throughput limitations explores how emerging commercial platforms are targeting the specific latency bottlenecks that could affect future margin profiles.

The extraordinary performance of Seagate Technology validates a broader structural shift in information technology hardware economics. With forward capacity fully booked through 2026 and pricing leverage firmly in hand, the company has officially transitioned from a cyclical hardware play to a primary artificial intelligence infrastructure provider. This breakout fundamentally redefines how markets will value data retention assets going forward.

This physical hardware dominance creates a foundation for higher-level enterprise agentic coordination frameworks, which require massive underlying data retention to reliably automate complex workflows across business operations.

Upcoming earnings reports from competitors across the supply chain will likely be judged against this aggressive new baseline. The hardware sector is no longer a laggard in the technology ecosystem, but a primary beneficiary of unprecedented capital expenditure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Seagate Technology's stock surged due to a fiscal third-quarter earnings blowout that crushed consensus estimates, demonstrating material revenue generation from the artificial intelligence boom for hardware vendors.

Following the earnings release, Morgan Stanley upgraded Seagate's target to $767 and Mizuho raised its target to $700, both issuing positive ratings.

The AI boom is significantly increasing demand for nearline hard disk drives, which are essential for long-term, high-capacity data retention required by language models, leading to HDD shortages and Seagate's capacity being booked through 2026.

Seagate reported Q3 revenue of $3.11 billion, a 44 percent year-over-year increase, achieved a record non-GAAP gross margin of 47 percent, and generated a decade-high free cash flow of $953 million.