Xero Posts 31% Revenue Jump Despite 53% Share Price Drop

4 hrs ago

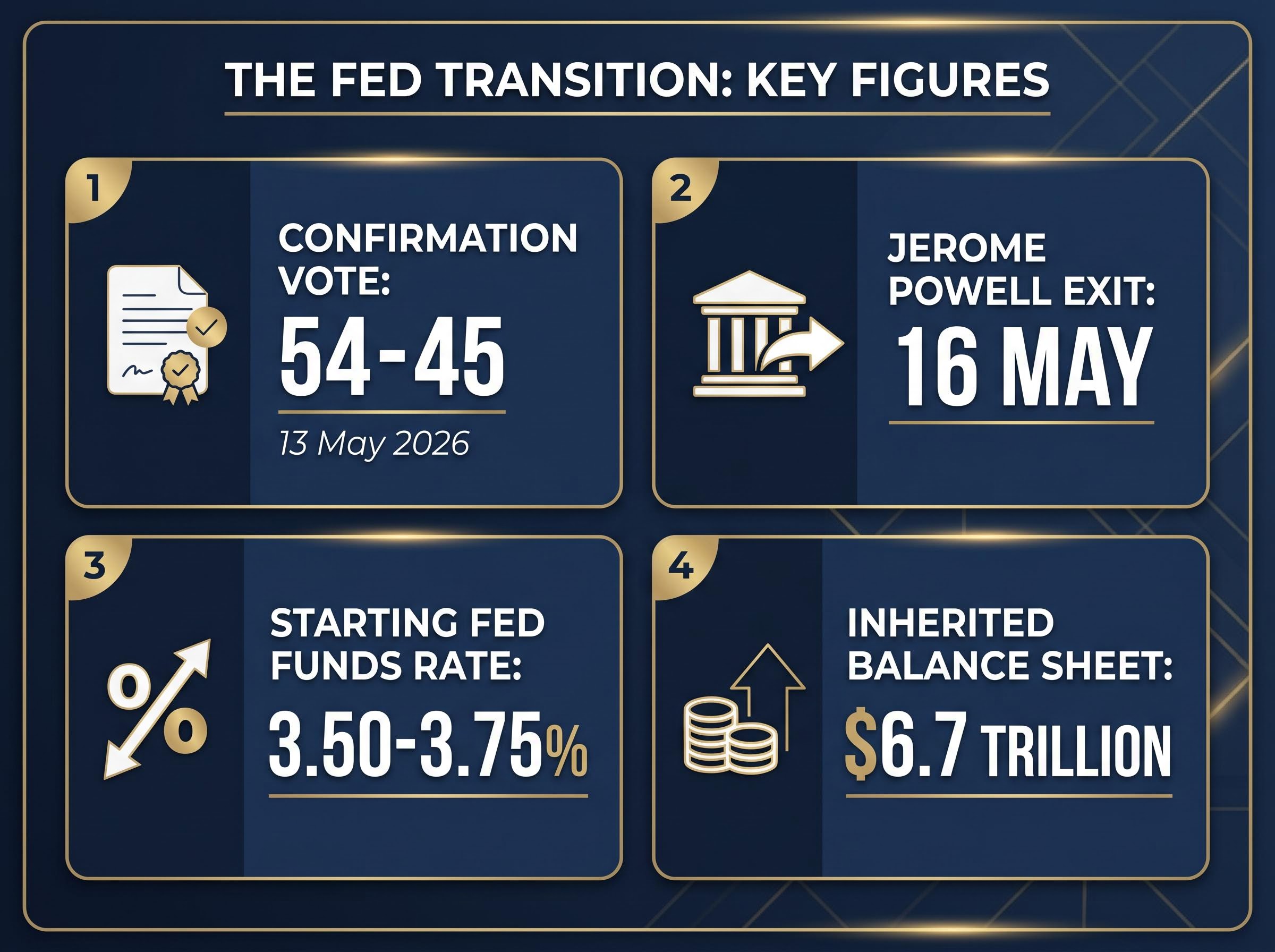

The United States Senate confirmed Kevin Warsh as the next Federal Reserve Chair on 13 May 2026 by a 54-45 vote, the narrowest margin ever recorded for the position, as wholesale inflation surged to its highest annual pace since December 2022 and the Strait of Hormuz remained closed to commercial shipping. Warsh inherits the central bank from Jerome Powell, whose chair term ends 16 May, along with a $6.7 trillion balance sheet, a federal funds rate of 3.50-3.75%, and an economy contending with energy-driven price acceleration. The modal market expectation has shifted from multiple rate cuts to “on hold,” with some futures contracts now pricing a non-trivial probability of a hike. What follows is an examination of what Warsh’s confirmation means for interest rates, the Fed’s independence, and how investors across equities, bonds, and rate-sensitive assets should position in the weeks ahead.

The 54-45 result is not just narrow. It is the slimmest confirmation margin for a Fed chair in the institution’s history, with only a single Democratic senator crossing party lines. The Senate Banking Committee hearing on 21 April 2026 had already signalled the partisan fault lines, but the near-party-line final vote converts those fault lines into a structural constraint on Warsh’s institutional authority.

Jerome Powell steps aside on 16 May but remains on the Fed’s Board of Governors. He is expected to maintain a reduced public presence, reflecting concerns about preserving the perception of central bank autonomy during the transition.

The bond market repricing that preceded the confirmation vote was itself a policy signal: the 10-year Treasury yield reached 4.42% on 13 May 2026, its highest level since June 2025, as investors began marking down duration assets before Warsh had cast a single vote as chair.

The political context is impossible to separate from the policy one. President Trump’s own remarks have framed the appointment in transactional terms:

“Anybody that disagrees with me will never be Fed chairman.” Trump also predicted that rates will drop “when Kevin gets in.”

That framing, paired with the thinnest confirmation margin on record, means Warsh enters office with limited bipartisan mandate at a moment when the Fed’s credibility is its most valuable asset.

Warsh’s 21 April 2026 testimony before the Senate Banking Committee remains the only verified baseline for assessing his policy intentions. In that hearing, he anchored his position on three points: the dual mandate, institutional independence, and the current state of the Fed’s balance sheet and inflation record.

On independence, his language was unequivocal:

“I’m committed to ensuring that the conduct of monetary policy remains strictly independent.”

He framed his obligation as running to “the law and the public,” not to the president, and addressed the question of private pressure directly:

“The president never once asked me to commit to any particular interest rate decision, period. Nor would I agree to do so if he had.”

Politico reported on 11 May 2026 that Warsh “has generally called for lowering interest rates” but has not committed to doing so. The distinction matters. His stated preference for rate-based tools over balance-sheet expansion is a philosophical stance about how the Fed should operate, not a forward commitment on the direction of the next move. He characterised the Fed he is inheriting as “confronting serious uncertainty, an overextended balance sheet, a poor record on inflation,” a framing that suggests caution rather than urgency to ease.

Investors reading market commentary through Warsh’s actual statements, rather than through Trump’s public remarks, will find a more reliable signal for anticipating Fed behaviour.

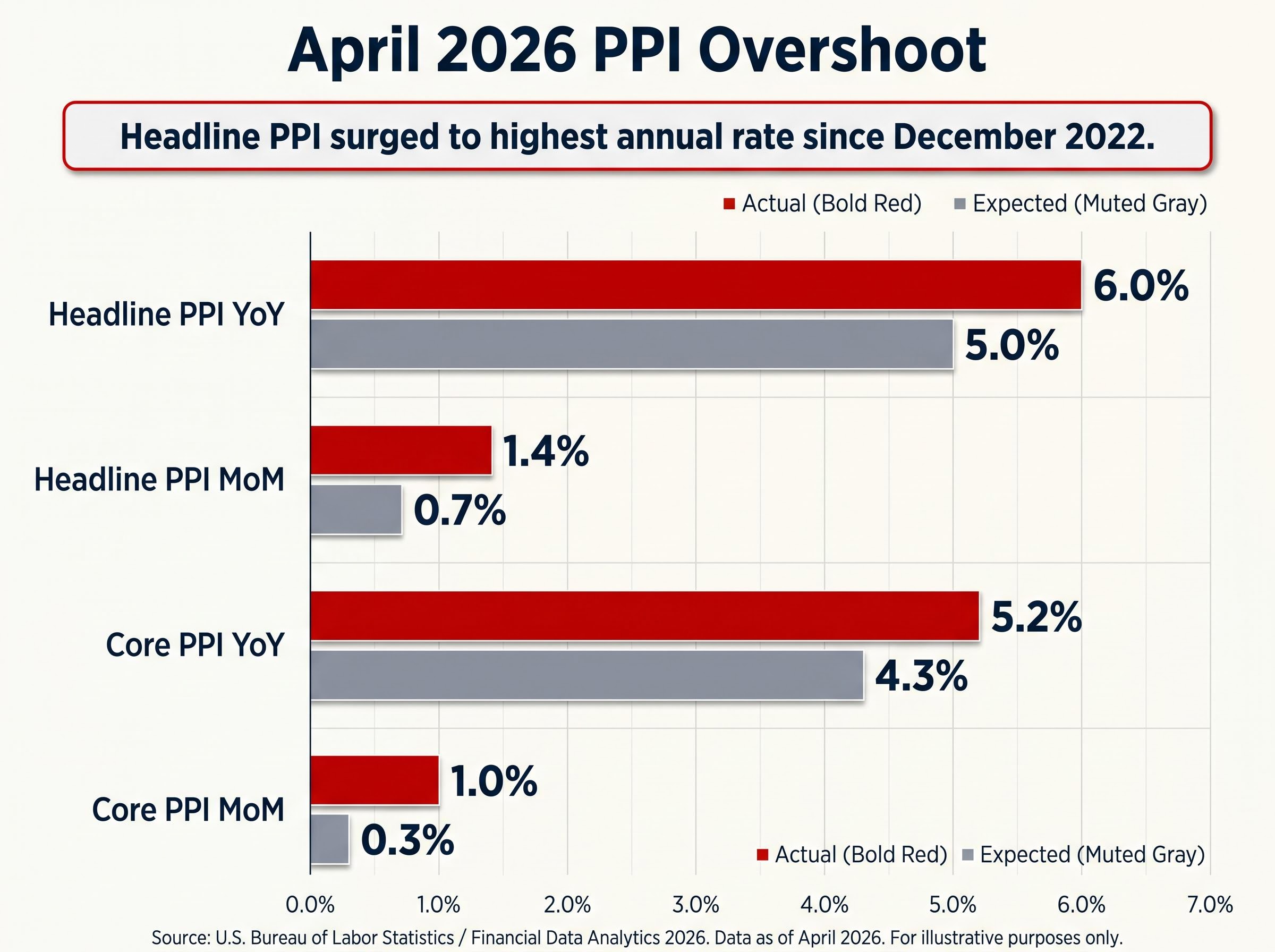

The ground shifted before Warsh was even sworn in. The April 2026 Producer Price Index (PPI) report landed as the most consequential inflation data point of the year, driven by energy prices tied to the Iran conflict and the continued closure of the Strait of Hormuz.

The headline PPI surged to 6.0% year-on-year, the highest annual rate since December 2022.

| Metric | Actual (MoM) | Expected (MoM) | Actual (YoY) | Expected (YoY) |

|---|---|---|---|---|

| Headline PPI | 1.4% | 0.7% | 6.0% | 5.0% |

| Core PPI | 1.0% | 0.3% | 5.2% | 4.3% |

| Energy (goods) | 7.8% | — | — | — |

| Services | 1.2% | — | — | — |

Final demand energy prices rose 7.8% month-on-month, with gasoline alone climbing 15.6%. Services PPI increased 1.2% month-on-month, the largest gain since March 2022. The breadth of the overshoot, across both goods and services, makes it difficult to dismiss as a narrow supply shock.

Corporate margin absorption has so far acted as a buffer between upstream energy costs and consumer prices, with major consumer goods companies compressing gross margins rather than raising shelf prices at the pace that would be required to fully pass through an 11% aggregate petrochemical cost increase, which is why the CPI print arriving before Warsh’s first FOMC meeting may not yet reflect the full inflationary force of the PPI overshoot.

Fed funds futures now price a roughly 99% probability of no change at the next meeting, with less than one full 25-basis-point move in either direction implied by December 2026. Before the April print, markets had priced 2-3 cuts by year-end. That expectation has been marked down sharply.

Warsh has not directly commented on the April PPI data. His hearing characterisation of the Fed’s “poor record on inflation” suggests he will be reluctant to wave it away. Investors pricing in early cuts are now betting against both the data and the new chair’s stated aversion to repeating that record.

The Fed’s $6.7 trillion balance sheet represents the accumulated residue of multiple rounds of quantitative easing (QE), the process by which the central bank purchased Treasury bonds and mortgage-backed securities (MBS) to push down long-term interest rates and inject liquidity into financial markets. The balance sheet grew sharply during the 2020 pandemic response and has been shrinking gradually since through a process called “runoff,” where the Fed allows maturing bonds to expire without replacing them.

Warsh regards this balance sheet as a problem. During his prior service as a Fed Governor from 2006 to 2011, he was a consistent critic of QE and balance-sheet expansion. His preference is for the Fed to use interest-rate adjustments as its primary tool and to let the balance sheet shrink passively over time, restoring policy flexibility for future crises.

The distinction matters for investors. A rate decision affects the cost of borrowing across the economy immediately. Balance-sheet runoff operates more slowly but directly influences the supply-demand balance for Treasury bonds and MBS, which in turn affects long-term yields and mortgage rates.

As of mid-May 2026, there is no published timetable or numerical target from Warsh for balance-sheet reduction. Analyst expectations converge on three points:

For bond investors in particular, the implication is mildly bearish for intermediate-to-long-term Treasuries. A leaner Fed footprint, combined with large net Treasury issuance to fund fiscal deficits, puts upward pressure on term premiums and long-term yields, even without a rate hike.

Warsh has denied any private commitment to the White House on rates. His “strictly independent” language is on the record. The question is whether formal pledges resolve the structural risk created by the president’s public commentary.

Trump told supporters that rates will drop “when Kevin gets in.”

Sen. Elizabeth Warren called Warsh a “sock puppet” during the confirmation process. Warsh’s standard independence language does not, by itself, remove the concern Warren articulated, because the risk is not about a single decision.

An anonymous former Fed governor quoted by Bloomberg said Warsh “is not likely to overtly subordinate policy decisions to the White House.” The same piece cautioned that “the risk is that the Fed’s reaction function becomes more politically sensitive over time.” Academic economists cited by the Wall Street Journal and the Financial Times in the days before the vote echoed the concern: if Warsh delivers cuts while PPI sits at 6.0% year-on-year and CPI has yet to roll over, markets may interpret it as political accommodation regardless of his stated reasoning.

FOMC dissent dynamics were already fracturing the committee Warsh inherits before his confirmation: the April 29 rate decision produced a historic four-way split, with hawks outnumbering the lone dovish dissenter three to one, and a PCE reading of 3.5% against a 2% target creating a genuine dual-mandate conflict that no single chair can resolve through communication alone.

“The Fed’s institutional independence can survive one chairman; the bigger question is whether Warsh pushes back publicly if Trump continues to pre-announce rate cuts for him,” one CNBC strategist noted on the day of the confirmation.

The concern is partly unquantifiable, which is exactly why it carries weight. A future easing decision, if it arrives while inflation remains elevated, could trigger a credibility-driven yield spike. That tail risk is now embedded in the backdrop, even if it cannot be assigned a precise probability.

The base case is straightforward: on hold through at least the next two to three FOMC meetings, with the Fed watching for CPI confirmation of the PPI trend and any evidence that the Iran-driven energy shock is becoming entrenched in broader prices.

The two tail scenarios define the range of outcomes:

Two-year Treasury yields rose modestly after the confirmation vote, consistent with higher-for-longer repricing.

Investors wanting granular detail on how the major banks have shifted their forecasts will find our full explainer on the Wall Street rate-cut timeline, which covers Goldman Sachs pushing its first expected cut to December 2026 and Bank of America eliminating both 2026 cuts entirely and rescheduling them to the July-September 2027 window, along with the specific PCE and unemployment thresholds each bank is using as trigger conditions.

The specific data points and events to monitor in the weeks ahead:

For equity investors, rate-sensitive sectors face continued pressure under the on-hold or hike scenarios. Bond investors should watch term premiums on longer Treasuries, particularly as balance-sheet runoff continues alongside elevated government issuance. Both groups need to track the specific dates and data points above to determine when the calculus shifts.

The tension Warsh must navigate is structurally unresolvable in the near term. Markets want cuts. The president is demanding them publicly. The inflation data gives Warsh no cover to deliver them without risking a credibility-destroying read as political capitulation.

The two most reliable signals available to investors are Warsh’s confirmed independence pledge and his hawkish record on balance-sheet policy. His actions, not Trump’s commentary, will determine the Fed’s trajectory.

The first genuine test arrives soon. How Warsh handles his initial public remarks as chair, and whether he addresses the April PPI directly, will indicate whether the institutional firewall holds. Investors should weight those remarks heavily when they come.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Kevin Warsh is the newly confirmed Federal Reserve Chair, having previously served as a Fed Governor from 2006 to 2011, where he was a consistent critic of quantitative easing and balance-sheet expansion. He was confirmed by the Senate on 13 May 2026 by a 54-45 vote, the narrowest margin ever recorded for the position.

During his Senate Banking Committee hearing on 21 April 2026, Warsh stated he is committed to ensuring monetary policy remains strictly independent, adding that President Trump never asked him to commit to any particular interest rate decision and that he would not have agreed to do so if asked.

The April 2026 Producer Price Index came in at 6.0% year-on-year, the highest since December 2022, driven largely by energy prices linked to the closure of the Strait of Hormuz. Fed funds futures now price roughly a 99% probability of no change at the next FOMC meeting, with markets having previously priced 2-3 rate cuts by year-end 2026.

Warsh favours using interest-rate adjustments as the Fed's primary tool and allowing the 6.7 trillion dollar balance sheet to shrink passively through continued runoff. For bond investors, this creates mild bearish pressure on intermediate-to-long-term Treasuries, as a leaner Fed footprint combined with large government issuance puts upward pressure on term premiums and long-term yields.

Rate-sensitive equity sectors, particularly real estate investment trusts and utilities, face the greatest pressure if rates remain on hold or rise further. Bond investors should monitor term premiums on longer-dated Treasuries, especially as balance-sheet runoff continues alongside elevated government debt issuance.