SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

7 hrs ago

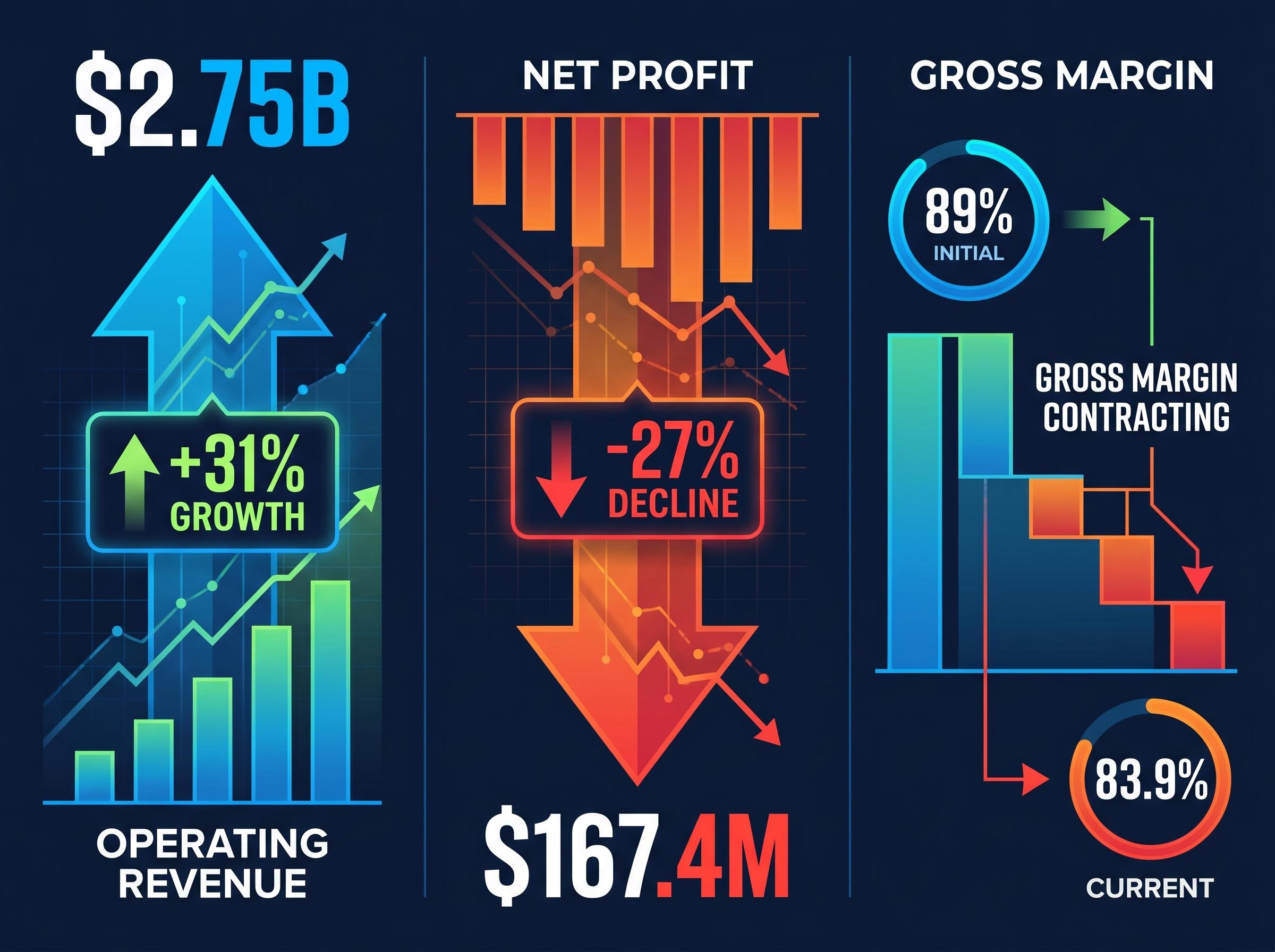

Xero posted 31% revenue growth to $2.75 billion in FY26, but net profit fell 27% to $167.4 million on the same day its share price was already down approximately 53% over the preceding 12 months. That divergence sits at the centre of today’s full-year results, released on the ASX on 14 May 2026. The Melio acquisition, completed in October 2025 for US$2.5 billion, has reshaped the company’s cost structure, inflating headline revenue while simultaneously compressing margins. The result is a set of numbers that can be read as either a growth inflection or a profitability warning, depending on where the reader looks. This article breaks down the key metrics, explains what Melio’s contribution means for the underlying business, and sets out what FY27 guidance and the FY28 revenue doubling target signal about the path ahead for ASX investors.

Operating revenue of $2.75 billion, up 31%. Net profit of $167.4 million, down 27%. Those two figures sit side by side in the same reporting period, and the gap between them is not a contradiction; it is the direct consequence of a deliberate strategic decision.

The bridge between those numbers: Gross profit margin contracted from 89% to 83.9% in FY26, the single largest margin compression in Xero’s listed history as a result of integrating Melio’s lower-margin payments revenue into the consolidated accounts.

Beneath the net profit decline, operational cash generation held up. EBITDA rose 18% to $757.3 million, and free cash flow expanded 9% to $554 million. The business is generating more cash than a year ago. It is generating less bottom-line profit.

| Metric | FY25 (implied) | FY26 | Change |

|---|---|---|---|

| Operating Revenue | ~$2.10B | $2.75B | +31% |

| Net Profit | ~$229M | $167.4M | -27% |

| Gross Margin | 89% | 83.9% | -5.1pp |

| EBITDA | ~$641M | $757.3M | +18% |

| Free Cash Flow | ~$508M | $554M | +9% |

For ASX investors parsing a mixed-signal result, the interplay between these metrics determines whether this is a growth company managing a transitional cost phase or one whose profitability trajectory is structurally deteriorating. That distinction drives the valuation debate from here.

A result where revenue grows 31% while net profit falls 27% is precisely the scenario where single-metric investors are most exposed to misreading a stock; different share valuation methods including price-to-sales, EV/EBITDA, and discounted cash flow each weight near-term profitability differently, and the choice of method can produce contradictory conclusions from the same underlying data.

Xero explicitly identified the Melio acquisition as the primary driver of profitability deterioration in FY26. The deal, completed on 15 October 2025 at a price of US$2.5 billion (approximately A$3.9 billion), added accounts payable and bill payment capabilities aimed squarely at the US small business market.

Forbes coverage of the Xero-Melio acquisition rationale highlights Melio’s existing US small business customer base and bank partnerships as the strategic assets Xero was purchasing, not just the payments infrastructure itself, which helps explain why management is willing to absorb near-term margin compression in exchange for an accelerated US market entry.

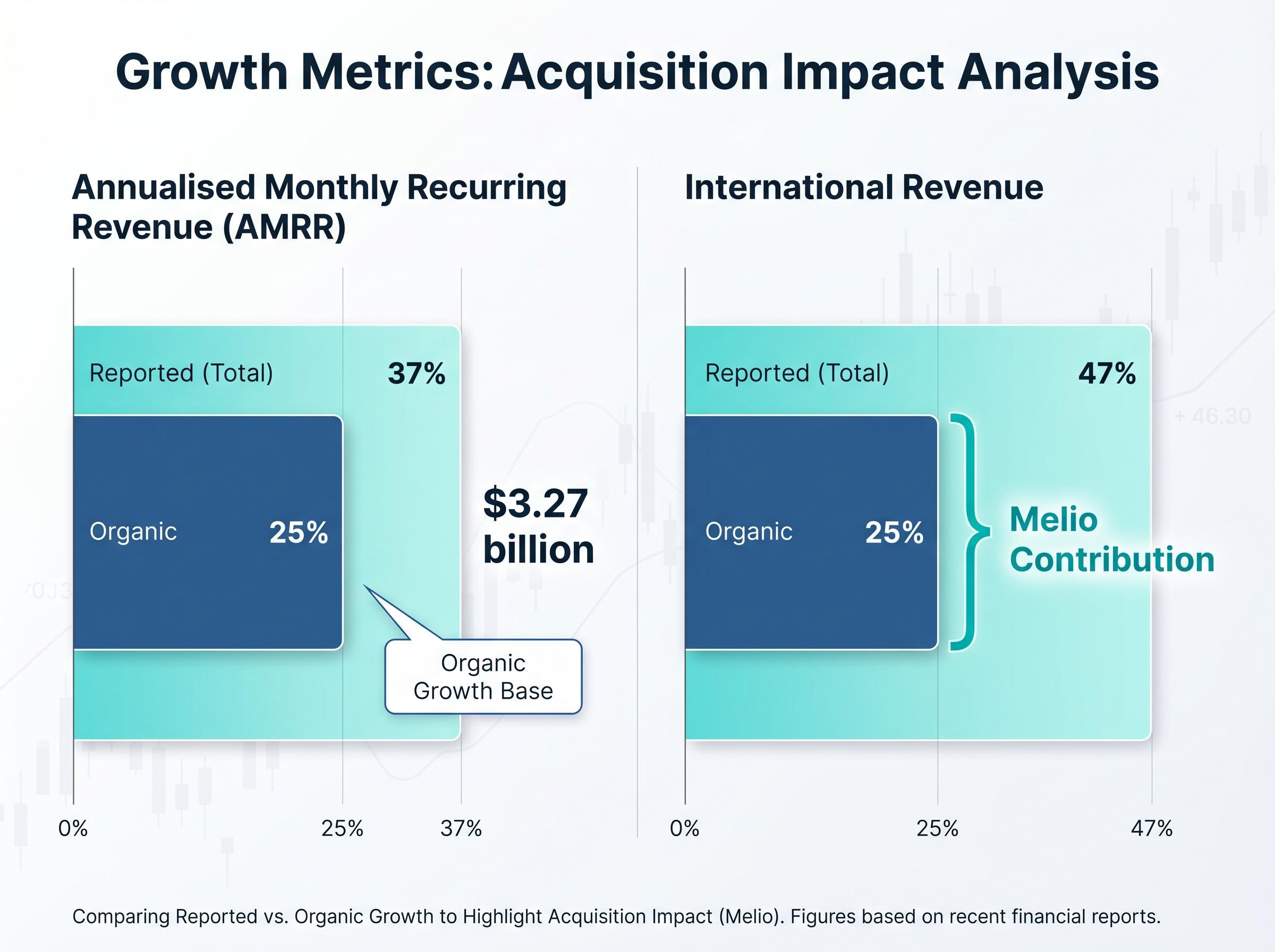

The organic versus reported growth comparison quantifies the acquisition’s contribution:

The gap between those figures, roughly 12 percentage points of AMRR growth, is Melio’s contribution. That is the size of what the acquisition added to the top line. It is also the layer that compressed the margin.

Xero launched bill payment capabilities for US small businesses in March 2026, built on Melio’s infrastructure. This represents the first tangible product return on the US$2.5 billion investment, positioning Xero as a broader financial platform rather than a pure accounting tool in a market long dominated by Intuit’s QuickBooks.

The customer growth story carries genuine substance, even if the margin story is complicated. Total subscribers reached 4.9 million, up 11%, but the cleaner quality metric tells a more interesting story.

Net new subscribers (excluding long-idle removed subscriptions) reached 506,000, up 22%, a sign that the pace of quality additions is accelerating even as headline growth moderates.

Average revenue per customer (ARPC) grew 23% to $55.44, evidence of pricing power and product mix improvement rather than volume expansion alone.

ARPC trajectory and subscriber quality are the leading indicators for whether Xero’s recurring revenue base is strengthening or thinning. Strong ARPC growth alongside accelerating net new additions signals the business is adding valuable customers, not just expanding the count.

Xero’s pre-acquisition model was a high-margin software-as-a-service (SaaS) subscription business. SaaS refers to cloud-based software delivered on a recurring subscription basis, where the marginal cost of serving an additional subscriber is low. That model typically produces gross margins in the high 80s to low 90s per cent.

Payments and bill-pay infrastructure, which is what Melio brings, operates on fundamentally different economics. Three factors explain why:

These costs compress gross margins toward the 70-80% range for payments-integrated businesses. The peer comparison anchors where Xero’s margin is likely heading.

SaaStr’s analysis of payments integration on SaaS margins confirms that adding fintech capabilities to a pure-play software business routinely compresses gross margins by 5-15 percentage points, with interchange and processing costs being the primary culprits, a pattern that maps directly onto Xero’s FY26 gross margin contraction from 89% to 83.9%.

| Company | Gross Margin | Revenue Growth | Business Model |

|---|---|---|---|

| Xero (FY26) | 83.9% | 31% | SaaS + payments (post-Melio) |

| Sage Group (FY2025) | 92.7% | ~7.8% | Primarily subscription SaaS |

| Intuit (Q2 2026) | ~80.9% | ~17% | SaaS + payments-integrated |

Xero is moving from the Sage end of the margin spectrum toward the Intuit end as payments revenue scales. Investors who understand this structural dynamic will interpret future gross margin movements with greater accuracy, distinguishing a permanent business model shift from a temporary integration drag.

Management provided FY27 guidance that frames the near-term trajectory clearly.

FY27 revenue guidance: $3.62 billion to $3.73 billion, with adjusted EBITDA of $860 million to $920 million, implying 13.5% to 21.5% year-on-year EBITDA growth.

Beyond FY27, Xero reiterated its target to double FY25 revenue by FY28, calculated on an organic basis excluding Melio revenue synergies. That makes the organic growth trajectory, not the acquisition-inflated headline, the measure against which management expects to be judged.

The AI layer adds a new variable. XeroForce, currently in invite-only alpha as of May 2026, is the company’s AI agent builder: a natural language tool designed to automate recurring finance and accounting workflows across Xero and third-party applications. The commercial strategy has three components:

Whether the revenue doubling ambition is credible depends on organic growth sustaining, Melio contributing revenue rather than only cost, and AI features beginning to drive ARPC expansion. These statements remain forward-looking and subject to market conditions and company performance.

Investors wanting the granular detail behind the FY28 ambition will find our dedicated guide to Melio’s breakeven path and AI adoption metrics, which examines the H2 FY28 breakeven timeline, the 61% increase in JAX AI engagement over three months, and the enhanced US disclosure framework Xero introduced to address investor transparency concerns.

XRO’s share price was already down approximately 53% over the 12 months prior to today’s announcement. A significant amount of negative sentiment was embedded in the price before a single FY26 figure was published.

Ahead of today’s release, analyst consensus on XRO sat at 11 buy ratings across 13 brokers with an average 12-month price target of A$141.45, implying approximately 69% upside from pre-result price levels, a spread between consensus targets and market pricing that reflected how deeply the selloff had moved the stock below fundamental estimates.

When a stock falls 53% heading into a result, the bar for a positive market reaction is lower. The concept is straightforward: if markets have already priced in substantial deterioration, a result that merely meets lowered expectations, rather than exceeding them, can still trigger a re-rating. The bad news may already be reflected in the share price.

The results contain genuine positives that could support that re-rating if investors interpret the margin contraction as transitional: AMRR at $3.27 billion (up 37%), net new subscribers of 506,000 (up 22%), and ARPC of $55.44 (up 23%).

The market’s live verdict on these numbers will unfold across several sources:

Xero is deliberately investing through its income statement today. Melio acquisition costs, payments infrastructure, and AI development are all flowing through FY26 expenses to build a larger, more diversified revenue base by FY28. The trade-off is real. Long-term investors willing to tolerate margin compression during a build phase may view this as rational capital allocation. Investors expecting profitability alongside growth will remain uncomfortable until margins stabilise.

The FY26 result is not a simple pass or fail. It is a set of deliberate trade-offs by a management team betting that US market penetration and AI-driven ARPC expansion will justify near-term profit sacrifice. Whether that bet pays off is the question FY27 results will begin to answer. The official ASX announcement, Xero’s investor presentation, and the earnings call replay provide the complete picture for those assessing the full detail.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AMRR stands for Annualised Monthly Recurring Revenue, a forward-looking measure of the revenue run-rate generated by current subscribers. For Xero, AMRR reached $3.27 billion in FY26, up 37% reported and 25% organically, making it a key indicator of underlying business momentum beyond the acquisition-inflated headline figures.

Xero's net profit fell 27% to $167.4 million in FY26 primarily because the Melio acquisition, completed in October 2025 for US$2.5 billion, added lower-margin payments revenue that compressed gross margins from 89% to 83.9%, the largest margin contraction in the company's listed history.

Melio is a US-based accounts payable and bill payment platform that Xero acquired in October 2025 for US$2.5 billion (approximately A$3.9 billion), giving Xero access to Melio's US small business customer base and payments infrastructure to compete more directly with Intuit's QuickBooks in the American market.

Xero guided for FY27 revenue of $3.62 billion to $3.73 billion with adjusted EBITDA of $860 million to $920 million, and reiterated a longer-term target to double FY25 revenue on an organic basis by FY28, excluding Melio revenue synergies.

XRO shares were already down approximately 53% in the 12 months before the FY26 announcement, meaning significant negative sentiment was priced in before results were published; analyst consensus ahead of the result sat at 11 buy ratings across 13 brokers with an average 12-month price target of A$141.45, implying around 69% upside from pre-result levels.