Wall Street’s two most prominent rate-cut optimists have quietly abandoned their 2026 easing timelines, a signal that the Federal Reserve’s long-anticipated policy pivot may now be a 2027 story at the earliest. Goldman Sachs and Bank of America, publishing updated forecasts in early May 2026, have each pushed their expected Fed rate cuts significantly later than previously anticipated. Core Personal Consumption Expenditures (PCE) inflation remains at 3.2% year-over-year as of March 2026, well above the Fed’s 2% target, and the April jobs report showed a labour market still too resilient to justify easing. These revisions reflect not just a shift in timing but a recalibration of how long this inflationary episode may persist. What follows is an examination of where Goldman Sachs and Bank of America now expect the first cuts to land, what inflation and labour market conditions are keeping the Fed on hold, what would need to change before cuts become viable, and why Bank of America is assigning a meaningful probability to rate hikes rather than cuts.

How Goldman Sachs and Bank of America rewrote their Fed timelines

Goldman Sachs economist David Mericle moved the bank’s two remaining projected cuts back one quarter each. The revised targets now sit at December 2026 for the first reduction and March 2027 for the second.

Goldman Sachs kept its terminal rate projection unchanged at 3.0%-3.25%, a detail that signals confidence in the destination even as the timeline stretches. Mericle also acknowledged that a scenario in which the Fed makes no further reductions remains plausible if economic conditions stay stable.

Bank of America’s revision was more aggressive. Economist Aditya Bhave eliminated both previously projected 2026 cuts entirely, rescheduling them to the July-September 2027 window. Where Goldman Sachs pushed its timeline by one quarter, Bank of America pushed by roughly a year.

The table below captures the scale of the divergence.

| Institution | Previous first cut | Revised first cut | Terminal rate |

|---|---|---|---|

| Goldman Sachs | Q3 2026 | December 2026 | 3.0%-3.25% |

| Bank of America | H2 2026 | July-September 2027 | Not specified |

These are not marginal tweaks. Both banks have pushed their first anticipated cut by at least two quarters, with Bank of America’s shift representing the most hawkish recalibration among major Wall Street institutions this year.

When big ASX news breaks, our subscribers know first

Why inflation keeps the Fed’s hands tied

The anchor point is straightforward: core PCE sat at 3.2% year-over-year as of March 2026, a full 120 basis points above the Fed’s 2% target. That gap alone keeps rate cuts off the table. The more consequential problem is the direction of travel.

Goldman Sachs’s Mericle projected that annual core PCE will remain closer to 3% than 2% for the entirety of 2026.

Goldman Sachs expects core PCE to stay nearer to 3% than 2% throughout 2026, driven in part by energy cost pass-through effects that have not yet fully filtered into core price readings.

Bank of America’s Bhave reinforced this view, noting that the pricing impact of a recent oil shock has not yet been fully reflected in current inflation data. That means additional upward pressure remains in the pipeline, even before accounting for other structural contributors.

Energy cost pass-through from the Strait of Hormuz closure is the single largest unresolved variable in the near-term inflation picture: Brent crude above $104 per barrel has already transmitted into gasoline at $4.50 per gallon, airfares up 8.2%, and grocery prices up 4.1% year-over-year, and the April CPI print due 12 May is forecast to show headline inflation accelerating further to 3.7%.

Three forces are holding inflation above the Fed’s comfort zone:

- Energy pass-through: Oil shock pricing effects are still filtering into goods and services costs

- Tariff effects: Import tariffs continue to contribute to goods inflation persistence

- Wage growth: Average hourly earnings running above 3.5% year-over-year, sustaining consumption-driven price pressure

Understanding this inflation pipeline matters because it tells investors and households when relief on borrowing costs is realistic. Current readings likely understate near-term price pressure rather than overstate it.

What has to change before the Fed will cut

Goldman Sachs has described two prerequisites for easing, and the economy has not met either one. The conditions function as a sequential checklist rather than a menu of options.

- Dissipation of the oil shock in monthly inflation readings: Energy cost pass-through must fade from core PCE prints before the Fed can treat any decline as sustainable

- Meaningful labour market softening: Unemployment needs to rise or payroll growth needs to slow materially beyond current levels

- Sustained disinflation toward the 2% target: A single improved reading would not be sufficient; the Fed requires a trend

The April 2026 labour market data, released 8 May 2026, illustrates why the second condition remains unmet. Nonfarm payrolls came in at +115,000, below the roughly 140,000 expected, but unemployment held steady at 4.3% and average hourly earnings grew +3.6% year-over-year. The labour market is cooling at the margin, not deteriorating.

The Fed held its policy rate at 3.50%-3.75% at the 28-29 April FOMC meeting. Even officials previously considered accommodative, including Governor Christopher Waller, have shifted toward supporting a prolonged hold, citing upside inflation risks. The internal threshold for cuts has risen.

The FOMC committee fracture runs deeper than the public hold decision suggests: the 8-4 dissenting vote was the largest since 1992, with dissenters pulling in opposite directions simultaneously, one member seeking an immediate cut while three others pushed for hike signalling to be added to the statement.

Approximately 55% of major forecasters now predict no 2026 cuts, up from 50% in April 2026. The consensus is moving in one direction, and it is not toward easing.

Knowing these specific conditions gives readers a practical framework for monitoring when the policy calculus might shift, rather than waiting for a surprise announcement.

The rate hike tail risk Wall Street is not ignoring

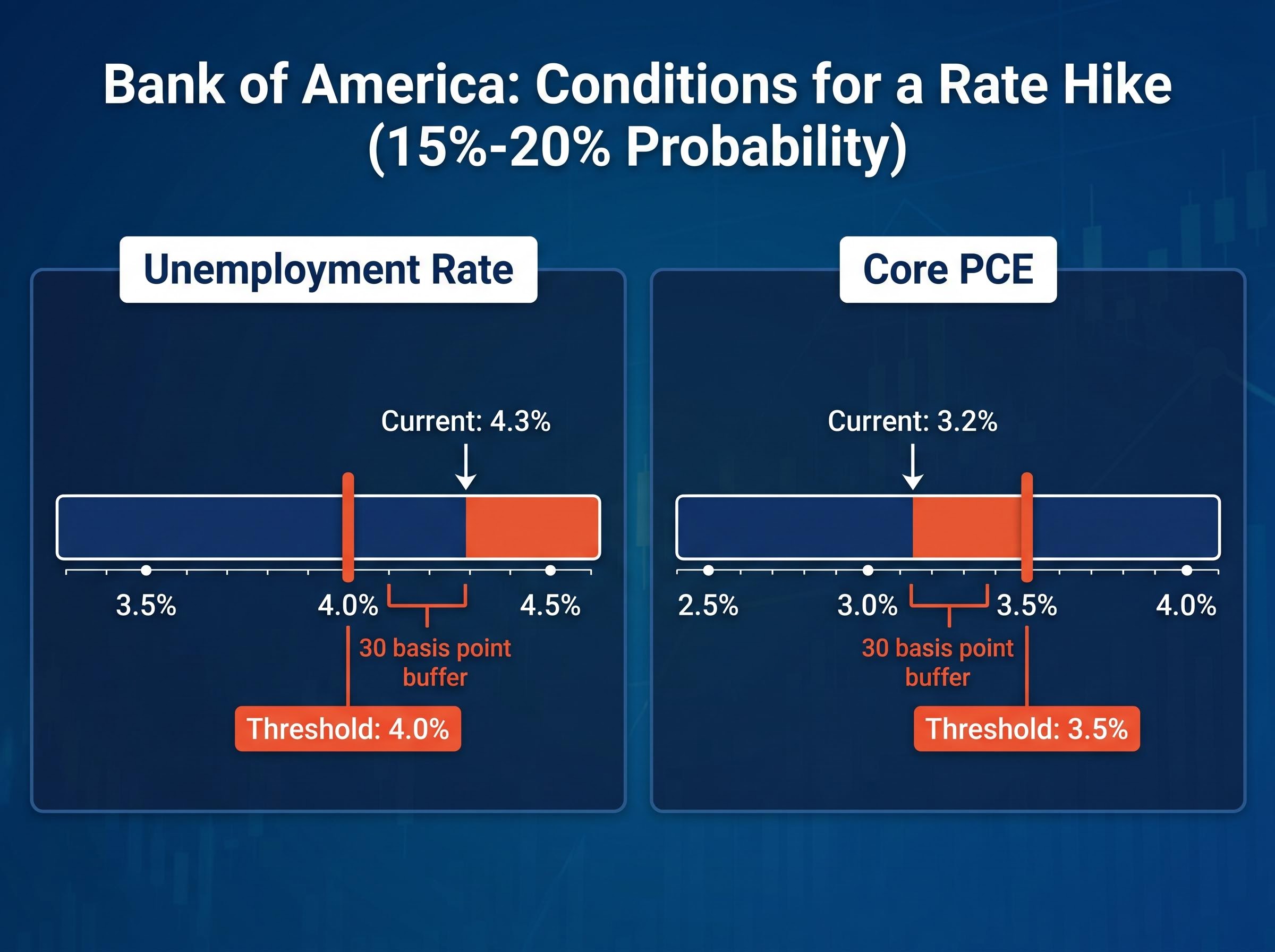

Bank of America is not just delaying its cut forecast. Bhave has assigned a 15%-20% probability to rate hikes, a figure that warrants attention rather than dismissal.

Bank of America analyst Aditya Bhave estimates a 15%-20% probability that the Fed’s next move is a rate hike rather than a cut, framing any such increase as an unwinding of a portion of the 2025 rate reductions rather than the start of a new tightening cycle.

Two trigger conditions would need to converge for hikes to materialise:

- Unemployment falling to 4.0% or below: Currently at 4.3%, leaving a 30 basis point buffer before the threshold

- Core PCE approaching 3.5%: Currently at 3.2%, leaving a 30 basis point buffer before the threshold

Neither buffer is large. A single strong payrolls report combined with an upside inflation surprise from energy pass-through could compress both gaps simultaneously.

A one-in-five chance of rate hikes is not a negligible tail risk. Investors with rate-sensitive positions, including fixed income allocations and floating-rate exposure, should understand the asymmetric scenario Bank of America is pricing in. The downside is not just “cuts take longer.” It is “cuts may not come at all.”

The next major ASX story will hit our subscribers first

Where Wall Street stands as a whole: a market divided on timing

Goldman Sachs and Bank of America are not outliers. They sit within a broader Wall Street consensus that has tilted decisively hawkish, though genuine disagreement persists at the margins.

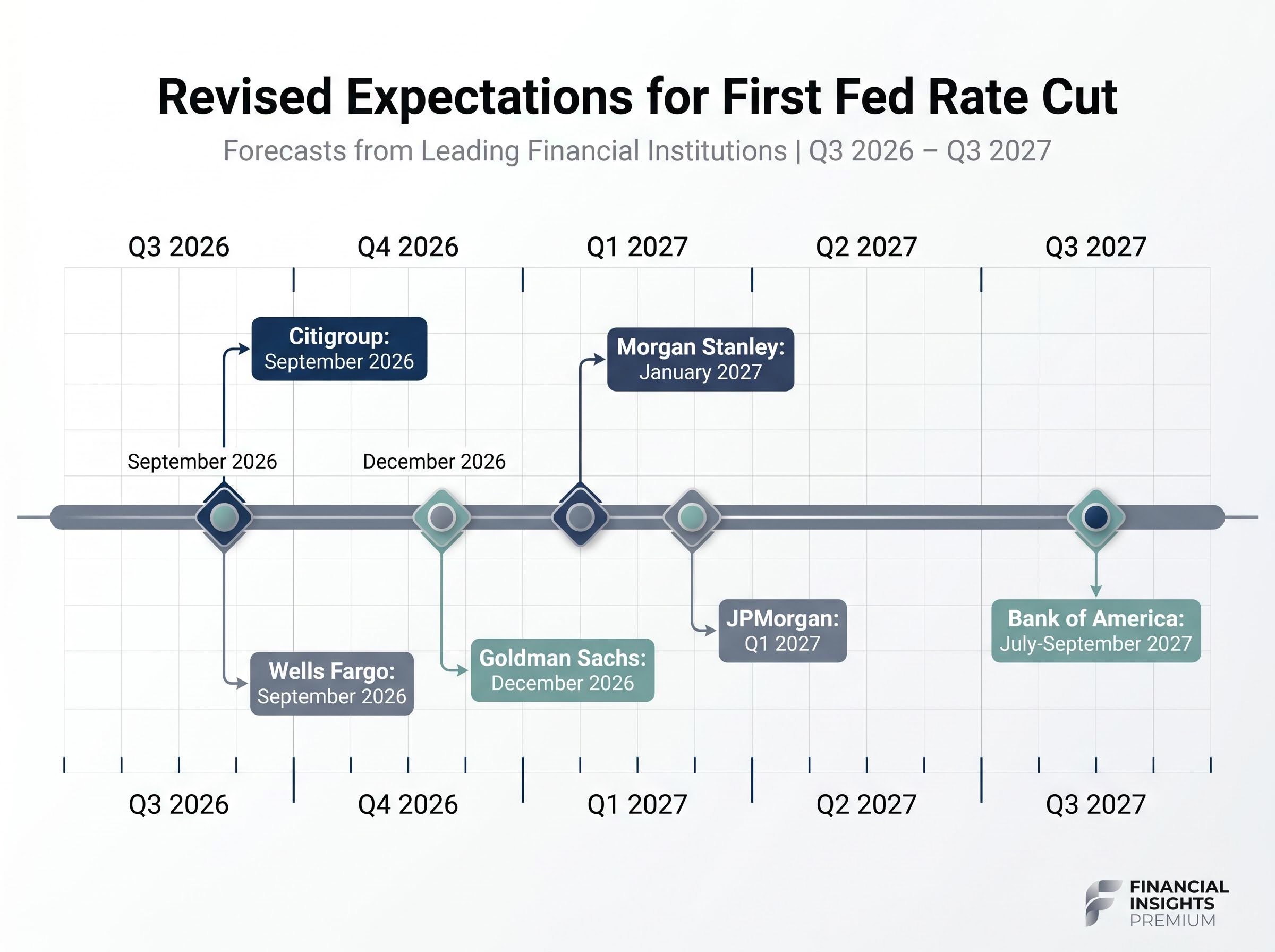

The hawkish bloc, led by JPMorgan, BNP Paribas, HSBC, and RBC, sees no cuts in 2026. JPMorgan expects the first reduction in Q1 2027 with a terminal rate of approximately 3.5%. Morgan Stanley sits nearby, targeting January 2027 for the first cut followed by a second in March 2027.

On the dovish end, Citigroup remains the primary outlier, holding to two 50 basis point cuts in 2026 (September and December) with a terminal rate of 3.25%. Wells Fargo occupies a middle ground, projecting a first 25 basis point cut in September 2026, revised from an earlier Q2 2026 view following the April payrolls data.

| Institution | First cut expected | Terminal rate |

|---|---|---|

| JPMorgan | Q1 2027 | ~3.5% |

| Goldman Sachs | December 2026 | 3.0%-3.25% |

| Morgan Stanley | January 2027 | Not specified |

| Citigroup | September 2026 | 3.25% |

| Wells Fargo | September 2026 | Not specified |

Roughly 55% of major forecasters now anticipate no cuts in 2026, up from 50% in April. Citigroup’s dovish position has not attracted meaningful institutional support; it represents a minority view that would require a sharp deterioration in labour market conditions to materialise.

Forward guidance reliability has become a genuine concern: with four dissents fracturing the committee and Jerome Powell remaining on the board as a governor after his chair tenure ends on 15 May, Kevin Warsh inherits an institution where building a new policy consensus is structurally harder than it has been at any point in the modern Fed era.

The 2% target is a 2027 problem, and markets are starting to accept it

The convergence of Wall Street hawks and mainstream banks around a 2027 easing scenario reflects a structural reassessment, not a temporary scheduling delay. Core PCE at 3.2%, an oil shock still filtering through to prices, and a labour market that refuses to soften have collectively pushed the Fed’s 2% target further out of reach than most forecasters anticipated even three months ago.

Borrowing costs, credit conditions, and rate-sensitive assets face a longer holding period than current pricing may reflect. Bank of America’s 15%-20% hike tail risk adds an asymmetric dimension that fixed income and floating-rate portfolios cannot afford to ignore. The policy pivot is coming; the question is whether it arrives in 2027 or not at all.

For investors tracking the specific events that could shift the 2027 easing timeline earlier or push it further out, our deep-dive into the three catalysts converging this week examines the April CPI print, the Powell-to-Warsh handover on 15 May, and the Trump-Xi Beijing summit, covering how each outcome maps to a different rate path scenario through 2027.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections are subject to market conditions and various risk factors.