Cook Warns Memory Costs Will Force Apple Price Increases in 2026

1 hr ago

Starbucks shares climbed nearly 6% after the company reported Q2 fiscal 2026 earnings on 28 April 2026, but the single-quarter beat is not where the real story lives. The more consequential development for long-term investors is what Evercore and Wolfe Research now project for earnings per share between now and fiscal 2028. Both firms raised their multi-year estimates following the Q2 results, and their projections diverge in magnitude while converging on the same structural thesis: margin flow-through from Starbucks’ turnaround is only beginning, and the largest gains remain ahead. With SBUX trading at $98.67 and the consensus target sitting at $102.16, near-term upside looks modest. The FY27-FY28 estimates tell a different story. What follows is an analysis of what each firm is projecting, why the FY27 margin inflection is the variable that matters most, and how investors should weigh the growth case against the macro and competitive risks that remain unresolved.

The Q2 beat was not close. Starbucks reported earnings per share of $0.50 against an estimate of $0.43, a 16% outperformance on the bottom line. Revenue came in at $9.53 billion versus the $9.16 billion consensus, and the stock responded with an after-hours move of approximately 5-6%, pushing shares to $98.67 as of 29 April 2026.

| Metric | Reported | Estimate |

|---|---|---|

| Q2 EPS | $0.50 | $0.43 |

| Q2 Revenue | $9.53B | $9.16B |

| FY26 Comp Sales Guidance | Above 5% | Prior: Above 3% |

| FY26 EPS Guidance | $2.25-$2.45 | Prior: $2.15-$2.40 |

Management raised FY26 guidance on both comparable sales and earnings. The comparable sales target moved to above 5% from above 3%, a revision attributed to a combination of operational improvements, product innovation, and early returns from the March 2026 loyalty programme overhaul.

U.S. comparable store sales grew 7% in Q2, the strongest result in roughly three years, with positive traffic growth recorded for a second consecutive quarter, providing the demand-side foundation that makes the analyst margin projections credible rather than speculative.

Comparable sales guidance upgrade: FY26 target raised to above 5%, up from above 3%, reflecting broad-based turnaround progress rather than a single driver.

The EPS guidance range widened upward to $2.25-$2.45 from $2.15-$2.40. These are the numbers that anchor the discussion. What Evercore and Wolfe Research did next is project where that earnings trajectory goes over the following two fiscal years.

Evercore’s revised estimates build a three-year staircase that accelerates meaningfully in FY27. The firm raised its FY26 EPS estimate to $2.45 from $2.30, a 6.5% upward revision that largely reflects the Q2 beat and raised guidance. The more telling revisions sit further out.

| Fiscal Year | Prior Estimate | Revised Estimate | Change |

|---|---|---|---|

| FY26 | $2.30 | $2.45 | +6.5% |

| FY27 | $3.09 | $3.25 | +5.2% |

| FY28 | $3.92 | $4.00 | +2.0% |

The FY27 estimate of $3.25 represents a 33% year-on-year increase from FY26, and the mechanics behind that jump are specific. Evercore has identified three conditions converging in FY27: labour reinvestment costs from the turnaround period rolling off, moderation in coffee-related input inflation, and the accumulation of productivity savings from the company’s $2 billion efficiency programme targeted through FY28.

The single data point that crystallises this thesis is the incremental North America margin projection.

Incremental North America margins: Evercore projects these will exceed 50% in FY27, compared with an estimated negative 7% in FY26.

That swing from negative 7% to above 50% is not a rounding adjustment. It represents the transition from a period where every dollar of revenue growth was absorbed (and more) by turnaround investment costs to one where revenue growth flows through to the bottom line at scale. Evercore raised its price target to $115 from $110 and maintained its Outperform rating.

The path to $4.00 in FY28 depends on that FY27 inflection holding.

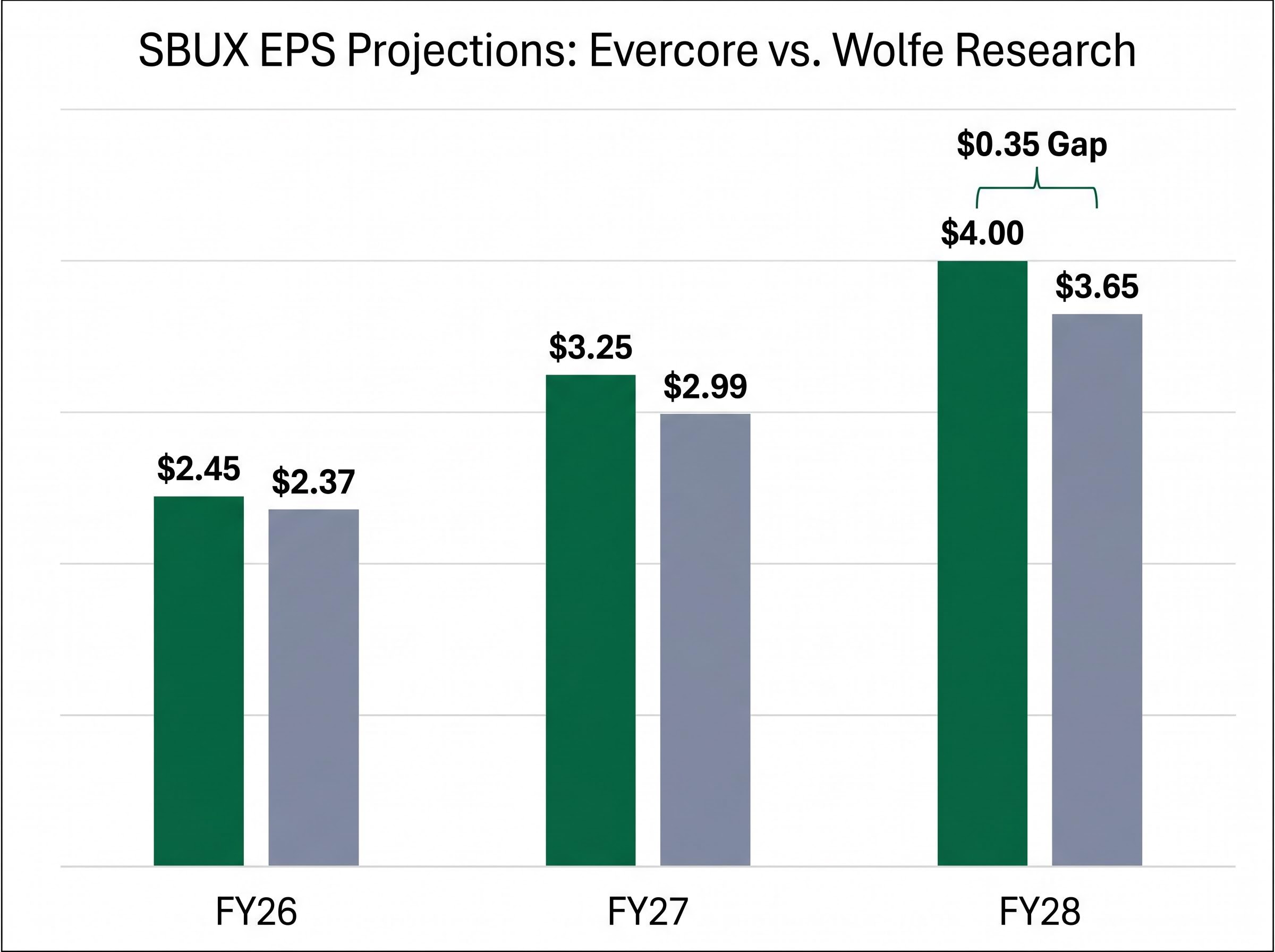

Wolfe Research tells a directionally similar story at a more measured pace. Its FY26 EPS estimate of $2.37 sits below Evercore’s $2.45, and the gap widens progressively: $2.99 versus $3.25 in FY27, and $3.65 versus $4.00 in FY28.

| Fiscal Year | Wolfe Research | Evercore | Gap |

|---|---|---|---|

| FY26 | $2.37 | $2.45 | $0.08 |

| FY27 | $2.99 | $3.25 | $0.26 |

| FY28 | $3.65 | $4.00 | $0.35 |

The widening gap reflects differing assumptions about how quickly margin expansion materialises, not a disagreement about whether it occurs. Wolfe cited two specific early-stage catalysts as reasons for its upward revisions:

What gives these revisions additional analytical weight is context. Wolfe Research downgraded SBUX to Peer Perform in March 2026. When a firm that recently downgraded a stock still raises its multi-year EPS estimates, the operational improvement is visible even through a cautious lens. The $0.35 gap between Wolfe’s FY28 estimate of $3.65 and Evercore’s $4.00, roughly 9.6%, quantifies how much execution uncertainty separates the two views.

Both analyst models rest on the same three structural drivers. Understanding which of these are within Starbucks’ operational control, and which require external cooperation, is the difference between a conviction-based position and a hope-based one.

The Energy Refresher line represents a category expansion play. Rather than competing directly with energy drink brands on their terms, Starbucks is leveraging its coffeehouse identity to enter a segment where consumer spending continues to grow. Early tracking data is positive, though it remains too early to confirm structural revenue contribution.

Grand View Research energy drinks market data projects a 7.2% CAGR for U.S. energy beverages through 2030, quantifying the scale of the category that Starbucks is entering with its Energy Refresher line and contextualising why the launch represents a meaningful revenue diversification opportunity.

North America same-store sales have improved by 13 percentage points across the six most recent quarters, per Evercore’s analysis. The March 2026 loyalty programme overhaul is designed to sustain that momentum by broadening the customer base beyond premium-frequency buyers. Early engagement data suggests the changes are attracting value-conscious customers, though sustained results over multiple quarters would be needed to validate the structural impact.

The margin expansion story that underpins both Evercore’s and Wolfe’s projections is specific enough to identify specific threats. Four risk categories could compress the FY27 inflection timeline:

Macro pressure on consumer discretionary stocks is not a theoretical concern in the current environment: national gasoline prices have surged 45% since January 2026, and three decades of data show the S&P 500 has averaged an 11% decline in the six months following weeks when gasoline exceeds $4.00 per gallon, a pattern that historically compresses spending at precisely the coffeehouse category.

Analyst price target range: The spread between TD Cowen’s low target of $89 and Evercore’s $115 illustrates the breadth of Wall Street opinion on SBUX, a $26 gap that reflects fundamentally different assumptions about execution pace.

JP Morgan set a $100 price target on 24 April 2026, just days before the Q2 report. The consensus target of $102.16 from 43 analysts implies less than 4% upside from the current $98.67. For investors considering the stock at these levels, the near-term consensus offers limited margin of safety; the case rests almost entirely on the multi-year trajectory.

The gap between Evercore and Wolfe is not a contradiction. It is a measurable range of execution uncertainty. Investors considering SBUX at $98.67 are implicitly choosing where on that spectrum they believe the company will land.

The conditions required for each scenario are specific:

The $0.35 gap between $3.65 and $4.00 in FY28 EPS amounts to approximately 9.6% in earnings divergence. At the current share price, less than 4% below the $102.16 consensus target, the valuation case for long-term holders rests almost entirely on whether the FY27 margin inflection proves as pronounced as Evercore models or as gradual as Wolfe assumes.

The question is not which firm to trust. It is what the buyer at $98.67 is betting on regarding the timing and magnitude of that inflection.

For investors wanting to benchmark how analyst estimate divergence typically resolves after a large-cap earnings beat with raised guidance, our full explainer on T-Mobile’s multi-year free cash flow compounding case walks through how JPMorgan’s 12% FCF-per-share CAGR projection through 2028 sits alongside more conservative analyst targets, illustrating the structural pattern of bull-case and conservative-case estimates converging on pace rather than direction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Evercore projects Starbucks EPS of $4.00 in fiscal 2028, while Wolfe Research estimates $3.65 for the same year. Both firms agree margin expansion will occur but differ on the pace of execution.

Starbucks reported Q2 EPS of $0.50 against an estimate of $0.43, a 16% beat, while revenue came in at $9.53 billion versus the $9.16 billion consensus. Management also raised FY26 comparable sales guidance to above 5% from above 3%.

Evercore identifies three converging factors for FY27: turnaround-era labour reinvestment costs rolling off, moderation in coffee-related input inflation, and savings from the company's $2 billion efficiency programme. Incremental North America margins are projected to exceed 50% in FY27, compared to negative 7% in FY26.

Key risks include persistent inflation delaying input cost moderation, elevated labour costs extending the negative incremental margin period, potential tariffs on coffee imports, and intensifying competition from Dunkin and independent cafes constraining same-store sales recovery.

The consensus target of $102.16 from 43 analysts implies less than 4% near-term upside from $98.67, meaning the investment case rests almost entirely on the multi-year FY27-FY28 earnings trajectory rather than near-term price appreciation.