BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

SpaceX’s S-1 registration statement, filed with the SEC in mid-2026, does more than price an IPO. It names Intel as a manufacturing partner on a facility targeting roughly 1 terawatt of annual compute output and outlines an ambition to deploy 100 gigawatts of AI processing power in orbit by as early as 2028. The filing lands at a moment when Intel is fighting to prove its foundry turnaround is real, AI infrastructure spending is accelerating at a pace Wall Street is still recalibrating to, and the definition of “compute infrastructure” is expanding beyond terrestrial data centres into entirely new physical domains. What follows breaks down what the Terafab partnership means for Intel’s manufacturing credibility and INTC investors, explains what SpaceX’s orbital compute ambitions would require in physical and logistical terms, and frames what remains genuinely uncertain versus what the S-1 confirms.

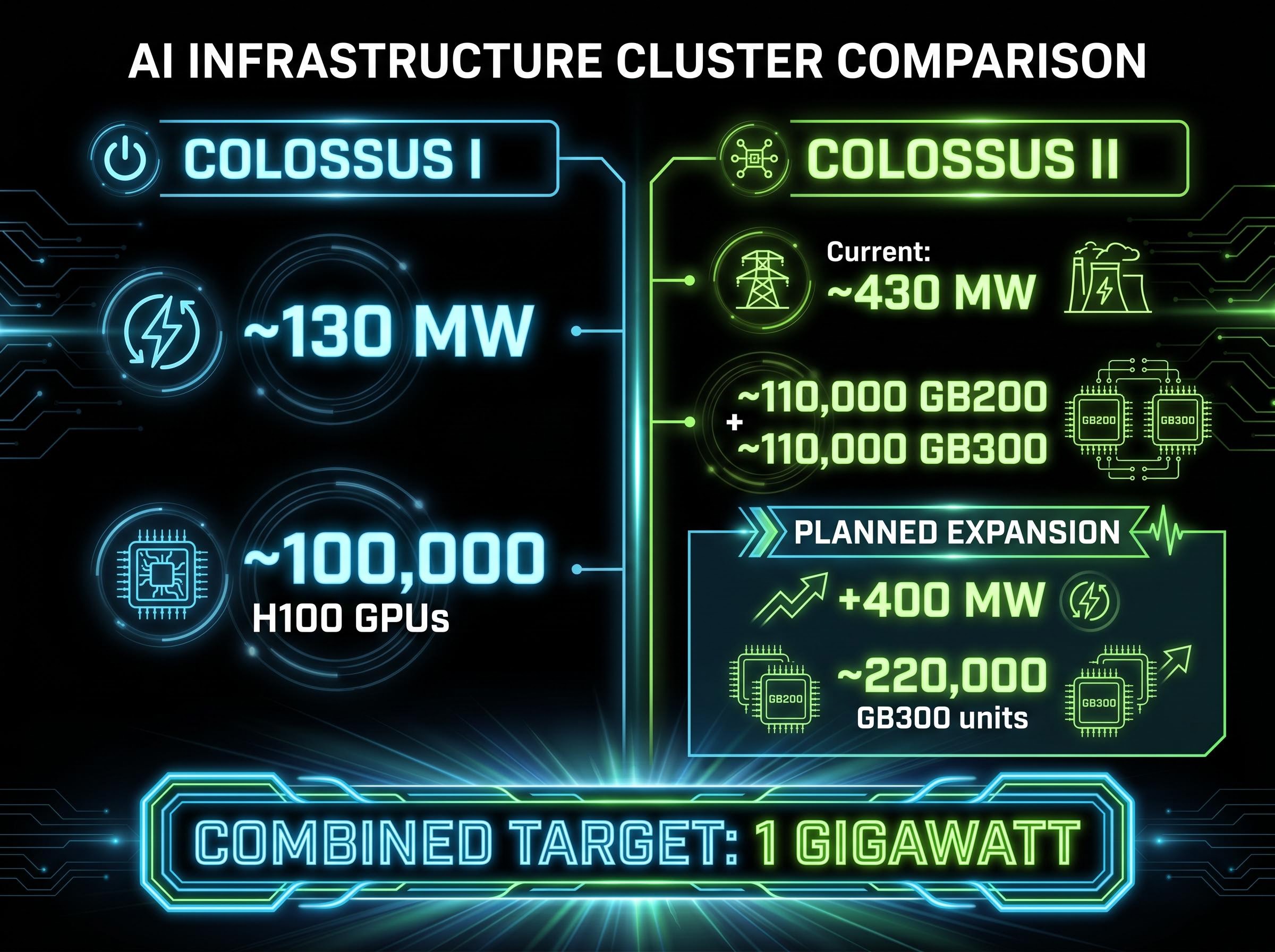

Before Terafab or satellites enter the picture, SpaceX is already one of the largest AI infrastructure operators in the world. Colossus I, the company’s first dedicated AI cluster, runs at approximately 130 megawatts with roughly 100,000 H100 GPUs. Colossus II operates at a larger scale.

The second cluster currently draws approximately 430 megawatts and houses roughly 110,000 GB200 and 110,000 GB300 processors, with a planned expansion adding another 400 megawatts and approximately 220,000 GB300 units. Combined, the two facilities are targeting 1 gigawatt of total capacity.

| Facility | Current Capacity (MW) | GPU/Processor Count | Planned Expansion |

|---|---|---|---|

| Colossus I | ~130 | ~100,000 H100 GPUs | Included in 1 GW combined target |

| Colossus II | ~430 | ~110,000 GB200 + ~110,000 GB300 | +400 MW, ~220,000 GB300 units |

The spending trajectory reinforces the scale. SpaceX’s AI-related expenditure in Q1 2026 reached $7.7 billion, implying an annualised run rate above $30 billion. That figure follows $12.7 billion in total AI capex across FY2025.

SpaceX’s Q1 2026 AI spending implies an annualised run rate exceeding $30 billion, more than doubling its FY2025 total of $12.7 billion.

Wolfe Research framed the S-1 as a semiconductor sector event, not merely a space company filing. The Colossus clusters and capex trajectory explain why: Terafab and the orbital compute programme are forward commitments layered on top of an already substantial operating base.

The SpaceX S-1 financials show $18.67 billion in full-year revenue alongside a $1.94 billion operating loss in Q1 2026, a combination that situates the Terafab announcement and orbital compute ambitions within a company that is scaling aggressively but is not yet profitable.

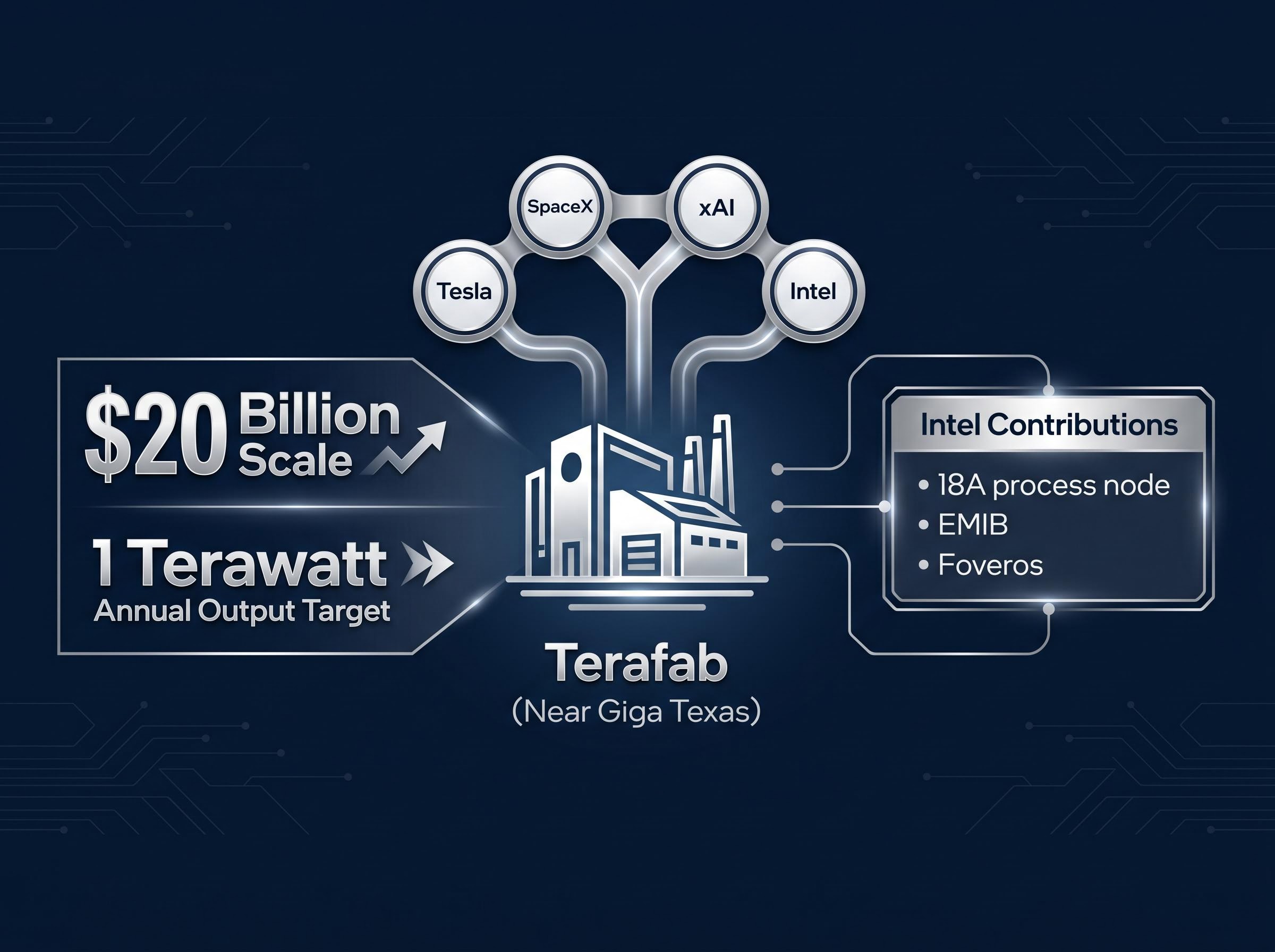

Terafab is described in the S-1 and subsequent announcements as a co-located, integrated complex targeting approximately 1 terawatt of annual compute hardware output. The concept consolidates chip design, fabrication, memory integration, and advanced packaging at a single site near Giga Texas, with a reported project scale of $20 billion, according to the Austin Business Journal (7 April 2026).

The partners named are SpaceX, Tesla, xAI, and Intel. The ambition is to produce compute hardware at a volume that would dwarf any existing single-site semiconductor operation.

Confirmed Terafab attributes include:

The S-1 and Intel’s public statements confirm Intel as a named foundry partner, the 1-terawatt output target, and the multi-company structure. What has not been disclosed is equally material.

No specific construction timeline, capital allocation breakdown, or per-partner capex obligation has appeared in the S-1 or subsequent filings. Wolfe Research noted the absence of these details. Exact capacity splits between Tesla and SpaceX output, specific chip product names, campus square footage, and Intel’s revenue or volume commitments remain unverified in public filings as of May 2026.

Intel’s selection rests on a specific set of capabilities that no other domestic foundry can currently match in combination. The company contributes its 18A process node, which features gate-all-around transistors and backside power delivery, alongside two advanced packaging technologies:

The Futurum Group (approximately 10 April 2026) connected these capabilities directly to Terafab’s requirement for vertical integration at domestic scale: design, fabrication, and packaging consolidated at a single complex. That structural argument differentiates Intel from pure-play foundries that may not offer equivalent on-shore consolidation.

Intel stated on X that it is “joining the Terafab project” to help “refactor silicon fab technology” for SpaceX, xAI, and Tesla.

Intel’s own public framing, reinforced by a Bloomberg Technology interview segment from approximately 7 April 2026, positioned this as a foundry engagement rather than a simple supply agreement. The distinction matters for Intel Foundry Services (IFS) credibility: a named role in a landmark IPO filing is a different kind of validation than a standard procurement contract.

Intel 18A node credibility is being tested across multiple simultaneous foundry conversations, with Apple’s early-stage discussions and the Terafab partnership both pointing to the same underlying question: whether IFS can achieve mass production yields sufficient to attract and retain large-scale customers before TSMC widens its capacity gap further.

Intel stock moved approximately 5% intraday on the announcement day before paring gains to roughly +2% at the close. The reaction suggests the market treated the news as a sentiment catalyst for the foundry narrative, not noise.

The S-1 establishes a target of 100 gigawatts of orbital AI compute capacity, deployed aboard satellite constellations by as early as 2028. The concept involves parking AI processing power in space rather than concentrating it in terrestrial data centres, leveraging SpaceX’s reusable launch fleet and existing Starlink constellation infrastructure.

The number registers as ambitious. Then the logistics arrive.

Wolfe Research assessed that achieving the 100-gigawatt target would require thousands of rocket launches annually, a cadence that would represent an unprecedented volume even for SpaceX’s Falcon and Starship programmes.

Academic analysis of orbital computing infrastructure power demands has identified the same scaling constraints that Wolfe Research flagged in its assessment of SpaceX’s 100-gigawatt target, with per-satellite power budgets and thermal dissipation in the vacuum of space among the most binding physical limits on constellation-based AI compute density.

Wolfe Research characterised the 100-GW orbital AI compute target as requiring thousands of annual launches, a volume without precedent in commercial spaceflight.

The S-1 establishes SpaceX’s structural advantage, its uniquely low-cost reusable launch capability and demonstrated large-constellation deployment via Starlink, without providing a detailed engineering schedule. Several questions remain open:

No quantitative breakdown of these variables appears in the S-1’s accessible sections. The orbital compute thesis is the most speculative element of SpaceX’s infrastructure roadmap, but it is also the most consequential for downstream chip demand, including from Intel.

The S-1 confirms two distinct semiconductor investment theses operating on different timelines. Nvidia holds the primary accelerator position across SpaceX’s existing AI clusters. Colossus I runs on H100 GPUs; Colossus II runs on GB200 and GB300 processors. The confirmed, near-term GPU procurement makes Nvidia the dominant hardware beneficiary of SpaceX’s current infrastructure build.

Intel occupies a different layer. Its role is manufacturing and packaging via IFS and Terafab, not supplying accelerators. The risk and reward profile differs accordingly: longer timeline, less certain revenue, but positioned at the foundational layer of production rather than the component layer.

CPU demand in AI infrastructure is compressing the historical 1:8 CPU-to-GPU deployment ratio toward 1:1 as agentic workloads emerge, a structural shift that adds a second potential revenue vector for Intel beyond its foundry role if its own chip designs can capture share in the server CPU market being rebuilt around AI agent architectures.

| Company | Role in SpaceX Ecosystem | Near-Term Revenue Visibility | Key Uncertainty |

|---|---|---|---|

| Nvidia | Primary accelerator supplier (Colossus I and II) | High (confirmed GPU procurement) | Whether orbital compute hardware uses Nvidia silicon |

| Intel | Manufacturing and packaging partner (IFS / Terafab) | Low (no disclosed revenue or volume commitments) | Terafab construction timeline and IFS revenue ramp |

Bloomberg coverage frames Broadcom in partnership with Google and Anthropic as the most visible competitive ecosystem in terrestrial AI infrastructure. No other company has announced an orbital AI compute constellation programme, leaving SpaceX’s orbital thesis without a comparable benchmark as of May 2026.

The gap between Terafab as a sentiment catalyst and Terafab as a fundamental driver for INTC comes down to specific disclosures that have not yet appeared. Investors tracking this story should monitor:

As of May 2026, Intel has not filed a Terafab-specific 8-K or disclosed Terafab revenue in its 10-Q, making independent verification of the investment scale difficult outside paywalled analyst research.

Intel SEC filings and 8-K disclosures remain the most direct mechanism for investors to independently verify whether Terafab has progressed from a named partnership to a financially committed programme, and the absence of a Terafab-specific 8-K as of May 2026 is itself a data point that distinguishes sentiment-level validation from contractual obligation.

The 2028 satellite deployment timeline is SpaceX’s stated target, not a disclosed engineering commitment. Wolfe Research’s launch-volume estimates are not publicly accessible and have not been independently corroborated in open financial data.

The most reliable public data sources ahead of a formal IPO roadshow are SpaceX S-1 amendments filed with the SEC and FCC constellation filings. The satellite programme’s financial legibility depends on Terafab’s output becoming defined; the orbital thesis does not become investable until the terrestrial manufacturing foundation is further specified.

The Terafab partnership confirms something material for Intel Foundry Services: its 18A node and advanced packaging have reached sufficient credibility to be named in a landmark IPO filing alongside Tesla and xAI. That is a meaningful reputational milestone for a foundry business the market has been reluctant to value.

The counterweight is equally clear. No Terafab revenue, timeline, or volume commitment appears in Intel’s own SEC filings as of May 2026. The partnership has not yet changed Intel’s fundamental financial outlook in a quantifiable way.

Intel stated it is “joining the Terafab project” to help “refactor silicon fab technology,” positioning the engagement as a foundry mandate rather than a supply contract.

The forward-looking question for INTC investors is whether Terafab and the satellite programme represent a genuine foundry revenue ramp or a high-profile association that flatters Intel’s narrative without yet altering its numbers. Terafab is simultaneously the most credible external validation Intel Foundry has received and the least financially legible partnership announcement it has made, because the two most important figures, revenue and timeline, remain undisclosed.

Investors working through how Nvidia, Intel, and the broader semiconductor stack fit within a structured portfolio will find our comprehensive walkthrough of AI infrastructure stock allocation covers the 50/40/10 hardware-cloud-software framework, Goldman Sachs projections for $527 billion in hyperscaler capex in 2026, and allocation sizing guidance for growth portfolios with AI infrastructure exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Terafab timelines, orbital compute targets, and revenue projections are speculative and subject to change based on market developments and company performance.

Terafab is a co-located semiconductor complex targeting approximately 1 terawatt of annual compute hardware output, reported at a $20 billion scale and co-located near Giga Texas. Its named partners are SpaceX, Tesla, xAI, and Intel.

The SpaceX S-1 filing names Intel as a manufacturing partner contributing its 18A process node, EMIB advanced packaging, and Foveros 3D stacking technology to the Terafab project, positioning Intel Foundry Services at the production layer rather than the component supply layer.

SpaceX's AI-related expenditure reached $7.7 billion in Q1 2026 alone, implying an annualised run rate above $30 billion, compared to $12.7 billion in total AI capex across all of FY2025, signalling accelerating demand for both GPU accelerators and foundry manufacturing capacity.

As of May 2026, no Terafab-specific construction timeline, per-partner capital commitment, revenue figure, or volume obligation has appeared in Intel's own SEC filings, meaning the partnership remains a reputational milestone rather than a financially quantifiable contract.

SpaceX's S-1 outlines a goal of deploying 100 gigawatts of AI processing power in orbit by as early as 2028, but Wolfe Research estimated this would require thousands of rocket launches annually, a cadence without precedent, and the S-1 provides no detailed engineering schedule or satellite architecture breakdown.