BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

SpaceX filed its IPO registration on 20 May 2026, pulling the curtain back on a company targeting a valuation of up to $2 trillion and, for the first time, disclosing the financial data behind one of the most closely watched private enterprises in history. The filing, which follows a confidential S-1 submission on 1 April 2026, represents the most consequential U.S. technology listing in years. It also reveals a suite of business ambitions that stretch well beyond rockets: orbital computing, financial services, asteroid mining, and a $60 billion acquisition option for AI code editor Cursor. For investors evaluating SPCX as a potential holding, the prospectus is the first authoritative window into both where SpaceX stands financially today and where management intends to take it over the next decade. What follows is a breakdown of what the filing actually discloses, from the revenue numbers to the governance structure to the forward-looking business lines that will define how the market prices SpaceX’s growth premium.

The numbers arrived without precedent. No private U.S. company of this scale has disclosed its financial position in an IPO filing before, and the headline figures establish a business of considerable revenue, operating at a loss.

The $1.94 billion operating loss reported in Q1 2026 is the figure that reframes the entire valuation discussion. SpaceX is a high-revenue enterprise that is not yet profitable.

That gap between scale and profitability is where the tension sits. Investors accustomed to evaluating mature businesses will recognise the pattern of aggressive reinvestment, but the magnitude of the loss against a $1.75 trillion-plus valuation ask means every growth ambition disclosed elsewhere in the filing carries weight it would not carry at a smaller price tag.

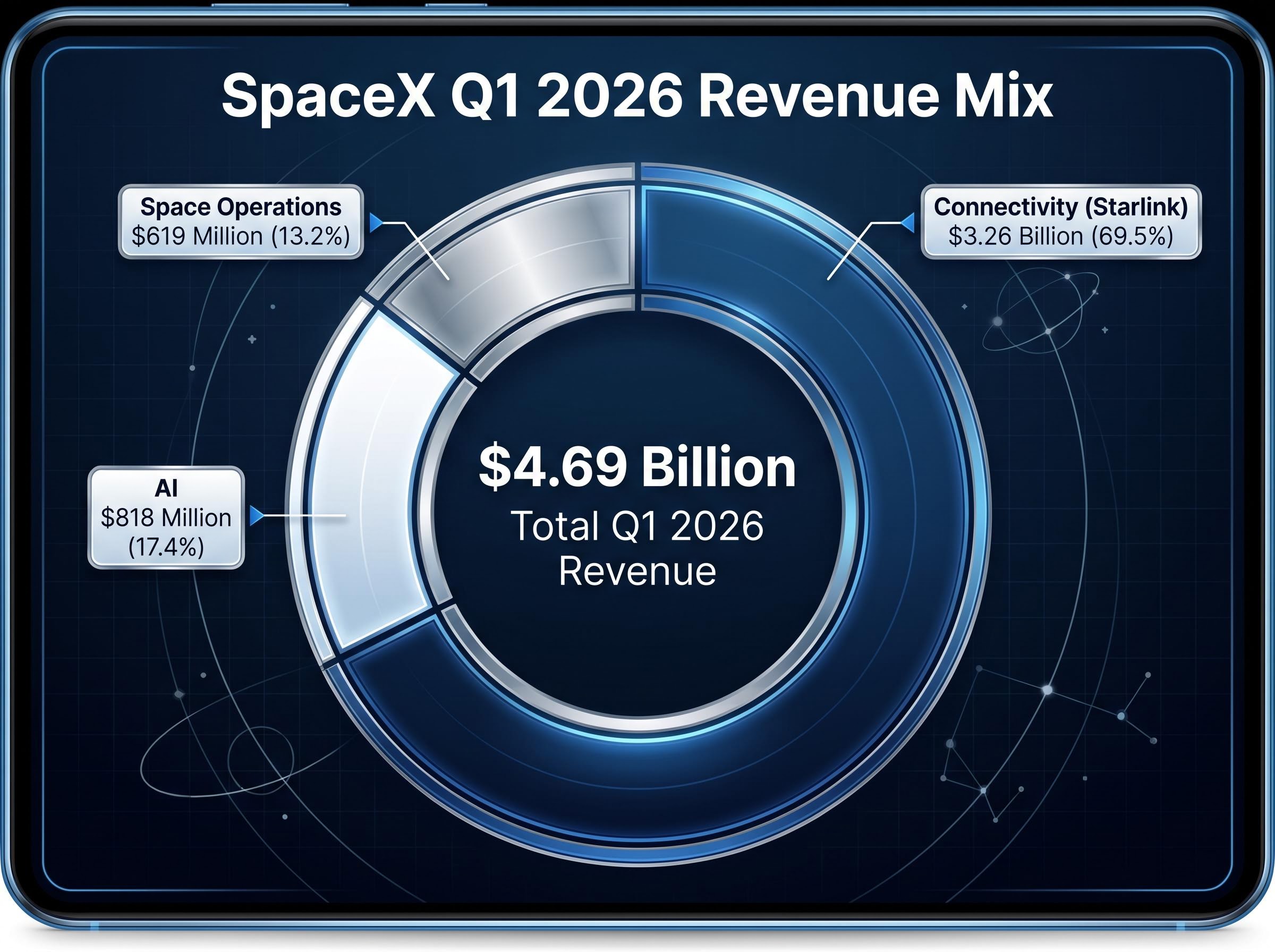

Starlink is carrying the financial load. The connectivity division generated $3.26 billion in Q1 2026, accounting for roughly 69% of total quarterly revenue. That dominance is expected, but the segment breakdown reveals a company already more diversified than its public image suggests.

| Q1 2026 Segment | Revenue | Share of Total |

|---|---|---|

| Connectivity (Starlink) | $3.26 billion | 69.5% |

| AI | $818 million | 17.4% |

| Space Operations | $619 million | 13.2% |

The AI segment’s $818 million is not a footnote. It signals where management believes the revenue mix will shift, and at nearly a fifth of quarterly revenue, it already commands enough scale to justify its own analyst coverage. Space operations, the launch business that built SpaceX’s reputation, now contributes the smallest share. For investors modelling long-term earnings potential, the segment split suggests the operating loss is funding a transition, not merely subsidising a single product.

The voting arithmetic is the first thing to absorb. According to the filing, Elon Musk holds 12.3% of Class A shares and 93.6% of Class B shares, producing a combined voting authority of approximately 79% of all outstanding votes.

A dual-class share structure separates economic ownership from voting power. Shareholders who buy Class A stock in the IPO will own a proportional economic stake in SpaceX, entitling them to a share of future profits, but they will hold a fraction of the voting influence that the structure gives to Class B holders. In practice, this means public shareholders will have effectively no ability to influence strategic direction, board composition, or executive compensation. For U.S. investors accustomed to governance norms at S&P 500 companies, where independent board oversight is standard, the controlled company designation is a material governance consideration. Every ambitious expansion plan disclosed in the filing is, ultimately, a plan that Musk alone has the voting power to pursue or abandon.

Research published by the Harvard Law School Forum on Corporate Governance documents how dual-class structures have become increasingly prevalent in technology IPOs, with founders routinely retaining super-voting shares that render public shareholders economically significant but strategically marginal.

The filing outlines five expansion verticals beyond SpaceX’s current revenue base. Each is presented below in order of disclosed timeline specificity, from the most near-term to the most open-ended:

SpaceX targets deployment of orbital AI computing hardware before the end of the 2020s, the only forward-looking milestone in this group with a hard-dated timeframe.

The AI infrastructure capital cycle underpinning SpaceX’s orbital compute ambitions is itself operating at historic scale: hyperscalers are projected to deploy between $630 billion and $700 billion in 2026 alone, a figure equivalent to roughly 2% of US GDP, which both validates the market SpaceX is entering and raises questions about whether orbital compute can compete with terrestrial data center economics.

These verticals are what separate SpaceX’s valuation from that of any other aerospace company. Some, particularly orbital computing and Terafab, have identifiable near-term revenue pathways. Others, particularly asteroid mining, are multi-decade speculative bets. Investors pricing SPCX at $1.75 trillion or above are implicitly assigning value to all of them.

These forward-looking disclosures are subject to change based on market developments, regulatory conditions, and company performance.

Cursor is an AI-assisted code editor, a software tool that uses artificial intelligence to help developers write and edit code more efficiently. It is not a household name outside the software industry, but SpaceX’s interest in it is substantial.

The implied valuation of the Cursor arrangement: $60 billion in Class A common stock.

At $60 billion, this would rank among the largest software acquisitions in U.S. history. The strategic logic connects to SpaceX’s existing AI segment, which generated $818 million in Q1 revenue, and to the orbital compute ambitions disclosed elsewhere in the filing. If the deal closes, it would position SpaceX as both an AI infrastructure provider and an AI software company. For SPCX investors, the question is whether Cursor accelerates a coherent AI monetisation path or dilutes Class A shareholders at a steep premium for an adjacency play.

This is a disclosed option arrangement, not a completed acquisition. The transaction remains subject to post-IPO execution and has not been finalised.

Every disclosure in the filing feeds into a single question: does the business SpaceX is describing justify a $1.75 trillion to $2 trillion-plus valuation?

The filing’s IPO process follows a defined timeline:

| Lead Bookrunners | Additional Underwriters |

|---|---|

| Goldman Sachs | Barclays |

| Morgan Stanley | Deutsche Bank Securities |

| Bank of America | RBC Capital Markets |

| Citigroup | UBS Investment Bank |

| J.P. Morgan | Wells Fargo Securities |

The roadshow will be the first real test. Institutional investors will weigh current-period operating losses against a multi-vertical growth story spanning this decade and beyond. The book-building process, specifically whether the deal prices at the top or bottom of the range, will be the most actionable signal available to retail investors considering SPCX.

IPO proceeds of this scale, with the $50-75 billion raise expected to surpass the combined totals of Saudi Aramco and Alibaba, would represent a capital absorption event unlike anything institutional allocators have navigated in a single deal, and the book-building dynamic over the June roadshow will determine whether demand holds at the upper end of that range.

20 May 2026 marks the beginning of public investor scrutiny, not the end of the evaluation process. The filing presents a company of extraordinary stated ambition, a governance structure that concentrates control in a single individual, an early-stage profitability profile, and a valuation that prices the full vision before most of it has been built.

The roadshow, institutional pricing, and the first post-listing quarterly filings will provide the next substantive information. Until then, the prospectus is the baseline, and the gap between what SpaceX earns today and what it aims to become is exactly where the investment thesis will be tested.

For readers wanting to situate the SPCX offering within broader market positioning signals, our full analysis of how SPCX fits the current tech valuation landscape examines sell-side forecast drift above independent estimates, Fisher Investments’ underweight move on technology, and BofA fund manager survey data showing maximum overweight positioning in US tech since before the 2021 peak.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and forward-looking statements referenced in this article are subject to market conditions and various risk factors.

The SpaceX IPO is the public offering of SpaceX shares under the ticker SPCX on Nasdaq, with pricing and listing targeted for 11-12 June 2026 following a roadshow beginning in early June 2026.

SpaceX reported full-year revenue of $18.67 billion and Q1 2026 revenue of $4.69 billion, with Starlink's connectivity segment contributing $3.26 billion, or roughly 69% of quarterly revenue.

SpaceX's dual-class structure gives Elon Musk approximately 79% of total voting power through Class B shares, meaning public investors who buy Class A shares will hold an economic stake but have effectively no influence over strategic or governance decisions.

SpaceX disclosed an option to acquire Cursor, an AI-assisted code editor, for $60 billion in Class A common stock, a deal planned to close after the IPO that would position SpaceX as both an AI infrastructure provider and an AI software company.

The SpaceX IPO prospectus disclosed five expansion verticals beyond its current operations: orbital AI computing hardware, Terafab semiconductor manufacturing with Tesla, Intel, and xAI, scaled launch frequency, financial services, and long-term asteroid mineral extraction.