Vance Pulls Out of Iran Talks, Sending Brent Below $80

59 mins ago

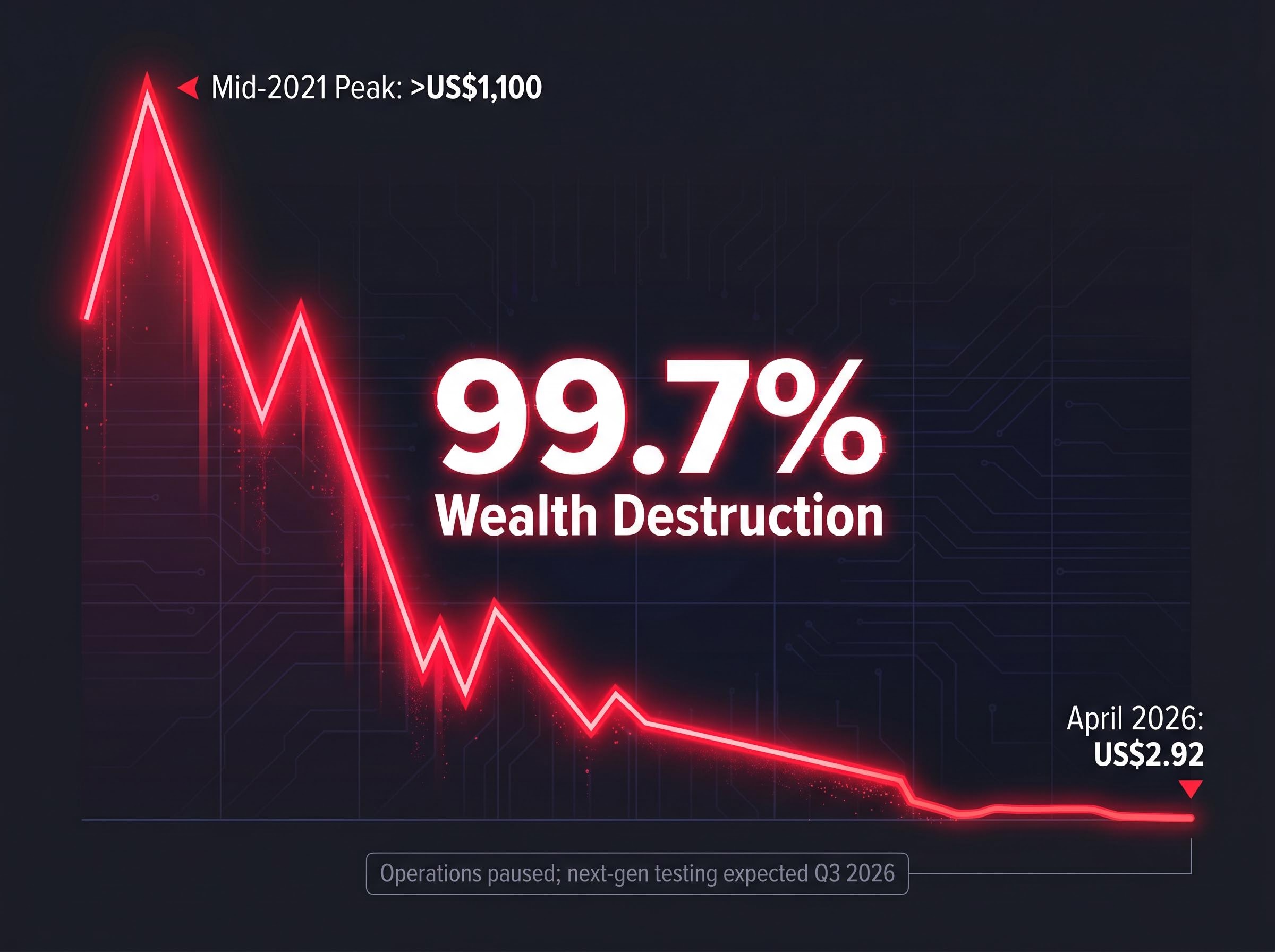

A stock that once traded above US$1,100 per share now changes hands at under US$3. That is a 99.7% destruction of shareholder wealth, unfolding over roughly five years in full view of public markets. With the Betashares Space Industry ETF (RCKT) newly announced for the ASX and commentary from the Australian Financial Review framing the sector as “back in a big way,” Australian retail investors are encountering space at a moment of peak enthusiasm. The timing creates a specific structural risk: enthusiasm arriving without institutional memory. What follows uses Virgin Galactic’s collapse as an analytical lens to identify the risk mechanisms present in early-stage thematic investing, examine how those mechanisms translate into ETF products, and deliver a practical due diligence framework for investors considering space sector investing through vehicles like RCKT.

In mid-2021, Virgin Galactic (NYSE: SPCE) surged approximately 300% within a single month. Zero interest rates, pandemic-era stimulus payments, and the arrival of commission-free trading through platforms such as Robinhood had flooded speculative equities with retail capital drawn to narrative appeal. The stock pushed above US$1,100 per share.

No commercial milestone justified that price. Virgin Galactic had no recurring revenue, no proven operational cadence, and no timeline for regular commercial flights. The valuation was built entirely on forward-looking narrative, the kind of premium that requires flawless execution to sustain and collapses rapidly without it.

99.7% decline. From a peak above US$1,100 in mid-2021 to US$2.92 by April 2026, Virgin Galactic’s share price trajectory represents one of the most severe wealth destruction events among publicly listed space companies.

The collapse was not a single event. It followed a multi-year sequence of identifiable failures.

Operations remain paused as of April 2026. Next-generation spaceship testing is expected to resume in Q3 2026 at the earliest. No bankruptcy or delisting has occurred, but the stock trades at US$2.92, a level where several analysts have flagged potential further deterioration toward zero given ongoing fundamental weakness.

The timeline matters because it reveals a pattern, not a surprise. Each stage was visible in advance to investors willing to interrogate the gap between narrative and execution.

Virgin Galactic’s trajectory was not an isolated misfortune. It was the predictable expression of structural features shared across early-stage space companies, features that distinguish this sector from conventional growth investing.

The first is the pre-revenue business model. Space companies require enormous upfront capital for hardware development, testing, and certification, with no reliable near-term cash flow. Development timelines stretch across years, and commercial milestones slip frequently due to engineering complexity, regulatory requirements, or launch failures.

The second is the SPAC listing mechanism. Many space companies that reached public markets between 2020 and 2022, including Virgin Galactic, Momentus (MNTS), and Astra Space, did so via Special Purpose Acquisition Companies (SPACs), shell entities that allow a private company to list publicly by merging with the shell rather than undergoing a conventional IPO. This pathway bypassed the scrutiny of a standard listing process, bringing companies to retail markets before they would have qualified for traditional public offerings.

SPAC listing mechanics allowed companies to reach retail markets without satisfying the revenue, governance, and disclosure thresholds required by a conventional IPO process; the Ovanti case from early 2026 illustrates how this pathway continues to operate on ASX-connected exchanges, with boards terminating deals and seeking larger sponsors when initial valuations fall short.

The pattern across this cohort is consistent: SPAC-driven enthusiasm followed by commercial execution failures, repeated capital raises, and sustained price deterioration.

Yale Journal on Regulation research on SPAC underperformance quantifies the pattern of post-merger share price deterioration across the 2020-2022 cohort, providing systematic evidence that the structural weaknesses seen in Virgin Galactic, Momentus, and Astra Space were sector-wide features of the SPAC listing mechanism rather than company-specific failures.

| Company | SPAC listing year | Key execution failure | Status (April 2026) |

|---|---|---|---|

| Virgin Galactic (SPCE) | 2019 | Suspended commercial flights; repeated capital raises | Trading at US$2.92; operations paused until Q3 2026 |

| Momentus (MNTS) | 2021 | Severe cash pressures; no sustained commercial traction | Surged ~81% in early 2026 over two sessions; volatility, not recovery |

| Astra Space | 2021 | Operational difficulties; reduced public profile | Part of the broader SPAC cautionary cohort |

Recognising SPAC origins and pre-revenue status as structural warning signals, rather than temporary growing pains, allows investors to assess new space listings with calibrated scepticism.

A basket structure is the strongest structural argument for ETF exposure over individual stock selection in speculative sectors. An ETF holding 30-50 space companies absorbs individual company failures without total capital loss. If a single holding follows a trajectory comparable to SPCE’s 99.7% decline, the portfolio-level impact is contained to that holding’s weighting rather than destroying the entire position.

This is a genuine improvement over concentrated single-stock exposure, and it is the primary reason thematic ETFs exist as products.

Diversification within a single speculative sector is not the same as de-risking a portfolio. Several material risks persist regardless of ETF packaging.

Sector-level concentration means the entire basket can decline simultaneously during a broad risk-off move or a shift in sentiment toward space equities. Valuation compression across the whole basket is possible when multiple holdings share elevated price-to-revenue ratios built on forward expectations. Newly launched products carry liquidity risk: wider bid-ask spreads and lower trading volumes increase transaction costs for retail investors. And if multiple holdings share the same SPAC-originated structural weaknesses, the diversification benefit may be thinner than the fund’s holding count suggests.

| Fund name | Ticker | Exchange | AUM | Recent performance |

|---|---|---|---|---|

| ARK Space Exploration & Innovation ETF | ARKX | NYSE Arca | ~US$737M | +101.82% (3-year, Mar 2024 to Mar 2026) |

| VanEck Space Innovators UCITS ETF | JEDI | Various European | ~€1,348M | +172.39% (1-year) |

| Betashares Space Industry ETF | RCKT | ASX | TBC (April 2026 launch) | N/A (newly announced) |

| Global X Space Tech ETF | ORBX | NYSE Arca | TBC | Launched 15 April 2026 |

| Tema Space Innovators ETF | NASA | NYSE Arca | TBC | Launched 31 March 2026 |

ARKX’s three-year return of +101.82% demonstrates that space-sector exposure has generated real returns. That same performance window, however, followed a prior deep drawdown period, illustrating that strong recent numbers do not erase structural sector risk.

ETF portfolio construction among Australian retail investors in 2026 is increasingly weighted toward international equity exposure, with Millennials allocating approximately 70% of holdings to ETFs and BetaShares forecasting total ASX ETF assets to exceed $500 billion by end-2028, a growth trajectory that creates both a larger audience for products like RCKT and a larger pool of investors who may be encountering thematic sector risk for the first time.

Analyst downside risk. Analysts have flagged up to 56% potential declines in 2026 for high-profile space holdings including Intuitive Machines (LUNR) and AST SpaceMobile (ASTS), both of which appear as thematic ETF holdings with elevated valuation risk relative to near-term revenue potential.

Australia’s regulatory architecture gives retail investors a structured foundation for due diligence that is stronger than intuition or media sentiment alone.

ASIC Regulatory Guide 282 sets out specific obligations for ETF issuers covering product governance, retail investor protections, securities lending disclosure, and oversight of private markets components within fund holdings, all of which apply directly to thematic space ETF products listed on the ASX.

ASIC Regulatory Guide 282 (RG 282), issued in November 2025, governs exchange-traded products with specific provisions relevant to thematic ETFs. The guide strengthens issuer responsibilities for product governance, enhances retail investor protections, imposes securities lending disclosure requirements, and heightens oversight of private markets components within ETF holdings.

ASIC’s broader intervention philosophy reinforces these provisions. A 2023 intervention (media release 23-327MR) to protect retail investors from high-risk offers established the precedent for thematic product oversight.

ASIC expects issuers to clearly communicate the speculative and concentrated nature of thematic sector exposure, including volatility risk relative to diversified broad-market products and the potential for significant capital loss in nascent commercial sectors.

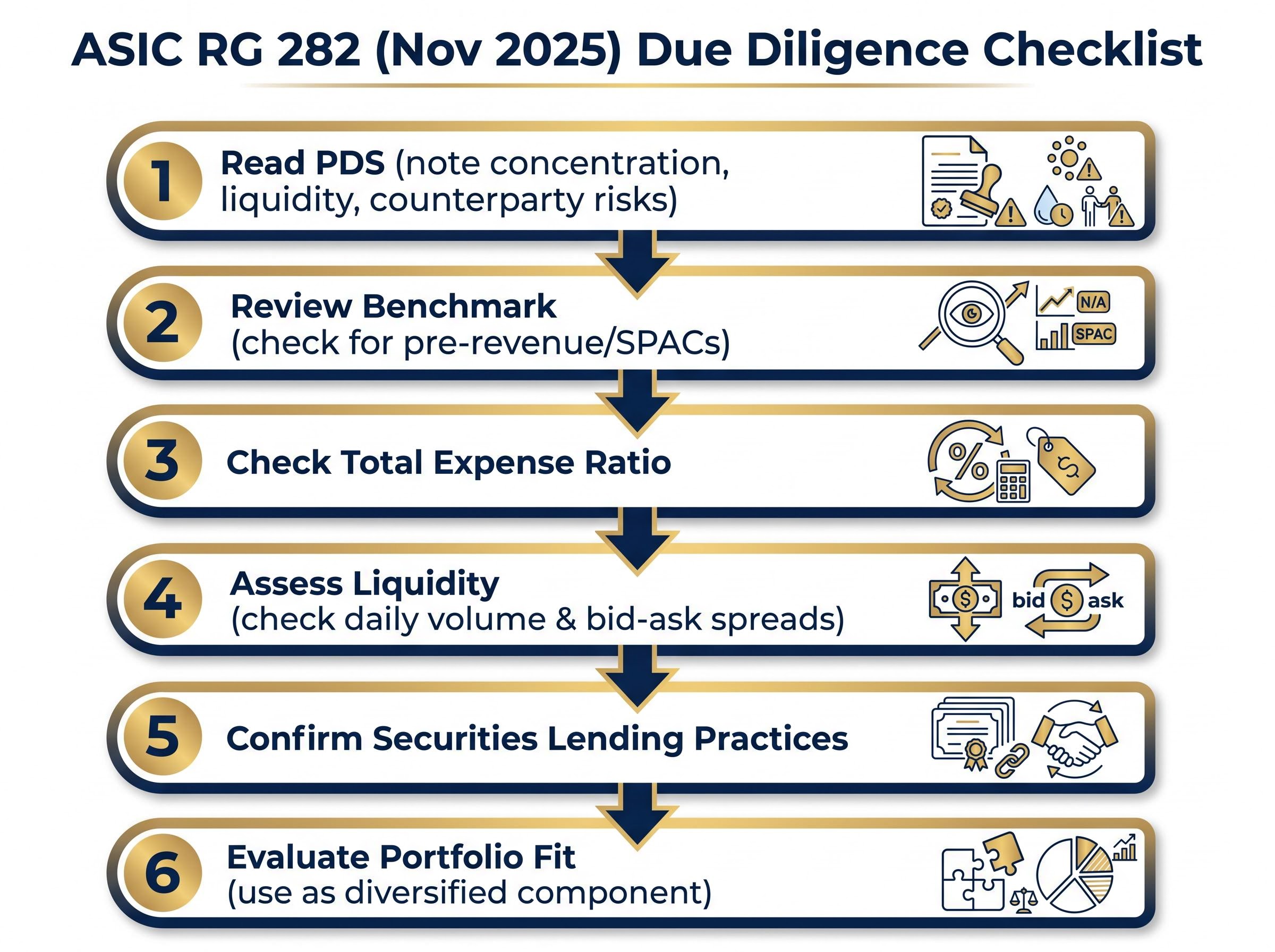

For Australian retail investors evaluating RCKT or any comparable product, the Product Disclosure Statement (PDS) is a non-optional step. The following checklist, consistent with ASIC guidance, provides a sequential review process:

The Virgin Galactic case, the structural ETF risk factors, and ASIC’s regulatory requirements converge on a single point: investors need a framework they can apply before committing capital. The following six-point checklist synthesises the analysis into actionable steps.

Position sizing and portfolio role clarity matter most when speculative thematic exposure is held alongside ASX-listed ETF alternatives that serve different functions, including income generation, inflation hedging, and liquidity management, since the total risk profile of a portfolio depends on what the thematic allocation is sitting next to, not just its own volatility characteristics.

As Kalkine Media noted in its Australian coverage, the widened accessibility of space ETFs must be weighed against the inherent speculative risk the sector carries. With RCKT now accessible directly on the ASX, removing the friction of international brokerage accounts, the barrier to entry has dropped substantially. A clear framework matters more, not less, when access becomes easy.

The performance data is real. ARKX returned +101.82% over three years. JEDI returned +172.39% over one year. Australian government space infrastructure funding provides a long-term policy tailwind. The sector’s commercial case remains structurally credible, and the Betashares RCKT launch marks a milestone in retail accessibility on the ASX.

The Virgin Galactic lesson is not that investors were wrong to believe in space. The lesson is that they paid a speculative premium during a period of extraordinary retail momentum without understanding the fundamental execution risk underneath the narrative. That distinction separates informed capital allocation from speculation.

Thematic sector maturity provides a useful benchmark for calibrating how much speculative premium is appropriate at any given stage of a sector’s development: climate tech, which BetaShares also covers through the ERTH ETF on the ASX, has moved from venture-style narrative pricing toward infrastructure-grade revenue visibility over roughly a decade, a trajectory that illustrates both what space investing could eventually look like and how far the sector currently sits from that endpoint.

Accessibility does not equal safety in speculative thematic investing. The investors best positioned to benefit from space-sector exposure are those who enter with a clear framework rather than narrative enthusiasm alone.

Three lessons from the Virgin Galactic case apply directly to thematic ETF investing:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Space sector investing involves buying shares or ETFs focused on companies developing commercial space technology, launch services, and related infrastructure. It is considered high risk because many companies are pre-revenue, carry multi-year development timelines, and have historically reached public markets via SPAC listings that bypass conventional IPO scrutiny.

Virgin Galactic peaked above US$1,100 per share in mid-2021 during a period of pandemic-era retail momentum and zero interest rates, despite having no commercial revenue. Over the following years, repeated operational delays, suspended flights, and multiple equity dilutions eroded investor confidence, with the stock trading at US$2.92 by April 2026.

RCKT is the Betashares Space Industry ETF listed on the ASX, announced in April 2026, which provides Australian retail investors with diversified exposure to global space sector companies without requiring an international brokerage account. Its specific holdings had not been disclosed at the time of the announcement, making a full PDS review essential before investing.

A basket structure limits the damage from any single company collapse, but it does not remove sector-level risks such as simultaneous valuation compression across holdings, liquidity issues in newly launched ETFs, or the fact that multiple holdings may share the same SPAC-originated structural weaknesses. Diversification within one speculative sector is not the same as de-risking a portfolio.

ASIC Regulatory Guide 282 requires ETF issuers to disclose concentration, liquidity, and counterparty risks, and investors should read the Product Disclosure Statement in full, review benchmark composition for pre-revenue or SPAC-originated holdings, check the total expense ratio, assess bid-ask spreads, and confirm whether securities lending applies before committing capital.