Energy Funds Post Record Outflows as Global Equities Bleed Capital

3 hrs ago

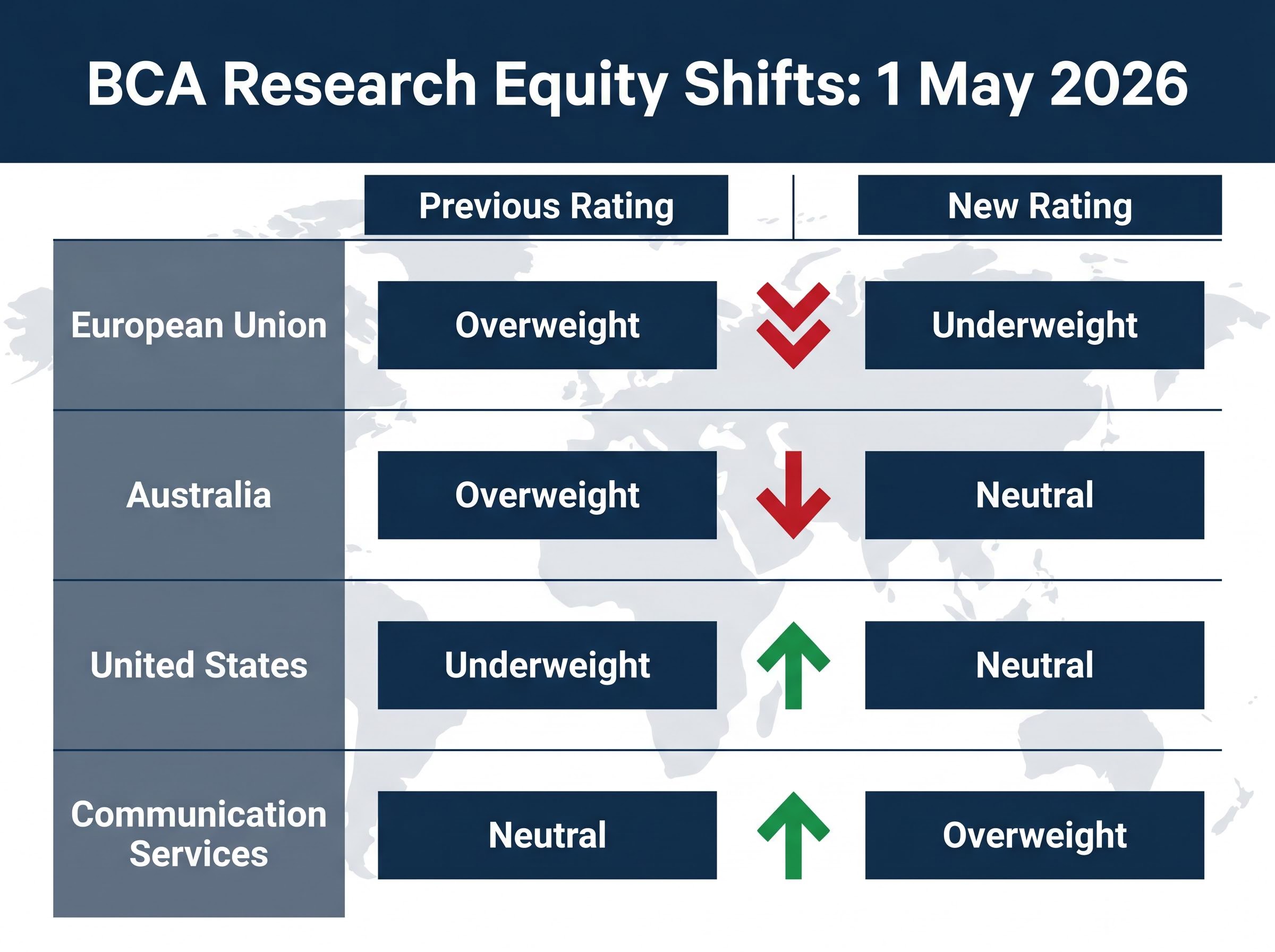

BCA Research made one of its sharpest regional equity calls of the year on 1 May 2026, slashing EU equities from overweight to underweight and cutting Australia from overweight to neutral, while simultaneously lifting U.S. equities to neutral. The catalyst is the ongoing Strait of Hormuz closure, announced by the Islamic Revolutionary Guard Corps (IRGC) on 27 March 2026, which has sent WTI crude surging roughly 24% year-to-date to around $71 per barrel and forced institutional investors to reassess which regions absorb the most damage from a sustained energy supply shock.

The triple move, issued as a single coordinated repositioning, carries a clear message: the geopolitical risk premium is no longer a uniform drag on global equities but a force that punishes energy-dependent regions while leaving others comparatively insulated. What follows explains precisely what BCA changed, why the Hormuz closure produces asymmetric regional damage, how the firm’s simultaneous AI-sector upgrade fits into the same framework, and what the combined moves signal for global equity positioning in the weeks ahead.

Three regional equity ratings moved in the same report, and they moved in the same direction: away from energy-vulnerable markets and toward the one with domestic production insulation. BCA chief strategist Juan Correa published the changes on 1 May 2026, framing them as a unified geopolitical risk view rather than three independent calls.

| Region | Previous Rating | New Rating |

|---|---|---|

| European Union | Overweight | Underweight |

| Australia | Overweight | Neutral |

| United States | Underweight | Neutral |

Juan Correa, BCA Research: The simultaneous shifts reflect a single thesis: the Hormuz closure has reordered which equity markets carry the greatest energy-cost burden, and allocations must follow.

The scale of the EU downgrade, a two-notch move from overweight to underweight, is the most aggressive. Australia’s one-notch cut and the U.S. upgrade to neutral complete a repositioning that amounts to a full rotation of regional risk preferences within a single publication.

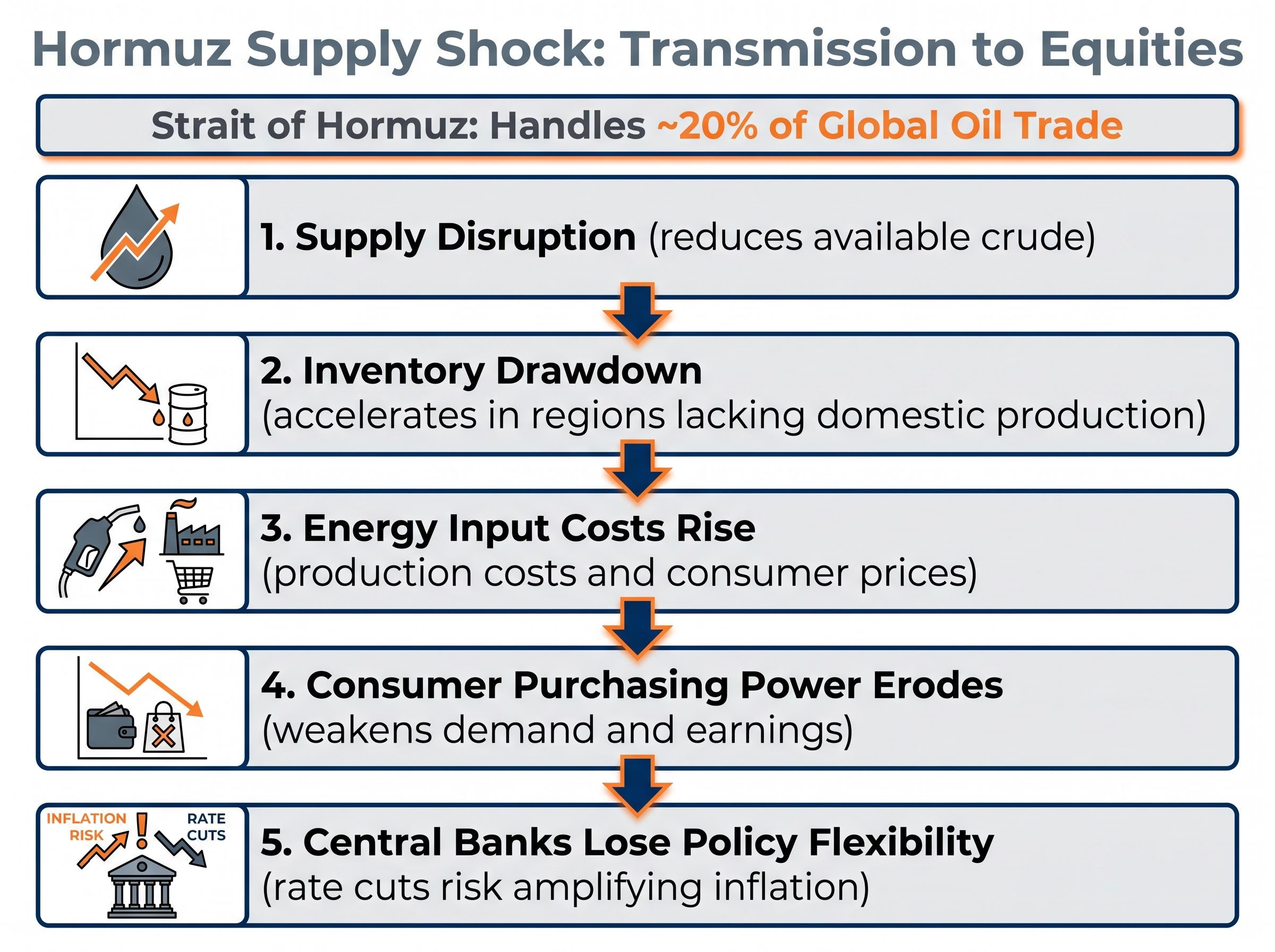

The IRGC announced the closure of the Strait of Hormuz on 27 March 2026, targeting shipping from the United States, Israel, and their allies. WTI crude climbed roughly 24% year-to-date through March, reaching approximately $71 per barrel, as markets priced in the loss of a chokepoint that handles roughly 20% of global oil trade, according to the Congressional Research Service (CRS R45281, 11 March 2026).

The oil price move, however, is only the first link in the chain. BCA Research identified three transmission channels through which the shock flows into regional equity markets:

The Hormuz oil price shock reached a peak on 30 April 2026 when Brent briefly touched $125 per barrel before closing at $111.88, as markets simultaneously priced in escalation and residual diplomatic optionality, an extreme intraday range that itself illustrates how uncertain the supply outlook remains.

The United States, by contrast, sits on a domestic energy production base that partially offsets the import disruption. Its refineries source a smaller share of crude from Middle Eastern routes, and the Federal Reserve retains comparatively more policy flexibility.

BCA’s analysis characterised the Hormuz-driven oil shock as taking easy monetary policy “off the table” as a market backstop. In prior energy disruptions, central banks in Europe and Australia could offset some demand destruction by cutting rates. This time, with energy costs feeding directly into consumer price indices, easing would risk stoking the inflation the shock itself generates. The Dallas Federal Reserve’s March 2026 analysis reinforced this constraint, noting the tension between supporting growth and containing imported inflation.

The same report that cut two regional equity ratings contained an offensive move: BCA upgraded the Communication Services sector from neutral to overweight on 1 May 2026, naming Meta and Google (Alphabet) as its preferred vehicles for AI exposure.

The upgrade connects to BCA’s broader “Great Rotation” framework for 2026, which anticipates capital shifting from broad technology holdings toward earnings-backed non-tech equities and selected AI plays with demonstrable revenue momentum. The AI capital expenditure cycle, in BCA’s view, operates independently of the consumer-spending pressures created by the oil shock.

The hyperscaler capital expenditure cycle now represents approximately 2% of US GDP, with projections for 2026 ranging from $630 billion to $700 billion; roughly 75% of that capital is directed toward physical hardware and data centre construction, creating semiconductor demand that is structurally independent of consumer confidence or energy cost pressures.

Juan Correa suggested the market may be in the early stages of a “sharp, accelerating rally” in AI-related equities, driven by corporate spending commitments that are already locked in.

The spending data supports that conviction:

BCA characterised this capital expenditure cycle as “endogenous,” meaning it is driven by corporate investment decisions rather than consumer demand, and therefore largely insulated from the Hormuz-induced purchasing power squeeze hitting other sectors.

The regional rating shifts are tactical overlays on a pre-existing 2026 framework, not a wholesale reversal. BCA’s standing S&P 500 outlook, published in January 2026, anchors the firm’s equity view:

BCA’s 13 April 2026 report, titled “After Supply Shock,” maintained benchmark asset allocations and a neutral overall equity stance. The firm declined to call for aggressive overweights or underweights on the basis of the energy shock alone, treating the Hormuz disruption as a regional differentiator rather than a systemic equity de-risking event.

Peter Berezin, in a 2 March 2026 commentary titled “Oil Shocks Ain’t What They Once Were,” argued that inflationary pass-through from oil price surges has diminished compared with historical episodes. Labour market slack, in BCA’s assessment, limits how persistently energy-driven inflation can embed in broader price levels.

Equity resilience during conflict has a strong historical base rate: the S&P 500 has delivered a positive return one year after conflict onset in 73% of cases since 1959, with a median gain of approximately 9.7%, a pattern that contextualises BCA’s decision not to call for aggressive de-risking despite maintaining a cautious earnings outlook.

Separately, BCA has maintained earnings scepticism that predates the Hormuz closure. The firm has questioned whether consensus S&P 500 EPS expectations can be met over the following 12-18 months, citing margin pressure and slowing revenue growth. This caution exists as a distinct risk overlay, independent of the geopolitical shock.

A physical shipping chokepoint may seem distant from an equity portfolio rating, but the transmission sequence is direct. The Strait of Hormuz handles roughly 20% of global oil trade, according to the Congressional Research Service.

The EIA analysis of global oil transit chokepoints puts the strait’s throughput at 20.9 million barrels per day in the first half of 2025, equivalent to roughly one-quarter of all maritime-traded oil worldwide, a figure that underscores why a sustained closure produces outsized damage in energy-import-dependent economies.

The strait’s share of global oil transit makes it the single most consequential chokepoint for energy-dependent equity markets worldwide.

When that chokepoint closes, the damage flows through a specific sequence:

The result is a differentiated equity impact: regions with high energy import dependence suffer earnings downgrades and lose their monetary policy safety net simultaneously, while regions with domestic energy production absorb a smaller share of the shock.

BCA’s AI upgrade illustrates the other side of this framework. The hyperscaler capital expenditure cycle operates as corporate-to-corporate spending that does not depend on consumer health, making it what BCA termed an “endogenous” growth driver, insulated from the supply shock mechanism. As of 28 April 2026, Al Jazeera reported that commercial shipping viability through the Strait remained a live, unresolved question.

BCA’s 1 May 2026 moves formalise a structural shift in how geopolitical risk translates into equity positioning. The Hormuz crisis has demonstrated that a single supply shock does not produce uniform global repricing; it creates regional winners and losers based on energy dependence, monetary policy flexibility, and domestic production profiles.

Earlier in 2026, BCA identified a “wall of worry” dynamic: investor positioning had been reduced since the conflict began, leaving capital on the sidelines. If the Hormuz situation resolves, that sidelined capital could re-enter equity markets rapidly, providing an upside catalyst that partially reverses the bearish regional calls. The firm also noted the current U.S. administration’s sensitivity to equity market declines as an additional factor tilting return probabilities to the upside.

The unresolved status of commercial shipping through the strait, as reported by Al Jazeera on 28 April 2026, remains the single variable most likely to trigger further rating revisions in either direction. Correa’s suggestion that AI-related equities could see a “sharp, accelerating rally” provides a partial offset to regional headwinds, but the broader question of whether the Hormuz closure persists or resolves will determine whether BCA’s current positioning holds or requires another recalibration.

BCA Research’s coordinated rating changes reflect a disciplined, evidence-based view that geopolitical supply shocks do not damage all equity markets equally. The specific positions, EU underweight, Australia neutral, U.S. neutral, and Communication Services overweight, represent a risk-adjusted response to a crisis whose resolution remains uncertain.

The Strait of Hormuz remains the single most important variable to monitor. BCA has stated its openness to further revisions if conditions shift, whether toward escalation or resolution. Investors following these developments should recognise that the firm’s regional cuts are tactical moves within a broader 2026 framework that remains constructive on U.S. equities and selectively aggressive on AI exposure.

For investors deciding how to act on BCA’s repositioning signals without making reactive trades around individual headlines, our comprehensive walkthrough of geopolitical investing strategy covers the behavioural research on why active trading during high-attention geopolitical events consistently underperforms buy-and-hold approaches, with historical S&P 500 outcome data from three prior oil-above-$100 episodes and a practical framework for separating systematic rebalancing from headline-driven decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including BCA Research’s S&P 500 targets and earnings projections, are subject to change based on market developments and geopolitical conditions.

As of 1 May 2026, BCA Research rates EU equities at underweight, Australia at neutral, and the United States at neutral, reflecting asymmetric damage from the Strait of Hormuz oil supply shock.

BCA Research downgraded EU equities because Europe's high energy import dependence, smaller strategic reserves, and constrained monetary policy response make it disproportionately vulnerable to the ongoing Strait of Hormuz closure and the resulting oil price surge.

The closure punishes energy-import-dependent regions like the EU and Australia through higher input costs, consumer purchasing power erosion, and reduced central bank flexibility, while the United States is comparatively insulated due to its domestic energy production base.

BCA Research upgraded Communication Services, naming Meta and Alphabet as preferred holdings, because AI-driven hyperscaler capital expenditure is corporate-to-corporate spending that operates independently of the consumer purchasing power squeeze caused by higher energy costs.

BCA Research's base-case year-end S&P 500 target for 2026 is 7,200-7,500, with an upside scenario of approximately 7,700 and a 2026 EPS estimate of $308, figures that predate the Hormuz-driven regional rating changes.