Vance Pulls Out of Iran Talks, Sending Brent Below $80

2 hrs ago

Global energy investment crossed US$3 trillion in 2024, with roughly two-thirds directed at clean energy, grids, and storage, according to the International Energy Agency. That is not a venture capital story. That is a capital expenditure cycle.

Climate technology has undergone a structural shift. What began as a collection of early-stage bets on unproven technologies has evolved into a foundational layer of the global energy and industrial economy. For Australian investors, this transition raises a practical question: how do you evaluate and access a sector that no longer behaves like a growth theme but increasingly resembles infrastructure?

This analysis traces how climate tech matured, what it actually encompasses today, why the investment case has become more durable, and how Australian investors can think about exposure in 2026 and beyond.

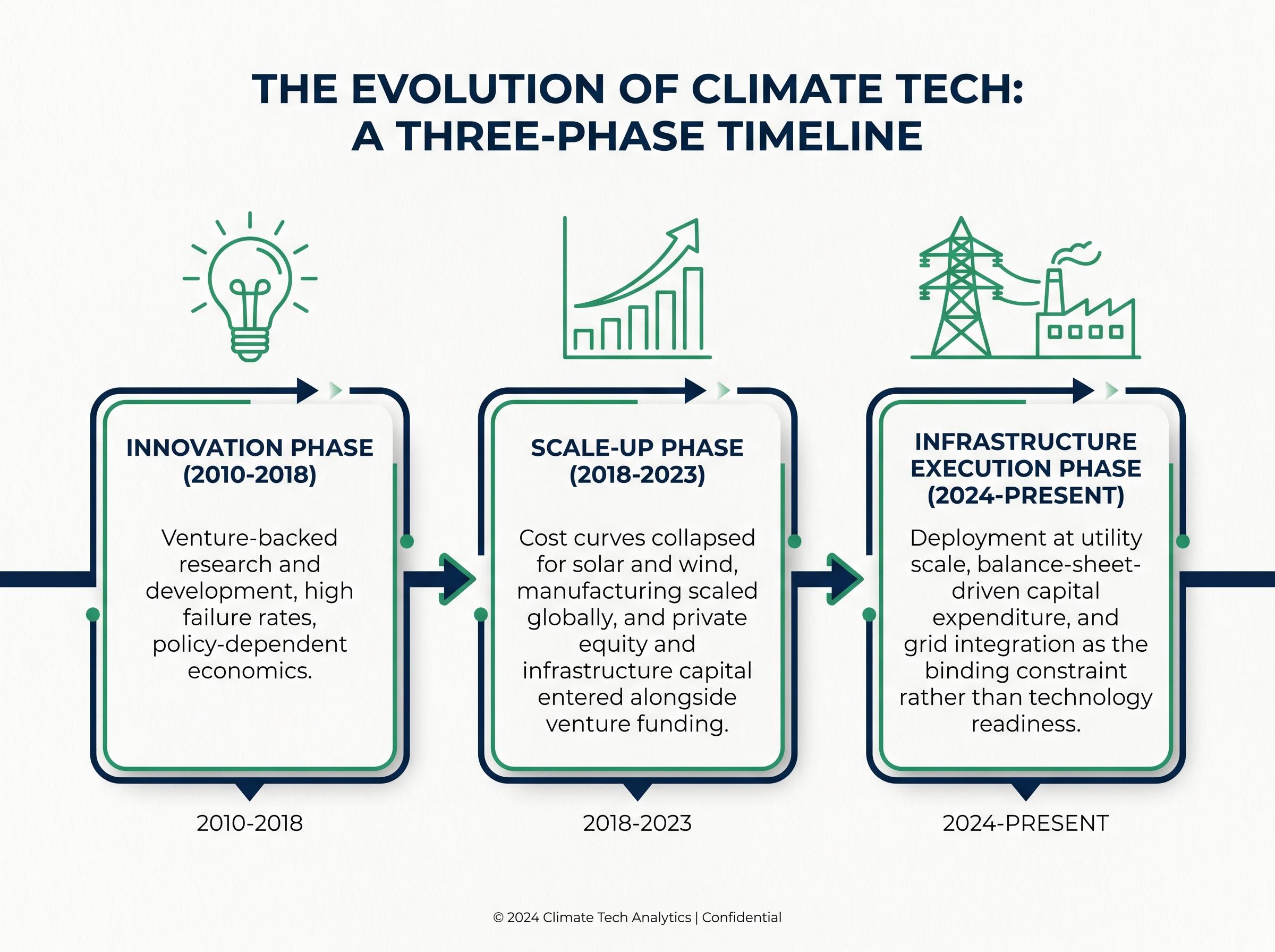

A decade ago, climate tech meant venture capital flowing into unproven battery chemistries, experimental carbon capture rigs, and solar startups competing on technology rather than cost. The capital was small, the failure rate was high, and the sector’s fortunes depended on government subsidies and policy continuity.

That phase is over. The sector’s evolution followed three distinct stages:

The numbers confirm the shift in capital type and scale. Global climate tech venture and growth investment reached $40.5 billion in 2025, up 8% year-on-year according to BloombergNEF. But the larger story sits in total energy investment.

Global energy investment exceeded US$3 trillion in 2024, with approximately two-thirds directed to clean energy, electrification, grid infrastructure, and storage (IEA). The scale of capital now flowing into the sector dwarfs the venture-stage billions that defined its earlier phase.

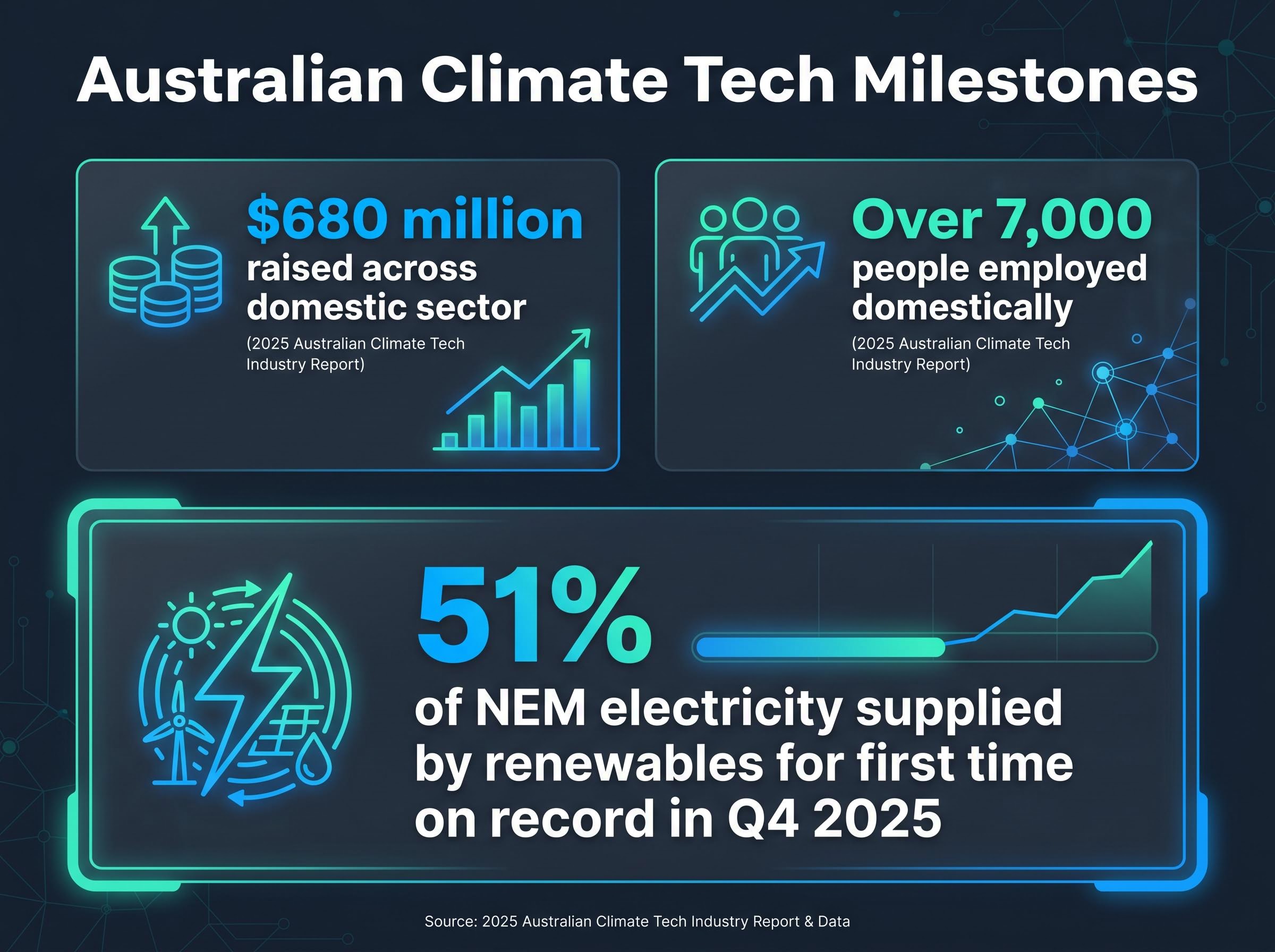

In Australia, the inflection point arrived with a specific data point: renewables supplied over 51% of electricity in the National Electricity Market (NEM) for the first time on record in Q4 2025. When more than half of a country’s grid electricity comes from renewables in a quarter, the sector has moved from disruption narrative to infrastructure fact.

AEMO’s Quarterly Energy Dynamics report for Q4 2025 confirmed that renewables crossed the 51% threshold in the National Electricity Market, providing the official grid data that underpins the sector’s transition from disruption narrative to infrastructure fact.

Climate tech in 2026 spans far more than solar panels and wind turbines. The sector encompasses renewable energy generation, energy storage, electric transport infrastructure, smart grids, low-carbon industrial processes, water management systems, and climate-resilient materials. Understanding this breadth matters because single-technology exposure is a category error when assessing a sector this diverse.

Two broad categories structure the investment landscape: mitigation technologies, which reduce emissions, and adaptation technologies, which build resilience against physical climate impacts. Both are investable, and both carry distinct demand drivers.

| Mitigation Technologies | Adaptation Technologies |

|---|---|

| Solar and wind generation | Water management systems |

| Battery storage | Climate-resilient building materials |

| Green steel production | AI-powered agricultural monitoring |

| Electric vehicle infrastructure | Flood and bushfire defence infrastructure |

| Carbon removal and capture | Heat-resistant urban infrastructure |

The 2025 Australian Climate Tech Industry Report recorded over $680 million raised and more than 7,000 people employed across the domestic sector. The report identified green steel, critical minerals, home electrification, AI-powered agriculture, mid-scale energy generation, batteries, and carbon removal as leading opportunity areas.

Australian climate tech carries a distinctive hardware and manufacturing orientation relative to the broader startup ecosystem. That orientation reflects a different risk and return profile: longer development timelines but more defensible competitive positions once operational.

The most important shift in the climate tech investment thesis is what now drives demand. A decade ago, the sector depended on policy mandates and subsidies. Today, three structural forces underpin the case, and none of them require a favourable election outcome to persist.

AI data centre power demand has become a structural accelerant for clean energy investment independent of climate policy, with Wall Street projecting $530-700 billion in global IT spending on data centres through 2026 and data centres forecast to consume 9% of US domestic electricity by 2030, up from 4% in 2023, creating a demand floor for grid-scale renewables and storage that would persist even if every climate mandate were reversed.

BloombergNEF estimates global energy transition investment needs to average $5.6 trillion annually from 2025 to 2030 for net zero alignment. That figure represents a structural demand floor, not a policy-contingent aspiration.

For Australian investors weighing geopolitical and policy uncertainty, this distinction between policy-driven and economics-driven demand is the most material factor in assessing whether climate tech exposure is structural or discretionary. When the economics work without subsidies, the sector’s revenue base becomes less vulnerable to electoral cycles.

A durable investment case does not mean an absence of risk. Four material risk categories should inform position sizing, vehicle selection, and time horizon rather than serve as reasons to avoid the sector entirely.

Regulatory and approval bottlenecks represent a structural constraint specific to the Australian market. Multi-billion dollar grid upgrade programmes are underway, but timeline uncertainty from regulatory complexity remains a known risk factor. Projects that are economically viable can still face years of delay before generating returns.

Funding access is the second domestic constraint. Approximately 40% of climate tech firms cite funding access as a major barrier to growth, according to the Climate Change Authority’s 2025 report. This affects the risk profile of private and early-stage exposure specifically, where capital-intensive hardware businesses may face longer paths to profitability than software-oriented peers.

US energy and climate policy shifts following the 2024-2025 election cycle have created uncertainty for globally exposed climate tech companies. Australian firms building solutions for international markets carry exposure to trade policy, tariff structures, and foreign subsidy regimes that sit outside domestic control.

Critical minerals supply chain vulnerabilities add a further layer. Australia’s role as a significant critical minerals producer creates opportunity, but global competition for these inputs introduces pricing and availability risks that flow through to manufacturing costs.

The battery materials supply chain sits at the intersection of two structural forces discussed in this analysis: the critical minerals vulnerability that creates input cost risk, and the US policy environment that can simultaneously represent a headwind for exports and a tailwind for domestically positioned manufacturers, as illustrated by NOVONIX’s US$103 million Section 48C tax credit certification for its Tennessee synthetic graphite facility.

| Risk Category | Description | Who It Affects Most | Mitigation Approach |

|---|---|---|---|

| Regulatory bottlenecks | Approval delays on grid and project infrastructure | Infrastructure-phase companies, project developers | Diversify across project stages and geographies |

| Funding access | Capital constraints for early-stage hardware firms | Private and pre-revenue climate tech companies | Favour listed vehicles or later-stage allocations |

| US policy uncertainty | Shifts in trade, subsidy, and energy regulation | Globally exposed climate tech firms | Assess revenue geography; favour domestic-weighted exposure |

| Critical minerals supply | Pricing and availability risks for key manufacturing inputs | Battery, green steel, and hardware manufacturers | Monitor supply chain concentration; consider vertically integrated firms |

Accurate risk pricing is what separates a considered allocation from a thematic bet. Each of these categories has a different mitigation pathway, which should inform how investors structure their exposure.

Understanding the sector’s trajectory and risks leads to a practical question: how do Australian investors actually access climate tech in a portfolio?

The BetaShares Climate Change Innovation and Adaptation ETF (ASX: ERTH) is the primary listed vehicle offering diversified climate tech exposure on the ASX. The fund holds positions across both early-stage innovators and established companies with stronger balance sheets, providing exposure to mitigation and adaptation categories.

Key characteristics of the ERTH ETF include:

Past performance does not guarantee future results. These figures should be verified against the current BetaShares factsheet, as they may vary with market movements.

Direct equities in ASX-listed climate tech companies represent a second pathway. Australian clean energy solutions are increasingly built for global markets, meaning individual ASX-listed names can carry meaningful international revenue exposure. The trade-off is higher concentration risk: a single regulatory setback or technology failure can materially affect a direct equity position in ways that a diversified fund absorbs.

Unlisted infrastructure funds with clean energy exposure offer a third avenue, typically suited to investors with longer time horizons and higher minimum investment thresholds. These vehicles provide access to project-level returns but carry liquidity constraints that listed alternatives do not.

Vehicle selection determines not just return potential but the specific risks being assumed. A diversified listed ETF absorbs regulatory and technology risk across a portfolio. A direct equity position concentrates it. The choice should reflect the investor’s conviction level, time horizon, and tolerance for sector-specific volatility.

The analytical arc of this sector points to a single conclusion: climate tech has crossed from thematic territory into infrastructure territory, and the evaluation lens needs to shift accordingly.

When renewables supply more than half of a national grid’s electricity in a quarter, when global energy investment exceeds US$3 trillion with two-thirds flowing to clean energy, and when multi-billion dollar grid upgrade programmes are underway across Australia, the sector is no longer assessed against innovation-cycle logic. It is assessed against infrastructure-cycle logic, with implications for valuation multiples, time horizons, and portfolio positioning.

Climate tech’s shift from speculative theme to infrastructure backbone requires investors to evaluate the sector through the lens of capital expenditure cycles, not venture capital return expectations.

For Australian investors specifically, the domestic manufacturing orientation and global market exposure of local climate tech firms create a layered opportunity. The 2025 Australian Climate Tech Industry Report’s identification of green steel, critical minerals, and home electrification as leading opportunity areas reflects where Australian-specific value creation is concentrated: at the intersection of the energy transition and the industrial economy.

With investment needing to average $5.6 trillion annually through 2030 according to BloombergNEF, the scale of the build-out is not contingent on any single policy cycle. Investors who continue to price climate tech as a speculative growth bet may be systematically underestimating a sector that increasingly behaves like the infrastructure it has become.

Investors wanting to understand how the infrastructure-cycle framing plays out at the portfolio level will find our full explainer on capital rotation to energy equities useful; it examines how $600-720 billion in projected 2026 big tech capital expenditure is flowing into physical power assets, which utilities are winning custom power contracts, and what the implications are for listed clean energy positions alongside broader infrastructure allocations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Climate tech investing refers to allocating capital into companies and projects that reduce greenhouse gas emissions (mitigation) or build resilience against physical climate impacts (adaptation), spanning sectors from renewable energy and battery storage to green steel, water management, and climate-resilient infrastructure.

Climate tech has shifted from a speculative, policy-dependent theme into an infrastructure-cycle sector, with global energy investment exceeding US$3 trillion in 2024 and solar and wind now cost-competitive with fossil fuels without subsidies in most markets, making the demand drivers more structural than discretionary.

Australian investors can access climate tech through the BetaShares Climate Change Innovation and Adaptation ETF (ASX: ERTH) for diversified listed exposure, direct ASX-listed equities in clean energy companies, or unlisted infrastructure funds with clean energy allocations for those with longer time horizons and higher minimum investment thresholds.

The four main risk categories are regulatory and approval bottlenecks causing project delays, funding access constraints for early-stage hardware firms, US policy uncertainty affecting globally exposed companies, and critical minerals supply chain vulnerabilities that flow through to manufacturing costs.

Renewables supplied over 51% of electricity in Australia's National Electricity Market for the first time on record in Q4 2025, according to AEMO's Quarterly Energy Dynamics report, marking the sector's transition from a disruption narrative to an infrastructure fact.