Why AUD/USD Hinges on the Strait of Hormuz, Not the RBA

3 hrs ago

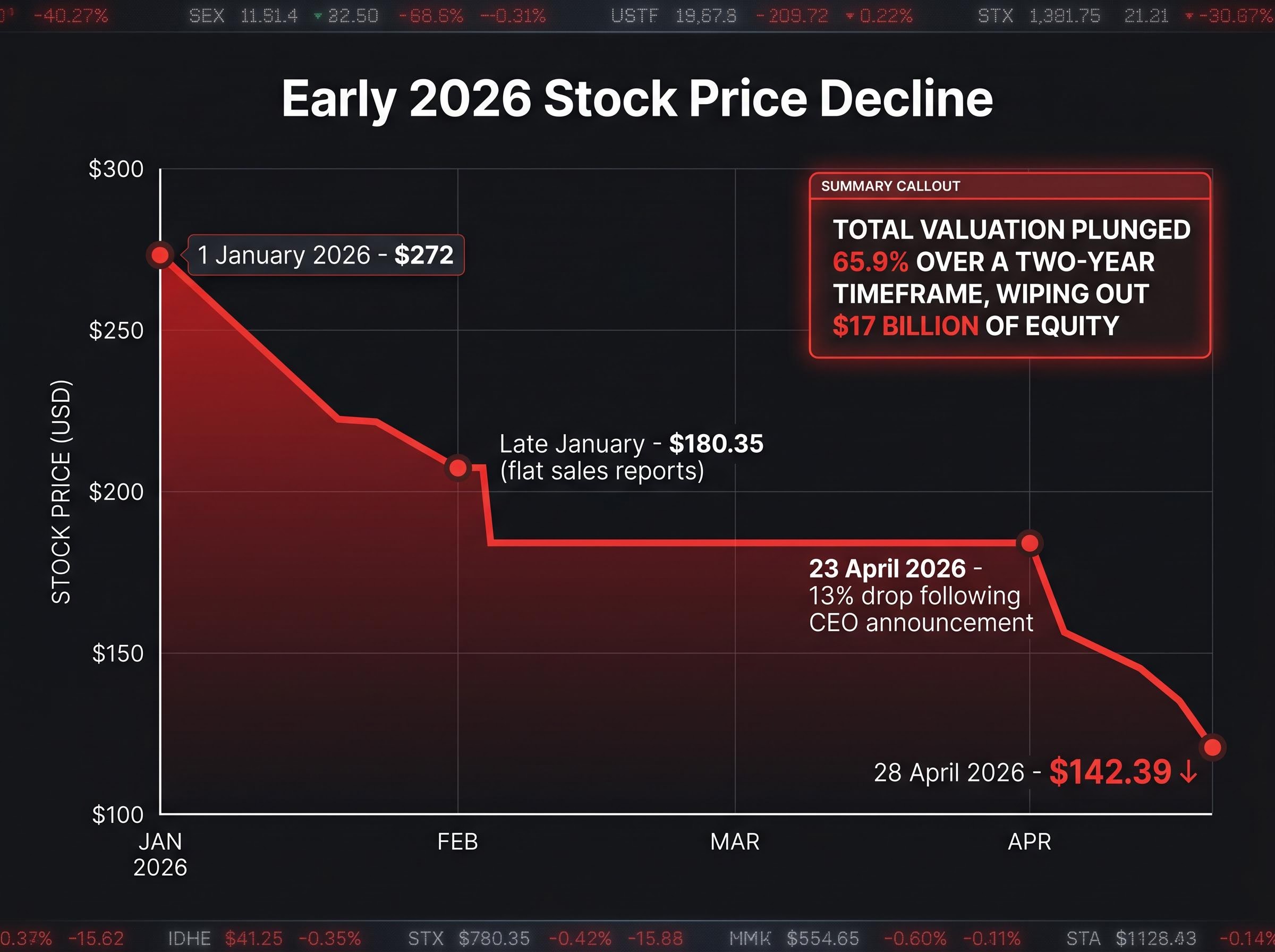

According to reports, a staggering $17 billion in equity value has vanished from one of the most prominent retail names on the market, triggering a fierce Lululemon proxy fight that threatens to completely upend the boardroom. Founder Chip Wilson formally escalated his campaign against the current corporate leadership this week, turning months of private hostility into a very public corporate siege. The battle lines were officially drawn with the board’s preliminary contested proxy statement filed with the Securities and Exchange Commission on 28 April 2026.

This is not merely a frustrated founder venting grievances from the sidelines. The current standoff involves formal SEC filings, allegations of millions in escrow demands, and deep questions about the brand’s fundamental trajectory in the United States. Retail investors are now caught in the crossfire of a deeply personal corporate conflict that will dictate the future of their holdings.

Understanding this conflict requires looking past the daily stock fluctuations. This analysis examines the formidable alternative leadership slate Wilson has proposed, the structural governance issues protecting the incumbents, and the underlying financial collapse driving the campaign.

Wilson did not nominate loyalists; he recruited proven retail and brand heavyweights to lead his corporate siege. The three external candidates put forward for the 2026 Annual Meeting bring distinct operational pedigrees designed to address specific vulnerabilities in the current management structure. The board immediately recognised the threat, urging shareholders to actively block this slate in their 28 April 2026 SEC filing while appointing a new director to solidify their defensive posture.

The challengers present a direct contrast to the current strategy, offering track records of massive equity expansion and aggressive brand scaling. Investors evaluating the viability of this alternative leadership must weigh these specific achievements against the board’s incumbent strategy.

The demand for fresh perspectives stems directly from a historical market capitalisation collapse that saw the company’s valuation plummet from previous highs near $50 billion.

| Nominee Name | Former Enterprise | Key Growth Metric |

|---|---|---|

| Marc Maurer | On Holding AG | Multiplied global sales nearly four times through international expansion |

| Eric Hirshberg | Activision Publishing Inc. | Reportedly oversaw roughly 500% equity valuation growth and doubled earnings |

| Laura Gentile | ESPN Inc. | Built a top-rated, trustworthy sports broadcasting enterprise |

The board claims they attempted good-faith engagements with these nominees before the proxy contest formally began in late 2025. However, the rapid escalation to a contested SEC filing reveals how seriously the current directors view this specific combination of executive talent.

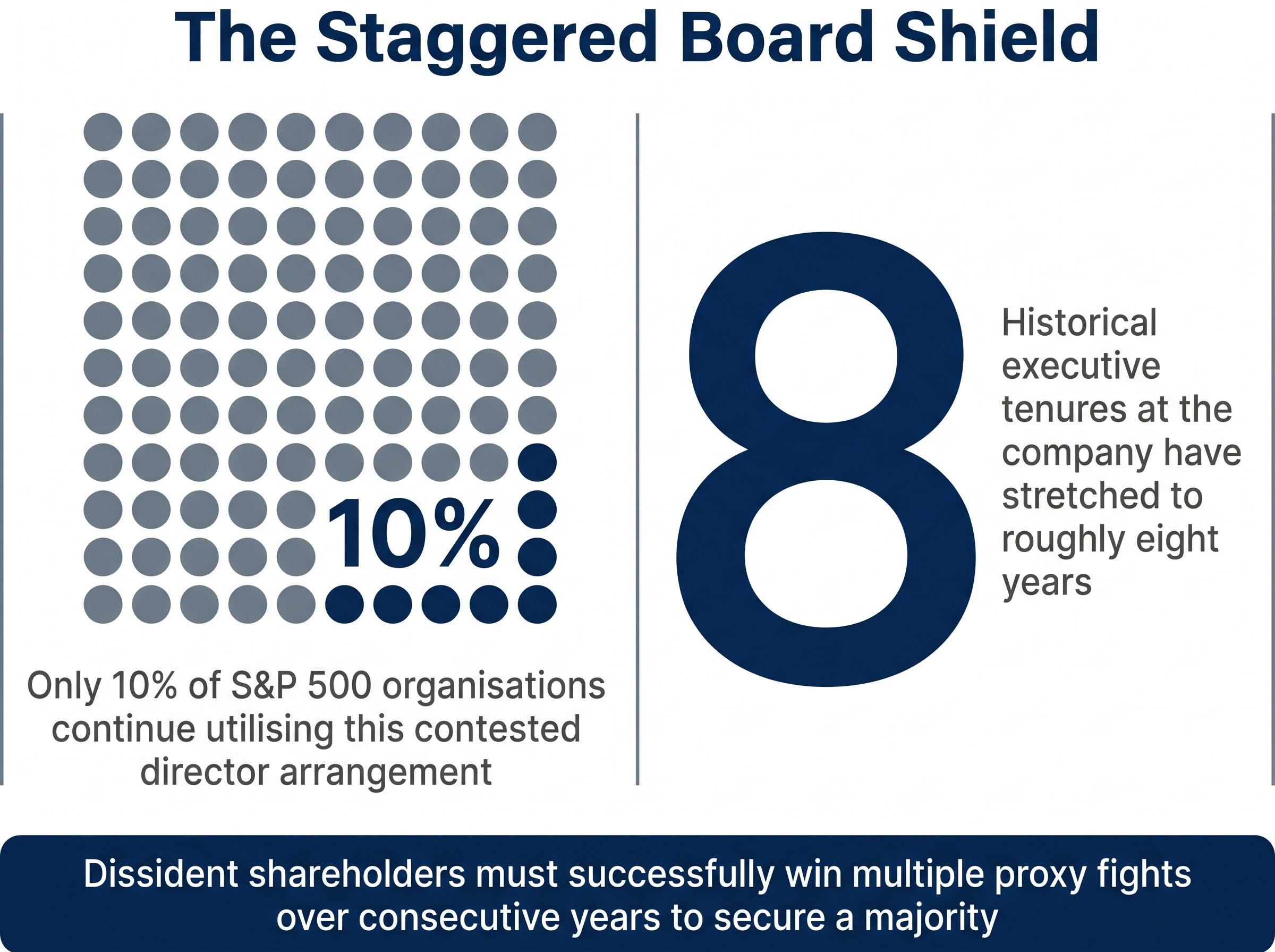

Retail investors often wonder why a founder cannot simply vote out an underperforming board in a single afternoon. The answer lies in a specific, highly contested corporate governance structure known as a staggered board.

A staggered board of directors divides leadership into different classes, with only one class standing for election each year. This mathematical fortress is exactly why sweeping leadership changes take years rather than months to execute. Wilson is directly targeting this arrangement because it serves as an outdated corporate shield, protecting executives regardless of immediate market performance or shareholder sentiment.

According to reports, only 10% of S&P 500 organisations continue utilising this contested director arrangement. The mechanism mathematically guarantees that even a deeply frustrated shareholder base cannot replace an entire board at a single annual meeting:

Extensive corporate governance research confirms this structural shift, demonstrating that maintaining different classes of directors subject to staggered elections is increasingly viewed as an outdated defensive mechanism.

Directors serve multi-year terms rather than facing annual accountability checks. Dissident shareholders must successfully win multiple proxy fights over consecutive years to secure a majority. Corporate incumbents can wait out activist campaigns, hoping investor fatigue sets in before the next election cycle. According to reports, historical executive tenures at the company have stretched to roughly eight years, highlighting the insulating effect of the structure.

Understanding this mechanism reveals why proxy battles are brutal, multi-year endeavours. The staggered structure protects the incumbents, making Wilson’s strategic targeting of specific seats this year an important first step in a much longer war.

The structural friction of the boardroom has recently devolved into intense personal animosity. Settlement negotiations between the founder and the current corporate leadership collapsed dramatically this spring, revealing a deeply fractured relationship. Wilson aired specific, explosive grievances in an open shareholder letter published on 29 April 2026.

This public correspondence accompanied a formal Schedule 14A definitive proxy statement outlining his specific board nominations, which provides a clear regulatory record of the escalating boardroom conflict.

The core of the dispute centres on alleged financial demands made by the current directors to secure an anti-criticism agreement. This hostile negotiation tactic effectively ended any chance of a quiet resolution between the warring factions.

“The board demanded a $1 million escrow deposit from me simply to secure an agreement that would prevent legitimate criticism of their ongoing strategic failures.”

This alleged demand highlights the depth of corporate dysfunction at the highest levels of the company. Exposing these failed settlements helps investors understand why the founder felt compelled to launch a public proxy campaign rather than seeking a quiet compromise.

Wilson’s grievances extend beyond personal disputes into structural concerns regarding private equity entanglements. According to reports, four current oversight members maintain extensive professional connections with Advent International L.P., a prominent private equity firm with a significant historical footprint in the retail sector.

The founder views this concentration of influence as actively detrimental to independent brand strategy. He argues that these overlapping historical and ongoing professional ties stifle objective oversight, turning the boardroom into a private equity echo chamber rather than an objective strategy hub. The impending withdrawal of the lead director associated with Advent International from upcoming re-elections suggests the public pressure campaign may already be forcing structural shifts.

The boardroom hostility might be dismissed as billionaire infighting if not for the catastrophic equity depreciation validating the founder’s anger. According to reports, total corporate valuation has plunged 65.9% over a two-year timeframe, wiping out $17 billion of equity capitalisation. This severe market underperformance is the primary catalyst driving the shareholder revolt.

The historic premium brand status is now clashing with a stark financial reality. According to reports, comparable retail locations across North and South America have experienced stagnant or shrinking revenue over eight sequential quarters.

This financial decay accelerated rapidly in the first four months of 2026, driven by strategic missteps and controversial leadership appointments:

Numbers do not lie, and the equity destruction gives the challenger slate a powerful argument. Investors can clearly assess that the founder’s drastic actions correlate directly with severe portfolio losses rather than mere ego.

For investors seeking a deeper understanding of the specific financial metrics driving this revolt, our detailed coverage of Lululemon’s brand dilution examines the recent 550 basis point drop in profitability and the company’s proposed 2026 action plan.

The upcoming shareholder vote represents a major juncture for the company’s future direction and its ability to recover lost equity. The stakes are immense, but Wilson’s campaign is currently missing one vital element for guaranteed success. As of late April 2026, the challenger slate lacks formal backing from major proxy advisory firms like Institutional Shareholder Services.

Prosecuting a successful corporate siege is significantly harder without these formal endorsements guiding institutional capital. The market is now waiting to see if major shareholders will break rank and support the external nominees based purely on the sheer scale of recent financial losses.

The next phase requires either the board to prove its new CEO can immediately reverse the revenue stagnation, or for the founder to successfully install his nominees.

Retail competitors facing similar market pressures have recently deployed multi-faceted turnaround strategies focused on store innovation and operational efficiency, setting a high benchmark for the new leadership team.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. These statements are speculative and subject to change based on market developments and company performance.

The Lululemon proxy fight is a public campaign by founder Chip Wilson against the current board and leadership, initiated due to a significant decline in equity value, strategic missteps, and concerns over corporate governance.

Chip Wilson nominated Marc Maurer from On Holding AG, Eric Hirshberg from Activision Publishing Inc., and Laura Gentile from ESPN Inc. as external candidates for the Lululemon board.

A staggered board divides directors into classes, meaning only a portion stand for election annually. This structure makes it mathematically challenging for dissident shareholders to replace the entire board in a single year.

The proxy battle is driven by a 65.9% corporate valuation plunge, equating to $17 billion in lost equity, and eight consecutive quarters of stagnant or shrinking revenue in comparable North and South American retail locations.

The board's announcement of Heidi O'Neill as incoming CEO was controversial because founder Chip Wilson immediately disapproved, and the stock dropped an additional 13% after the news, despite her extensive experience at Nike Inc.