Soft Payrolls, Sticky Wages: the Fed’s Dilemma in 2026

6 hrs ago

Washington cleared the way for Nvidia’s H200 chips to reach some of China’s biggest technology firms. Then Beijing told those firms to wait. On 14 May 2026, Reuters reported that approximately ten Chinese companies, including Alibaba, Tencent, and ByteDance, received U.S. government purchasing authorisations for the H200, only to pull back under reported pressure from Chinese authorities. The development lands in the middle of a Trump-Xi summit in Beijing and days after a bilateral tariff truce, making it one of the most consequential and contradictory moments in the AI chip trade since export controls tightened. What follows untangles what actually happened, why Nvidia shares moved despite zero transactions being completed, and what the standoff means for investors tracking whether the company can reclaim meaningful revenue from its largest former market.

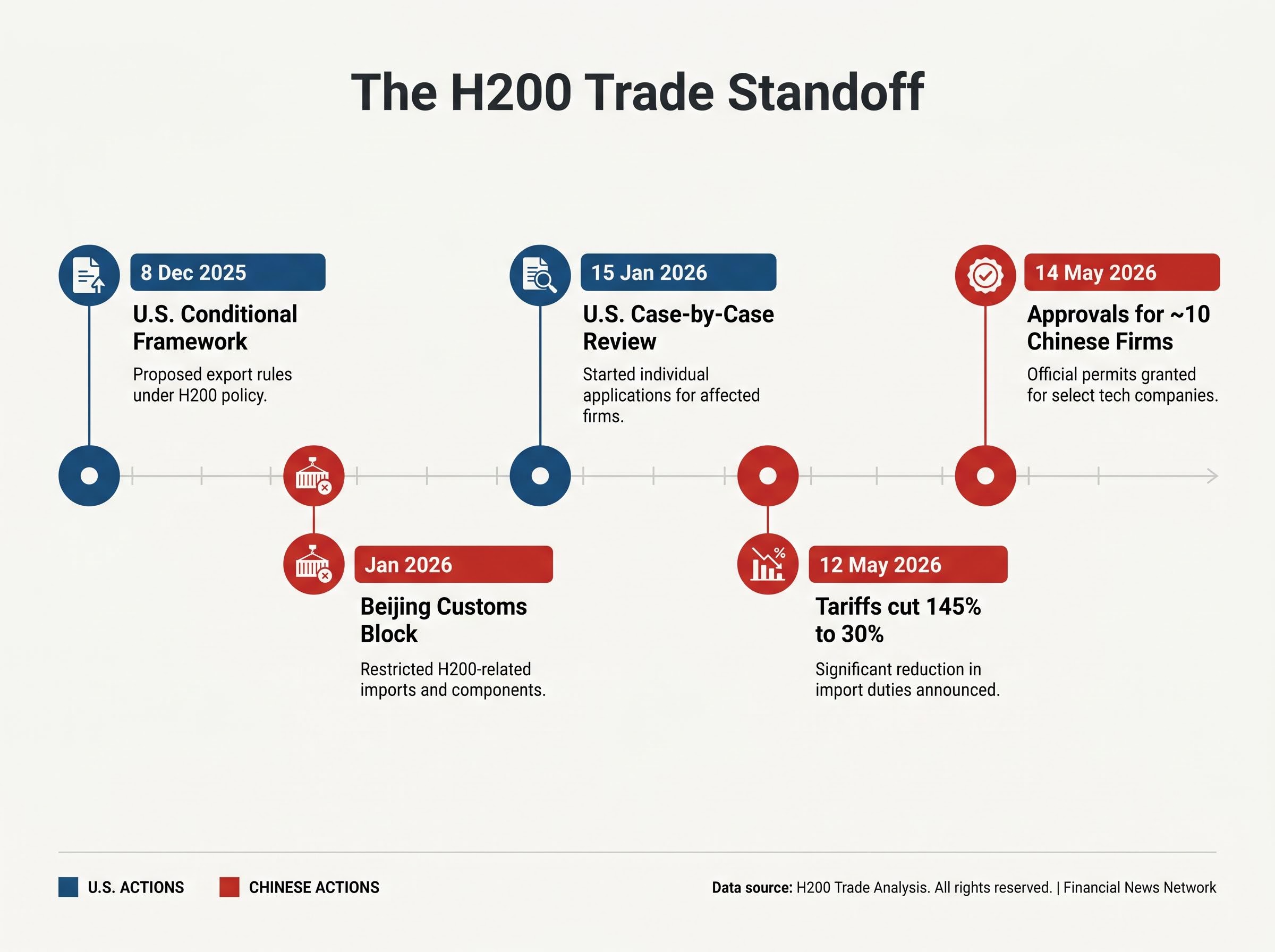

The U.S. approvals are real and not in dispute. Under a conditional framework dating to 8 December 2025, the Bureau of Industry and Security (BIS) cleared approximately ten Chinese firms to purchase Nvidia H200 chips, with per-firm caps reported at up to 75,000 units. Authorised buyers and distributors include:

Lenovo publicly confirmed its approved status. The chips could be sourced directly from Nvidia or through authorised distribution channels.

Then came the complicating layer. Beijing’s customs authority has been blocking commercial H200 imports since January 2026, with exceptions carved out only for universities and government-affiliated research laboratories. Despite U.S.-side clearance, zero H200 shipments have reached Chinese commercial entities.

Commerce Secretary Howard Lutnick confirmed that no sales have been completed as of the report date, attributing the stall to Beijing’s customs-level block rather than any U.S. licensing failure.

The headline reads as progress. The underlying reality has not changed.

The U.S. approval is not a rubber stamp. It reflects a structural policy change that makes Beijing’s refusal to act on it more striking.

Prior to 15 January 2026, BIS reviewed H200 export licence requests to China and Macau under a presumption-of-denial standard, meaning applications were expected to be rejected unless compelling reasons existed to approve them. The same process applies to other sensitive dual-use technology exports and carries legal enforceability.

On that date, BIS shifted to a case-by-case review framework. Trade law analysts at AFS Law assessed the change as substantive rather than symbolic:

The BIS semiconductor export licensing revision, effective 15 January 2026, formalized the policy shift for H200, AMD MI325X, and comparable advanced chips, attaching certification and end-use monitoring requirements to any approved licence rather than treating approval as unconditional.

“Instead of reviewing these license requests under a presumption of denial, [BIS] will instead conduct a case-by-case review.”

The compliance conditions attached to approved licences include:

The distinction matters for investors. The U.S. policy environment is now structurally more permissive than it was six months ago. Whether chips actually flow depends on a decision being made in Beijing, not Washington.

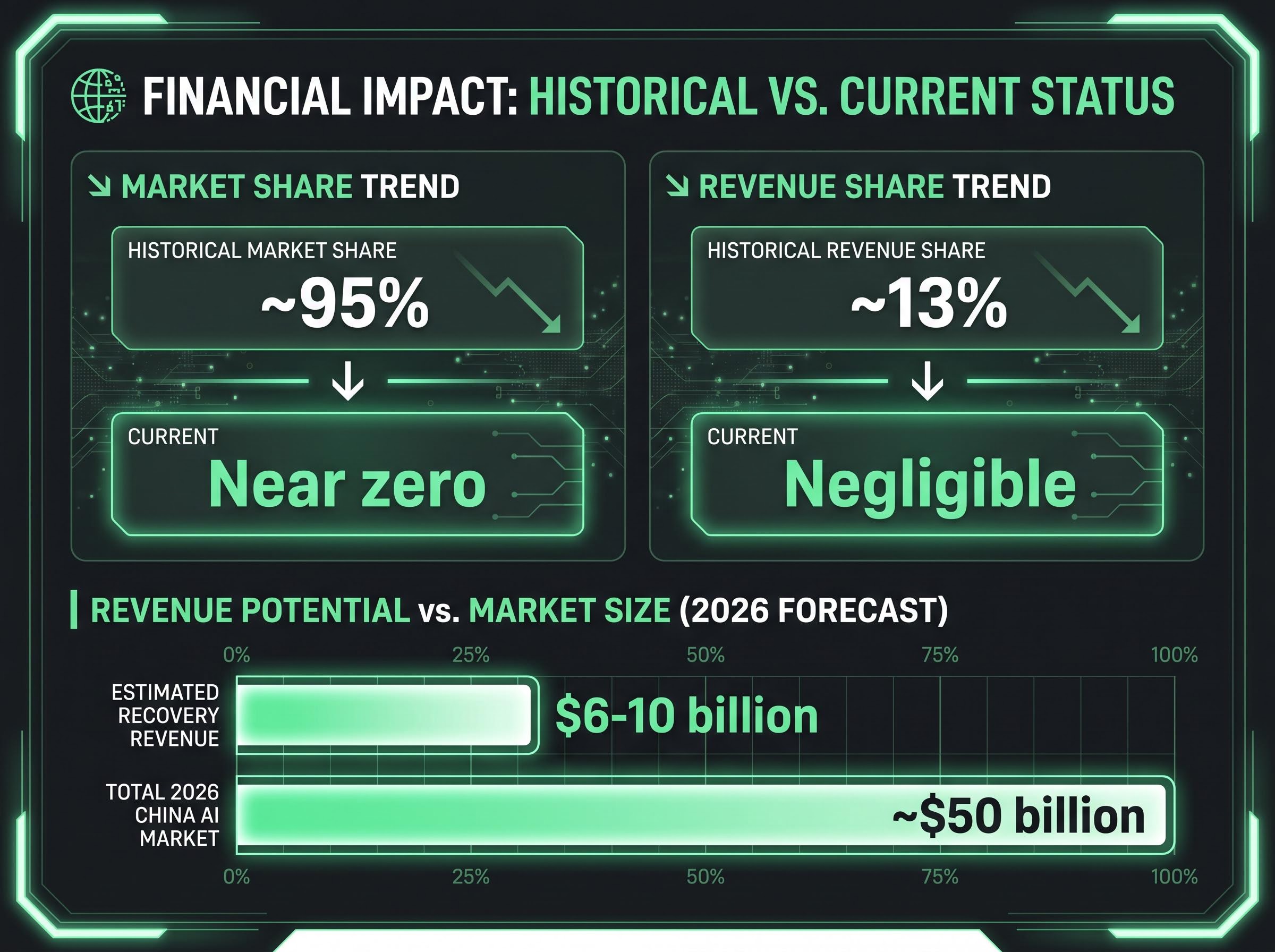

Before U.S. export restrictions tightened, Nvidia held roughly 95% of China’s advanced chip market. China accounted for approximately 13% of the company’s total revenue. Both figures have since collapsed toward zero for advanced-tier products.

Hyperscaler capex commitments of approximately $725 billion for 2026 represent the non-China structural floor underpinning Nvidia’s revenue trajectory; Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, and their combined guidance implies that Nvidia’s data centre order book remains substantially insulated from the China access question.

The table below frames the scale of what is at stake.

| Metric | Historical figure | Current / projected figure |

|---|---|---|

| China market share (advanced chips) | ~95% | Near zero (commercial shipments blocked) |

| China share of Nvidia revenue | ~13% | Negligible (no H200 sales completed) |

| Estimated annual revenue if restrictions ease | N/A | $6-10 billion (Tech Insider estimate, March 2026) |

NVDA closed at $225.83 on 13 May 2026. Reuters reported an approximately 1.8% premarket gain on 14 May, though this figure should be verified against live sources.

Nvidia CEO Jensen Huang has publicly estimated that China’s AI market could be valued at approximately $50 billion in 2026, framing the opportunity as one the company intends to compete for if regulatory conditions allow.

The $6-10 billion annual revenue estimate represents a meaningful recovery but still a fraction of what Huang’s own market-sizing implies. For investors, the gap between the addressable market and the achievable market is where the real uncertainty sits.

Investors exploring why the underlying demand signal is strong even as the commercial access window remains closed will find our full explainer on China’s AI budget timelines, which draws on the Morgan Stanley AlphaWise 1H26 China CIO Survey to show that 47% of CIOs are targeting 2027 for initial AI project rollouts, a data point that reframes the revenue gap as a timing question rather than a demand question.

Expectations ran high heading into the 13-14 May summit. Huang joined the U.S. delegation at Trump’s personal invitation, with the group stopping in Alaska before arriving in Beijing. His presence carried deliberate diplomatic weight: the CEO of the world’s most valuable chipmaker sitting across from the buyers his company cannot currently supply.

The summit’s chip-related developments unfolded in quick succession:

Beijing representatives at Huang’s meetings reportedly emphasised Huawei Ascend alternatives, according to unverified accounts of the discussions.

The reduction from 145% to 30% removes one layer of cost friction and represents a genuinely positive structural development. It does not, however, override Beijing’s separate customs-level block on commercial H200 imports. Even at 30%, the combined tariff burden and the import block make large-scale commercial sales structurally difficult in the near term.

The premarket move in NVDA shares reflected the diplomatic optics. The fundamentals did not change.

The summit pricing disconnect visible in NVDA’s premarket move reflects a broader pattern across the session: the Nasdaq, the Shanghai Composite, and cyclical names all advanced on 13 May on optimism spread across trade purchases, AI security talks, and Iran risk, despite analysts at Fidelity International flagging low expectations for comprehensive agreement on any of those three agenda items.

Beijing’s customs block is not bureaucratic inertia. It is industrial policy with its own logic.

Commerce Secretary Lutnick has characterised the block as a deliberate choice by the Chinese government to promote domestic semiconductor development over dependence on U.S. AI hardware.

Lutnick has publicly stated that China’s government is actively blocking imports in an effort to promote domestic chip development, framing the zero-sales outcome as a CCP industrial policy choice rather than a licensing or logistics failure.

The domestic ecosystem Beijing is building in parallel includes several actors:

The Ministry of Industry and Information Technology (MIIT) has announced policies supporting domestic AI chip development, including subsidies for domestic producers, though specific figures remain unconfirmed through official MIIT communications.

Underlying demand for H200 chips in China remains strong. Units are circulating through informal grey-market channels at significant premiums over U.S. list prices, indicating that the official block is suppressing commercial access without eliminating the appetite for the hardware.

The durability of Beijing’s import block is the single most important variable in any forecast of Nvidia’s China revenue recovery. As long as the block reflects a strategic commitment to domestic self-reliance rather than a negotiating tactic, investors should expect the timeline for meaningful H200 sales to remain uncertain.

The net position for investors is this: U.S. policy is structurally more permissive than it was six months ago. Beijing’s import block is the controlling variable, and it has not changed.

Goldman Sachs maintains a Buy rating on NVDA, characterising recent diplomatic developments as a “short-term catalyst” while acknowledging that Beijing’s block limits upside. The firm’s $165 price target was set prior to current trading levels and should not be interpreted as current guidance. Analyst sentiment is broadly positive on long-term demand fundamentals but cautious on near-term China revenue realisation.

Nvidia’s valuation relative to Broadcom illustrates the market’s unresolved debate over China risk pricing: at approximately 24x forward earnings, NVDA trades at a meaningful discount to Broadcom’s 37x, a gap that partly reflects the market embedding a geopolitical haircut onto Nvidia’s multiple that Broadcom, with its hyperscaler-focused contract revenue, does not carry.

Three signals would indicate the standoff is genuinely shifting:

Until at least one of those signals materialises, the gap between U.S. approval and Chinese access remains open. The stock moved on hope. The investment case still waits on fact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding potential revenue figures and policy developments are speculative and subject to change based on market developments and geopolitical conditions.

The Bureau of Industry and Security shifted from a presumption-of-denial standard to a case-by-case review framework on 15 January 2026, meaning H200 export licence applications to China are now individually evaluated with conditions such as per-firm unit caps and end-use monitoring, rather than being automatically rejected.

Beijing's customs authority has been blocking commercial H200 imports since January 2026, with exceptions only for universities and government-affiliated research labs, meaning Chinese firms like Alibaba and Tencent hold valid U.S. purchasing authorisations but cannot receive shipments because the block operates independently of U.S. licensing.

A March 2026 Tech Insider estimate put the potential annual revenue recovery at $6-10 billion if restrictions ease, though CEO Jensen Huang has sized China's total AI chip market at approximately $50 billion for 2026, suggesting the recoverable figure could be substantially larger over time.

Investors should watch for a formal reversal of Beijing's customs-level commercial import block, public order announcements from approved buyers such as Alibaba or Tencent, and further tariff reductions below the current 30% threshold, as any one of these would represent a material shift in the current stalemate.

Beijing is actively directing cloud operators including Alibaba and Baidu to shift AI workloads to domestic alternatives such as Huawei Ascend chips, while providing subsidies to firms like Biren Technology and Cambricon, which means even if the import block is lifted, Nvidia faces a market that has been deliberately restructured away from U.S. hardware dependence.