Crude Drops 4% on Hormuz Hopes, but the Deal Isn’t Done

28 mins ago

The Nikkei 225 closed above 65,000 for the first time in its history on 25 May 2026, printing an intraday peak of 65,408.87 and delivering a 3.3% single-session gain that rewrote the record books for Japanese equities. The surge was concentrated in semiconductor and AI-linked shares, with spillover from U.S. chipmaker strength arriving into Asian hours via Nasdaq futures even as American cash markets sat idle for a public holiday. Public holidays in Hong Kong and South Korea meant Tokyo carried the regional headline alone. What follows covers the specific stocks that powered the record, the transmission mechanism that brought Wall Street’s AI trade into Japan, how the rest of Asia-Pacific fared on the same day, and the conditions analysts say could unwind the rally.

The numbers bear repeating. The Nikkei 225 reached an intraday high of 65,408.87, a level never previously touched, on a session that saw the index gain as much as 3.3%. The broader TOPIX confirmed the move was not confined to a handful of heavyweight names, hitting its own all-time intraday high of 3,953.89, up as much as 1.6%.

Key index metrics from the session:

The dual record across both indices matters. When the Nikkei rallies on a narrow group of mega-caps, the TOPIX often lags. That both printed new highs on the same session suggests the enthusiasm extended beyond headline AI names into the broader Japanese equity market. For investors tracking Asia-Pacific allocations or Japanese equity benchmarks, a first-ever breach of 65,000 is the kind of event that can trigger benchmark reweighting decisions and fresh inflow cycles.

Japan’s stock market outlook heading into this milestone was already diverging from the bearish narrative circulating in financial media, with Q1 2026 GDP growing at 2.1% annualised on private-sector demand, export volumes up 7.1%, and institutional assessments from the IMF, OECD, and Moody’s treating sovereign debt concerns as a long-run consideration rather than an imminent threat to equity stability.

Strip away the index-level headline and the story narrows to a specific investment thesis. Renesas Electronics (TYO:6723) and Rohm Ltd (TYO:6963) each surged approximately 10% intraday on 25 May 2026, accounting for a disproportionate share of the Nikkei’s advance.

Neither stock moved on fresh earnings releases or formal guidance upgrades that day. The gains were momentum-driven, grounded in a re-rating of both companies against multi-year demand curves rather than a single quarterly data point.

A Tokyo-based tech analyst at a domestic brokerage, quoted in Nikkei Asia, stated that “Rohm and Renesas are being re-rated not on today’s earnings but on multi-year AI and EV demand curves,” characterising the 10% moves as “momentum-driven but grounded in a credible capex story.”

The common catalysts cited across both names:

That distinction, between a momentum trade riding a credible capital expenditure story and a move anchored in fresh fundamental evidence, is worth holding onto. It shapes how investors should assess the durability of these gains if the AI narrative pauses or if U.S. chip earnings disappoint in coming quarters.

The AI capex cycle driving Renesas and Rohm is the same force that has powered the Phlx Semiconductor Index roughly 66% year-to-date through May 2026, with hyperscalers including Microsoft, Google, Amazon, and Meta committing a combined approximately $725 billion in 2026 capital expenditure explicitly directed toward agent-driven inference infrastructure.

U.S. cash markets were closed on 25 May 2026. Yet Japanese chip stocks moved as if Wall Street had just delivered a blowout earnings night. The mechanism was specific and worth understanding, because it will repeat.

Nasdaq 100 futures rose more than 1% during Asian trading hours, extending overnight U.S. AI and semiconductor gains into the session. Those futures became the only live American signal available to Asian desks, and they were enough. Foreign investors, already positioned in Japanese semiconductors as a complementary vehicle to ride the U.S. AI theme, used the futures move as confirmation to add exposure.

A regional strategist at a global bank, quoted by CNBC, described the dynamic directly: “The feedback loop between Wall Street’s AI trade and Asia’s semiconductor complex is now very tight; gains in U.S. chip names translate almost one-for-one into flows into Japanese, Korean, and Taiwan tech.”

A Daiwa Securities strategist, via Nikkei Asia, called the move “a classic AI-chip momentum leg” and described Japan as offering “a diversified way to play AI hardware, including power semiconductors, specialty materials and manufacturing equipment, rather than just GPU leaders.”

The Daiwa framing matters because it explains why Japan specifically benefits from U.S. AI enthusiasm rather than just mirroring it. Renesas and Rohm are not GPU makers. They manufacture power semiconductors, automotive chips, and components for data-centre power management, the infrastructure layer beneath the headline AI names. When U.S. investors want exposure to AI hardware beyond Nvidia, Japanese chip stocks offer a differentiated entry point. That structural positioning is what turns a single session’s futures-driven rally into a recurring pattern: strong U.S. AI earnings translate into Tokyo buying the following morning, and investors who understand this transmission can anticipate the flow rather than react to it.

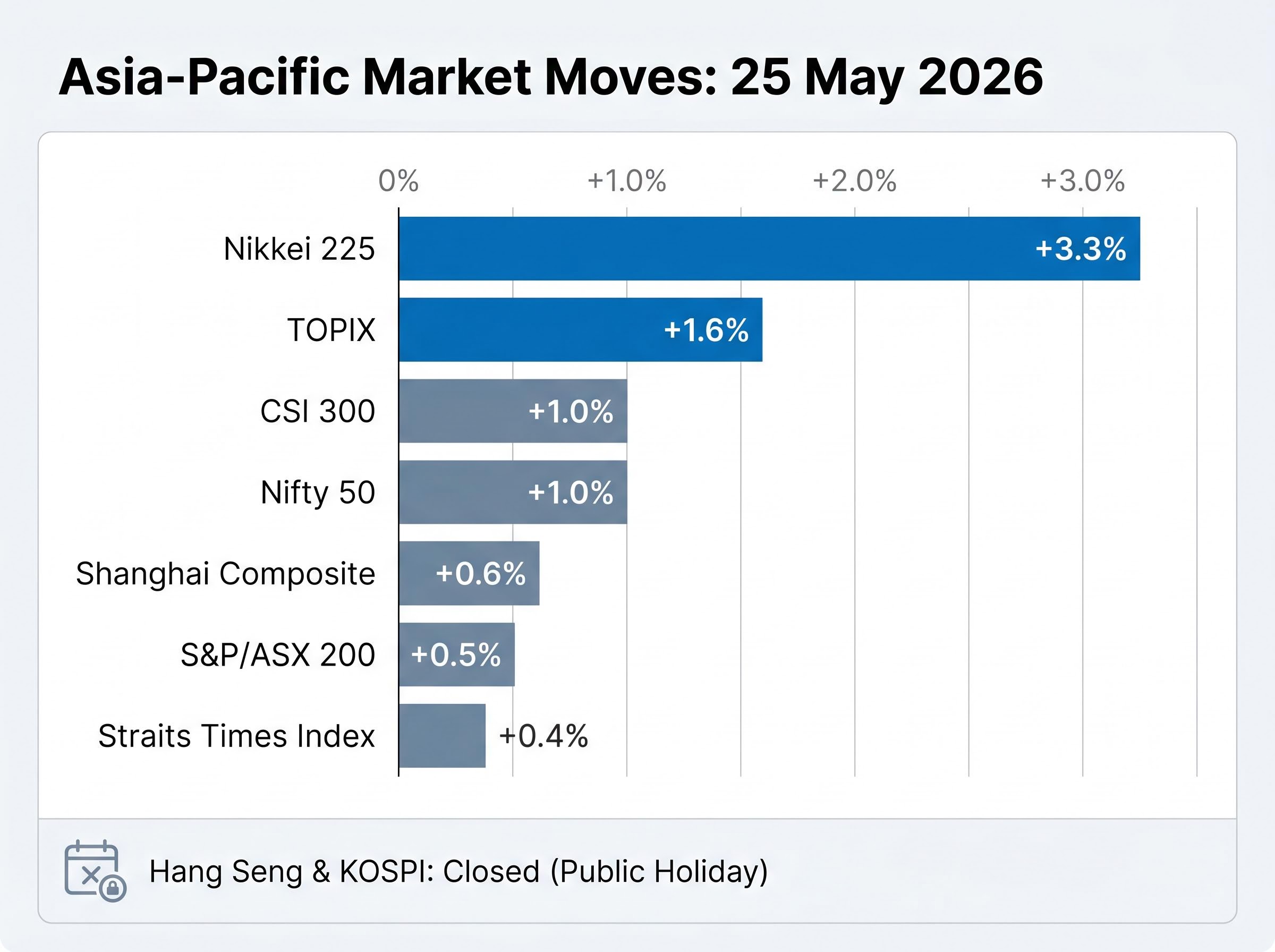

The rally extended beyond Tokyo, but unevenly. Gains across the region ranged from modest to moderate, and two of Asia’s largest markets were absent entirely.

| Market | Index | Approximate Move (25 May 2026) |

|---|---|---|

| Japan | Nikkei 225 | +3.3% |

| Japan | TOPIX | +1.6% |

| China | Shanghai Composite | +0.6% |

| China | CSI 300 | +1.0% |

| Australia | S&P/ASX 200 | +0.5% |

| Singapore | Straits Times Index | +0.4% |

| India | Nifty 50 | +1.0% (early trading) |

| Hong Kong | Hang Seng | Closed (public holiday) |

| South Korea | KOSPI | Closed (public holiday) |

Hong Kong and South Korea, two of the region’s most tech-heavy markets, were closed for public holidays. Their absence limits the breadth signal: a full reading of how Asia’s semiconductor complex digested the U.S. AI impulse will only arrive when those markets reopen.

An additional tailwind arrived from the energy side. Brent crude fell more than 4% to below $100 per barrel on headlines suggesting progress in U.S.-Iran Strait of Hormuz talks, compressing the geopolitical risk premium. For energy-importing economies across Asia, lower oil prices function as a de facto stimulus. HSBC‘s Asia-Pacific equity strategy team, via Nikkei Asia, noted lower oil as a net regional positive but cautioned that valuation dispersion is widening between AI-linked shares and traditional cyclicals.

Records invite optimism. The analysts covering this one are distributing it carefully.

Morgan Stanley‘s Asia strategy team, via Reuters, warned that “positioning is getting crowded in certain chip names.” The firm identified stickier-than-expected U.S. inflation and any renewed spike in energy prices, should Middle East talks stumble, as the conditions most likely to undercut the rally.

Crowded positioning in AI names is not a risk unique to this session: Wolfe Research identified U.S. equity positioning at its most concentrated levels since late 2021 in the week before the Nikkei record, with a yen carry trade unwind, AI capex disappointment, and persistent inflation all listed as compounding tail risks that would pressure the same semiconductor complex now driving Tokyo’s gains.

Goldman Sachs‘ Japan equity strategy note, summarised in the Financial Times, framed AI-related capital expenditure and structurally higher semiconductor demand as the catalyst, with corporate governance reforms and rising return on equity providing a supportive backdrop. The tone was constructive but conditional.

Nomura, via CNBC, said the AI impulse can remain a powerful driver through 2026 while recommending investors watch for policy shocks from the Federal Reserve, Bank of Japan normalisation risks, and election-related volatility across Asia-Pacific.

ANZ Research, via the Financial Times, characterised the overall environment as “a constructive, but fragile, risk-on phase.”

The risk factors identified across these desks cluster around a specific set of triggers:

Taken together, these represent a monitoring framework rather than a sell signal. The rally’s foundations, AI capital expenditure, governance reform, and lower oil, remain intact. The question is whether the conditions that support them will cooperate.

The Nikkei 225’s breach of 65,000 sits at the intersection of three forces: a global AI capital cycle channelling hardware demand into Japanese semiconductor names, Japan-specific governance reforms raising the investability of the market for foreign funds, and a macro tailwind from falling oil prices that benefits Asia’s import-dependent economies.

None of those forces exhausted themselves on 25 May 2026. The AI capex cycle has years of projected build-out ahead. Governance reforms are structural, not cyclical. And the oil price decline, if the Iran negotiations hold, could sustain risk appetite across the region.

The tight feedback loop between U.S. AI earnings and Asian semiconductor markets means any major American chip result in the coming weeks will be watched in Tokyo as closely as on Wall Street. The Nikkei’s record is not a one-day anomaly. It is a function of forces that remain in play, with identifiable catalysts and identifiable risks, and investors positioned in either direction will find the next signal in the same places that produced this one.

International developed market valuations sit near multi-decade extremes relative to U.S. Tech, with MSCI EAFE trading at roughly a 50-55% forward P/E discount to the S&P 500 IT sector as of Q1-Q2 2026, a spread that helps explain why institutional managers including BlackRock, Vanguard, and Goldman Sachs have published views favouring rotation toward markets like Japan even as aggregate fund flows remain skewed toward U.S. large-cap growth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

On 25 May 2026, the Nikkei 225 set a new all-time intraday high of 65,408.87, marking the first time in the index's history that it closed above 65,000, with a single-session gain of 3.3%.

Renesas Electronics (TYO:6723) and Rohm Ltd (TYO:6963) each surged approximately 10% intraday on 25 May 2026, driven by momentum tied to global AI and electric vehicle semiconductor demand rather than fresh earnings releases.

With U.S. cash markets shut for a public holiday, Nasdaq 100 futures rose more than 1% during Asian trading hours, acting as the sole live American signal and prompting foreign investors already positioned in Japanese semiconductors to add further exposure.

Analysts at Morgan Stanley, Nomura, and Wolfe Research identified crowded positioning in AI and chip names, stickier-than-expected U.S. inflation, Bank of Japan policy normalisation, a yen carry trade unwind, and fragile U.S.-Iran negotiations as the key risks most likely to pressure the rally.

Gains across the region were modest and uneven: China's CSI 300 rose roughly 1.0%, India's Nifty 50 gained approximately 1.0% in early trading, Australia's ASX 200 added 0.5%, and Singapore's Straits Times Index rose 0.4%, while Hong Kong and South Korea were closed for public holidays.