Australia Sheds 19,000 Jobs as Unemployment Climbs to 4.5%

2 hrs ago

At the start of 2026, Wall Street’s consensus pointed firmly toward Federal Reserve rate cuts. Strategists mapped timelines, traders positioned for easing, and the conversation centred on how many reductions the year would deliver. By the final week of May 2026, that consensus had inverted. Futures markets flipped to pricing in at least one rate increase before year-end, a reversal driven not by a single data point but by a convergence of forces: an escalating conflict with Iran lifting oil prices, inflation readings re-accelerating well above the Fed’s 2% target, and four senior Fed officials breaking from their prior neutrality within a narrow five-day window. The April 2026 Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, is scheduled for release on 28 May 2026 and could either validate or disrupt the hawkish pivot. What follows unpacks why the reversal happened, what the Fed’s own communications revealed, and what practical steps investors can take to position portfolios for a world where the next rate move may be up, not down.

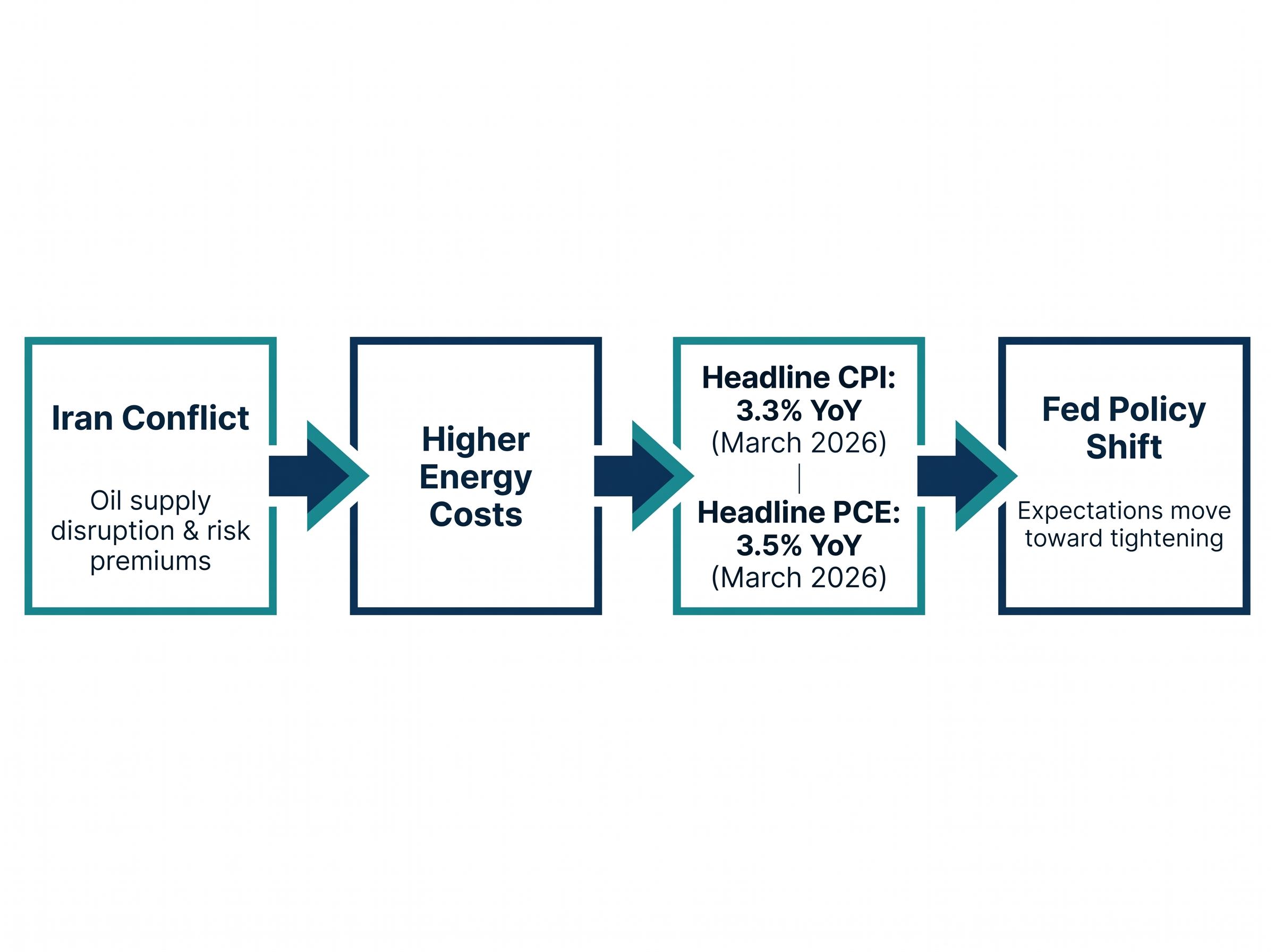

The chain runs in one direction and it runs quickly. Military escalation between the United States and Iran disrupted global oil supply routes. Elevated crude prices fed into transportation, manufacturing, and consumer goods costs across the U.S. economy. Those costs showed up in the inflation data that the Federal Reserve uses to set monetary policy.

The Hormuz supply disruption has removed an estimated 17-20 million barrels per day from global seaborne flows, a scale without modern precedent, and the competing forces of increased Venezuelan exports, higher U.S. rig counts, and OPEC+ production adjustments have so far acted as a partial price ceiling that explains why Brent has not yet exceeded $120 despite the severity of the closure.

The transmission mechanism follows three channels:

The numbers confirmed what the supply chain was already signalling. Headline CPI reached 3.3% year-over-year as of March 2026, according to the U.S. Treasury’s Borrowing Advisory Committee (TBAC) statement of 4 May 2026, up from 2.4% a year earlier. Headline PCE hit 3.5% year-over-year over the same period, per Welch and Forbes.

“The inflationary impact from the war with Iran is showing up in the latest economic data.” — Welch and Forbes, Economic Outlook, May 2026

Not everyone reads the data the same way. The Treasury’s TBAC framing emphasised resilience, arguing that increased domestic oil production insulates the U.S. economy from energy price fluctuations and that “energy prices should recede following the cessation of conflict in Iran.” Private-sector analysts at Welch and Forbes took a more cautious line, describing the energy-driven inflation spike as likely “transitory if a deal with Iran can be completed” but one that will “challenge the Federal Reserve’s policy committee as they navigate a fine line between its dual mandates.”

That split matters. If the conflict resolves, the inflation case for a hike weakens materially. If it persists, the Fed’s hand may be forced. The 30-year U.S. Treasury yield touched its highest level since 2007 during the week of 22 May 2026, and the 10-year yield reached its highest since January 2025. Both moves were driven by inflation expectations rooted in this energy story.

Between 19 May and 23 May 2026, four senior Federal Reserve officials made public remarks that, taken together, amounted to the most hawkish cluster of communications since the current tightening cycle began.

No single statement declared a rate hike imminent. Each used conditional language. But the cumulative effect of four officials saying variations of the same thing in five days was unmistakable.

| Official | Institution | Date | Key phrase |

|---|---|---|---|

| Loretta Mester | Federal Reserve Bank of Cleveland | 19 May 2026 | “We may have to move rates higher” if inflation re-accelerates |

| Raphael Bostic | Federal Reserve Bank of Atlanta | 20 May 2026 | “A hike is not my base case, but if inflation moves higher from here, we’d have to be open to it” |

| Christopher Waller | Federal Reserve Board of Governors | 21 May 2026 | “Further policy tightening later this year cannot be ruled out” |

| John C. Williams | Federal Reserve Bank of New York | 23 May 2026 | “We would need to consider whether additional firming is appropriate” |

Governor Waller’s language carried the most market weight. His statement that “if inflation does not resume its downward path in the next few months, further policy tightening later this year cannot be ruled out,” delivered at the Peterson Institute for International Economics, was the phrase futures markets responded to most directly, according to CNBC coverage.

The distinction to preserve is that none of these officials named a hike as a base case. The market repricing responded to conditional language and, more importantly, to the removal of any remaining expectation for cuts.

The minutes from the 28-29 April 2026 FOMC meeting provided institutional confirmation. Policymakers expressed increasing concern about price pressures linked to the ongoing Iran conflict. No minutes language explicitly called for a hike, but the documented anxiety over inflation persistence gave the public comments from Williams, Waller, Bostic, and Mester their institutional credibility. The public remarks and the internal record pointed in the same direction.

The FOMC meeting minutes from April 28-29 recorded a unanimous vote to hold at 3.50-3.75%, but the committee’s internal framing described the decision as a data-collection pause rather than an end to the tightening cycle, language that gave the subsequent public comments from Waller, Williams, Bostic, and Mester their institutional credibility.

The PCE price index is the Federal Reserve’s formally preferred measure of inflation, distinct from the more widely reported CPI. The difference lies in weighting: CPI uses a fixed basket of goods and services, while PCE adjusts its weightings based on actual consumer spending patterns. When consumers substitute cheaper alternatives in response to rising prices, PCE captures that behaviour. This makes it, in the Fed’s view, a more accurate reflection of real household consumption.

The Federal Reserve’s PCE inflation target of 2% is measured using the PCE price index specifically because its construction accounts for changing consumer spending patterns, capturing substitution behaviour that a fixed-basket measure like CPI cannot reflect.

Three steps connect the current energy shock to the PCE number investors should be watching:

The most recent data showed headline PCE at 3.5% year-over-year and core PCE at 3.2% in March 2026, up from 3.0% in February, according to Welch and Forbes. Both readings sit well above the Fed’s 2% target.

The gap between core PCE at 3.2% and the Fed’s 2% target represents 120 basis points of overshoot, the widest margin since late 2023 and the metric that gives conditional hike language its credibility.

The April 2026 PCE report is scheduled for release on 28 May 2026 at 8:30 a.m. Eastern Time, according to the Bureau of Economic Analysis. Anthony Saglimbene of Ameriprise has noted that the April data is anticipated to reflect pass-through from months of elevated oil prices into broader consumer prices. An upside surprise would give markets and the Fed more reason to price in a hike. A downside surprise could begin to reverse the hawkish shift.

The bond market, the equity market, and the futures market are each telling a slightly different part of the same story. Read together, they paint a picture of an investment environment repricing in real time.

| Yield measure | Level (approx. 24 May 2026) | Historical context |

|---|---|---|

| 10-year U.S. Treasury | 4.572% | Highest since January 2025 |

| 30-year U.S. Treasury | 5.082% | Highest since 2007 |

Those yield levels represent the bond market’s most concrete expression of inflation repricing. Longer-dated Treasuries have sold off as investors demand higher compensation for holding duration through a period of uncertain inflation and a potentially tightening Fed.

The 30-year Treasury yield at 5.082% is not an isolated U.S. phenomenon: the synchronised global bond selloff has pushed the UK 30-year gilt to a 28-year high near 4.9% and Japan’s 30-year JGB to a record 4%, with four reinforcing drivers, including above-consensus U.S. inflation, elevated energy prices, contagion from rising U.S. term premia, and geopolitical risk, operating simultaneously across every major sovereign market.

The equity market, by contrast, has continued to climb. The S&P 500 is up more than 9% year-to-date as of the week of 22 May 2026, trading near record levels after eight consecutive weeks of gains. That strength has not gone unnoticed by strategists who question its sustainability. Anthony Saglimbene of Ameriprise and Scott Wren of Wells Fargo Investment Institute have both flagged that high expectations for earnings and economic growth are already priced in, reducing the market’s buffer against negative surprises. Jim Baird of Plante Moran Financial Advisors has warned that if the upward trend in long-term yields persists, it could effectively cap broader equity market gains.

Three separate signals tell the story:

The macro backdrop described above points to three practical adjustments, ranked by urgency, that respond to specific risks that have already materialised.

The AI capital expenditure cycle offers a specific reason to favour quality growth over speculative yield. Nvidia’s Q2 revenue guidance of approximately $91 billion exceeded consensus estimates, providing earnings-level confirmation that corporate spending on AI infrastructure remains intact. First-quarter S&P 500 earnings grew at approximately 29% year-over-year, a pace that supports valuations even in a higher-rate environment.

Technology stocks carry their own valuation risk if rates move higher, and that tension is real. But earnings-growth confirmation at this pace provides a degree of fundamental support that speculative or highly leveraged names cannot match. The economist survey cited in the Treasury’s TBAC statement showed an average 33% recession probability over the next 12 months, relatively low and consistent with a Fed that retains room to tighten without triggering a downturn.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The coming weeks present a genuine fork. If the April PCE print on 28 May shows further re-acceleration, the conditional hike language from Williams, Waller, Bostic, and Mester hardens into something closer to a base case. If it shows deceleration, the pause narrative reasserts itself.

“The Federal Reserve’s policy committee [will] navigate a fine line between its dual mandates of maximum employment and stable prices.” — Welch and Forbes, Economic Outlook, May 2026

The resolution of the Iran conflict remains the wild card that neither the Fed nor investors can time, and that uncertainty argues for defensive positioning regardless of which PCE outcome materialises.

For investors who want to go deeper on the structural asset allocation implications of a world where bonds and equities can fall simultaneously, our full explainer on portfolio resilience beyond the 60/40 framework walks through Bridgewater’s economic environment diversification approach, a three-tier adaptive portfolio structure, and the specific tools available to retail investors for replicating institutional-grade dynamic allocation.

Three triggers will move markets materially in either direction from here:

One thing is clear regardless of which path unfolds: the era of expected cuts is over for 2026. The gap between core PCE at 3.2% and the Fed’s 2% target must narrow before any easing can be considered. Every portfolio decision from here should be made against that backdrop.

The PCE (Personal Consumption Expenditures) price index is the Federal Reserve's preferred inflation gauge because it adjusts its weightings based on actual consumer spending patterns, capturing substitution behaviour that the fixed-basket CPI measure cannot reflect. The Fed targets 2% inflation as measured by PCE.

A combination of Iran conflict-driven oil supply disruptions, re-accelerating inflation (headline PCE at 3.5% and core PCE at 3.2% as of March 2026), and hawkish public statements from four senior Fed officials in a five-day window have pushed futures markets to price in at least one rate hike before year-end, reversing earlier expectations for cuts.

Between 19 and 23 May 2026, four senior Fed officials including Governor Christopher Waller and New York Fed President John Williams each used conditional language suggesting further tightening could not be ruled out if inflation failed to resume its downward path. None named a hike as their base case, but the cluster of hawkish remarks drove significant market repricing.

Analysts recommend shortening fixed income duration and using laddered maturities to limit exposure to rising yields, maintaining a quality bias in equities with selective exposure to AI and capital expenditure themes, and holding adequate liquidity to avoid being forced into decisions during volatile conditions.

The April 2026 PCE report, due on 28 May 2026 at 8:30 a.m. Eastern Time, is the single most important data point before the next FOMC decision because an upside surprise would strengthen the case for a Federal Reserve rate hike, while a deceleration could begin to reverse the hawkish shift in market pricing.