Oil Surges to $80 on Iran Crisis, Barclays Warns Against Panic

3 hrs ago

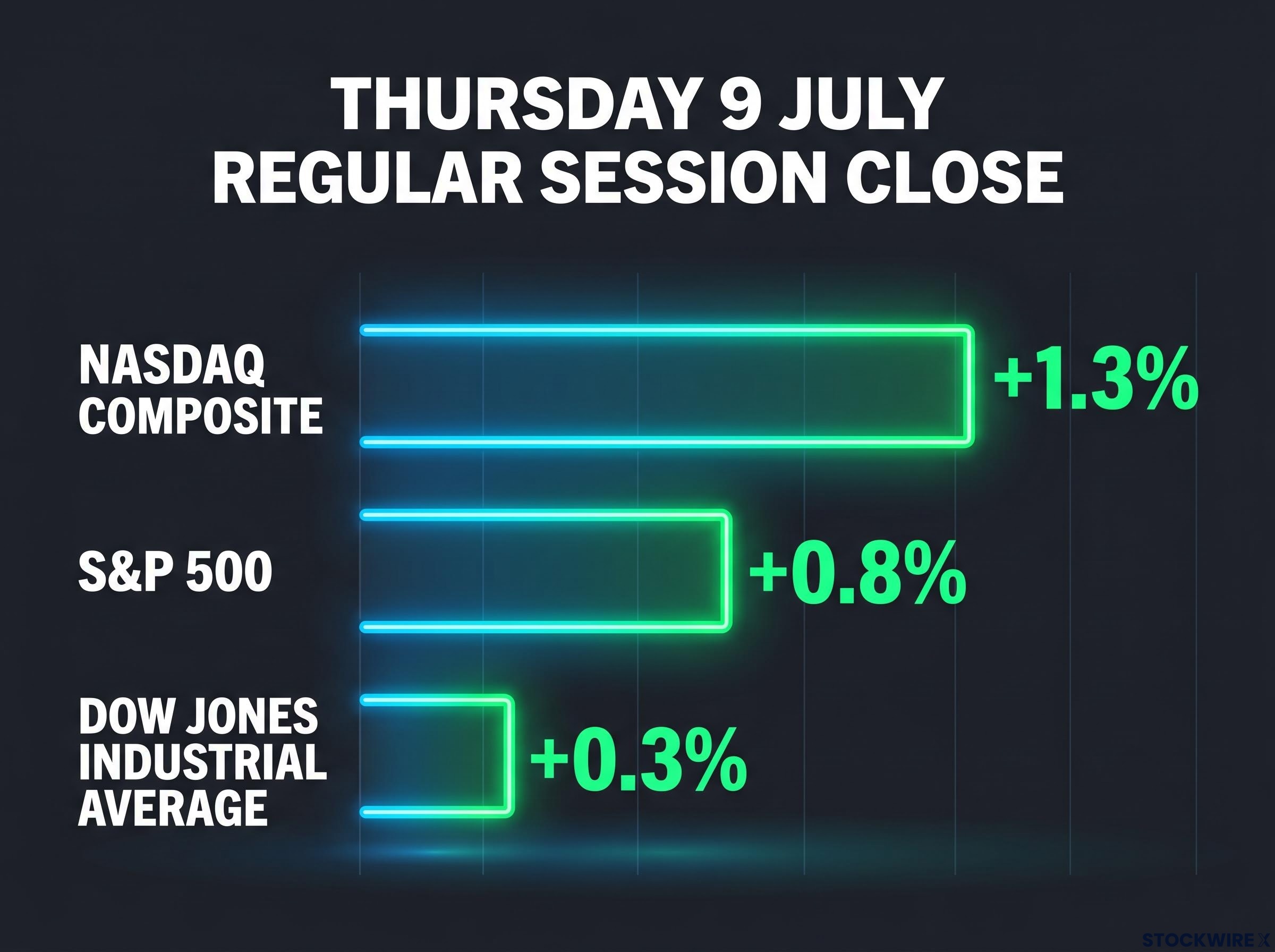

Wall Street closed higher on Thursday 9 July, with the Nasdaq Composite’s 1.3% gain outpacing both the S&P 500 and the Dow, as diplomatic signals between Washington and Tehran shifted the market’s fear calculus overnight. The session’s strongest performers were concentrated in artificial intelligence and semiconductor names, not spread across the broader tape.

That concentration matters. In the days prior, the deepening confrontation between the US and Iran had pushed oil prices sharply higher on fears that crude supply routes could be choked off. Thursday’s reversal came from two converging forces: a geopolitical temperature drop and a semiconductor sector that posted back-to-back gains of roughly 3% on the Philadelphia Semiconductor Index (SOX), a benchmark tracking the largest US-listed chipmakers. AI demand was the fuel under the chip trade.

If you are sitting on AI or semiconductor exposure and trying to work out whether Thursday was a one-day bounce or a resumed uptrend, here is what the session’s data actually tells you about the durability of the AI trade and the risks still attached to it.

The Nasdaq Composite led with a 1.3% advance. The S&P 500 gained 0.8%. The Dow Jones Industrial Average added 0.3%.

That spread is the story. A full percentage point separated the Dow from the Nasdaq, which tells you Thursday was a growth-tilted, AI-specific advance, not a broad risk-on session where capital flowed evenly across sectors. Investors with diversified index exposure participated, but those holding chip and AI-linked equities captured the real move.

After hours, the tape cooled. By 8:40 PM ET, S&P 500 futures were sitting at 7,578.75, down about 0.1%, Nasdaq 100 futures had retreated approximately 0.3% to 29,829.75, and Dow futures were barely moved at 52,738.0. Those are not reversals. They are the market pausing to assess whether Friday’s open confirms the thesis or fades it.

| Instrument | Regular session move | After-hours (8:40 PM ET) |

|---|---|---|

| Dow Jones Industrial Average | +0.3% | Approx. unchanged (52,738.0) |

| S&P 500 | +0.8% | −0.1% (7,578.75) |

| Nasdaq Composite | +1.3% | N/A |

| Nasdaq 100 Futures | N/A | −0.3% (29,829.75) |

| S&P 500 Futures | N/A | −0.1% (7,578.75) |

One 3% session in the Philadelphia Semiconductor Index is a good day. Two consecutive 3% sessions is a statement.

The SOX wrapped up 9 July with another gain of close to 3%, matching the prior session’s advance. A back-to-back move of that magnitude has appeared only a handful of times across 2026, making the sequence notable rather than routine.

When institutional capital re-enters a sector at this pace over multiple sessions, it signals something beyond a short squeeze or a retail-driven bounce. It tells you that large allocators are re-rating the durability of AI-driven demand, not just reacting to a headline. That distinction matters: a short squeeze fades when the covering is done, but an institutional re-rating changes the supply-demand picture for the shares themselves.

The hyperscaler capex commitments underpinning institutional conviction in semiconductor names are running at levels that compress near-term hyperscaler profitability while creating structural pricing power for chip suppliers: Goldman Sachs projects the largest technology companies will collectively spend approximately $770 billion on capex in 2026, equivalent to roughly 100% of their operating cash flow.

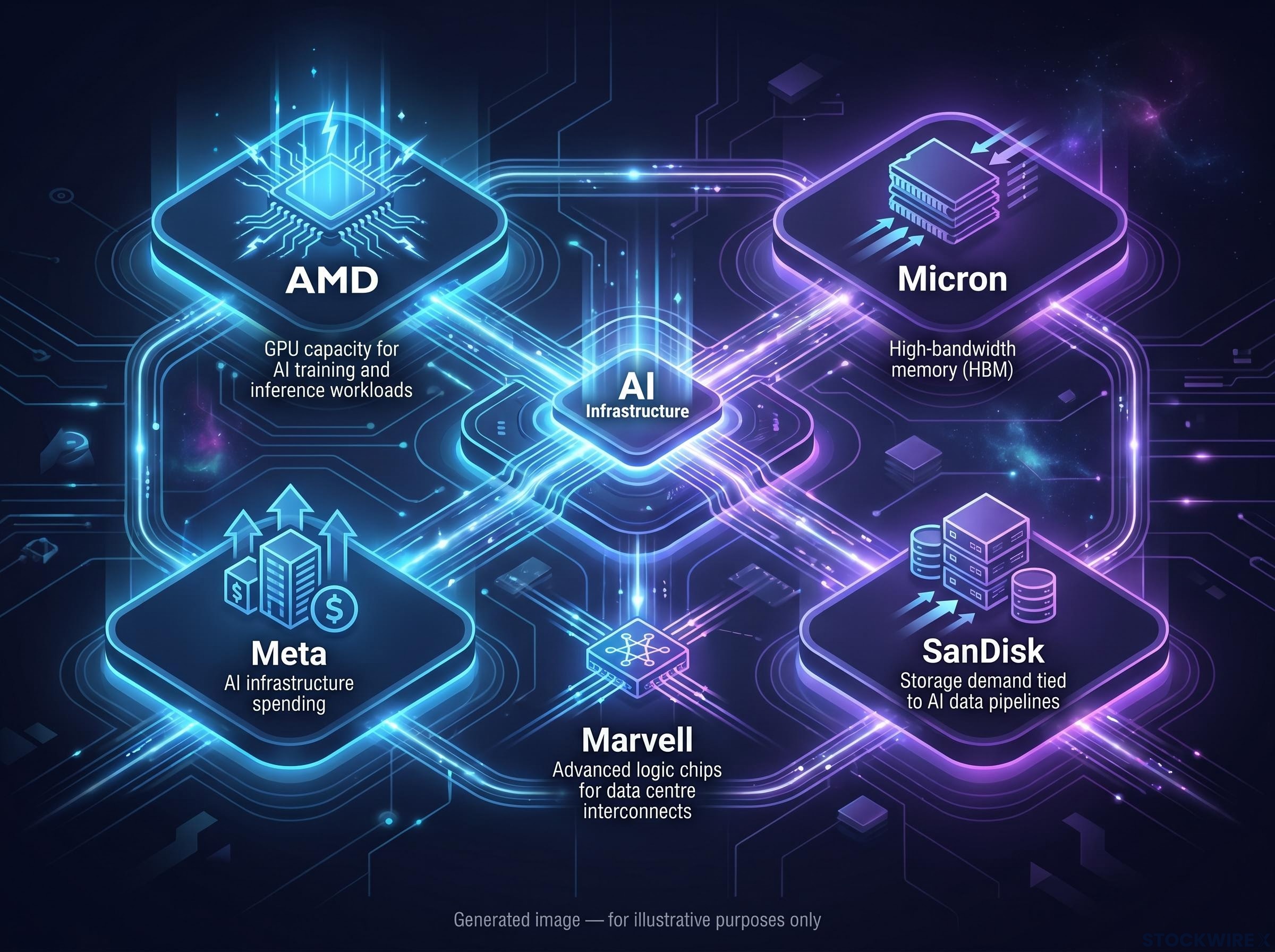

The individual names within the move confirm the thesis:

Each mover is tied to a specific layer of AI infrastructure, not to a single product cycle. For investors already holding semiconductor exposure, two consecutive 3% days is not noise. It signals that institutional conviction is re-entering the trade, which changes the risk-reward calculus compared to a single-day pop.

Thursday’s rally rested partly on a signal, not a deal. That distinction deserves weight before the optimism runs too far ahead of the evidence.

President Donald Trump announced publicly that Iran had made contact with Washington to explore the possibility of talks, a comment that functioned as the geopolitical catalyst for the session’s equity recovery. In the days prior, the mounting tensions between the US and Iran had stoked concerns about potential disruptions to oil flows through the Strait of Hormuz, the narrow passage through which roughly a fifth of the world’s daily oil supply flows. Those fears had driven equity losses in the preceding session.

The mechanism is straightforward. When fear-driven selling precedes a diplomatic signal, even a partial de-escalation allows equity risk premiums to compress rapidly, producing outsized price moves on relatively thin news. Markets were not pricing in peace on Thursday; they were pricing out the worst-case scenario.

This is consistent with the 2026 pattern in which tentative diplomatic signals have repeatedly cooled oil prices and supported growth equities. But the fragility is real. Military exchanges between the two countries continued alongside the negotiation language. If the signal fails to develop into substantive engagement, the Strait of Hormuz risk premium returns to oil prices, and the AI-semiconductor trade faces the same headwind that rattled it days earlier.

The Strait of Hormuz risk premium that markets partially unwound on Thursday has historically re-entered oil prices quickly when diplomatic signals fail to develop into verifiable agreements; state-coordinated shipping transits through the strait have emerged as a real-time diplomatic signal that often moves faster than official statements.

Crude oil pulled back on Thursday, partially reversing the week’s prior spike. That may look like an energy story. For anyone holding AI or semiconductor names, it is a valuation story.

Here is the transmission mechanism, link by link:

The June 2026 FOMC statement confirmed that inflation remains elevated relative to the Fed’s 2 percent target, with energy supply shocks cited as a contributing factor, the precise transmission mechanism that makes oil price swings a direct input to the Fed’s rate calculus.

Thursday’s oil pullback removed one of the clearest near-term threats to the valuation multiples that AI and semiconductor stocks trade on.

A declining VIX (the market’s fear gauge, which measures expected volatility in the S&P 500) reinforced the move. Lower oil and lower volatility together created the benign backdrop that allowed Thursday’s growth stock rally to occur. If either reverses, the support structure shifts.

Thursday’s session did not arrive in isolation. Throughout 2026, a consistent pattern has emerged in AI and semiconductor names, and understanding it reframes 9 July from a standalone event into one instance of a repeating market structure.

The pattern has three structural features:

If you understand that institutional capital has repeatedly treated geopolitical dips in AI names as entry points throughout 2026, you have a framework for interpreting Thursday as pattern confirmation rather than a novel event. That changes how you weight the durability of the current move.

The rally has identifiable foundations. Each one can be tested. Here are the three variables that matter most:

Semiconductor stock valuations within the current rally are not uniform: Micron trades below 9x forward earnings despite HBM revenue growing approximately 300% year-over-year, while other names in the same index carry multiples that exceed their own dot-com-era peaks, a dispersion that matters when assessing which positions carry the most reversal risk if earnings guidance disappoints.

None of these three risks is remote given the conditions that produced Thursday’s rally. If you hold AI and semiconductor exposure, treat this as an active watchlist, not background noise.

What Thursday confirmed:

What remains unresolved:

The three variables that will determine whether next week confirms Thursday or fades it: oil price direction, any follow-up Iran diplomatic developments, and upcoming AI chipmaker guidance. Those are the specific inputs worth tracking, not the headline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

Two forces converged: a diplomatic signal from Iran indicating openness to talks with Washington, which partially unwound the Strait of Hormuz oil-supply risk premium, and a second consecutive roughly 3% gain in the Philadelphia Semiconductor Index driven by institutional conviction in AI infrastructure demand.

The Philadelphia Semiconductor Index (SOX) tracks the largest US-listed chipmakers and serves as a benchmark for the health of the semiconductor sector; back-to-back gains of approximately 3% in the SOX signal that large institutional allocators are re-rating AI-driven demand as durable, not just reacting to a single headline.

Higher oil raises inflation expectations, which pressures the Federal Reserve to keep rates elevated or hike further; higher discount rates then compress the future-earnings multiples that AI and semiconductor companies trade on, pushing their stock prices lower even without any change in their underlying business performance.

The session's notable movers included AMD (GPU capacity for AI training and inference), Micron (high-bandwidth memory for AI servers), Marvell (advanced logic chips for data centre interconnects), Meta (as an AI infrastructure demand signal), and SanDisk (storage demand tied to AI data pipelines).

The three key risks are a US-Iran re-escalation that spikes oil and narrows Fed rate flexibility, a high-profile earnings miss or cautious guidance from a leading AI chip supplier that tests whether institutional conviction is earnings-supported, and an inflation data surprise or Fed communication shift that raises discount rates and compresses growth stock multiples.