Trump Tears Up Iran Deal as Oil and Rate Markets Reprice

19 hrs ago

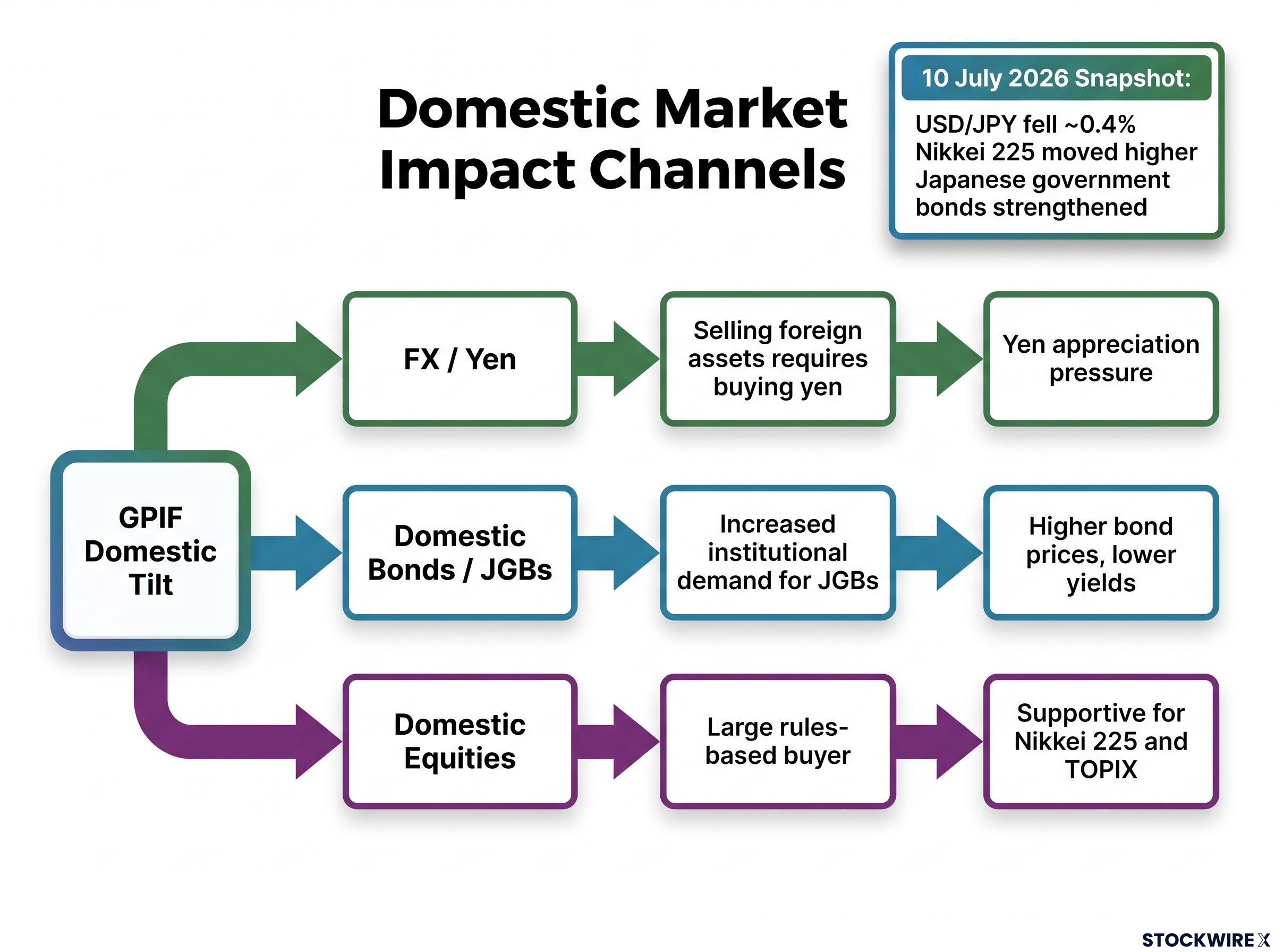

Japan’s Finance Minister Satsuki Katayama announced on 10 July 2026 that the government intends to redirect the country’s pension funds toward domestic assets. Within the same session, USD/JPY fell approximately 0.4%, the Nikkei 225 pushed higher, and Japanese government bonds strengthened. Markets did not wait for a policy document to decide this matters.

Standing at the heart of this story is the Government Pension Investment Fund (GPIF), the world’s single largest pension fund, with assets approaching $2 trillion and an overseas allocation that accounts for around half of its total portfolio. Even a modest reweighting at that scale carries structural consequences for the yen, Japanese asset prices, and global capital flows, including demand for U.S. Treasuries. The government’s “Honebuto” Basic Policy framework, scheduled for release on 21 July 2026, represents the next concrete milestone markets are watching.

Here is what the mechanics actually look like, what is already in motion, and which signals will confirm whether this is a structural shift or a policy trial balloon.

Finance Minister Satsuki Katayama did not float the idea through a parliamentary committee or a background briefing. The announcement came directly, and currency, equity, and bond markets responded in unison within the same session.

Same-session market snapshot, 10 July 2026: USD/JPY fell approximately 0.4%. The Nikkei 225 moved higher. Japanese government bonds strengthened.

That triple reaction is the credibility signal. Traders read this as a near-term policy direction rather than aspirational commentary, and the speed of the response is what separates a ministerial signal from a think-tank white paper.

The announcement did not arrive in a vacuum. Ruling-party lawmakers had already been urging GPIF to increase domestic private equity and venture capital exposure as part of a broader push to turn Japan into an “asset management nation.” Katayama’s statement converts a background discussion into a named policy priority, and the market treated it accordingly.

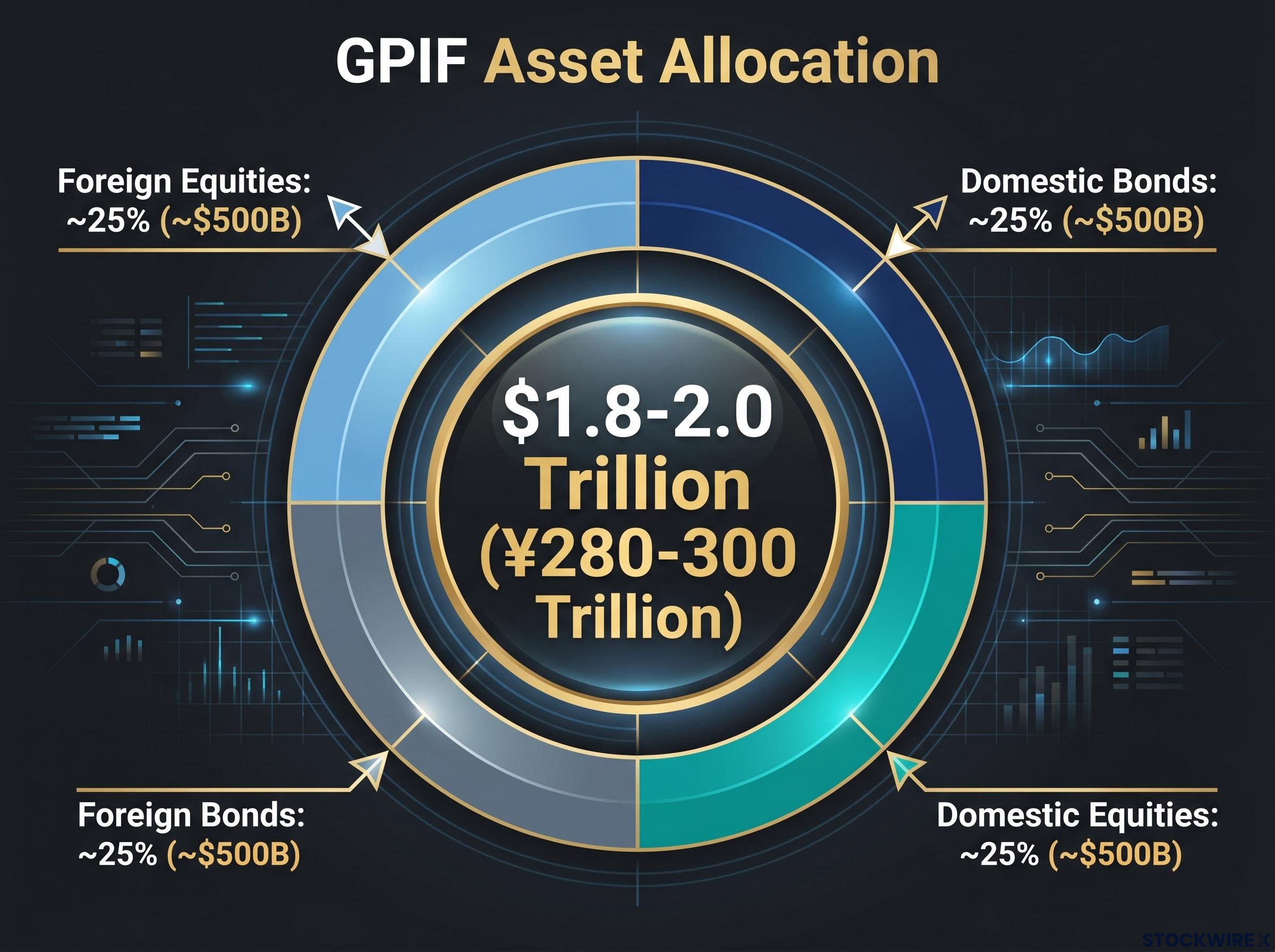

GPIF is not one of the largest pension funds in the world. It is the largest, with assets close to ¥280-300 trillion (approximately $1.8-2.0 trillion depending on the exchange rate). Its portfolio decisions carry systemic weight across both domestic and global markets.

The fund’s structure is straightforward: four asset buckets, each holding roughly 25% of total assets.

GPIF’s latest portfolio results for fiscal 2025 confirm the fund’s four-bucket structure, with each asset class holding approximately 25% of total assets and the overall portfolio sitting close to ¥290 trillion, the baseline from which any policy-driven reweighting would be measured.

| Asset Class | Current Weight | Approximate Value |

|---|---|---|

| Domestic Bonds | ~25% | ~$500B |

| Domestic Equities | ~25% | ~$500B |

| Foreign Bonds | ~25% | ~$500B |

| Foreign Equities | ~25% | ~$500B |

That produces a roughly 50/50 domestic-to-foreign split. The policy portfolio, the formal document that sets these target weights, is approved by the Ministry of Health, Labour and Welfare and revised infrequently. Changes are incremental rather than tactical.

That governance structure is the point. Any approved shift will not be reversed next quarter, which is precisely why even a 5-10 percentage-point reweighting carries multi-year market relevance.

A GPIF-led shift from overseas to domestic assets transmits through three channels, and they connect as a single repatriation story.

| Channel | Mechanism | Directional Impact |

|---|---|---|

| FX / Yen | Selling foreign assets requires buying yen | Yen appreciation pressure |

| Domestic Bonds / JGBs | Increased institutional demand for JGBs | Higher bond prices, lower yields |

| Domestic Equities | Large rules-based buyer enters concentrated market | Supportive for Nikkei 225 and TOPIX |

The FX channel is the most direct. When GPIF sells foreign securities and converts the proceeds into yen, it generates persistent demand for the currency. The yen’s structural weakness over recent years has been driven largely by interest rate differentials and yen-funded carry trades. A sustained repatriation flow can offset those carry-trade outflows over time, and it showed up in the same session as the announcement because currency markets price expectations fastest.

BOJ rate normalisation has progressively eroded the interest rate differential that made yen-funded carry trades structurally attractive, with the overnight call rate reaching 1.0% in June 2026 and a structured JGB tapering schedule running through March 2027 signalling that the tightening cycle is not yet complete.

A 5-10 percentage-point shift from foreign to domestic assets would imply tens of billions to low hundreds of billions of dollars in FX flows over a multi-year horizon.

The bond channel is less straightforward. GPIF’s domestic bond allocation declined significantly in the 2010s and 2020s as the fund diversified internationally, and its own recent results show domestic bonds have been a drag in a higher-rate environment. That makes a simple bond-heavy tilt less likely. Any reallocation may favour domestic equities and alternative assets instead.

The equities channel is where the directional support is clearest. GPIF entering as a large incremental buyer is supportive for the Nikkei 225 and TOPIX, though crowding risk exists in policy-favoured sectors if multiple institutions chase the same names.

What Japan’s domestic markets gain, the rest of the world loses at the margin. The mirror image of a domestic tilt has three spillover channels:

Treasury yield implications of reduced Japanese demand extend beyond bond pricing: with the 10-year yield at 4.66-4.67% and functioning as a direct pressure point on mortgage rates, corporate borrowing costs, and federal debt servicing simultaneously, even a gradual reduction in Japan’s price-insensitive long-term buying removes a structural stabiliser from the market.

If you hold global bond or equity index exposure, the Japan repatriation story is not just a yen-watcher’s concern. It is a marginal-demand story with real yield and pricing consequences for assets you may already own.

Two sections of directional analysis deserve a counterweight. Three structural constraints define the timeline of any reallocation:

The constraints do not invalidate the thesis. They define its timeline. A reader positioning around this story needs to think in years, not quarters.

Everything the reader has absorbed converts into four concrete forward-looking signals:

The Honebuto document on 21 July is the first hard test. Eleven days from today, the language around pension capital will confirm or qualify what the market priced in this morning.

The 10 July announcement is a credible policy catalyst backed by an immediate and coherent market reaction across three asset classes. Formal confirmation via the Honebuto framework and an eventual GPIF policy portfolio revision will determine how large and durable the reallocation actually is.

This is a multi-year structural story, not a one-session trade. The constraints on GPIF’s speed are as important to understand as the directional thesis itself.

For readers wanting to place Japan’s repatriation within the broader global reserve shift, our deep-dive into central bank reserve diversification examines the OMFIF survey finding that net dollar-reduction intent now outnumbers net dollar-increase intent for the first time on record, with central bank gold accumulation running at approximately 1,000 tonnes per year.

What the reader does with this information depends on existing exposure to yen-denominated assets, Japanese equities, or global bond markets. The next eleven days before the Honebuto release are a reasonable window to assess that exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding policy changes and market impacts are speculative and subject to change based on government decisions and market developments.

The Government Pension Investment Fund (GPIF) is the world's largest pension fund, with assets close to $2 trillion split roughly 50/50 between domestic and foreign holdings. Its allocation decisions carry systemic weight because even a modest reweighting moves prices in yen, Japanese government bonds, U.S. Treasuries, and global equities.

When GPIF sells foreign securities and converts the proceeds into yen, it generates persistent upward pressure on the currency. A 5-10 percentage-point shift from foreign to domestic assets would imply tens of billions to low hundreds of billions of dollars in FX flows over a multi-year horizon, reinforcing yen appreciation beyond what interest rate differentials alone would explain.

The Honebuto framework is Japan's government Basic Policy document, anticipated for release on 21 July 2026, which is expected to address how the country will direct capital toward AI, semiconductors, and the energy sector. The specific language around pension capital allocation will confirm whether the Finance Minister's 10 July announcement represents a formal policy commitment or early positioning.

The clearest confirmations are a formal revision to GPIF's policy portfolio target weights, quarterly GPIF disclosures showing the domestic share rising from roughly 50% toward 55-60%, sustained yen strength beyond what rate differentials explain, and quarterly data showing declining Japanese holdings of U.S. Treasuries.

Japan is historically one of the largest single foreign holders of U.S. government bonds, and a strategic reduction in that position removes a price-insensitive, long-term buyer from the market. Even a gradual pullback adds modest upward pressure to Treasury yields, compounding existing pressure from the 10-year yield already sitting at 4.66-4.67%.