BofA Double-Upgrades Intel to Buy With a $135 Street-High Target

1 hr ago

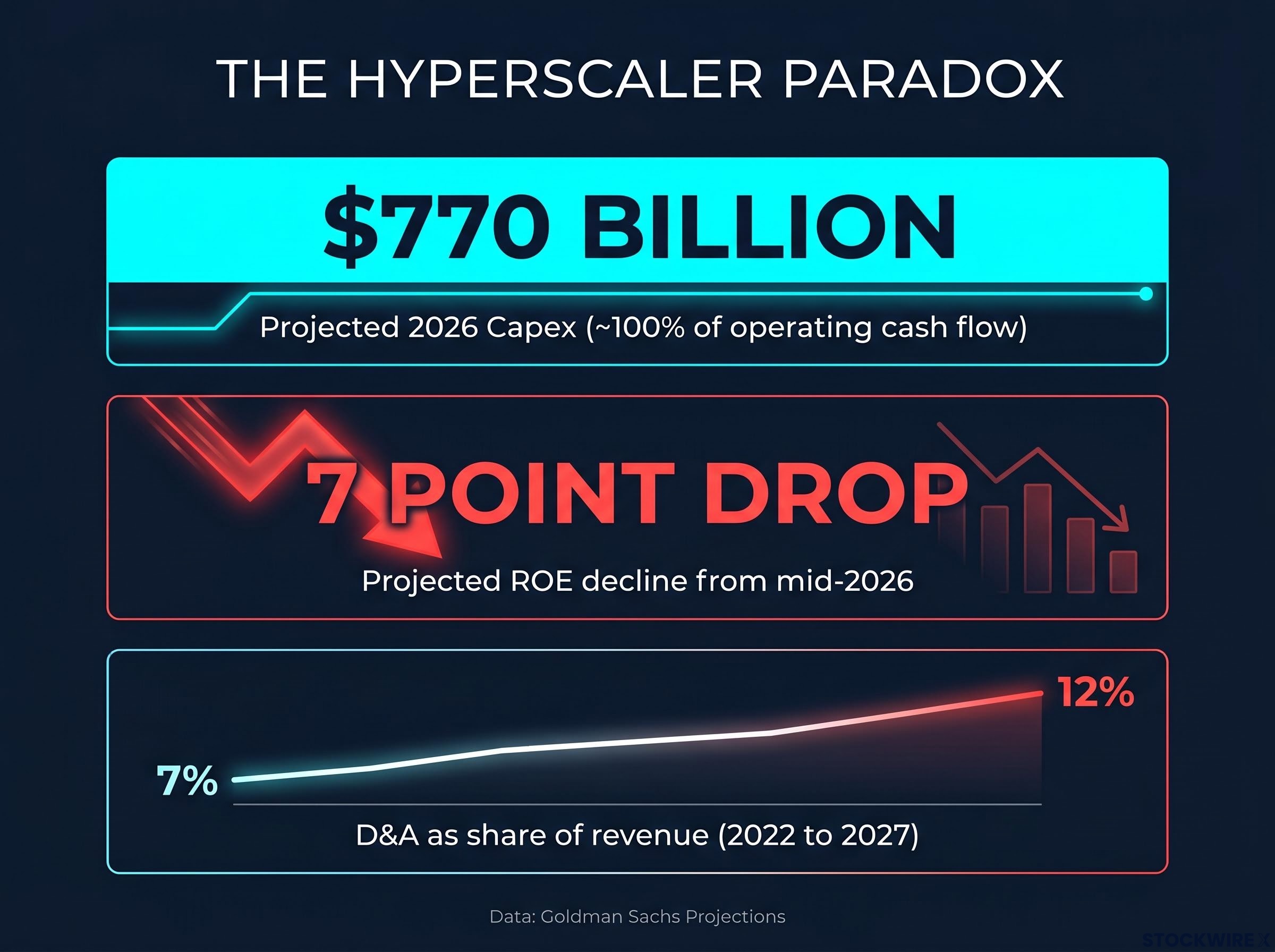

Goldman Sachs projects that major hyperscalers will collectively spend approximately $770 billion on capital expenditures in 2026, a figure roughly equivalent to 100% of their operating cash flow. That number sounds like dominance. Goldman Sachs reads it as a warning sign.

The AI infrastructure buildout is generating a striking paradox: the companies writing the largest cheques are facing meaningful near-term profitability compression, while a different set of companies, the chipmakers and equipment suppliers behind the scenes, are accumulating pricing power and margin advantage. Understanding where within the AI value chain profitability is actually concentrating is one of the defining investment questions of 2026.

What follows unpacks Goldman Sachs’ framing of AI semiconductor stocks as primary beneficiaries of the capex supercycle, distinguishes the semiconductor investment thesis from the hyperscaler story, and provides a structured framework for evaluating which parts of the chip layer carry the clearest advantage.

The same spending creating compression for the buyers is generating structural advantage for the sellers. Goldman Sachs characterises semiconductor companies as among the primary beneficiaries of the AI capital spending cycle, citing strong pricing power and above-average margins within this environment.

The mechanism is straightforward. Demand for AI-critical chips, particularly GPUs, high-bandwidth memory, and specialised accelerators, significantly outstrips near-term supply. That imbalance confers unusual pricing power on suppliers. Hyperscalers cannot slow their buildout without ceding competitive position, which means semiconductor vendors are selling into compelled demand rather than discretionary budgets.

The current AI investment cycle has already surpassed every prior technology spending peak in US history, with IT hardware and software reaching a record 4.9% of GDP in Q1 2026, eclipsing both the dot-com era high of approximately 4.2% and the cloud buildout peak of approximately 3.8%.

Portfolio manager Joseph Shaposhnik argues that “the suppliers of the picks and shovels are likely to continue to do very, very well,” characterising semiconductor suppliers as a lower-risk, more durable way to benefit from AI growth than hyperscalers or software names directly exposed to disruption.

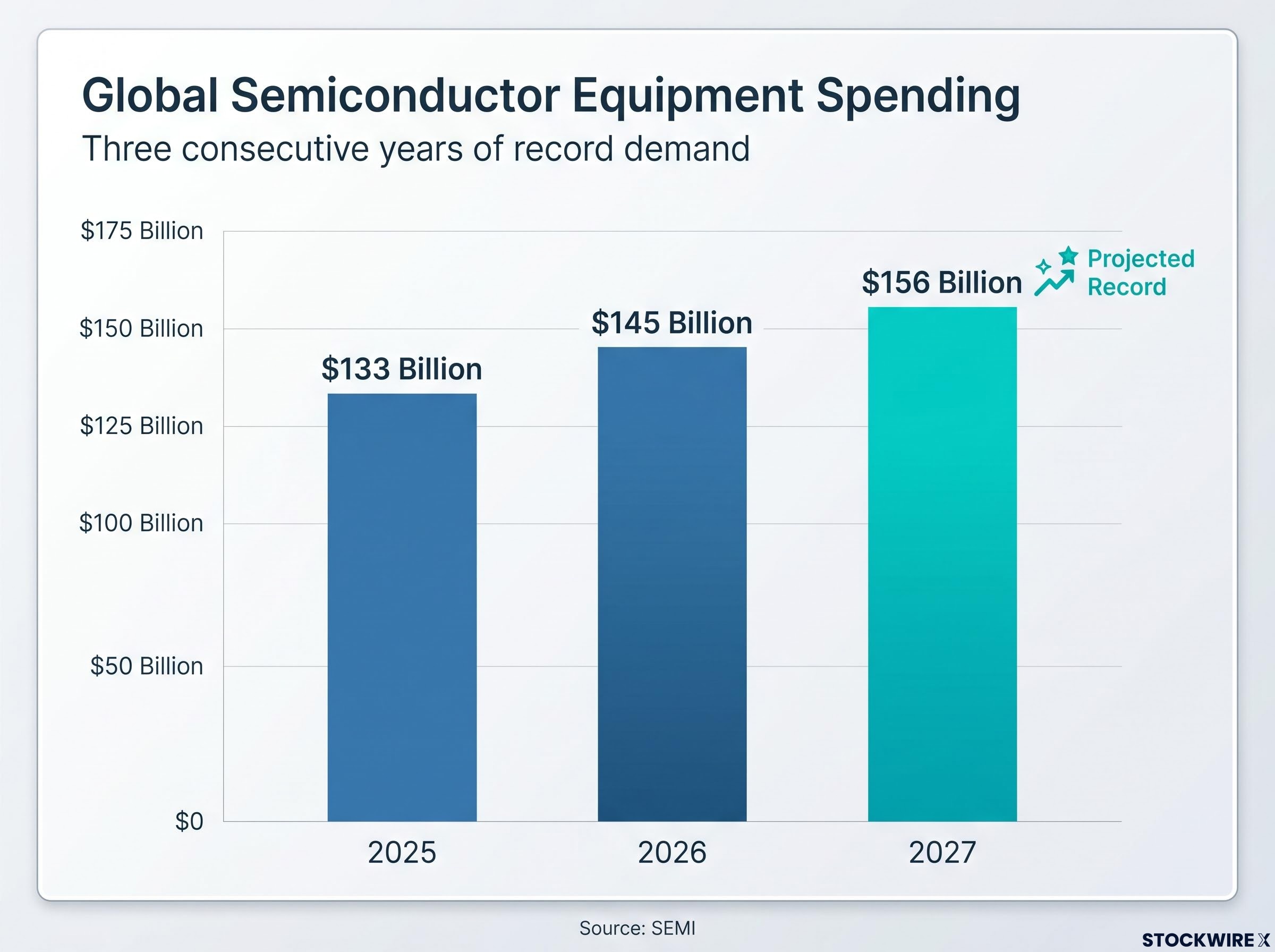

SEMI, the global semiconductor industry association, forecasts three consecutive years of record equipment spending that quantify the demand trajectory:

The asymmetry at the centre of this thesis is worth stating plainly: suppliers of enabling technology accumulate pricing power precisely because the buyers are compelled to keep spending. That dynamic is structurally different from the hyperscaler position, and it is where Goldman Sachs sees the clearest long-term AI tailwind.

The numbers arrive first, and they do not reconcile easily.

Goldman Sachs projects that return on equity among the largest technology companies will fall by an average of seven percentage points in the year ahead, measured from mid-2026. These are companies spending at record levels, and their profitability is moving in the opposite direction.

Q1 2026 earnings evidence illustrates the paradox in real time: Meta fell approximately 10% after reporting while Alphabet surged, with Goldman Sachs separately flagging that a significant share of Big Tech’s reported profit growth was driven by mark-to-market gains on private equity stakes rather than core cloud or advertising operations.

Goldman Sachs projects ROE among the largest technology companies will fall by an average of seven percentage points in the year ahead, a compression driven directly by the scale of AI infrastructure investment.

Three financial indicators frame the pressure:

What these figures describe is not a temporary investment trough. Hyperscalers are structurally shifting from asset-light software franchises to capital-heavy infrastructure businesses, and investors still pricing them as the former may be underestimating how profoundly that transition reshapes their return profiles.

“Buy semiconductors” is not a single trade. Three distinct sub-segments within the chip layer carry differentiated return logic, and understanding where each sits in the value chain determines both margin structure and capital requirements before any company-specific analysis begins.

| Sub-Segment | Representative Players | Margin Structure | Primary AI Demand Driver |

|---|---|---|---|

| Fabless AI chip designers | GPU and accelerator designers | High margins; no fabrication capex burden | Direct AI training and inference workloads |

| Memory and advanced packaging | HBM and packaging specialists | Cyclical but currently elevated by supply constraints | HBM demand for AI accelerators; advanced packaging for chiplet architectures |

| Semiconductor equipment suppliers | ASML, Applied Materials, Lam Research, KLA, Tokyo Electron | High utilisation-driven returns; capital-intensive but pricing power offsets | Every fab expansion in the supercycle |

Fabless designers capture particularly high margins because they hold pricing power on the design and intellectual property without bearing the full capital cost of fabrication. Independent semiconductor analysis projects the global market could reach $1.1-1.4 trillion by 2030 and approximately $1.5 trillion by 2033, implying roughly 11% annual growth from 2023 to 2033. Sustaining that market would require annual industry capex exceeding $460 billion by 2033, consistent with a long-run capital intensity of approximately 30-32%.

The equipment layer holds a distinct position in the value chain: long-cycle demand visibility and direct leverage to every fab expansion in the supercycle. ASML, Applied Materials, Lam Research, KLA, and Tokyo Electron are named by independent analysis as among the clearest beneficiaries.

SEMI explicitly attributes the 2027 spending record in part to back-end test and packaging investments driven by HBM demand. Despite being capital-intensive businesses themselves, these equipment suppliers benefit from very high utilisation and pricing power at this point in the cycle, supporting strong earnings power across the group.

The AI capex supercycle raises the long-run trend line for semiconductor demand. It does not eliminate the industry’s inherent cyclicality. This distinction separates a durable investment position from a momentum trade, and misunderstanding it is where most retail investors make errors in the space.

The framework has two layers:

Goldman Sachs expects AI adoption to eventually drive productivity improvements that could lift revenues, per-employee earnings, and profit margins across a broad range of industries, providing the structural underpinning for a multi-year semiconductor investment horizon.

Investors who internalise this cycle-within-a-trend framework can hold through corrections that would otherwise look alarming. Those who mistake the structural thesis for a promise of uninterrupted quarterly growth will sell at exactly the wrong moments.

The semiconductor thesis is not without vulnerabilities, and the quality of an investor’s position depends on knowing exactly which conditions would weaken it. Four risk categories function as selectivity arguments within the opportunity rather than reasons to abandon the structural case.

Custom AI chip economics are driven by lower per-inference costs, improved energy efficiency, and reduced dependence on a single external supplier, with Broadcom’s $4.1 billion AI semiconductor revenue in Q1 2025 providing concrete evidence that this market is already operating at scale rather than remaining a theoretical threat.

The CHIPS and Science Act investment framework allocates approximately $50 billion to strengthen domestic semiconductor manufacturing and supply chain resilience, split between an $11 billion research and development office and a $39 billion program office providing direct incentives for U.S. fab expansion, giving companies aligned with reshoring programmes a subsidised capex advantage that partially offsets the policy-driven execution complexity noted above.

The custom silicon threat warrants separate framing because it operates at the company level rather than the macro level. Hyperscalers developing bespoke accelerators aim to reduce reliance on third-party GPU vendors, which represents a medium-term competitive threat to incumbent chip designers.

The risk argues for diversification within the chip layer, toward equipment, memory, and packaging, rather than concentrated GPU-designer exposure. Custom silicon development itself creates demand for semiconductor equipment and advanced packaging, partially recycling the competitive threat back into the broader chip ecosystem.

For investors wanting to stress-test the semiconductor thesis against its most material near-term risk, our full explainer on the capex-to-revenue lag in AI semiconductor stocks examines the 18-24 month gap identified by Morningstar analysts between hyperscaler hardware deployment and the AI revenue generation that would justify current valuations, alongside geopolitical risk distribution across ASML, Nvidia, and AMD.

Translating the macro thesis into company-level research requires a structured evaluation framework. Four factors, ordered by priority, provide the criteria an investor would apply when assessing individual semiconductor names as capex supercycle beneficiaries.

| Evaluation Factor | What to Look For | Why It Matters in the Current Cycle |

|---|---|---|

| Position in the AI capex stack | Fabless vs. foundry vs. equipment vs. memory | Determines margin ceiling and capex floor before company-specific analysis |

| Directness of AI demand tie | Products critical to AI training/inference vs. legacy components | Direct linkage to compelled hyperscaler spending provides demand durability |

| Margin structure and capital intensity | Gross margins, capex-to-revenue ratio, free cash flow conversion | The supercycle rewards capital-light models disproportionately |

| Policy and geopolitical exposure | CHIPS Act eligibility, reshoring alignment, export control sensitivity | Subsidised expansion creates visibility; regulatory dependency creates fragility |

Shaposhnik’s framing reinforces why position in the stack matters most: semiconductor suppliers and some infrastructure vendors are “lower-fragility” beneficiaries compared to software companies facing AI commoditisation risk. The evaluation framework makes that distinction operational.

A single principle has operated throughout this analysis: in large-scale technology infrastructure cycles, profitability tends to migrate toward suppliers of enabling technology rather than accumulating at the platform owners who are compelled to keep investing. The hyperscaler squeeze and the semiconductor advantage are not competing views. They are two sides of the same capex cycle.

The near-term indicators confirm where the cycle currently sits. SEMI projects equipment spending peaking at $156 billion in 2027. The global semiconductor market is projected to grow toward $1.1-1.4 trillion by 2030 and potentially $1.5 trillion by 2033. That trajectory represents the structural runway, but investors with shorter time horizons need to account for cyclical interruptions along that path.

Goldman Sachs characterises semiconductor companies as among the primary long-term beneficiaries of the AI capital spending cycle, a position supported by strong pricing power, above-average margins, and direct leverage to compelled hyperscaler investment.

Investors who understand that profitability migrates within technology cycles, not just toward the most visible names, are better positioned to identify durable long-term holdings before consensus fully prices the thesis. The question is not whether AI spending continues. The question is which balance sheets absorb the cost and which income statements capture the margin.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI semiconductor stocks are shares in companies that design, manufacture, or supply equipment for chips used in artificial intelligence workloads, including GPUs, high-bandwidth memory, and wafer fab equipment. Investors follow them because demand for AI-critical chips significantly outstrips near-term supply, conferring unusual pricing power on suppliers selling into compelled hyperscaler spending.

Goldman Sachs argues that the companies writing the largest infrastructure cheques face meaningful profitability compression, with ROE projected to fall seven percentage points from mid-2026, while semiconductor suppliers accumulate pricing power and above-average margins because hyperscalers cannot slow their buildout without ceding competitive position.

Fabless designers capture high margins by holding pricing power on intellectual property without bearing fabrication capex, while equipment suppliers like ASML, Applied Materials, and Lam Research benefit from long-cycle demand visibility and high utilisation rates tied to every fab expansion in the AI capex supercycle.

The AI capex supercycle raises the long-run demand trend line for semiconductors but does not eliminate the industry's inherent cycles of over-build and inventory digestion; the projected 11% annual growth rate from 2023-2033 represents a trend rate, not a guaranteed annual outcome, meaning corrections can occur within an otherwise durable upward trajectory.

The four primary risk categories are valuation risk from high starting multiples, potential hyperscaler capex normalisation if ROE discipline or macro deterioration causes a pullback, custom silicon programmes where hyperscalers develop proprietary accelerators to reduce reliance on third-party GPU vendors, and geopolitical supply chain fragmentation driven by export controls and reshoring policy.