Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

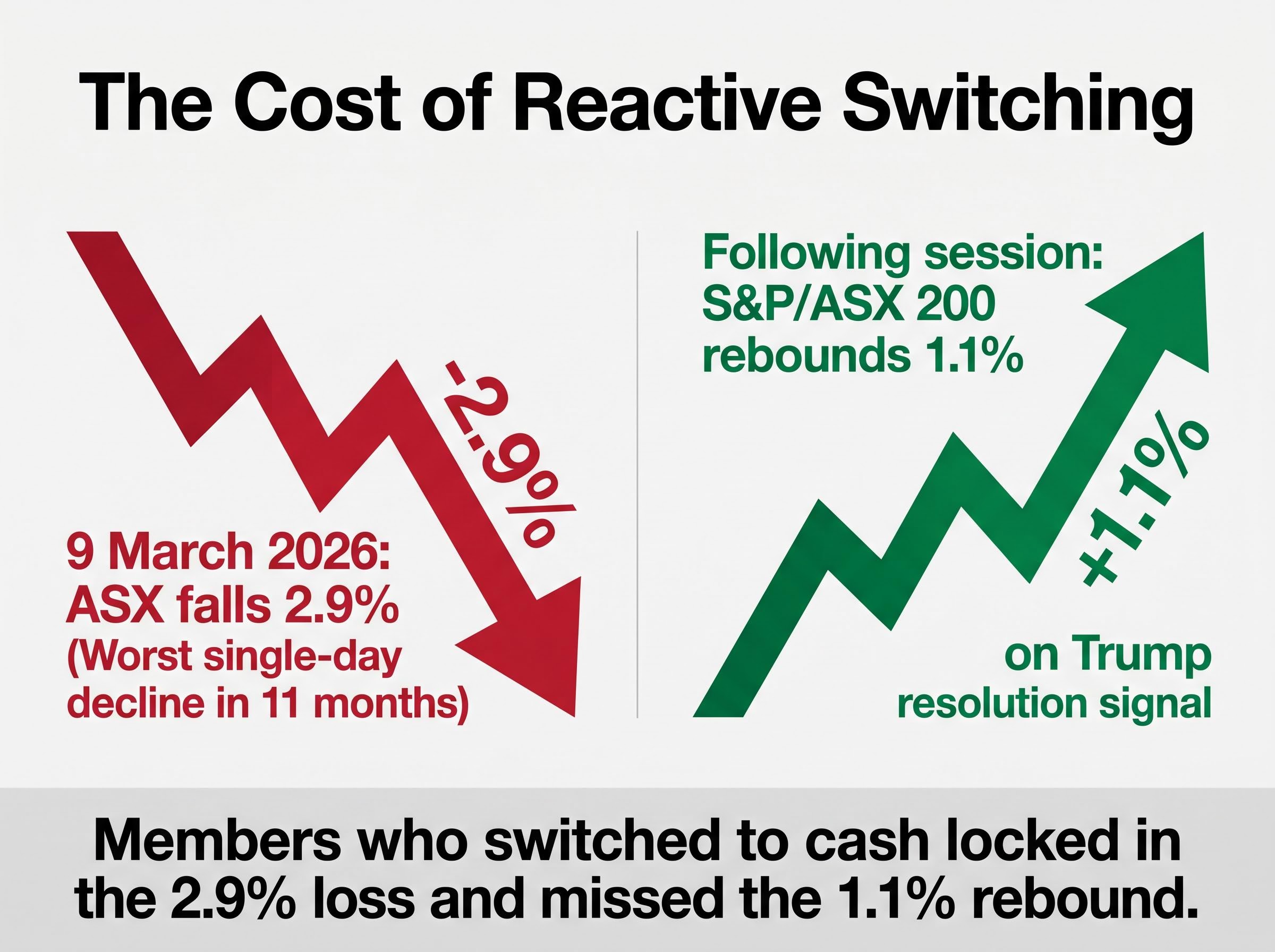

During the peak of the Iran conflict in March 2026, thousands of Australian superannuation members did exactly what their funds advised them not to do. They switched to cash, locking in losses from a 2.9% ASX single-day drop, and then watched the market recover 1.1% in a single session after diplomatic signals emerged. Oil prices swinging from $82 to nearly $120 per barrel, equity markets down roughly 10%, and a flood of alarming headlines created the conditions where doing something felt more responsible than doing nothing. That instinct, however well-intentioned, is precisely the mechanism through which most long-term investment value is destroyed.

This guide explains why reactive behaviour during market volatility costs investors more than the volatility itself, what the evidence from Australia’s biggest super funds reveals about even expert market timing, and what a genuinely durable approach to volatile markets looks like for Australian investors in 2026.

On 9 March 2026, the ASX recorded its worst single-day decline in 11 months, falling 2.9% as the Strait of Hormuz closure sent oil prices surging and headlines into overdrive. Superannuation members responded predictably. Switching requests to cash options surged, as thousands of Australians locked in their losses at the worst possible moment.

Then the reversal came. After US President Trump signalled conflict-resolution intent, the S&P/ASX 200 rebounded 1.1% in a single session. Members who had switched to cash missed it.

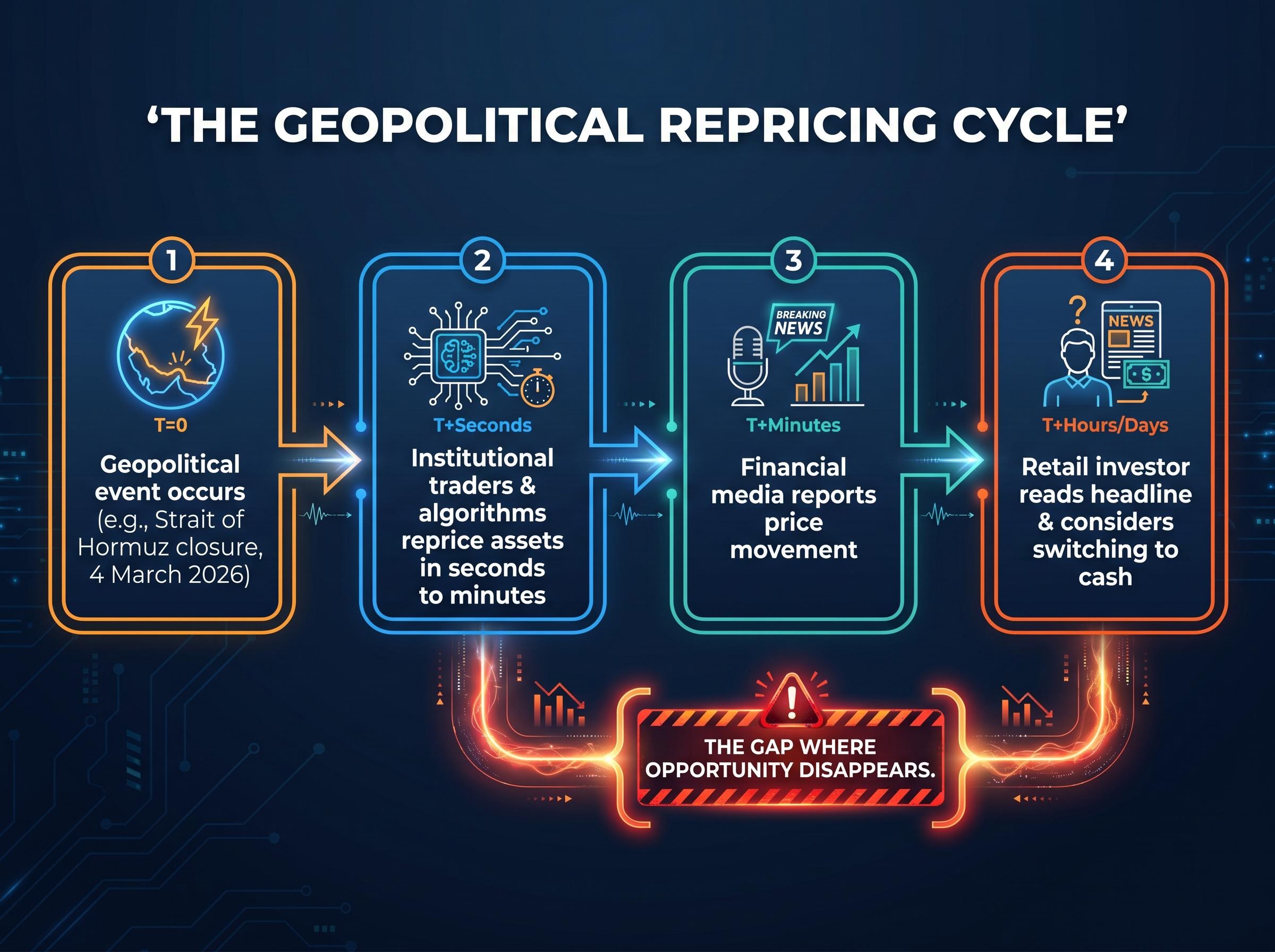

The sequence is not new. It followed the same three-stage cycle that played out during COVID-19 in 2020, and during the Global Financial Crisis before that:

Balanced superannuation options fell approximately 3.2% for March 2026, their worst monthly result since 2022. Yet the monthly figure told only part of the story.

APRA’s quarterly superannuation industry data, published as of December 2025, provides the official baseline for tracking member switching activity and fund-level asset movements across Australia’s superannuation system, the same dataset that contextualises the scale of cash-switching behaviour observed during the March 2026 volatility episode.

AustralianSuper reported positive year-to-date returns despite the March drawdown, reinforcing that short-term volatility had not erased the broader gains accumulated earlier in the year.

The pattern is structural, not situational. Recognising it as a recurring human tendency, rather than a rational response to unique circumstances, is the first step toward resisting it. The instinct to act during a sharp decline is better understood as a signal to pause.

The instinct to protect savings by moving to cash carries its own hidden cost: with Australia’s headline CPI reaching 4.6% for the 12 months to March 2026, real returns on cash holdings are negative after inflation, meaning the perception of safety comes with a documented and measurable purchasing power penalty.

If anyone should be able to time markets successfully, it is the investment teams at Australia’s largest superannuation funds. They employ hundreds of analysts, have access to institutional-grade data, and manage portfolios worth hundreds of billions of dollars. The evidence from 2026, however, suggests even they struggle.

In remarks reported by Investment Magazine in March 2026, AustralianSuper’s departing Chief Investment Officer publicly acknowledged regret over underweighting artificial intelligence and digital sector stocks from around 2022. The decision was itself a timing call, a bet that those sectors were overvalued or that capital would be better deployed elsewhere. Simply holding benchmark-level exposure would have captured the majority of the gains the fund missed.

The structural irony is significant. The same institution advising members not to make reactive decisions had itself made a directional allocation choice that underperformed a passive benchmark. Australian super funds collectively allocated an estimated $143 billion toward AI-related investments by late 2025, according to the Australian Financial Review, suggesting the sector’s underweighting was eventually reversed, but only after the opportunity cost had compounded.

During the Iran conflict, fund communications to members employed language that sounded strategic but offered no testable prediction:

According to the Australian Financial Review in April 2026, some funds raised equity allocations during the conflict while others built cash reserves. Both approaches were described publicly as strategic. Neither was presented with a falsifiable framework that members could later use to evaluate whether the call was correct.

ASIC’s review of super trustee communications, published in October 2025, identified glaring gaps in how funds explain investment decisions to members, including a tendency toward one-size-fits-all messaging that lacks the specificity members would need to evaluate whether a stated strategy was actually executed.

If institutions with these resources cannot consistently time markets, the case for retail investors attempting the same, with less information, higher transaction costs, and more emotional proximity to their savings, is considerably weaker.

The cost of reactive trading during volatile periods is rarely visible on a single statement. It accumulates through three distinct channels, each of which peaks precisely when the temptation to trade is strongest.

| Cost Type | What It Is | When It Peaks | Who Bears It |

|---|---|---|---|

| Transaction costs | Fees charged on each buy or sell, including brokerage and fund switching fees | During elevated trading volumes in volatile markets | The individual investor or fund member |

| Price impact | The cost of buying or selling into a moving market, where the price shifts between decision and execution | During periods of wide bid-ask spreads and rapid price movement | The individual investor, often invisibly within pooled fund structures |

| Timing risk | The gap between selling (often near the bottom) and re-entering (often after recovery has begun) | During sharp declines followed by rapid, partial recoveries | The individual investor directly |

These costs compound silently over time. Inside pooled superannuation structures, individual transaction activity is not itemised for members, which means the cumulative drag from switching behaviour during volatile periods remains largely invisible. No publicly available APRA-level data currently breaks down these costs in a way that allows members to assess the total impact of their switching decisions.

The scale of emotional investing costs becomes concrete in platform-level data: trading volumes on Selfwealth by Syfe doubled during the April 2025 US tariff announcement, and in FY 2024 Australian retail CFD investors collectively lost more than $458 million, with 68% of participants recording losses according to ASIC REP 828.

Some of the largest funds have themselves acknowledged, in their own communications during the March 2026 period, that refraining from action is frequently the optimal response during elevated turbulence. That concession is significant. When the institutions managing the money say that doing nothing is often the best strategy, the evidence against reactive trading becomes difficult to dismiss.

The Strait of Hormuz closure on 4 March 2026 offers a precise illustration of how quickly geopolitical information moves into asset prices. Oil was trading at $80-$82 per barrel on 2 March. Within days of the closure, prices had escalated to nearly $120 per barrel at peak. Intraday swings of 5-10% occurred on specific trading days during the conflict period. Gold traded in a range of approximately $5,001-$5,417 per ounce during March, reflecting the breadth of volatility across asset classes.

The speed of that repricing is the structural problem for any investor attempting to react. In markets with millions of participants processing identical information simultaneously, the price already reflects the consensus view by the time a retail investor reads the headline and considers acting.

The sequence makes this concrete:

The gap between step two and step four is where the opportunity disappears. By the time the decision to act feels urgent, the market has already moved.

CommBank economists Belinda Allen, Dhar, and Cartwright emphasised that the economic impact of the conflict would be duration-dependent: disruptions lasting weeks would carry manageable consequences, while disruptions lasting months would create sustained inflation and growth headwinds for Australia.

Even professional forecasters, with direct access to macroeconomic modelling, resisted making directional calls on the conflict’s resolution timeline. If they could not predict whether the disruption would last weeks or months, the basis for a retail investor to make a portfolio decision in real time is thinner still. Waiting for clarity before acting is not a cautious approach; the clarity, when it arrives, is already priced in.

Systematic investing strategies that automate allocation decisions remove the most dangerous link in the chain: the moment where a volatile headline and an anxious investor intersect, with $6.9 billion flowing into global equity ETFs from Australian investors in Q1 2026 despite simultaneous RBA rate hikes and commodity shocks, the structural shift toward rules-based approaches is increasingly visible in flow data.

The alternative to reactive trading is not passive resignation. It is a deliberate framework built to capture long-term market returns while removing the decision points where behavioural errors are most likely.

That framework has four components, each of which can be applied by Australian investors through superannuation fund selection or ASX-listed exchange-traded funds (ETFs):

Bell Financial Group’s CIO Will Riggall, in a market wrap on 13 March 2026 covering Iran conflict impacts, implicitly favoured diversification over attempts to time the market, a position consistent with the structural evidence.

The data suggests Australian investors are increasingly voting for this approach with real money. The Australian ETF market recorded a record $48.3 billion in inflows during 2025, with passive strategies clearly dominant. Passive ETFs attracted approximately $7.7 billion quarterly compared with approximately $2.5 billion quarterly for active ETFs.

That growth trajectory continued into 2026 despite the Iran conflict volatility. Passive strategies maintained leadership in net inflows, consistent with a longer-term structural shift in Australian retail investor behaviour toward lower-cost, index-based approaches. This is not trend-following. It is a rational structural response to the accumulated evidence on active management costs and outcomes.

Investors ready to move from principle to structure will find our full explainer on ASX portfolio construction for volatile markets covers the three-layer framework in detail: a cash buffer for near-term protection, income-generating bonds for yield, and diversified equities for long-term growth, with worked examples drawn from the March 2026 period when Australian ETF investors committed $5.6 billion to the market even as the ASX fell 7.8%.

The greatest threat to long-term investment returns during volatile periods is not the market decline itself. It is the behavioural response to it. The March 2026 episode demonstrated this with uncomfortable clarity: members who switched to cash during the 2.9% ASX drop on 9 March locked in losses and faced the risk of missing the 1.1% rebound that followed days later.

Staying invested when headlines are alarming is genuinely difficult. The anxiety is real, and the impulse to protect savings is understandable. The evidence, however, consistently points in one direction. Inaction, within a well-structured portfolio, is the strategy that preserves the most value over time.

A practical step for Australian investors: check whether superannuation savings are in a low-cost, diversified balanced or index option, and whether holdings outside super reflect the same principles. If they do, the framework is already in place.

The investors who fared best during March 2026 were, by most accounts, those who did not check their balances daily and did not act. That is not complacency. It is discipline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A market volatility strategy is a structured approach to investing that maintains broad diversification, minimises costs, and removes emotionally driven trading decisions during periods of sharp market movement, preserving long-term returns rather than reacting to short-term headlines.

Switching to cash during a downturn locks in losses at the worst possible moment and risks missing rapid recoveries, as seen in March 2026 when members who exited after a 2.9% ASX drop missed a 1.1% single-session rebound days later.

Geopolitical shocks reprice assets within seconds as institutional traders and algorithms respond, meaning by the time a retail investor reads a headline and considers acting, the market has already adjusted and the opportunity to react profitably has passed.

Australia's largest super funds issued communications using language such as harvesting volatility and raising liquidity, but ASIC reviews have found these messages often lack the specificity members need to evaluate whether a stated strategy was actually executed.

A durable strategy combines broad diversification across asset classes and geographies, low-cost index funds or ETFs, systematic calendar-based rebalancing, and the deliberate removal of decision points that expose investors to headline-driven behavioural errors.