On Friday, Goldman Sachs told clients that the most crowded trade on Wall Street is leaving money on the table, and it named three specific places to look instead.

The note, published 18 July 2026, arrives as AI-related equities have driven outsized volatility across U.S. markets. Individual stock correlations have retreated to levels not seen in generations, the equal-weighted S&P 500 has pushed into record territory, and earnings leadership remains heavily concentrated in a narrow band of AI and energy names. Goldman is not calling time on the AI trade. It is arguing that a lopsided portfolio creates a structural blind spot, and that three distinct themes outside the AI cluster currently offer underpriced upside.

Here is what the data says on each of Goldman’s three investment themes, the underlying logic that makes them attractive right now, and what you would need to believe for each one to pay off.

Why Goldman is looking beyond the AI trade right now

Goldman’s 18 July 2026 research note is not an AI bear case. It is a portfolio construction argument built on two specific market signals:

- The equal-weighted S&P 500 has posted fresh all-time highs, suggesting broad earnings strength beneath the headline index.

- Correlations between individual stocks have receded to their lowest point in several decades, meaning individual stocks are moving on their own fundamentals rather than in lockstep with the market.

Together, those signals tell you something specific. When correlations are this low, individual stock selection matters more than it has in years. A passive allocation to mega-cap momentum captures less of the market’s total opportunity set, and theme-based positioning outside the AI cluster becomes a genuine edge rather than a contrarian gesture.

The structural backdrop Goldman is responding to has been building for months: index concentration risk has reached levels that surpass historical peaks, with five mega-cap stocks controlling roughly 23% of the broad U.S. market index and driving the majority of both Q1 2026 losses and April’s recovery.

That is the structural backdrop Goldman is responding to. The three themes that follow are its answer.

When big ASX news breaks, our subscribers know first

Theme one: consumer experience stocks offer undervalued resilience

You cannot virtualise a live concert. You cannot automate a hotel stay. That inherent defensiveness against AI-driven displacement is the starting point for Goldman’s first theme: consumer experience companies spanning travel, leisure, hospitality, entertainment, and food service.

The category includes:

- Travel and leisure operators

- Hospitality chains

- Entertainment and live-event businesses

- Quick-service restaurants and coffee chains

As of July 2026, this group of businesses has already delivered stronger returns than the broader equal-weighted consumer discretionary sector on a year-to-date basis. Yet the valuation picture tells a more interesting story.

Despite that outperformance, the prices investors are currently paying for consumer experience stocks sit beneath their own long-run historical norms, suggesting the market has acknowledged the quality without yet fully pricing it in.

That gap is the specific opportunity Goldman is highlighting. The market has rewarded these names relative to their sector peers but has not yet closed the distance to their own historical valuation range. For an investor, that means the recognition has started without the full repricing, which is precisely the window where adding exposure carries a favourable risk-reward profile.

Goldman’s consumer experience theme does not stand alone: a consumer sector recovery thesis has been building across major bank research desks, with JPMorgan’s equity strategy team separately identifying H2 2026 as a re-rating window for consumer cyclicals after years of underperformance relative to every other cyclical group.

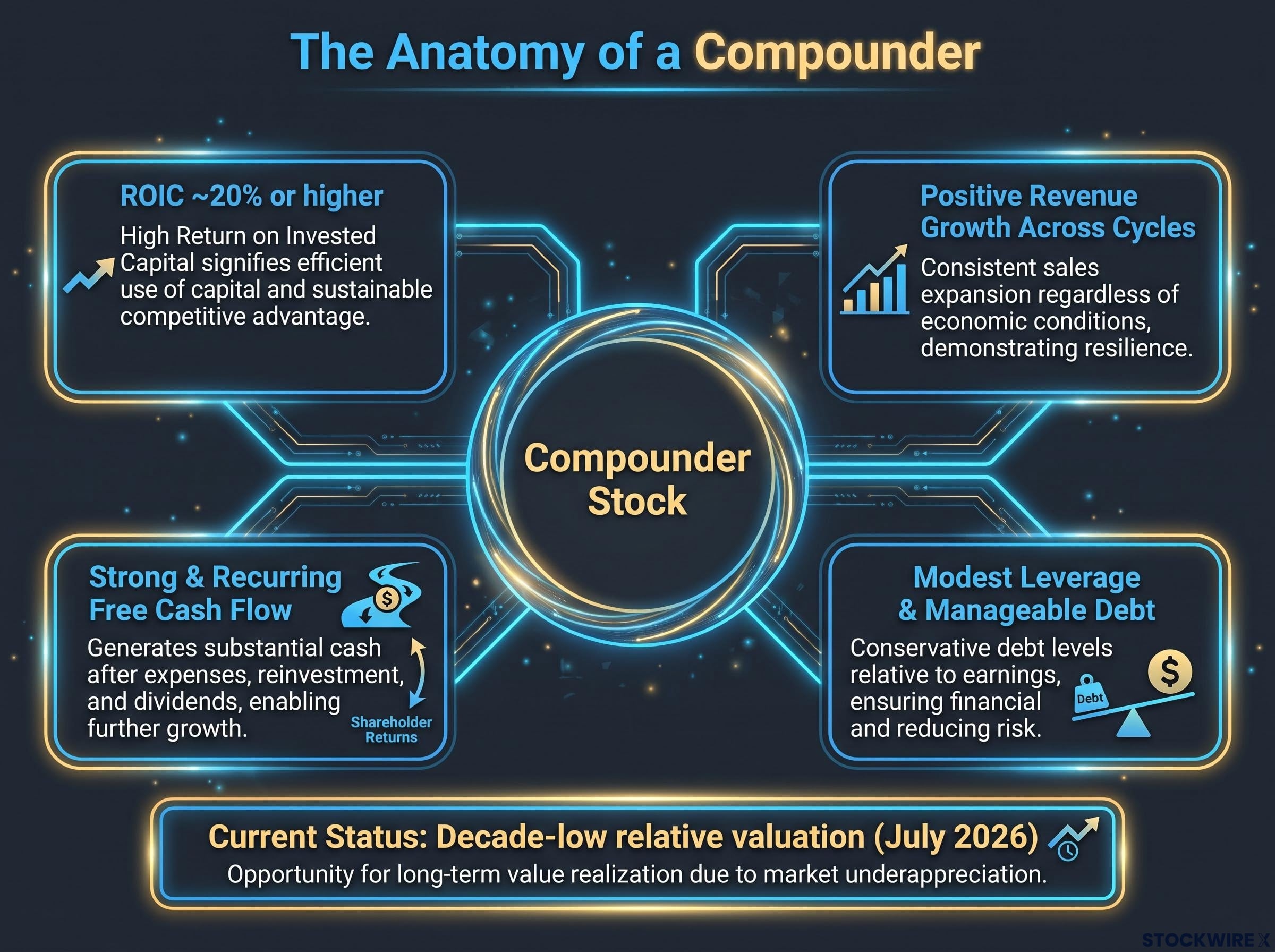

What makes a compounder, and why this category is at a decade-low relative valuation

A compounder is a company that steadily grows its intrinsic value by earning high returns on capital and reinvesting those cash flows year after year. The term gets used loosely, so here is what a professional screen actually requires.

| Characteristic | Threshold | Why it matters | Risk if absent |

|---|---|---|---|

| Return on invested capital (ROIC) | Roughly 20% or higher, sustained | Proves the business earns well above its cost of capital | Capital destruction over time |

| Revenue growth consistency | Positive growth across multiple cycles | Signals durable demand, not cyclical luck | Earnings volatility undermines compounding |

| Leverage | Modest, with manageable debt levels | Protects compounding from interest-rate shocks | Balance sheet fragility in downturns |

| Free cash flow generation | Strong and recurring | Funds reinvestment without dilution or debt | Growth requires external capital, diluting returns |

ROIC, or return on invested capital, measures how much profit a company generates for every dollar of capital deployed in the business. A 20% threshold means the business is turning $1 of investment into $0.20 of annual profit, well above the cost of that capital.

Why compounders are cheap right now, not broken

As of July 2026, compounder valuations have slipped to relative levels close to their weakest point in roughly ten years, even as the underlying fundamentals remain strong. The reason is straightforward: capital has rotated toward a narrow cluster of AI momentum names, leaving quality businesses outside that cluster structurally underowned.

This is cheap-because-overlooked, not cheap-because-broken. The underlying earnings power, balance sheet health, and cash generation have not deteriorated. The market has simply directed its attention elsewhere.

The compounders thesis rests on the same structural mispricing logic that value investors have applied for decades: finding undervalued stocks in areas where professional attention is thin, then waiting for fundamentals to close the gap between price and intrinsic value.

A decade-low relative valuation in a category defined by superior fundamentals is historically the condition that precedes mean-reversion. That is the core bet Goldman is framing. It requires patience; compounders can stay undervalued for extended periods in a momentum-driven market, and this is a medium- to long-term thesis rather than a near-term trade.

M&A targets: capturing deal premiums before the market does

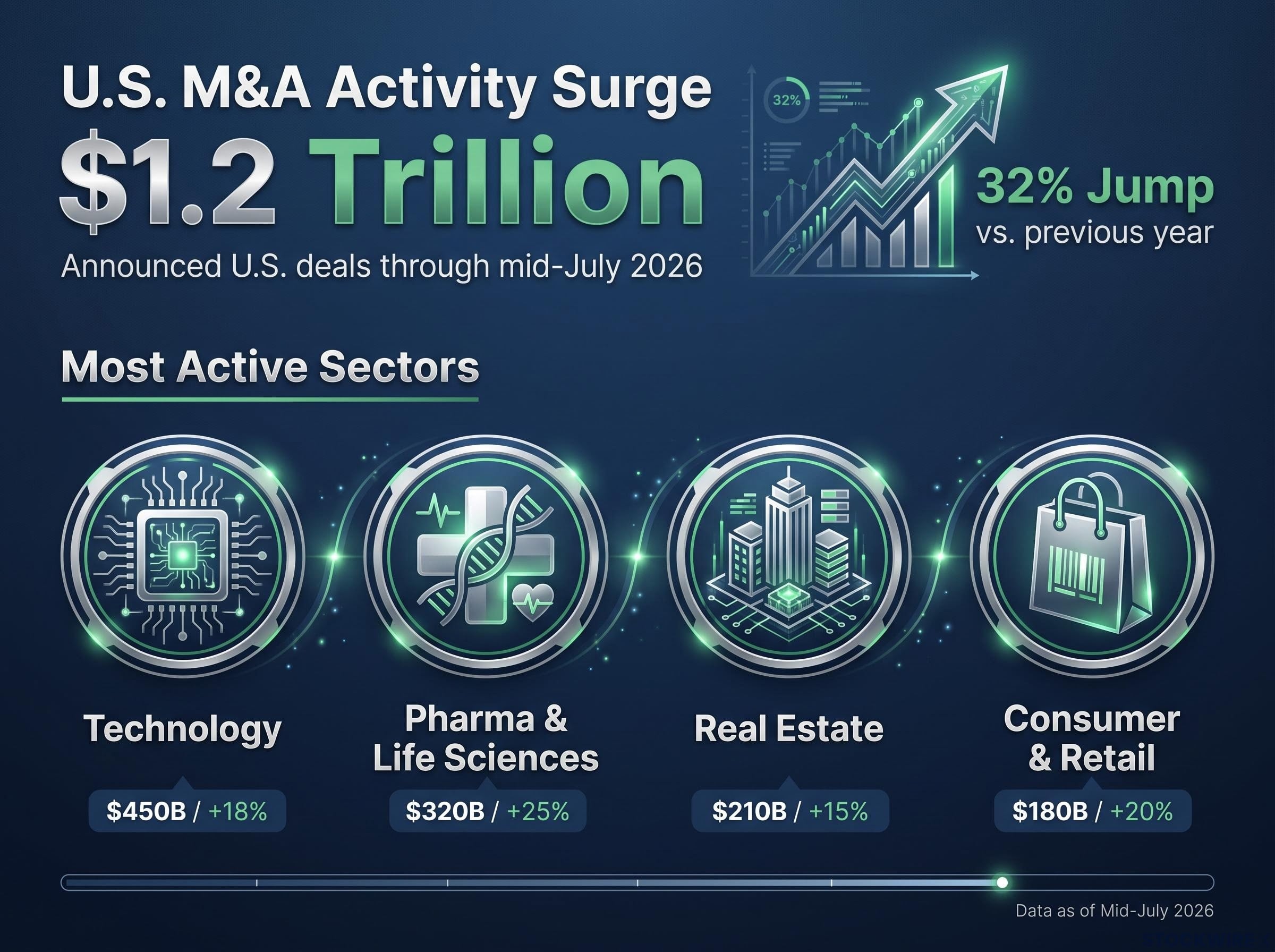

U.S. merger and acquisition activity has crossed approximately $1.2 trillion in announced deals through mid-July 2026, representing a 32% jump compared with the same period a year ago.

That acceleration tells you strategic buyers and private equity are deploying capital aggressively. The supporting conditions are all pointing the same direction: stabilising financing costs, more predictable regulation, and significant dry powder sitting at both corporate acquirers and PE funds.

Goldman points out that the share prices of probable acquisition targets have not yet moved to reflect the busier deal environment. The opportunity sits in the gap between where these companies trade today and the value implied by an active M&A cycle.

The characteristics Goldman associates with likely targets:

- Valuable assets or intellectual property

- Slower growth than peers but still profitable

- Sub-scale players in industries where larger rivals are consolidating

The sectors seeing the heaviest activity:

- Technology

- Pharma and life sciences

- Real estate

- Consumer and retail

This is the most event-driven of the three themes. If you identify a probable target before a deal is announced, you capture the takeover premium. If the deal never comes, you own a slower-growth business at a price that may not compensate for the wait. Position sizing across multiple candidates is not optional here; it is how you manage the binary nature of the risk.

The next major ASX story will hit our subscribers first

Risks every investor should weigh before acting on these themes

Each of these three themes carries a distinct set of conditions that would need to change for the thesis to underperform. Knowing what to monitor matters more than knowing the upside case.

| Theme | Key risk | What to monitor |

|---|---|---|

| Consumer experience | Cyclical exposure to consumer sentiment and discretionary spending | Consumer confidence data, employment trends, discretionary spending indicators |

| Compounders | Extended underperformance in momentum-driven markets | Market breadth, rotation signals, relative valuation trends over quarters |

| M&A targets | Deals delayed, blocked, or never materialised | Financing costs, regulatory signals, macro conditions, deal pipeline announcements |

Goldman frames all three themes as portfolio additions, not AI replacements. Durable demand does not mean recession-proof. Superior fundamentals do not guarantee near-term repricing. And deal probability is not deal certainty. Understanding what would break each thesis gives you a clearer view of position sizing and time horizon than simply knowing the upside case.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

What the Goldman note actually changes for your portfolio thinking

The three themes are distinct in their mechanics, but the underlying portfolio logic is the same: lower your exposure to the AI momentum cluster and add exposure to quality, value, or event-driven returns that the current market structure is underpricing.

Goldman’s portfolio construction argument maps directly onto a principle Ray Dalio formalised at Bridgewater: combining genuinely uncorrelated return streams reduces portfolio volatility without sacrificing expected returns, with research showing 15-20 independent streams can cut volatility by approximately 80%.

The single variable that matters most going forward is whether AI-related concentration in U.S. equities deepens or begins to broaden. If market leadership widens, all three themes benefit simultaneously. If concentration deepens further, patience becomes the price of diversification.

With the equal-weighted S&P 500 registering record highs alongside stock correlations at generational lows, the data already suggests the market is broadening beneath the surface. Goldman’s note is a signal about where the blind spots are right now.

The question worth asking: do those same blind spots exist in your own portfolio?