Brent crude jumped close to 10% on Monday, pushing prices into the low $80s per barrel, following President Trump‘s announcement that he was terminating the ceasefire with Iran and moving to restore a blockade on Iranian maritime shipping.

A single-day oil price spike of that magnitude demands a question: has the energy market fundamentally changed, or has it just panicked?

The answer sits at an unusual intersection. The Strait of Hormuz threat is real, but the global energy system handling it today operates under a structurally altered set of conditions compared with those prevailing before Russia’s 2022 invasion of Ukraine. Supply chains have diversified. Non-OPEC output has grown. Storage buffers have expanded. The market’s toolkit for absorbing a Gulf disruption is larger than it was a decade ago, and that matters for how you read the price on screen.

Here is the framework for separating the fear component of this spike from the fundamentals component, and for identifying the three variables that will determine whether the move sticks or reverses.

What just happened in oil markets

The trigger was specific. President Trump formally declared the ceasefire with Iran at an end and signalled his intention to restore a blockade targeting Iranian maritime shipping. Oil markets responded immediately.

- Trigger event: Trump’s declaration ending the ceasefire and announcing the maritime blockade

- Magnitude: A single-day surge of nearly 10% on Monday (week of 17 July 2026), with intraday moves ranging approximately 9-13%

- Subsequent behaviour: Brent settled in the low $80s, roughly $80 per barrel at time of commentary, with partial retracement already visible in subsequent sessions

Near-10% in a single session. That is one of the sharpest single-day moves in Brent crude in recent years, and the kind of headline number that forces a reassessment.

The partial retracement matters. Even within the spike’s own momentum, market participants began walking back the worst-case assumptions. Traders priced in a full Strait of Hormuz disruption on Monday morning. By the time the session closed, and in the sessions that followed, they were already reassessing whether that scenario was actually unfolding. The settlement level in the low $80s, not the $90s or $100s, tells you something about where the market’s collective judgement actually landed.

When big ASX news breaks, our subscribers know first

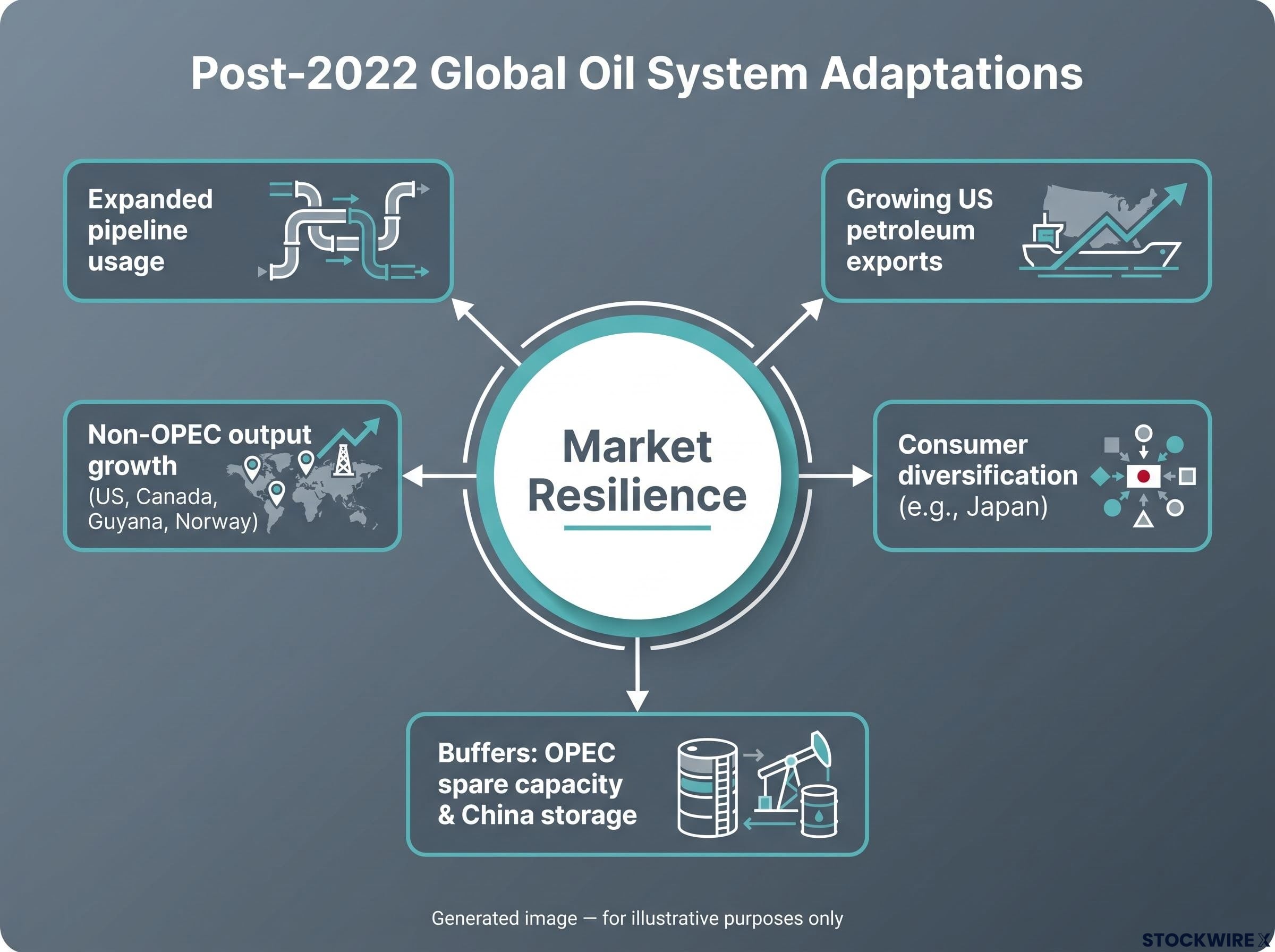

Why the global oil system is better equipped to absorb this than it looks

The spike arrived into an energy market whose underlying architecture has shifted substantially since Russia’s 2022 invasion of Ukraine. That invasion drove deeper and more durable structural changes to global energy markets than virtually any comparable shock in the modern era, and the resilience built since then is now functioning as a set of genuine shock absorbers.

The adaptations are specific and documented:

- Expanded pipeline usage has reduced dependence on any single maritime corridor

- Growing US petroleum exports have reshaped global supply flows

- Non-OPEC output growth from the US, Canada, Guyana, and Norway has added significant new barrels outside OPEC’s direct control

- Consumer diversification is already advanced; Japan, for example, had already shifted its energy sourcing away from traditional Gulf suppliers before this conflict began

Non-OPEC output growth from the United States, Canada, Guyana, and Brazil has fragmented the supply landscape that OPEC once dominated, with US production averaging 13.2 million barrels per day in 2025 and rising, compressing the cartel’s effective pricing lever to a fraction of its historical range.

The surplus backdrop the spike is fighting against

The International Energy Agency (IEA) assesses that global supply is currently ample, with rising non-OPEC output expected to exceed demand growth in 2026. OPEC holds significant spare capacity. China’s large onshore and floating storage provides a further buffer against short-term Gulf export disruptions.

Fisher Investments frames it directly: the Strait of Hormuz is considered less strategically vital than in prior periods due to these structural adaptations. The vulnerability map for a Hormuz disruption has genuinely shrunk, and pricing the current spike as if it carries the same leverage it once did is likely to overstate the risk.

Is this a fear premium or a new equilibrium?

Start with the market’s own language. Analysts across major outlets describe the current environment as “cautious” rather than panicked. That distinction matters. A panicked market reprices everything at once, forcing liquidations and dislocating forward curves. A cautious market adds a risk premium and waits for more information.

The evidence leans toward fear premium:

- The case for a fear-driven spike:

- Prices settled in the low $80s, consistent with a risk premium layered on otherwise balanced fundamentals, not a runaway shortage

- The IEA and bank strategists confirm global supply remains ample

- Partial retracement from the Monday peak suggests participants are reassessing, not capitulating

- The case for a structural repricing:

- The ceasefire’s collapse reintroduces genuine chokepoint risk for roughly 20% of the world’s traded oil

- Shipping insurance costs and tanker rerouting create real, measurable friction even without a full closure

- Duration of hostilities remains unknown, which keeps the risk premium from dissipating fully

War-risk insurance premiums are set by P&I clubs on actuarial rather than diplomatic timescales, meaning shipping hesitancy persists for weeks to months after any ceasefire is signed and creates measurable friction costs that keep a risk premium embedded in Brent even when physical passage is technically possible.

Fisher Investments’ framing: Financial markets price anticipated conditions 3 to 30 months ahead rather than reacting solely to current events, and markets do not require ideal conditions to continue functioning effectively. The current spike likely embeds a forward risk premium, not a pure reflection of present physical supply disruption.

Prior surges during the current conflict support this reading. When Brent briefly touched above the $120 range at earlier stages of the conflict, subsequent trading quickly reversed those gains as participants concluded the market had overshot on fear. That pattern of spike-and-reassess has already established a precedent.

The low-$80s level is more consistent with a market pricing a risk scenario than with a market signalling that a physical shortage has already arrived. That distinction has direct implications for how transient the move may prove.

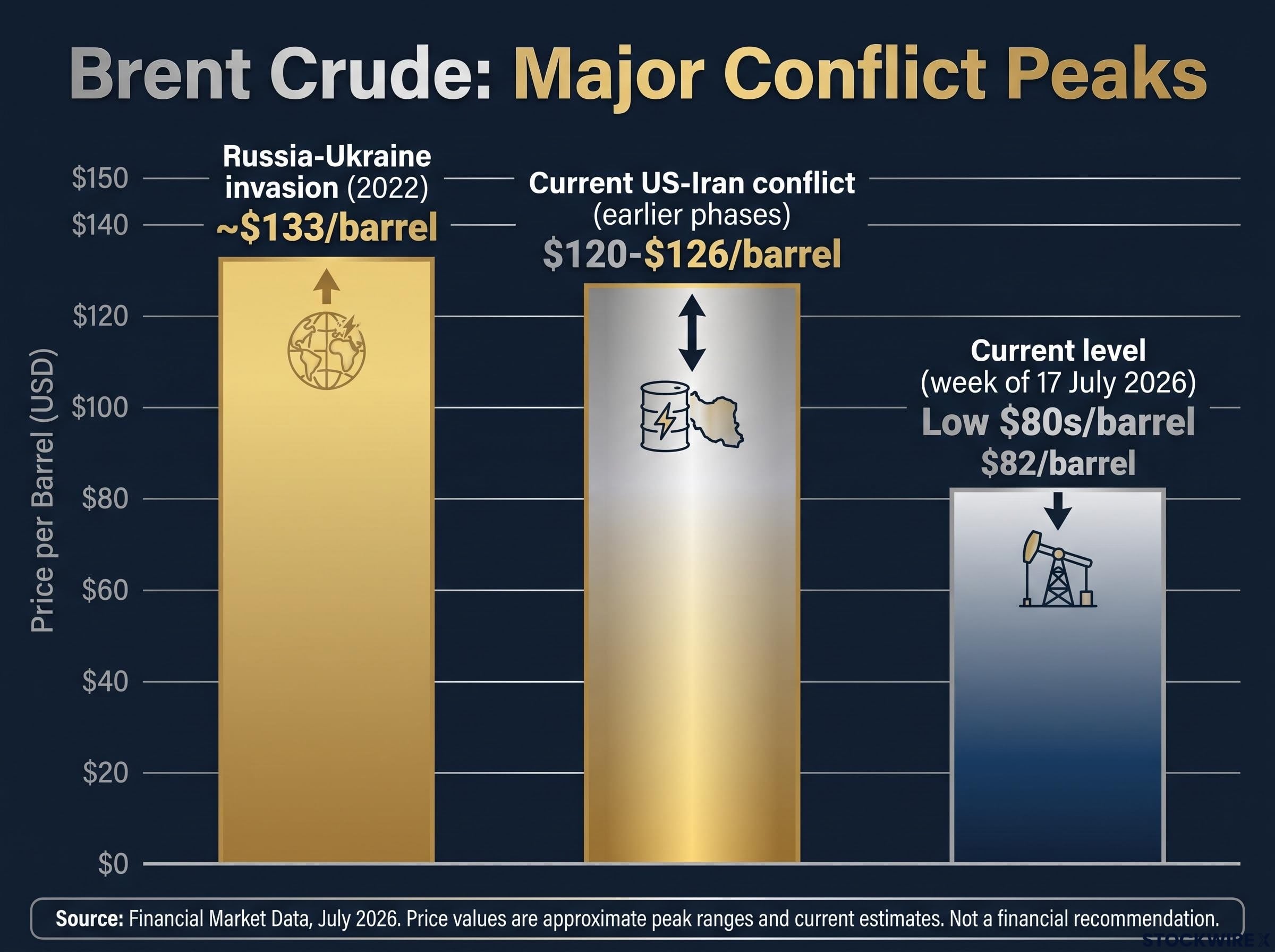

Historical anchoring: how this spike compares to past energy shocks

Context changes the shape of a number. A near-10% single-day move sounds alarming. But the level it reached tells its own story.

| Event | Peak Brent price | Subsequent behaviour |

|---|---|---|

| Russia-Ukraine invasion (2022) | ~$133/barrel | Declined relatively quickly |

| Current US-Iran conflict (earlier phases) | Briefly above $120-$126/barrel* | Knocked back by market reassessment |

| Current level (week of 17 July 2026) | Low $80s/barrel | Partial retracement from near-10% spike |

*Earlier conflict-phase peaks are reported but not independently verified.

Russia’s 2022 invasion remains the most relevant recent reference point. Brent reached a high of approximately $133 per barrel before retreating over the months that followed. The structural adaptations that invasion triggered, from pipeline diversification to accelerated non-OPEC output growth, are precisely the shock absorbers that are moderating the current spike.

The gap between $133 (2022 crisis peak) and $80 (current spike level) is not just a number. It is an implicit market verdict on how differently this conflict is being assessed relative to the last major energy shock. That gap, after a near-10% single-day move, argues for proportion over panic.

The next major ASX story will hit our subscribers first

Three scenarios that would turn this from overreaction into something worse

The structural resilience case holds only if certain worst-case scenarios fail to materialise. Three variables matter more than any single session’s percentage move:

- A full, sustained closure of the Strait of Hormuz. This would be qualitatively different from what markets are currently pricing. Some analysts estimate a reopening could knock $10-$20 off Brent (this figure is reported but not independently verified), implying that today’s level already embeds a sizeable closure risk premium. If closure is avoided or brief, significant mean reversion is likely.

- Broad regional escalation into major Gulf producers. A conflict that draws in additional producers or causes significant damage to export infrastructure would erode the diversification and spare capacity arguments. This scenario most directly challenges the structural shock-absorber case made above.

- Extended duration. A brief flare-up with partial disruptions is manageable in a surplus environment. A multi-month conflict that repeatedly impairs shipments and tests stockpiles, pipelines, and alternative routes would be fundamentally different, potentially converting a fear-driven spike into a genuine structural repricing.

Some analysts estimate that a reopening of the Strait of Hormuz could instantly knock $10-$20 off Brent prices. If that estimate is even directionally correct, it tells you how much speculative premium is already embedded in the current level. (Note: this estimate is reported but not independently verified.)

These three variables are your monitoring framework. Tracking them is how you distinguish noise from signal in the weeks ahead.

What the spike tells you, and what to watch next

The evidence, as it currently stands, points in one direction. The low-$80s spike is consistent with a market pricing elevated uncertainty rather than a catastrophic, structural shortage. The fundamentals support that reading: surplus supply, OPEC spare capacity, storage buffers, rising non-OPEC output, and a global energy system that has already adapted to life with chokepoint risk.

That assessment holds only if the three escalation scenarios fail to materialise. The variables to watch:

- Strait of Hormuz status: Any move toward full, sustained closure changes the calculus entirely

- Regional escalation scope: Whether the conflict draws in additional Gulf producers or damages export infrastructure

- Duration: Whether hostilities extend into a multi-month campaign that tests the system’s reserves and alternative routes

Fisher Investments has long argued that markets can absorb imperfect conditions without breaking down, and the current situation, for all its genuine risk, has not yet crossed the threshold of a structural rupture in global energy supply. The spike was real. The fear is legitimate. But the evidence points toward an overshoot rather than a new regime, and the variables that would change that verdict are known and watchable.

Geopolitical risk investing has shifted from a tail-risk consideration to a base-case portfolio variable for major allocators, with the oil shock transmitting through inflation expectations, central bank signalling, and equity market sell-offs across multiple asset classes simultaneously.

This article is for informational purposes only and should not be considered financial advice. Oil and energy exposures carry significant risk. Investors should conduct their own research and consult with financial professionals before making investment decisions. Portfolio decisions should reflect individual objectives, constraints, and risk tolerance.