JPMorgan’s equity strategy team declared on Monday that consumer cyclical stocks have hit a floor, naming the second half of 2026 as the window when a sector that has trailed every other cyclical group for years could finally turn. The call comes from Mislav Matejka, Head of Global Equity Strategy at J.P. Morgan, one of Wall Street’s most closely followed research desks, and it rests on a specific convergence: consumer equities sitting at multi-year relative lows, consumer confidence near historic lows across most global regions, and three macro catalysts arriving simultaneously. By the end of this piece, you will understand exactly why JPMorgan believes this moment is different, which subsectors the bank favours (and the one it explicitly avoids), and what data points to watch in real time to judge whether the thesis is playing out.

Why consumer stocks became the market’s biggest laggard

While other cyclical segments rode clear structural tailwinds through the post-COVID period and into 2026, consumer cyclicals found no equivalent driver. Financials, industrials, and technology each had a specific engine propelling them forward, while consumer names were left behind:

- Financials rode a rising interest rate environment that fattened net interest margins.

- Industrials benefited from a sustained wave of infrastructure-related spending.

- AI-linked technology surged on growth expectations tied to artificial intelligence adoption.

- Consumer cyclicals lacked any comparable structural catalyst, leaving their relative price performance grinding down to multi-year lows.

That divergence sits at the core of JPMorgan’s argument. Rather than a reason for caution, Matejka frames this sustained underperformance as the very condition that creates opportunity: a sector where negative expectations are already embedded in valuations, and where even a partial improvement in the backdrop could produce disproportionate relative gains.

Sentiment as a contrarian signal, not a warning

According to JPMorgan’s mid-2026 assessment, consumer confidence gauges across most global regions are hovering near historic lows. On the surface, that appears to support a cautious stance. But the bank’s reading of history points the other way.

The University of Michigan Consumer Sentiment Index reading for June 2026 came in at 48.9, recovering marginally from May’s all-time low of 44.8, a level that places current sentiment firmly in the historically depressed range that JPMorgan’s analysis identifies as a contrarian setup for the sector.

Stock markets tend to price in economic conditions well before those conditions show up in hard data. By the time sentiment reaches its most depressed levels, much of the damage is typically already reflected in share prices. Matejka’s analysis suggests that troughs in consumer confidence have, in the past, set the stage for stronger-than-average equity performance in the sector, precisely because any recovery from such a low base can move prices sharply. The further pessimism has run, the more powerful the eventual re-rating tends to be.

When big ASX news breaks, our subscribers know first

The three catalysts JPMorgan says could trigger the recovery

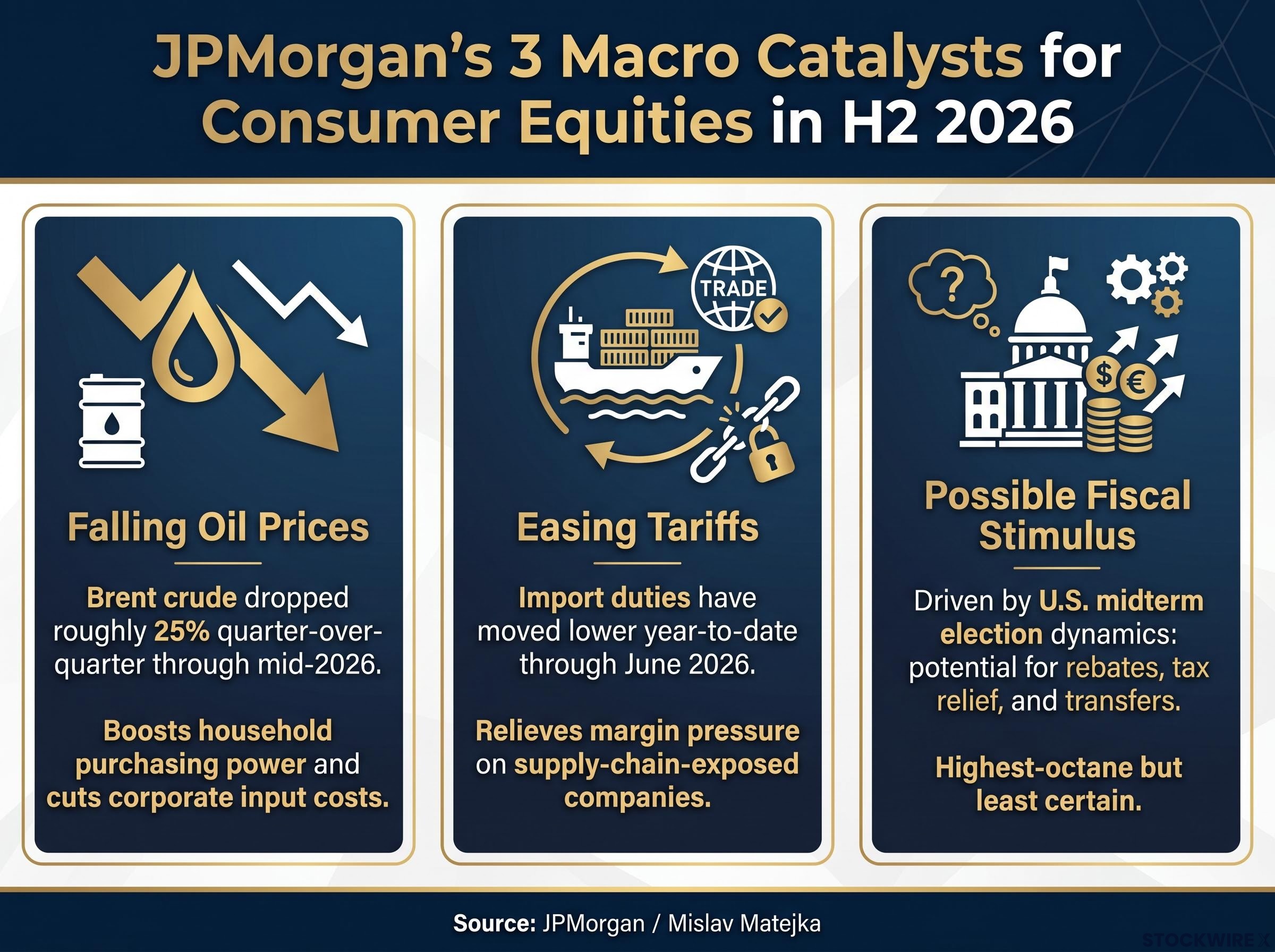

Matejka’s team does not rely solely on valuation and sentiment. The note identifies three macro forces that could convert a statistical floor into an actual recovery, each with a direct transmission mechanism to consumer earnings.

- Falling oil prices: Brent crude dropped roughly 25% on a quarter-over-quarter basis through mid-2026, with the decline boosting household purchasing power while also cutting input costs for consumer-facing businesses at the same time.

- Easing tariffs: Import duties have moved lower year-to-date through June 2026, relieving pressure on supply-chain-exposed consumer companies that had seen margins squeezed by what amounted to a tax on imported goods.

- Possible fiscal stimulus: U.S. midterm election dynamics raise the probability of household-targeted fiscal measures (rebates, tax relief, transfers), the highest-octane catalyst but the least certain.

Brent crude’s roughly 25% quarter-over-quarter fall is the most concrete data point in the thesis, with the price drop feeding through to both consumer energy costs and corporate cost structures at the same time.

The catalysts are ordered by certainty for a reason. Oil is already down. Tariffs have already eased. Fiscal support remains a political scenario. But if all three even partially materialise together, the earnings recovery in consumer names could accelerate faster than current consensus expects, which is the core opportunity JPMorgan is positioning for.

What consumer cyclicals actually are and why they matter to a portfolio

Consumer cyclicals are companies whose revenues rise and fall with household spending confidence and disposable income. When consumers feel confident and have money to spend, these businesses thrive. When confidence drops and budgets tighten, they suffer disproportionately.

The sector spans a wide range of industries:

- Luxury goods

- Airlines and hotels

- Restaurants and leisure

- General retail

- Automobiles

That diversity is precisely why the sector matters for portfolio construction. Consumer cyclicals amplify economic cycles: they underperform more sharply in downturns and rebound more aggressively when conditions improve. JPMorgan frames this as a 6-24 month regime call, not a stock-picking opinion. The question the thesis asks is not “are these great companies?” but “is the macro backdrop about to improve?”

Consumer cyclicals amplify economic cycles more sharply than almost any other segment, which is why cyclical vs defensive allocation decisions carry outsized consequences at turning points: the same characteristics that dragged this sector down through the post-COVID tightening cycle are precisely what make it a high-octane instrument when conditions reverse.

Why mean reversion is a legitimate framework here

Mean reversion, the tendency for extreme performance gaps to narrow over time, breaks down in sectors facing permanent structural impairment (think legacy print media or commoditised manufacturing being displaced by technology). Consumer cyclicals do not fit that profile. Households will always spend on goods, travel, and experiences. The sector’s economic importance and diversity make structural collapse scenarios unlikely, which means extended multi-year underperformance tends to set up future relative outperformance rather than permanent decline.

Where JPMorgan is placing its bets, and where it is not

The call is selective. Matejka’s team is not endorsing every consumer name indiscriminately.

The parallel case for European consumer stocks published in mid-June 2026 by Barclays’ Emmanuel Cau adds regional texture to JPMorgan’s global thesis: US luxury spending accelerated from 6% in Q1 to 17% quarter-to-date by mid-June, suggesting the demand recovery Matejka is positioned for may already be showing in high-frequency data across the Atlantic before it registers in broader confidence surveys.

| Subsector | JPMorgan Stance | Key Driver | Primary Risk |

|---|---|---|---|

| Luxury | Favoured | Pricing power, strong balance sheets, fast re-rating on sentiment shift | China demand slowdown |

| Travel & Leisure | Favoured | Double benefit: demand recovery plus lower fuel costs | Renewed energy price spike |

| Retail | Favoured | Operating leverage to traffic, mix, and input cost improvements | Consumer recession |

| Autos | Cautious | Some valuation support after extended weakness | Overcapacity, EV transition complexity, pricing normalisation |

The autos carve-out is the most practically useful signal in the entire note. Matejka acknowledged that auto valuations have become increasingly extended on the downside, but structural headwinds (overcapacity, the complexity of the EV transition, and post-pandemic pricing normalisation) are sufficient to override the macro tailwind logic.

That exception tells you something beyond autos. Before acting on any piece of this thesis, run the same structural screen the bank ran on autos against whatever name or fund you are considering. Macro tailwinds do not automatically erase structural problems at the subsector level.

How to think about this call without overreacting to it

A Wall Street floor call is a starting point for analysis, not a trading trigger. Matejka’s thesis implies a 6-24 month time horizon, a regime shift, not a signal to buy on Monday morning. Volatility within that window should be expected, and the sector could easily move ahead of hard economic data actually improving.

The broader 2026 equity outlook from five major asset managers, including BlackRock and JPMorgan, frames the consumer cyclical thesis within a more complex late-cycle picture: institutions maintain overweight equity positions overall, but diverge sharply on which sectors carry the most risk, with Morgan Stanley and Bank of America flagging a potential 10-20% drawdown that would test the durability of any sector-rotation call.

The risks that could derail the setup

Three downside scenarios would require reassessing the thesis entirely:

- A renewed energy price spike that reverses the household income and corporate margin benefits.

- A global recession signal that overwhelms the positive macro catalysts.

- An aggressive return to monetary policy tightening that reprices risk assets broadly.

These are not reasons to dismiss the call. They are conditions that would change the setup the call depends on.

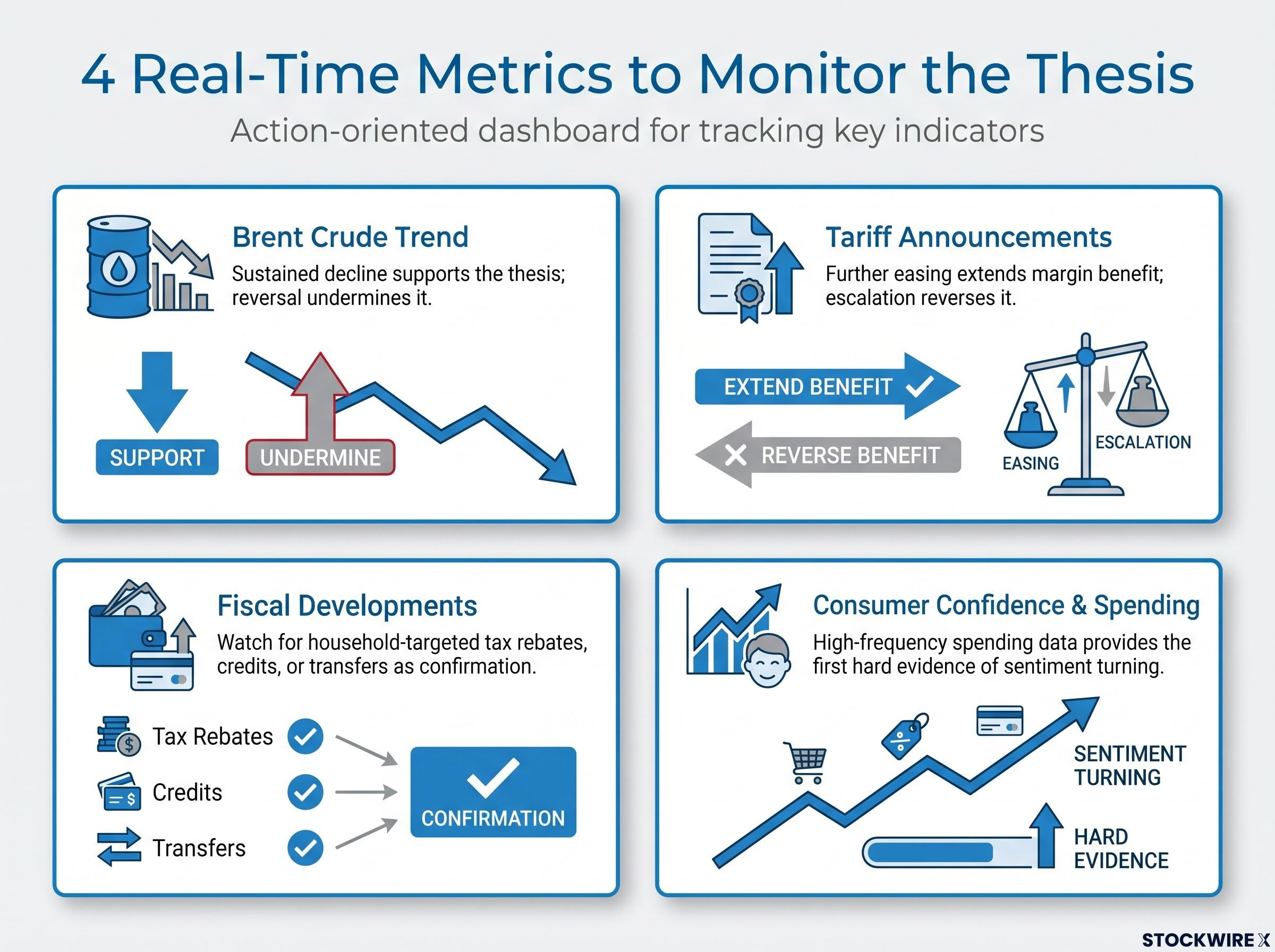

To track whether the thesis is playing out, monitor four data points in real time:

- Brent crude trend: sustained decline supports the thesis; a reversal undermines it.

- Tariff announcements: further easing extends the margin benefit; escalation reverses it.

- Household-targeted fiscal developments: tax rebates, credits, or transfers would be the highest-impact confirmation signal.

- Consumer confidence indices and high-frequency spending data: the first hard evidence of whether sentiment is turning.

A well-constructed contrarian call can still be early by six to twelve months. Knowing the specific signals that confirm or invalidate the thesis is what separates a disciplined response from an impulsive one.

For investors monitoring whether the thesis is playing out in real time, our full explainer on quarter-end rebalancing mechanics covers the approximately $165 billion in institutional selling pressure JPMorgan itself flagged for late June 2026, providing the context needed to distinguish temporary mechanical price moves driven by pension and sovereign wealth fund rebalancing from genuine shifts in sector momentum.

The next major ASX story will hit our subscribers first

JPMorgan’s floor call matters because of who is making it, and when

Matejka is not a junior analyst floating a speculative idea. As Head of Global Equity Strategy at J.P. Morgan, his directional calls move institutional capital. The note was published on 22 June 2026, precisely at the moment the bank believes the H2 2026 recovery window is opening.

The three-pillar case: consumer cyclicals sitting at multi-year relative performance troughs, consumer confidence gauges depressed across most global regions, and three specific macro catalysts (oil, tariffs, fiscal support) arriving together in H2 2026.

The relevant question is not whether to follow the call blindly. It is whether your current portfolio already reflects or contradicts the setup Matejka is describing.

The consumer stocks outlook for H2 2026 reflects a broader shift already underway

JPMorgan is not predicting an economic boom. It is identifying a sector where bad news is priced in and where several simultaneous macro forces could unlock a multi-quarter recovery. The thesis works for luxury, travel and leisure, and retail. It does not work for autos. And it depends on at least partial catalyst materialisation.

The right response is to assess your current consumer sector exposure against this framework, monitor the four data points outlined above, and treat any position as a risk-managed tilt within a broader portfolio, not a directional bet on a single macro narrative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking statements are speculative and subject to change based on market developments, geopolitical events, and company performance.

—