Bank of America published a client note on 17 July 2026 arguing the Federal Reserve needs to raise interest rates three more times this year. The call, authored by analyst Aditya Bhave, puts the bank at the hawkish end of Wall Street even as softer June inflation data gave other forecasters reason to pull back.

The note arrives at a moment of genuine market confusion. June’s Consumer Price Index (CPI) came in below expectations. Polymarket puts the odds of a July Fed hold at roughly 73.5%. Yet BofA’s analysts are not just holding their ground; they are framing 75 basis points of additional tightening as a floor, not a ceiling. For retail investors, a forecast this far outside the consensus deserves a clear-eyed examination of the reasoning behind it.

Here is what BofA is actually arguing, why its view diverges so sharply from market pricing, and what Fed rate hikes on this scale would mean for portfolios positioned around the assumption that the tightening cycle is already over.

June’s soft inflation print did not change BofA’s view, and here is why

Start with what looked like good news. June headline CPI dropped 0.4% on a monthly basis, finishing below what analysts had anticipated. Core CPI (which strips out food and energy) recorded a monthly fall, a result that has occurred on just seven occasions since 1985. On the surface, the data read like a pressure valve opening.

BofA acknowledged the numbers. The bank adjusted its core Personal Consumption Expenditures (PCE) month-over-month tracking figure, the metric the Fed actually uses to set policy, to 0.15% for June, reflecting the softer reading. But that is a monthly revision, not a structural reversal.

The annual picture tells a different story. BofA’s year-over-year core PCE forecast remained unchanged at 3.3%, sitting roughly 130 basis points clear of the Fed’s 2% target. One soft monthly CPI print is not the same metric the Fed uses to make rate decisions, and BofA is explicitly arguing the annual trajectory has not improved enough to matter.

The core PCE trajectory that BofA is tracking held at 3.4% year-over-year as recently as May 2026, sitting 140 basis points above the Fed’s target and providing no basis for cuts, a data point that reinforces BofA’s argument that one soft monthly CPI print has not shifted the structural picture.

The June CPI data that BofA was responding to showed core inflation flatline at 0.0% month-over-month, the largest downside miss relative to consensus in over a year, pulling the annual core rate to 2.6% and prompting most forecasters to strengthen their case for earlier rate cuts.

- Headline CPI (June 2026): -0.4% month-over-month

- Core CPI monthly decline: seventh occurrence since 1985

- BofA core PCE tracking (June): revised down to 0.15% month-over-month

- BofA year-over-year core PCE projection: 3.3%

- Fed inflation target: 2%

Bhave’s framing: A single soft monthly reading does not change the structural picture. Annual core inflation is still elevated and drifting higher, not falling decisively back toward 2%.

When big ASX news breaks, our subscribers know first

What does 75 basis points actually mean, and how did BofA get there

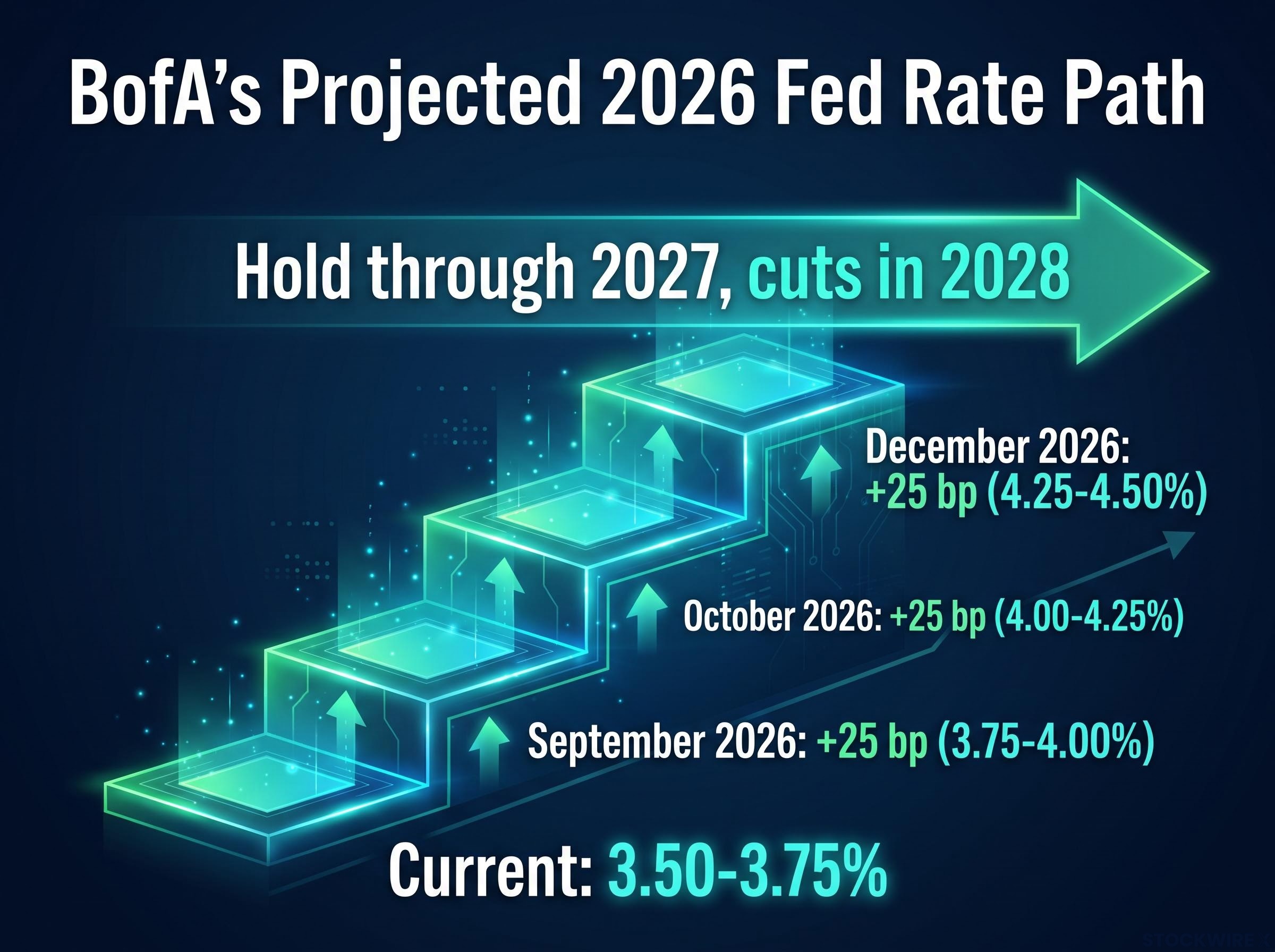

A basis point is one hundredth of a percentage point. When BofA says it expects 75 basis points of hikes, it means three separate 25-basis-point increases, each one lifting the Fed’s benchmark rate by a quarter of a percentage point. The bank projects those moves for September, October, and December 2026, which would take the federal funds target range from its current 3.50-3.75% to approximately 4.25-4.50%.

| Meeting month | Projected action | Resulting target range |

|---|---|---|

| September 2026 | +25 bp hike | 3.75-4.00% |

| October 2026 | +25 bp hike | 4.00-4.25% |

| December 2026 | +25 bp hike | 4.25-4.50% |

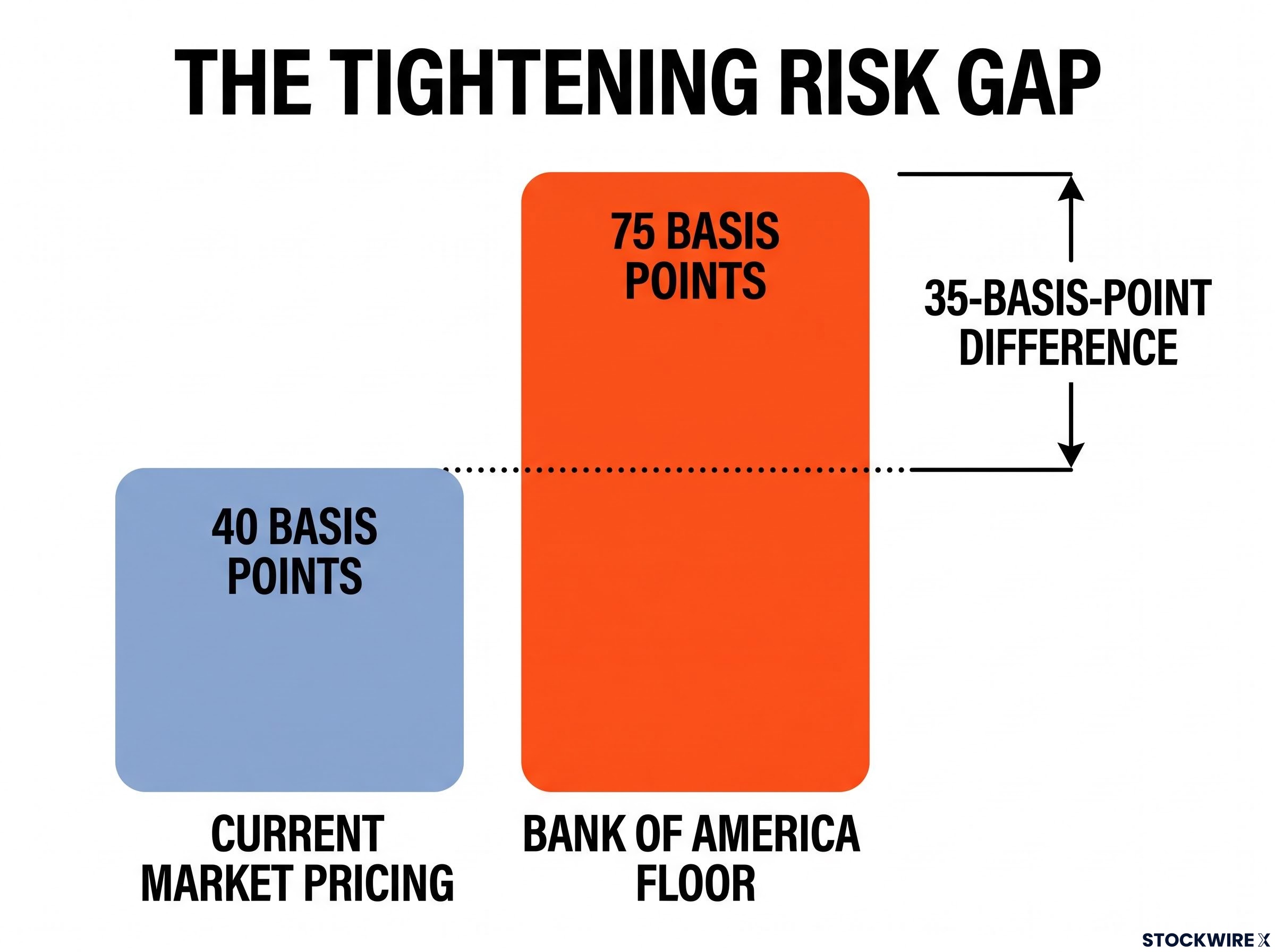

That matters because markets have only priced in roughly 40 basis points of hikes as of mid-July. The gap is not a rounding error.

The pricing gap: Current market pricing reflects around 40 bp of additional tightening, whereas BofA places the minimum required at 75 bp. That 35-basis-point difference represents a materially different rate environment, one that would reprice bonds, growth equities, and mortgage-sensitive assets if BofA proves correct.

BofA’s base case also calls for rates to hold through 2027, with cuts only beginning in 2028. That extends the duration of tightening well beyond what many investors may be anticipating.

Who is Kevin Warsh, and why does BofA see him as the catalyst for renewed tightening

Kevin Warsh was confirmed as Federal Reserve Chair effective 22 May 2026. In BofA’s forecast, his appointment is not background context. It is an active variable shifting the bank’s probability calculus toward more aggressive tightening.

Warsh’s confirmation into a 3.8% headline CPI environment was immediately flagged by markets as a potential inflection point, with three regional Fed presidents already calling for Q3 hikes and CME FedWatch pricing only a 37% probability of any move before year-end at that time.

What Warsh’s testimony showed

BofA assessed Warsh’s recent congressional testimony and found three things worth noting:

- A firm emphasis on bringing inflation back under control

- A broadly positive assessment of the productivity growth outlook

- No fresh policy signals, and nothing to suggest that newly created task forces would provide grounds for deferring rate increases

In short, continuity rather than a dovish pivot.

How BofA reads his incentives

BofA goes further than the testimony itself. The bank contends that Warsh holds good reasons to move on rates without delay: acting promptly would build his inflation-fighting credibility while allowing him to avoid being held responsible for the price pressures that took hold before he took office. This is BofA’s interpretive framing, not a statement from Warsh or documented Fed policy. But it is a stated component of the bank’s published reasoning, and it explains why BofA treats the leadership change as an inflation-hawkish signal rather than a neutral transition.

BofA’s pushback on the “transitory factors” argument

BofA was explicit about the client scepticism it was addressing: the argument that recent price pressures stem from one-time or temporary factors rather than embedded inflation. The bank’s response was direct.

- The labour market remains resilient, with strong job growth giving the Fed room to tighten

- Energy price pressures are adding to inflationary forces rather than signalling demand weakness

- Tariffs are layering additional cost pressure onto an already elevated inflation base

- 75 basis points is framed as a minimum, not merely a central estimate

Bhave’s assessment: “The data simply don’t warrant cuts this year. Core inflation is too high, and moving up.”

That puts BofA in direct disagreement with more optimistic market interpretations. If the bank’s structural-inflation argument is right and the transitory camp is wrong, investors positioned for a soft landing and imminent cuts are carrying more rate risk than they may recognise. The distinction is not academic; it determines whether portfolios built around a “peak rates” assumption are correctly positioned or exposed to a repricing event.

The next major ASX story will hit our subscribers first

What BofA’s scenario means for bonds, equities, and cash

The 75-basis-point path to 4.25-4.50%, followed by a hold through 2027, has specific implications across asset classes.

| Asset class | BofA scenario impact | Key consideration |

|---|---|---|

| Long-duration bonds | Price pressure from higher yields | Most directly rate-sensitive; vulnerability window extends through 2027 |

| Growth/tech equities | Discount-rate compression on valuations | More exposed to 4.25-4.50% terminal rate than to the 40 bp already priced |

| Short-duration and floating-rate | Higher yields with less price risk | Benefit directly from “higher for longer” environment |

| Financials | Higher net interest margins | Banks benefit, but credit risk warrants monitoring |

| Cash and short-term bills | Increasingly attractive relative yield | Holding high-yielding short-term instruments becomes more competitive against reaching for duration |

| REITs and mortgage-sensitive | Pressure on leveraged structures | Suffer disproportionately when tightening exceeds market expectations |

The core question for your portfolio is straightforward. If rates rise another 75 bp and stay there through 2027, does your current positioning survive that scenario? If the answer is unclear, BofA’s note is a prompt to stress-test now rather than after the first September hike.

Treasury yield dynamics that follow from a 75-basis-point hike cycle do not operate in isolation: at roughly $952 billion in annual interest payments, the federal government’s own debt servicing costs rise with each incremental move higher, compressing the equity risk premium and transmitting directly into mortgage rates at the household level.

What the consensus gets wrong if BofA is right

BofA’s three-hike forecast is currently the most hawkish among major Wall Street institutions. That alone is a reason to take it seriously as a risk scenario, not to dismiss it as an outlier. Outlier calls that prove correct are precisely the ones that catch consensus-positioned portfolios off guard.

The specific assumption BofA is challenging: that the roughly 40 basis points of hikes reflected in current market pricing captures the true extent of tightening ahead. The bank’s own analysis sets the minimum at 75 bp, which is close to twice what investors have built into their expectations.

The core gap: Investor pricing currently reflects around 40 bp of additional hikes, while BofA’s floor sits at 75 bp. That divergence is a measure of how much tightening risk the consensus may be leaving unaccounted for.

With September as the earliest scheduled hike in BofA’s forecast, there is still time to assess portfolio exposure before the cycle resumes. But the window to reposition around a “cuts-are-coming” assumption narrows with each inflation print that fails to show decisive progress back toward 2%. The consensus is not necessarily wrong. But if your portfolio implicitly assumes it is right, you should understand exactly what you are betting against.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—