BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

Goldman Sachs has identified one specific number, due Tuesday morning, as the most consequential near-term variable for U.S. equity markets. Options markets are already pricing in a meaningful swing either way.

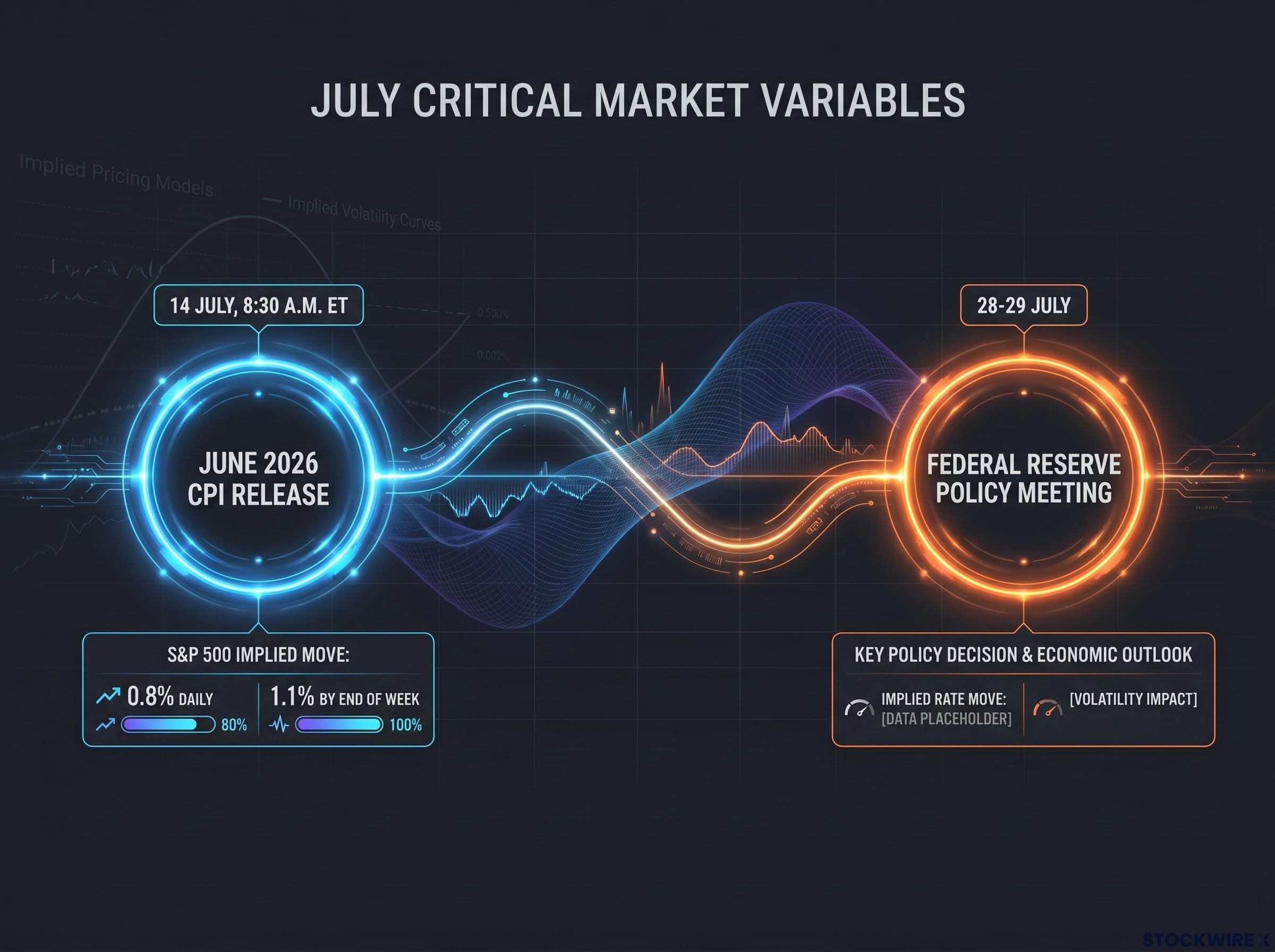

The June 2026 Consumer Price Index (CPI) release is scheduled for 8:30 a.m. ET on 14 July, and the Federal Reserve’s next policy meeting is set for 28-29 July. The window between an inflation surprise and a market repricing has rarely been shorter. Goldman’s concern centres on a precise transmission risk: even a moderate upside surprise in the inflation reading could push rate hike probabilities higher, squeezing valuations across a richly priced market that has built in very little tolerance for tighter policy.

Here is what Goldman is specifically watching, why this print carries more weight than a typical CPI release, and what the inflation equity risk means for how you should be positioned going into Tuesday.

Goldman’s warning is not a generalised inflation fear. It identifies a precise chain of events: an above-forecast CPI print raises the odds of further Fed rate increases, which flows directly into equity valuations via a steeper discount rate. The bank argues this is not a theoretical concern but a live one, given how little room an expensive market leaves for absorbing any hawkish policy shift.

Ahead of Tuesday’s release, the market had built in approximately 50 basis points of cumulative tightening stretching to mid-2027, a figure Goldman treats as the central risk variable. That number is both the risk and the opportunity. If CPI comes in hot, that figure climbs and equities reprice lower. If the print is soft, some of that priced-in tightening unwinds and equities get a tailwind.

The June 2026 FOMC minutes confirm that policymakers held the federal funds rate steady while explicitly acknowledging inflation running above the Fed’s 2% longer-run objective, a posture that leaves the July meeting highly sensitive to any upside CPI surprise.

Goldman’s June core CPI estimate: approximately 0.17% month-over-month, running under the broader market consensus.

For headline CPI, Goldman put its estimate at roughly -0.11%, with lower energy prices doing most of the work in pulling the figure negative. The bank also noted that the current setup resembles earlier periods when stretched valuations meant equities had little buffer against any policy tightening that arrived faster than expected. The implication is direct: if you hold rate-sensitive positions, your exposure runs in both directions on this print.

June inflation data published on 30 June already showed gasoline prices retreating roughly 11.5% from their May peak, a shift that Goldman’s approximately -0.11% headline forecast reflects directly and that sets the baseline expectation against which Tuesday’s actual print will be measured.

| Scenario | Core CPI direction | Fed expectations | Likely equity impact |

|---|---|---|---|

| Hot print | Above 0.17% m/m | Tightening expectations rise beyond 50 bps | Valuations compress, rate-sensitive names sell off |

| Soft print | At or below 0.17% m/m | Priced-in tightening partially unwinds | Relief rally, growth stocks recover |

Options markets have already made a concrete bet on the size of Tuesday’s move. According to options pricing, the S&P 500 could shift by around 0.8% on the day of the CPI release itself, with the implied move widening to approximately 1.1% by the end of that week. That is not a directional bet; it is a measure of uncertainty, and it is meaningfully above the average CPI-day implied move over the past 12 months.

An 0.8% implied daily move on a single data print tells you that institutional positioning is already defensive. For investors with concentrated exposure to rate-sensitive names, this is a concrete risk calibration, not background noise.

Goldman identified three categories of equities most vulnerable if the print triggers a hawkish repricing:

The headline CPI number will dominate Tuesday’s initial reaction, but the sub-components are what the Fed actually watches. If you want to interpret the 8:30 a.m. print in real time rather than waiting for analyst commentary hours later, here is what matters in order of Fed-policy relevance:

The May 2026 CPI print delivered a 4.2% headline reading driven almost entirely by a 40.5% annual surge in gasoline prices, while core CPI held at a comparatively contained 2.9%, establishing the split between energy-driven headline figures and stickier underlying measures that the June release will now either confirm or complicate.

Goldman’s headline figure is pegged at roughly -0.11%, with energy price declines carrying the bulk of that move lower. Set that against the actual release at 8:30 a.m. ET on Tuesday.

The bank’s June core CPI estimate of approximately 0.17% month-over-month comes in below where consensus currently sits. If that forecast proves accurate, it would support the case that disinflation is progressing and reduce immediate pressure for additional tightening. But if shelter or core services re-accelerate even modestly above that forecast, a single sub-component could be enough to shift rate expectations and pressure growth stock valuations, regardless of what the headline number shows.

Goldman’s near-term inflation warning sits inside a broader outlook that remains constructive on equities. The two positions are not contradictory; they operate on different timeframes.

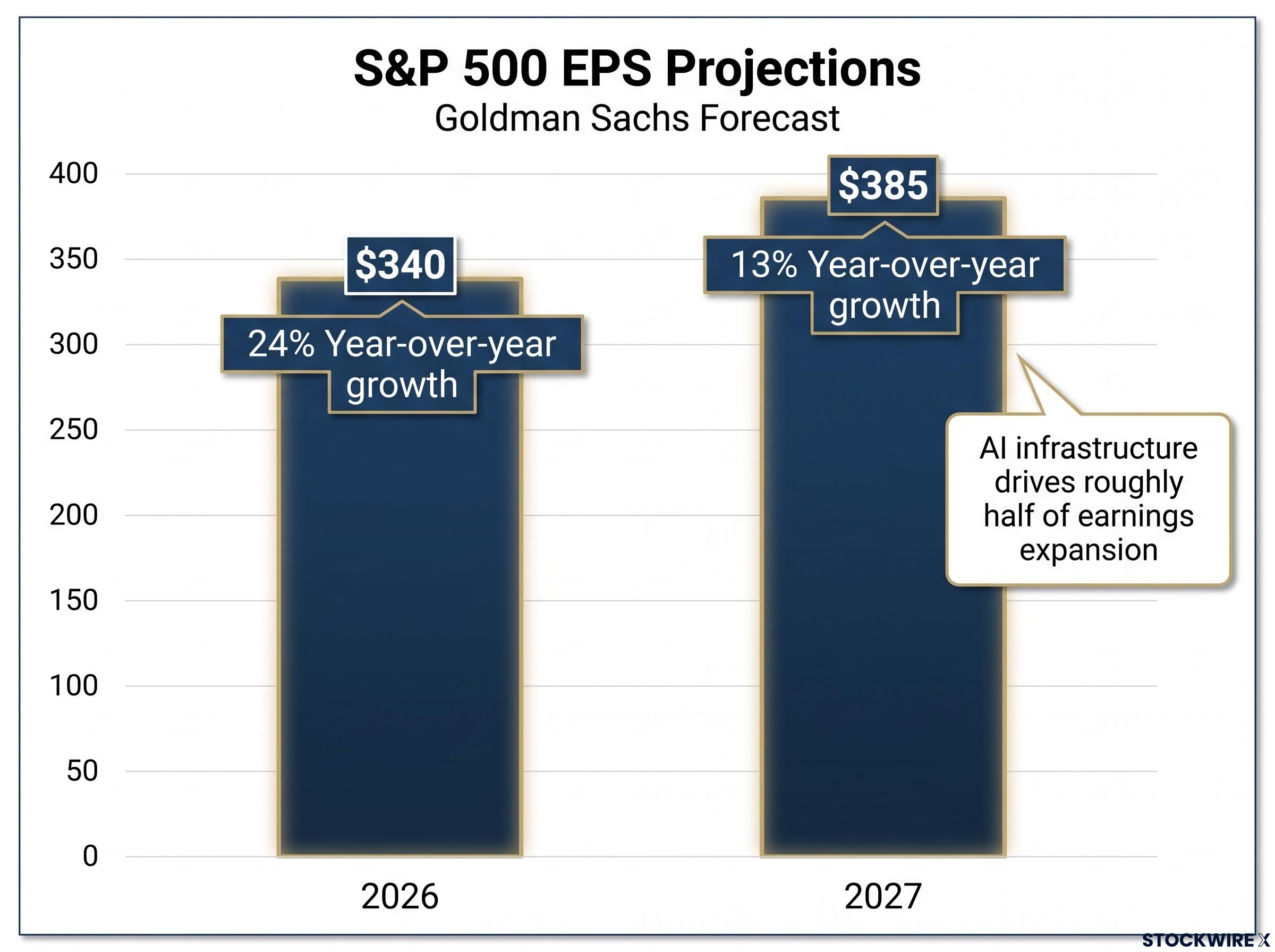

The earnings trajectory Goldman projects is substantial. S&P 500 earnings per share (EPS), the portion of a company’s profit allocated to each outstanding share of stock, are forecast at $340 for 2026, representing 24% year-over-year growth, and $385 for 2027, representing 13% growth. AI-infrastructure beneficiaries account for roughly half of that earnings expansion.

The risk that earnings growth already priced in by the market limits upside even if Goldman’s $340 EPS forecast proves accurate sits at the core of Bank of America’s analysis, which shows the S&P 500 trading expensive on 16 of 20 valuation metrics and consensus long-term growth expectations at their highest level since 2021.

| Year | EPS projection | Year-over-year growth | Key driver |

|---|---|---|---|

| 2026 | $340 | 24% | AI infrastructure and broad earnings recovery |

| 2027 | $385 | 13% | Continued AI momentum and margin expansion |

Goldman’s July 2026 US Market Pulse expects risk assets to move higher in H2 2026, and the firm’s 2026 global growth forecast sits at 2.8%. The tension is real but specific: elevated valuations mean the constructive destination can still be reached via a bumpier path. Even if Tuesday’s print triggers a short-term de-rating, the earnings foundation under equities remains intact for investors with a six-to-twelve-month horizon.

Goldman’s warning translates the abstract inflation risk into a specific portfolio audit. The positioning logic is concrete:

The record equity inflows of $150 billion recorded in June 2026, flagged by Barclays as a FOMO-driven crowding signal rather than a fundamental re-rating, compound Goldman’s inflation concern by reducing the market’s capacity to absorb a hawkish surprise: when positioning is already maximal, a modest repricing trigger can produce a disproportionate price move.

BlackRock’s 2026 Midyear Outlook corroborates the concentration risk: narrow AI-driven leadership amplifies vulnerability if financing conditions tighten.

For an investor holding a growth-heavy, rate-sensitive portfolio, the right read from Goldman’s warning is not to exit equities but to audit exposure to floating-rate-debt-heavy names before Tuesday’s open. The medium-term case remains constructive; the near-term path is binary, and balance sheet quality is the filter that separates the names that absorb a hawkish surprise from those that buckle under one.

Tuesday’s CPI is consequential for near-term equity pricing, but it is not a verdict on the medium-term earnings thesis that both Goldman and BlackRock endorse. The 50 basis points of priced-in tightening is the live variable: it either unwinds or expands depending on the print, and that single repricing will set the tone through the end of July.

What remains open after Tuesday:

Goldman’s constructive horizon extends through H2 2026 and into 2027. Tuesday’s number tells you how smooth or bumpy the path will be. It does not change the destination, unless the data says something the market has not yet begun to price.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Inflation equity risk is the danger that a higher-than-expected inflation reading forces the Federal Reserve to raise interest rates further, which increases the discount rate applied to future earnings and compresses stock valuations. Goldman Sachs has identified this as the live near-term threat heading into the June 2026 CPI release, particularly for a market already pricing in 50 basis points of cumulative tightening.

Goldman Sachs estimates June 2026 core CPI at approximately 0.17% month-over-month, which is below the broader market consensus, and headline CPI at roughly -0.11%, with declining energy prices doing most of the work in pulling the headline figure negative.

Goldman identified three categories most vulnerable to a hawkish repricing: highly leveraged companies carrying significant floating-rate debt, growth stocks trading at elevated multiples where higher discount rates directly compress valuations, and companies with weak balance sheets where tighter financing conditions erode both operational flexibility and investor confidence.

Options markets are pricing in an implied move of around 0.8% for the S&P 500 on the day of the CPI release itself, widening to approximately 1.1% by the end of that week, both figures meaningfully above the average CPI-day implied move over the prior 12 months.

Goldman's positioning logic centres on auditing concentration in rate-sensitive names before Tuesday's open, prioritising companies with strong balance sheets and low floating-rate debt exposure, while maintaining overall equity exposure given that both Goldman and BlackRock hold constructive medium-term stances on equities.