SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

19 hrs ago

BlackRock, the world’s largest asset manager with more than $11 trillion under management, published a geopolitical outlook dated 11 July 2026 that reportedly elevates two technology-driven risk categories to its highest threat tier. The first is a newly consolidated threat tier that brings cyber risk and terrorism under one classification, with AI-enabled activity by state-backed actors identified as the key driver. The second is a U.S.-China technology decoupling that BlackRock projects will push AI-related policy questions, from data centres to labour disruption, toward the centre of U.S. midterm election debate.

A formal reclassification by BlackRock carries weight beyond the firm’s own portfolios. Its Geopolitical Risk Dashboard is one of the most widely tracked institutional signals in asset allocation, and changes to its risk taxonomy influence how capital flows across sectors. Publicly available BlackRock materials through mid-2026 have carried U.S.-China strategic competition at a Medium rating and listed cyber and terrorism as separate categories. If today’s report confirms a formal upgrade, it represents a material departure from that taxonomy.

Here is what the report reportedly says, where the evidence base is solid versus contested, and which sectors and positions are most directly in the crosshairs. You will finish knowing whether this changes anything about how you think about technology-sector exposure.

The 11 July 2026 BlackRock geopolitical outlook reportedly consolidates what were previously two distinct risk categories, cyber and terrorism, into a single high-risk tier. The reported rationale is that state-backed cyber operations, supercharged by increasingly powerful AI systems, now present threats to commercial entities and national security infrastructure that can no longer be usefully separated from terrorism as a risk class.

Two claims attributed to the July report stand out:

The offence-defence asymmetry in AI-enabled cyber operations is not theoretical: Palo Alto Networks’ internal AI scan compressed five to seven years of conventional vulnerability discovery into six weeks, a data point that illustrates precisely the capability expansion BlackRock attributes to state-backed actors in its reclassification rationale.

There is a verification gap worth naming directly. Publicly available BlackRock materials through May 2026, including the Geopolitical Risk Dashboard, list cyber and terrorism as discrete, separately rated categories. The research layer cannot independently confirm this merger in any publicly accessible dashboard. The July report may postdate the latest available materials, or the original source may be characterising BlackRock‘s directional framing rather than citing a formal taxonomic change.

BlackRock Thematic Investing Outlook 2026: Defence is evolving toward “digital, autonomous, and cyber capabilities” amid geopolitical fragmentation, with themes converging around “compute and conflict.”

If the reclassification holds on verification, it tells you that BlackRock‘s analytical framework now treats AI-enabled cyber attacks and terrorism as a single category of threat rather than two manageable separate risks. That distinction has direct implications for how defensively positioned a portfolio should be across data infrastructure and defence.

BlackRock‘s documented public position on U.S.-China competition has been measured. Ben Powell of the BlackRock Investment Institute has described the bilateral relationship as a “real and ongoing negotiation” with some characteristically “spiky episodes.” Full decoupling has been characterised as unlikely in the near term. The Geopolitical Risk Dashboard, updated May 2026, assigned U.S.-China strategic competition a Medium risk rating and framed China as the “axis” around which U.S. defence, trade, technology, energy, and security issues revolve.

The July report reportedly shifts that framing. The original source attributes to BlackRock a formal elevation of U.S.-China technology decoupling specifically (not the broader strategic competition) into a named high-priority risk tier. Separately, the report is said to forecast that AI will become a more prominent feature of U.S. political discourse ahead of the midterms, with questions around data centre build-out, energy demand, job displacement, and AI governance all drawing heightened attention.

The U.S.-China tech fault lines that BlackRock is reportedly elevating have a specific geopolitical anatomy: the May 2026 Beijing summit produced tariff and agricultural agreements but left Taiwan’s political status and AI chip export controls entirely unresolved, a structural gap that semiconductor investors tracking Nvidia, TSMC, and ASML exposure cannot price away through summit optimism.

| Risk dimension | May 2026 dashboard position | Reported July 11 position |

|---|---|---|

| U.S.-China strategic competition | Medium rating; structural backdrop | Tech decoupling elevated to high-priority tier |

| Cyber and terrorism | Separate categories, distinct ratings | Merged into single high-risk classification |

The BlackRock Geopolitical Risk Indicator (BGRI) measures market attention to each risk category, which means a formal tier change affects how allocation models weight the category in practice. Medium-rated structural risks typically inform long-horizon positioning: gradual hedging, slow rotation, patient rebalancing. Top-tier acute risks drive shorter-horizon defensive moves, the kind that produce visible capital flows within weeks rather than quarters.

If confirmed, the shift from a structural Medium-rated backdrop to a named high-priority risk tells you that BlackRock now views tech decoupling as capable of producing acute near-term market disruptions rather than just long-duration portfolio drag. That is a different investment problem entirely.

Setting the contested claims aside, BlackRock‘s confirmed published positions provide a solid analytical foundation. The 2026 Midyear Global Investment Outlook and related publications identify AI-led growth as the firm’s primary investment thesis. Defence is evolving toward digital and autonomous capabilities. Digital infrastructure is a major capital expenditure destination. And geopolitical chokepoints in critical technology supply chains are named explicitly as a risk factor.

BlackRock 2026 Midyear Outlook: Markets in 2026 are “shaped by AI, record capital expenditure and rising leverage.”

BlackRock is not offering blanket optimism on AI. The firm calls for careful selection among AI beneficiaries rather than broad-based exposure, flagging AI costs and capacity constraints as a counterweight to the growth thesis. That selectivity filter is as much a part of the signal as the growth thesis itself.

The confirmed analytical vocabulary BlackRock uses across its published work:

The analytical foundations for both the cyber-AI convergence argument and the technology decoupling elevation are present in BlackRock‘s published work, even where the formal taxonomy has not yet been updated. Even without the July claims being verified, the confirmed positions already point you toward the same sectoral conclusions: defence and cybersecurity as fragmentation beneficiaries, infrastructure as a capital expenditure magnet, and AI selectivity as the operative discipline.

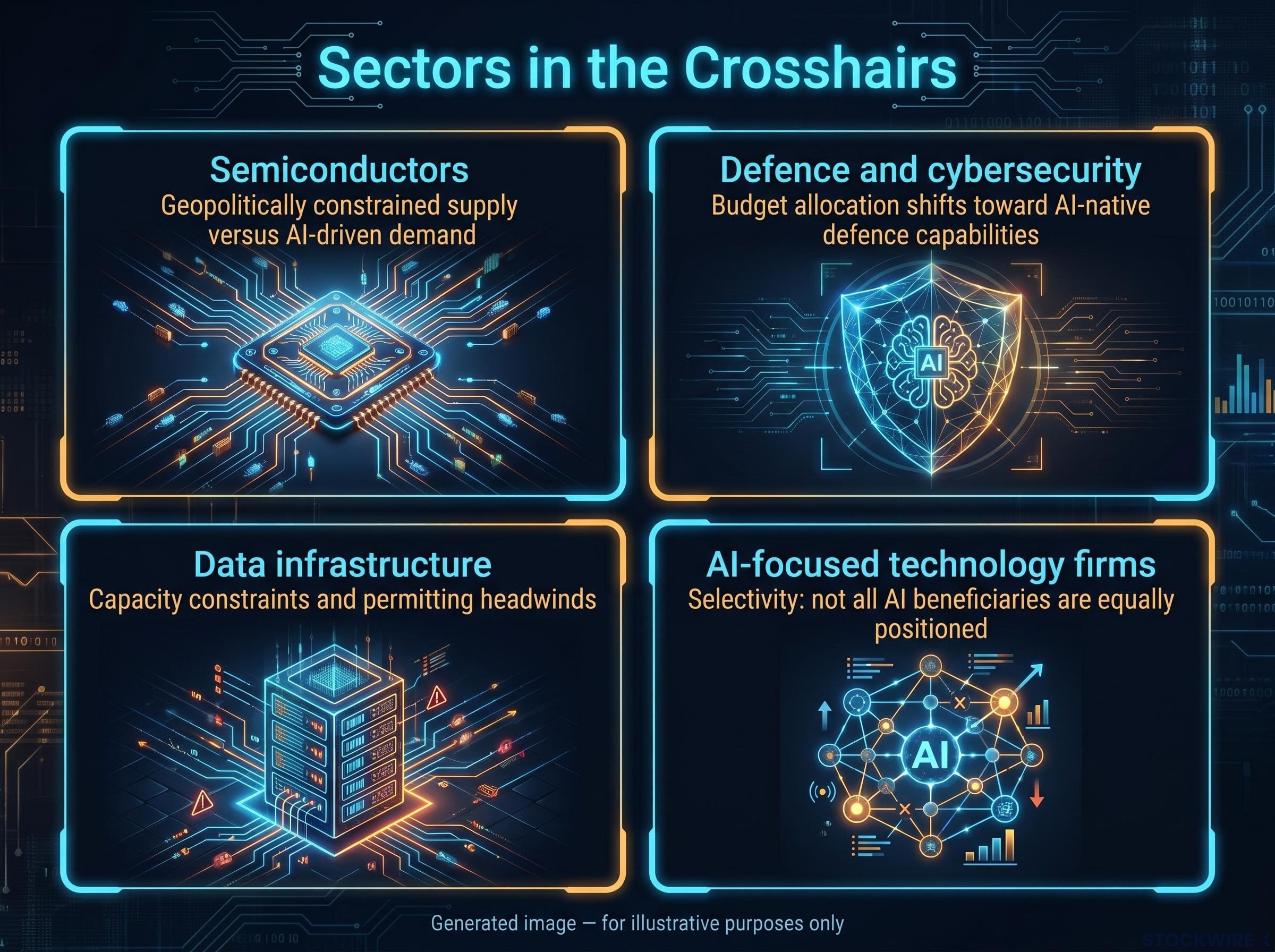

Four sectors sit at the intersection of BlackRock‘s confirmed AI thesis and the reported risk elevations. For each, the exposure logic draws on both documented positions and, where relevant, the July report’s framing.

| Sector | BlackRock confirmed position | Reported July 11 implication | Key risk to watch |

|---|---|---|---|

| Semiconductors | Export controls and industrial policy cited as volatility drivers; AI-driven chip demand central to growth thesis | Tech decoupling elevation sharpens supply-chain fragmentation risk | Geopolitically constrained supply versus AI-driven demand |

| Defence and cybersecurity | Explicitly named as fragmentation beneficiaries; “compute and conflict” convergence | Cyber-terrorism merger reinforces defensive positioning thesis | Budget allocation shifts toward AI-native defence capabilities |

| Data infrastructure | Primary AI enabler; major capital expenditure destination | Energy consumption and political scrutiny of data centres intensify | Capacity constraints and permitting headwinds |

| AI-focused technology firms | AI as central earnings driver; cost risk flagged as selective filter | Regulatory and geopolitical competition accelerate cost pressures | Selectivity: not all AI beneficiaries are equally positioned |

BlackRock‘s own published language calls for careful selection rather than blanket AI exposure, which means sector-level exposure within these categories is not uniform. For you, the practical implication of BlackRock‘s framing, both confirmed and reported, is that defence-adjacent cybersecurity and domestic semiconductor names carry a more defensible thesis than broad AI software exposure at current valuations.

For investors wanting to translate BlackRock’s semiconductor sector thesis into a concrete allocation framework, our deep-dive into semiconductor cycle positioning examines the five-indicator approach for capturing peak-cycle gains without holding premium multiples through the 2027-2029 supply wave.

The BGRI is a market-attention measure, not a directional trade signal. It tracks how much institutional focus each geopolitical risk category is receiving and feeds that attention data into allocation frameworks. A tier change tells you that a risk category is commanding more capital-allocation weight; it does not tell you which direction to trade.

How markets process geopolitical risk matters here: the BGRI is a market-attention measure, meaning a tier change affects capital allocation weight without being a directional trade signal, and historical evidence shows consensus predictions have consistently overestimated equity damage across recent escalation events.

The verification gap matters and should be addressed directly. The July report may represent a genuine taxonomy update, or it may be an interpretive characterisation of BlackRock‘s directional framing. The confirmation test is specific: watch for BlackRock‘s public Geopolitical Risk Dashboard to update. If cyber and terrorism appear as a merged category, and if U.S.-China tech decoupling carries a higher-than-Medium rating, the July claims are confirmed. Until then, they remain attributed but unverified.

Ben Powell, BlackRock Investment Institute: The U.S.-China relationship is a “real and ongoing negotiation” with some characteristically “spiky episodes.”

Regardless of whether the formal reclassification is confirmed, the structural forces driving both risk categories are already in motion and documented. AI-enabled offensive cyber capabilities are advancing. Technology supply-chain fragmentation is accelerating. The right posture is not to wait for dashboard confirmation before acting, but to recognise that BlackRock‘s confirmed analytical framework already points toward the same defensive and infrastructure-oriented positioning that the reported elevation would recommend.

Two parallel tracks run through this story. The first is BlackRock‘s confirmed AI and geopolitical fragmentation thesis, documented across its 2026 Midyear Outlook and Thematic Investing Outlook, pointing investors toward defence, cybersecurity, semiconductors, and digital infrastructure as sectors reshaped by structural forces already in motion. The second is the reported but unverified July reclassifications, which, if confirmed, would formally elevate those same forces from background structural risks to acute, top-tier allocation priorities.

The sectors most exposed are identifiable regardless of which track proves accurate. The structural forces are documented and directional. The formal taxonomy is pending verification. Watch for BlackRock‘s next public Geopolitical Risk Dashboard update as the definitive confirmation or correction of the July claims.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding BlackRock’s reported risk reclassifications are based on attributed sources and are subject to change based on market developments and official BlackRock publications.

The BlackRock Geopolitical Risk Indicator (BGRI) measures how much institutional attention each geopolitical risk category is receiving, feeding that data into allocation frameworks. A formal tier change signals that a risk category now commands greater capital-allocation weight, which can produce visible defensive capital flows within weeks rather than quarters.

BlackRock's reported rationale is that AI systems have materially expanded the offensive reach of state-sponsored actors to the point where cyber and terrorism threats converge at the highest severity levels, making them operationally indistinguishable as a risk class.

The reported upgrade shifts U.S.-China technology decoupling from a structural Medium-rated backdrop to a named high-priority risk, signalling that BlackRock now views it as capable of producing acute near-term market disruptions, with geopolitically constrained chip supply chains a specific pressure point for names like Nvidia, TSMC, and ASML.

BlackRock's confirmed published positions across its 2026 Midyear Outlook and Thematic Investing Outlook point toward defence and cybersecurity as fragmentation beneficiaries, semiconductors and digital infrastructure as capital expenditure destinations, and AI-focused technology firms as selective (not blanket) opportunities where cost and capacity constraints serve as a filter.

The confirmation test is specific: watch for BlackRock's public Geopolitical Risk Dashboard to update; if cyber and terrorism appear as a merged category and U.S.-China tech decoupling carries a rating above Medium, the July claims are confirmed. Until that dashboard update is published, the reclassifications remain attributed but unverified.