The Federal Reserve released the minutes from its April 28-29 meeting today, and the message is harder to misread than markets might prefer. The federal funds rate stays at 3.50-3.75%, but the committee is not settling into a holding pattern. With PCE inflation running at 3.5% year-over-year, oil prices sitting above $107 a barrel, and the Middle East conflict continuing to feed energy costs into the broader price environment, policymakers are explicitly keeping further rate hikes on the table. The minutes, released 20 May 2026, reveal a committee whose bias still leans toward tightening, not easing. What follows is a breakdown of what the April minutes actually signal for Federal Reserve interest rates, why geopolitical risk is now an active variable inside the Fed’s framework, and what specific conditions must change before rate cuts become a realistic prospect.

Fed holds rates steady but keeps the door open to further hikes

The Federal Open Market Committee (FOMC) voted unanimously to hold the federal funds rate at 3.50-3.75% at the conclusion of its April 28-29 meeting. On its face, the decision looks like stability. It is not.

The minutes, released on 20 May 2026, contain repeated references to “additional policy firming” as a likely next step if inflation fails to moderate. Most committee members assessed that further tightening remained warranted under current conditions, framing the hold as a deliberate pause for data collection rather than a signal that the tightening cycle is finished.

The April 28-29 meeting produced four FOMC dissents, the most at any single Federal Reserve meeting since 1992, a detail that sharpens the picture of internal disagreement the minutes only partially surface in their published language.

“Officials signaled they could raise rates again if inflation fails to ease, even as they kept borrowing costs unchanged.” — Bloomberg

Reuters separately reported that policymakers are “not yet ready to discuss rate cuts,” a characterisation that aligns with the minutes’ internal disposition. Economists described the release as “mildly hawkish,” stressing the committee is “not closing the door on further hikes” and that the bar for any easing remains high.

For investors interpreting a rate hold as evidence that tightening is over, the minutes present an uncomfortable correction. The committee’s bias still points upward if conditions deteriorate.

When big ASX news breaks, our subscribers know first

Why 3.5% inflation keeps the Fed’s finger near the trigger

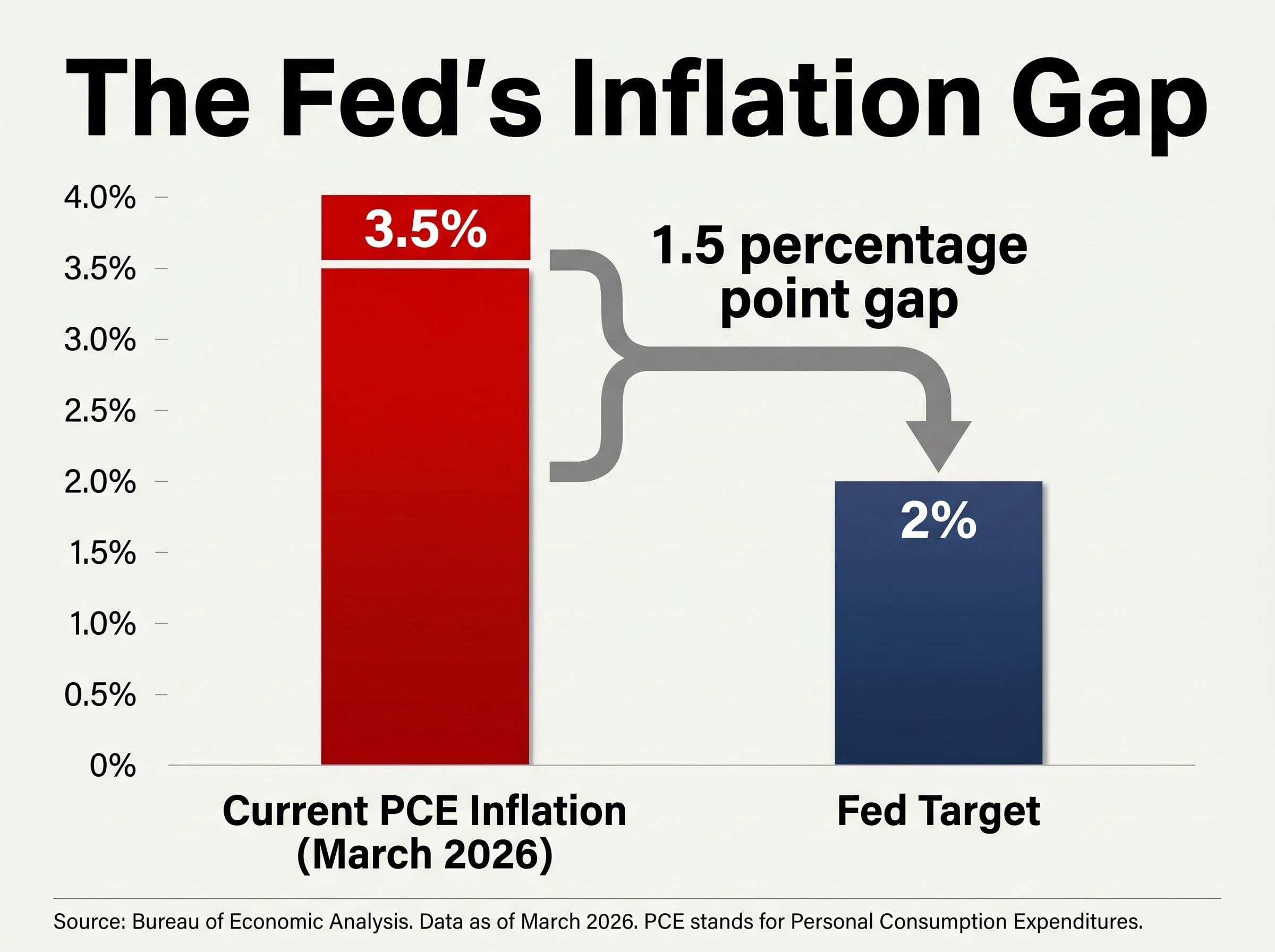

Fed Chair Jerome Powell put the inflation number on the record at the 29 April press conference: total PCE prices rose 3.5% over the twelve months ending in March 2026.

“Estimates based on the consumer price index and other data indicate that total PCE prices rose 3.5% over the 12 months ending in March, boosted by the significant rise in global oil prices that has resulted from the conflict in the Middle East.” — Chair Powell, 29 April 2026

That 3.5% figure sits 1.5 percentage points above the Fed’s 2% target, a gap wide enough that most committee members see conditions as nowhere near meeting the threshold for policy relaxation. The problem compounds when the headline number is broken apart.

- Total PCE inflation: 3.5% year-over-year (March 2026)

- Fed target: 2%

- Gap: 1.5 percentage points

- Core inflation status: Below 2022-2023 peaks, but still elevated and inconsistent with a near-term return to target

Even stripping out the volatile energy component, core inflation remains uncomfortably above the Fed’s comfort zone. Analyst consensus across major outlets frames core readings as having eased from their worst levels but not fast enough to give the committee confidence that the disinflationary trend will hold. At 3.5% headline PCE, the Fed has limited room to ease without risking its credibility on the 2% mandate.

How the Middle East conflict became a monetary policy problem

The Middle East conflict is no longer background noise in the Fed’s deliberations. It is an active variable inside the committee’s inflation calculus, with a direct transmission line from the conflict zone to American borrowing costs.

The mechanism runs through oil. Supply disruptions and risk premiums in producing regions have pushed crude prices well above pre-conflict levels. As of 20 May 2026, WTI crude trades at approximately $107.77 per barrel, with Brent crude ranging between $105 and $111 per barrel. Those prices feed directly into headline CPI and PCE through petrol, transport, and energy input costs.

The oil shock transmission from Gulf supply disruptions to US headline inflation is not a new channel, but the scale of the current disruption, with the IEA characterising it as the largest in recorded history, means the energy component is now carrying more weight in the PCE calculation than in any prior tightening cycle.

| Variable | Current level | Policy implication |

|---|---|---|

| WTI crude | ~$107.77/bbl | Upward pressure on headline inflation |

| Brent crude | ~$105-$111/bbl | Elevated; tied to Middle East supply risk |

| PCE inflation | 3.5% YoY | Well above 2% target |

| Fed funds rate | 3.50-3.75% | On hold; hike bias remains |

Several FOMC members cited upside inflation risks linked specifically to higher energy prices from the conflict, according to Reuters reporting on the minutes. The committee is watching whether energy-driven price increases bleed into wages and broader price-setting behaviour, which would shift the problem from a temporary supply shock to a structural inflation concern.

“In the near term, higher energy prices will push up overall inflation. Beyond that, the scope and duration of potential effects on the economy remain unclear, as does the future course of the conflict itself.” — Chair Powell, 29 April 2026

The geopolitical dimension means a portion of the inflation risk confronting the Fed sits outside its direct control. If the conflict escalates further, the committee may face pressure to tighten even without domestic economic overheating providing the justification.

What it would actually take for the Fed to start cutting rates

The minutes and recent Fed commentary identify two explicit conditions that must be met before rate cuts come into consideration:

- Sustained disinflation: Core PCE must be moving convincingly toward 2% on a sustained basis, not just one or two softer monthly prints.

- Meaningful labour market deterioration: Unemployment must rise materially, or job creation must slow enough to signal genuine slack building in the economy.

- A broader shift in the risk balance, where the cost of keeping policy too tight begins to outweigh the risk of inflation remaining elevated, would also factor into any pivot.

Bloomberg reported that rate cuts would only be considered appropriate “when there is greater confidence that inflation is moving sustainably toward 2% or if labor market conditions deteriorate materially.” The bar, according to economists quoted in the coverage, is “quite high.”

| Condition | Current status | Met? |

|---|---|---|

| PCE moving toward 2% | 3.5%, 1.5pp above target | No |

| Labour market deterioration | 4.3% unemployment, +115,000 payrolls | No |

| Risk balance shift | Committee sees inflation risk as dominant | No |

What the labour market numbers are telling the Fed

The April 2026 employment situation, released by the Bureau of Labor Statistics (BLS) on 8 May 2026, showed an unemployment rate of 4.3% and nonfarm payroll gains of +115,000. Those figures represent moderate softening but not the kind of deterioration the minutes describe as necessary.

The BLS Employment Situation Summary for April 2026, released on 8 May 2026, recorded nonfarm payroll gains of 115,000 and an unemployment rate of 4.3%, figures that confirm a labour market cooling gradually rather than deteriorating at the pace the Fed has described as necessary before easing becomes appropriate.

Payroll growth has slowed from the 200,000-plus monthly pace of prior years, yet it remains positive. The labour market is cooling without breaking. For a committee that is explicitly concerned about repeating a “stop-and-go” pattern of cutting prematurely, one or two softer prints will not be sufficient. The Fed needs sustained, convincing evidence across both inflation and employment before it moves.

Labour market deterioration signals are more mixed beneath the headline than the unemployment rate alone suggests: ISM Manufacturing and Services Employment indices both contracted in April, involuntary part-time employment surged by 445,000, and the three-month average of payroll gains sat at just 48,000 per month.

The next major ASX story will hit our subscribers first

Markets absorb a hawkish signal as rate-cut bets get pushed out

The market reaction to the minutes told the same story the text did, only faster.

- Equities: Modestly lower to flat following the release; rate-sensitive technology and growth sectors underperformed relative to defensive and value shares

- Two-year Treasury yields: Edged higher, reflecting increased probability assigned to another 25 basis point hike later in 2026

- Ten-year Treasury yields: Rose modestly, though less than the two-year, slightly steepening the front of the curve

- U.S. dollar: Strengthened against major currencies, with FX desks citing upside inflation risks and the high bar for cuts as supportive

Fed funds futures showed a modest uptick in the probability of another rate increase later in 2026, with rate-cut expectations pushed further out.

Reuters characterised the minutes as “pushing back against imminent rate-cut speculation.”

The mechanism behind the two-year yield move is direct: that maturity is most sensitive to near-term rate expectations, and the minutes made clear that the next move, if it comes, is more likely upward than downward. The market has absorbed a “higher for longer” message, not a pivot signal.

The Fed’s narrow path forward and what investors should watch next

Three overlapping pressures now define the Fed’s near-term path. Inflation remains 1.5 percentage points above target. Energy costs are tied to a geopolitical situation the committee cannot predict or control. The labour market is softening but not breaking.

| Variable | Current reading | Fed threshold | Gap |

|---|---|---|---|

| PCE inflation | 3.5% | Sustained move toward 2% | 1.5 percentage points |

| Unemployment | 4.3% | “Meaningful deterioration” | Not yet triggered |

| WTI crude | ~$107.77/bbl | Not specified | Elevated; upside inflation risk |

| Fed funds rate | 3.50-3.75% | On hold | Hike bias remains |

Economists at major banks have delayed their first-cut forecasts into late 2026, with several making those projections conditional on a more pronounced economic slowdown. The committee’s explicit concern about avoiding a “stop-and-go” pattern reinforces the view that any pivot will require overwhelming evidence, not marginal improvement.

Investors tracking the precise bank-by-bank timeline for potential easing will find our full explainer on Fed rate cut forecasts for 2026-2027, which covers Goldman Sachs and Bank of America’s revised projections, the core PCE trajectory assumptions behind each forecast, and the specific labour market thresholds that would need to be breached before cuts re-enter the conversation.

The three data releases that will determine whether the next move is a hike or an eventual cut:

- Monthly PCE readings: The most direct measure of progress toward the Fed’s 2% target

- Monthly employment situation (BLS): The labour market signal the committee says it needs before easing becomes appropriate

- Oil prices and Middle East developments: The variable the Fed cannot model but must monitor, given its direct pass-through to headline inflation

The structural tension is now fully visible. The Fed wants to avoid premature easing that risks re-accelerating prices. It also wants to avoid excessive tightening that pushes the economy into an unnecessary recession. Today’s minutes confirm the committee believes it has not yet reached the point where either pivot is warranted.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.