Nvidia just posted $81.62 billion in quarterly revenue, a record, and then guided the next quarter to $91 billion, a figure Wall Street had not priced in. The results landed after markets closed on 20 May 2026 and confirm that demand for the company’s AI infrastructure hardware continues to accelerate despite elevated macro headwinds including rising rates and geopolitical pressure on equity markets. What follows breaks down what the headline numbers actually mean, what the $80 billion buyback and 25x dividend increase signal about management’s confidence, and what the forward guidance implies for investors tracking AI infrastructure spending.

Nvidia’s Q1 numbers in full: what beat, and by how much

Wall Street expected a strong quarter. It got a stronger one.

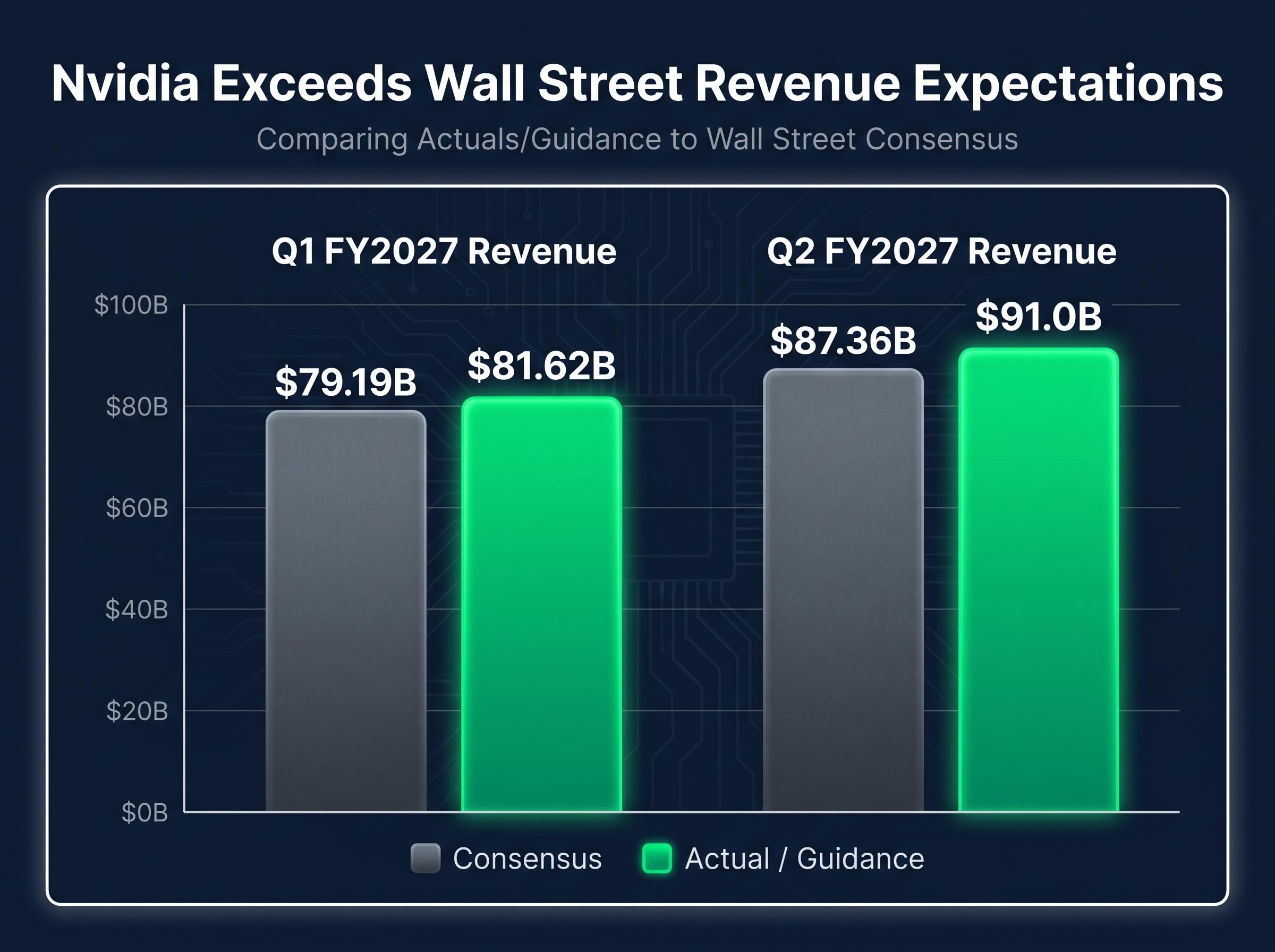

Nvidia reported $81.62 billion in Q1 FY2027 revenue against an analyst consensus estimate of $79.19 billion, a beat of more than $2.4 billion.

The gap extended beyond the top line. Non-GAAP earnings per share came in at $1.87 versus the $1.77 consensus, while GAAP EPS reached $2.39. The beat covered both metrics simultaneously, giving analysts a firmer foundation for upward revisions.

Gross margin sustainability near 75% was the highest-priority signal Bank of America analyst Vivek Arya identified heading into the print, with HBM supply constraints from SK Hynix, Samsung, and Micron framed as a structural cost headwind that headline revenue beats alone could not offset.

- Revenue: $81.62 billion (up 85% year-over-year, up 20% quarter-over-quarter)

- Non-GAAP EPS: $1.87 vs. $1.77 consensus

- GAAP EPS: $2.39

- YoY revenue growth: 85%

The after-hours share reaction told its own story. Nvidia shares dipped approximately 0.3% following the release, a reminder that a beat alone, when expectations are already stretched, does not guarantee an immediate price pop. The market had priced in strength; it got more strength, and still paused.

When big ASX news breaks, our subscribers know first

Data centre is not a segment, it is almost the entire company

Three years ago, Nvidia sold gaming GPUs, professional visualisation hardware, and automotive chips alongside its data centre business. That company no longer exists in any meaningful financial sense.

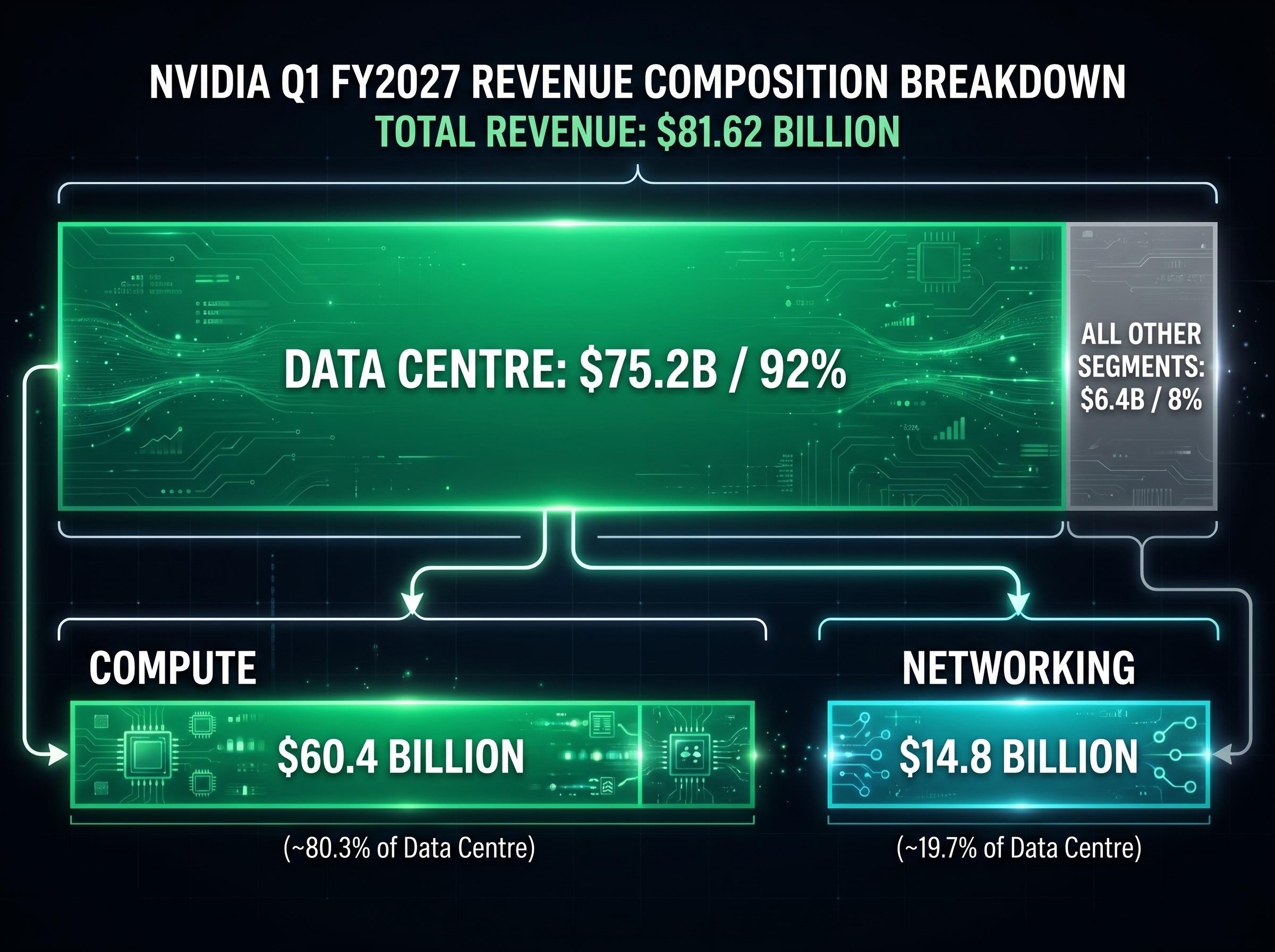

Data centre revenue reached $75.2 billion in Q1 FY2027, representing approximately 92% of total quarterly revenue. The remaining segments, gaming, professional visualisation, automotive, and edge computing, contributed roughly $6.4 billion combined. The concentration is not a trend; it is a structural reality.

| Segment | Q1 FY2027 Revenue | Share of Total | YoY Growth |

|---|---|---|---|

| Data Centre | $75.2B | ~92% | +92% |

| All Other Segments | ~$6.4B | ~8% | — |

Data centre revenue also grew 21% quarter-over-quarter, indicating that the trajectory is accelerating rather than plateauing.

Inside the data centre number: compute vs. networking

The $75.2 billion splits into two components that tell different but complementary stories. Compute revenue, primarily GPU procurement for AI training and inference workloads, reached $60.4 billion. Networking revenue, covering interconnect and switch infrastructure, hit $14.8 billion.

The networking figure is significant on its own. At $14.8 billion in a single quarter, Nvidia’s networking business alone would rank as a substantial standalone technology revenue line. Its scale signals that hyperscalers are building out full-stack AI infrastructure, not simply adding GPUs in isolation but wiring together the fabric those GPUs require to operate at scale.

What AI is and why Nvidia sits at its centre

The revenue figures above are driven by a single structural fact: artificial intelligence workloads require a type of computing power that conventional processors cannot deliver efficiently. AI models, the software systems behind tools like chatbots, image generators, and autonomous systems, must be trained on enormous datasets and then run continuously to produce outputs. Both training and running these models (a process called inference) demand parallel processing at a scale that only graphics processing units (GPUs) can provide cost-effectively.

Nvidia designs and supplies those GPUs. Its current Blackwell-generation hardware sits at the centre of virtually every major AI deployment globally, and the company’s CUDA software platform has become the standard development environment for AI engineers. CEO Jensen Huang has framed the current moment in direct terms.

Jensen Huang has characterised the current AI infrastructure buildout as the largest in human history, with Nvidia positioned as the sole platform deployed across all major cloud environments.

The primary buyers are the four largest cloud infrastructure operators:

Hyperscaler capex commitments reaching $725 billion for 2026, with a $1 trillion annual run rate projected for 2027, form the demand architecture that makes Nvidia’s order book visibility possible; Amazon, Microsoft, Alphabet, and Meta each entered Q1 2026 with board-approved spending programmes that had already locked in GPU procurement timelines.

- Microsoft: Azure AI infrastructure built on successive generations of Nvidia GPU instances

- Amazon: AWS GPU-based compute instances powering AI workloads at scale

- Google: Cloud AI infrastructure running alongside Google’s own TPU hardware

- Meta: Large-scale AI infrastructure investment with significant Nvidia GPU deployments

Over approximately three years through May 2026, Nvidia’s market capitalisation grew to exceed $5 trillion, reflecting investor conviction that this hardware demand is structural rather than cyclical.

The $80 billion buyback and 25x dividend hike are not routine announcements

Capital return programmes at technology companies are common. The scale of what Nvidia announced alongside Q1 results is not.

Nvidia raised its quarterly dividend from $0.01 per share to $0.25 per share, a 2,400% increase.

- Dividend increase: $0.01 to $0.25 per share (a 25x or 2,400% increase)

- Buyback authorisation: $80 billion additional, one of the largest in the company’s history

The arithmetic of the dividend matters. Moving from a token payout to $0.25 per share quarterly does not transform Nvidia into a yield stock, but it sends a specific signal: management believes the company’s cash generation is durable enough to support a meaningful, recurring shareholder commitment rather than a symbolic one.

A capital return policy shift had been the mechanism Bank of America analysts argued could close the valuation gap between Nvidia’s approximately 24.5x forward earnings and the Magnificent Seven peer average of 49x, with a dividend yield of 0.5%-1.0% identified as the level needed to bring income fund mandates into the buyer base.

The $80 billion buyback authorisation reinforces that signal. A programme of that magnitude requires management confidence in both the stock’s intrinsic value at current levels and the company’s capacity to generate the free cash flow necessary to fund it. Together, these announcements position Nvidia as a company that has matured financially even as its revenue growth rate remains at levels typically associated with early-stage businesses.

The Q2 guidance of $91 billion is the number that matters most

For a company growing at this rate, last quarter’s results are already priced. The forward view carries more weight.

Nvidia guided Q2 FY2027 revenue to $91.0 billion (plus or minus 2%). The analyst consensus heading into the print sat at approximately $87.36 billion, making the guidance beat worth more than $3.5 billion above expectations.

| Metric | Q1 FY2027 Actual | Q2 FY2027 Guidance | Q2 Analyst Consensus |

|---|---|---|---|

| Revenue | $81.62B | $91.0B (±2%) | ~$87.36B |

The implied sequential growth from Q1 to Q2 is approximately 11.5%, a rate that, if sustained, would place Nvidia on an annualised revenue trajectory well above $350 billion. Three forward-looking implications stand out:

- Guidance beat magnitude: Exceeding consensus by more than $3.5 billion on a $91 billion base signals that Nvidia’s order book visibility is strong enough for management to set a high bar publicly.

- Sequential growth rate: An 11.5% quarter-over-quarter increase indicates the acceleration has not peaked.

- Platform roadmap visibility: Blackwell-generation hardware is driving current deployments, with the Rubin architecture on the horizon, giving management a supply-side basis for sustained confidence.

The next major ASX story will hit our subscribers first

A record quarter in a market running hot on AI: what investors should weigh now

The Q1 FY2027 print delivered on every measurable front. Revenue and EPS beat consensus. The capital return programme signalled financial maturity. Forward guidance implied the growth rate is still rising. Taken together, the report positions Nvidia as the clearest single-stock proxy for global AI infrastructure spending as of today, 20 May 2026.

That positioning sits within a broader context. The Philadelphia Semiconductor Index posted an 18-consecutive-session winning streak from late March through late April 2026, the longest in the index’s history, reflecting a sector-wide repricing of AI exposure. Rising rate expectations, the Washington-Iran geopolitical situation, and a concurrent global bond selloff have all exerted pressure on equities during the same period.

Three variables that could shift the outlook from here

- Hyperscaler capex durability: Whether Microsoft, Amazon, Google, and Meta sustain or moderate GPU procurement commitments through their upcoming earnings cycles

- Competitive displacement risk: Custom silicon programmes (Amazon Trainium, Google TPU, Meta custom accelerators) could reduce reliance on Nvidia hardware over time

- Macro rate trajectory: Higher-for-longer interest rate environments historically compress multiples on stocks whose valuations depend on future earnings growth

The capex-to-revenue lag, estimated at 18-24 months by Morningstar analyst Dennis Li, is the structural tension sitting behind every hyperscaler GPU procurement commitment: the spending is real, the infrastructure is being built, but only 20% of current AI agent pilots are projected to scale to production by 2027, which means the revenue justification for sustained hardware orders remains partially prospective.

The approximately 0.3% after-hours decline serves as a useful reminder. Record results priced into record expectations do not automatically produce immediate share price appreciation.

Nvidia’s numbers just redefined what a record quarter looks like

Three signals define this print: a revenue and EPS beat that exceeded an already-elevated consensus, a capital return programme large enough to reposition the stock for income-oriented and value-oriented investors, and Q2 guidance of $91 billion that suggests the acceleration has further to run. The muted after-hours reaction underscores a reality that will persist: at these valuations, exceptional results must continually exceed elevated expectations to move the share price.

The $91 billion guidance figure is now the benchmark. All attention shifts to whether Nvidia can deliver a third consecutive record quarter. Investors tracking AI infrastructure investment should monitor hyperscaler earnings calls in the coming weeks for confirmation of sustained GPU procurement commitments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including revenue guidance and growth projections, are subject to change based on market developments and company performance.