RBA Holds Cash Rate at 4.35% After Three Straight Hikes

1 hr ago

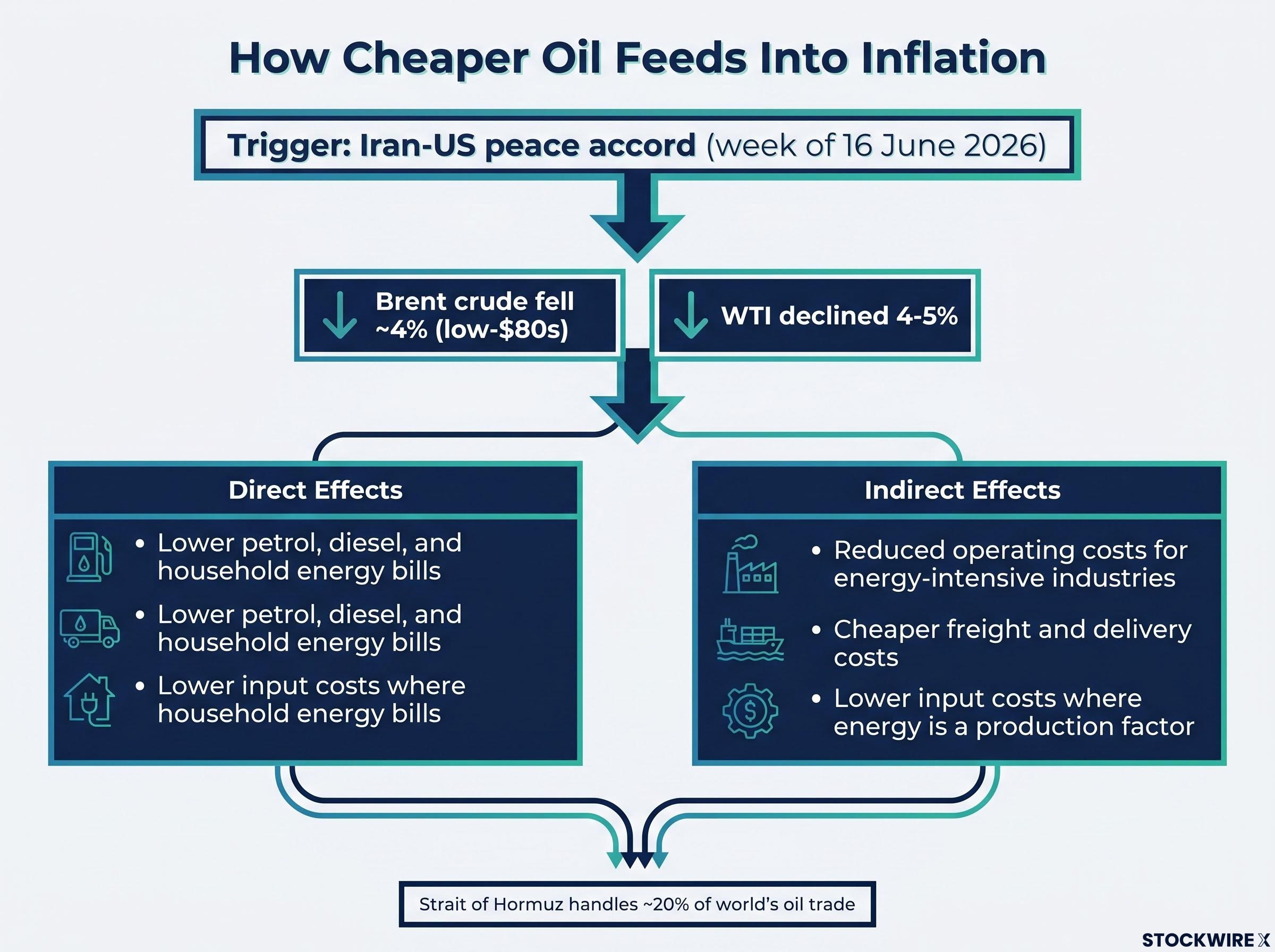

The Strait of Hormuz, the narrow waterway that handles roughly one-fifth of the world’s oil trade, is reopening. A prospective Iran-US peace accord announced this week sent financial markets into a swift repricing, with Brent crude falling approximately 4% to its lowest level in about three months. The development lands as Australian households continue to absorb elevated cost-of-living pressures and the Reserve Bank of Australia (RBA) has just held rates steady at its June 2026 meeting. For borrowers, investors, and policymakers, the question is whether falling oil prices translate into genuine inflation relief, or whether the picture is more complicated than the headline move in crude suggests. What follows explains how the Strait of Hormuz reopening feeds into fuel and energy costs, why central banks including the RBA will not treat cheaper oil as a settled verdict on inflation, and what specific signals to watch in coming weeks.

The Strait of Hormuz is a narrow passage between Iran and Oman through which approximately 20% of the world’s oil trade passes. When the Iran-US conflict escalated in late February 2026, restrictions on shipping through the strait effectively choked one of the global economy’s most consequential supply arteries, contributing directly to elevated energy costs in the months that followed.

The EIA oil chokepoint data confirms that in 2024, roughly 20 million barrels per day moved through the strait, equivalent to approximately 20% of global petroleum liquids consumption, making any sustained closure one of the most consequential supply disruptions the energy market can absorb.

The peace accord announcement, reported during the week of 16 June 2026, prompted an immediate repricing across energy markets.

The scale of the repricing that followed the peace accord is only fully appreciable against the baseline: the oil price surge from the Hormuz closure had sent Brent from approximately $70 per barrel in late February 2026 to above $110 by mid-May, a 57% move driven almost entirely by the effective removal of roughly 20% of global seaborne supply.

Brent crude fell approximately 4% to the low-$80s per barrel, its lowest level in roughly three months. WTI declined by an estimated 4-5%.

The scale of the move reflects how severely the closure had distorted global supply expectations. Three immediate consequences followed the reopening news:

Whether the physical reopening delivers the supply increase markets are pricing in remains an open question. Oil supply data in the weeks ahead will provide the first empirical test.

Lower crude reduces the cost of petrol, diesel, and household energy. Because fuel and energy carry a visible weight in the Australian consumer price basket, this relief pulls headline Consumer Price Index (CPI) lower in a relatively measurable and rapid way. Transport and energy costs had been feeding through to broader prices in the months preceding the agreement, so even a partial reversal is meaningful.

Energy is an input cost across transport, logistics, manufacturing, agriculture, and food processing. As crude falls, firms’ cost bases ease, and that relief can gradually filter through to a wider set of goods and services prices over subsequent months. The word “gradually” matters. These indirect channels operate with a lag, and their magnitude depends on whether lower crude is sustained rather than a brief relief event.

The lag between a crude price drop and its appearance across the full consumer price basket reflects the two distinct direct and indirect transmission channels: the direct channel hits petrol and energy bills within weeks, while the indirect channel through logistics, agriculture, and manufacturing supply chains operates on a 6-12 month lag and may still be building even as the headline number eases.

| Channel | Direct Effects | Indirect Effects |

|---|---|---|

| Fuel and energy | Lower petrol, diesel, and household energy bills | Reduced operating costs for energy-intensive industries |

| Transport and logistics | Cheaper freight and delivery costs | Slower-rising prices for goods reliant on long supply chains |

| Manufactured goods | Lower input costs where energy is a production factor | Gradual easing of cost pressures in food processing and agriculture |

The distinction between headline CPI and core inflation is where the story gets complicated. Core inflation strips out food and energy precisely because they are volatile and often driven by external shocks. Even after removing energy, underlying price pressures in Australia have remained elevated.

The assumption is intuitive: cheaper oil means lower prices, which should mean rate cuts. Central banks do not follow that logic mechanically, and the reason is worth understanding.

The RBA targets inflation of 2-3% on average over time, focusing on underlying measures such as the trimmed mean, which filters out the most volatile price movements in either direction. This is the measure that drives rate decisions, not headline CPI.

The RBA inflation targeting framework specifies a 2-3% average target over time and designates the trimmed mean as the preferred underlying measure precisely because it strips out volatile price movements, including those driven by energy supply shocks of the kind the Strait of Hormuz reopening represents.

Historically, the RBA and peer central banks have tended to “look through” supply-side energy shocks that are clearly geopolitical in origin. A conflict closes a shipping lane, oil spikes, and then a peace deal reopens it; the price swing in both directions is treated as temporary noise rather than a signal about domestic economic conditions.

What the RBA and other central banks monitor instead is whether underlying domestic cost pressures are genuinely moderating. The US CPI for May 2026 illustrated the point: the annual rate came in at approximately 4.2%, the highest in three years, with higher transportation and energy costs feeding through to broader prices. Even stripping out energy, core measures still showed a modest monthly increase. Markets had already assumed the Federal Reserve would hold rates steady at its upcoming meeting.

The Iran-US peace deal is disinflationary, meaning it removes upside risk to inflation. It is not deflationary, meaning it does not on its own guarantee that prices fall broadly. That distinction shapes how quickly (or slowly) rate cuts arrive.

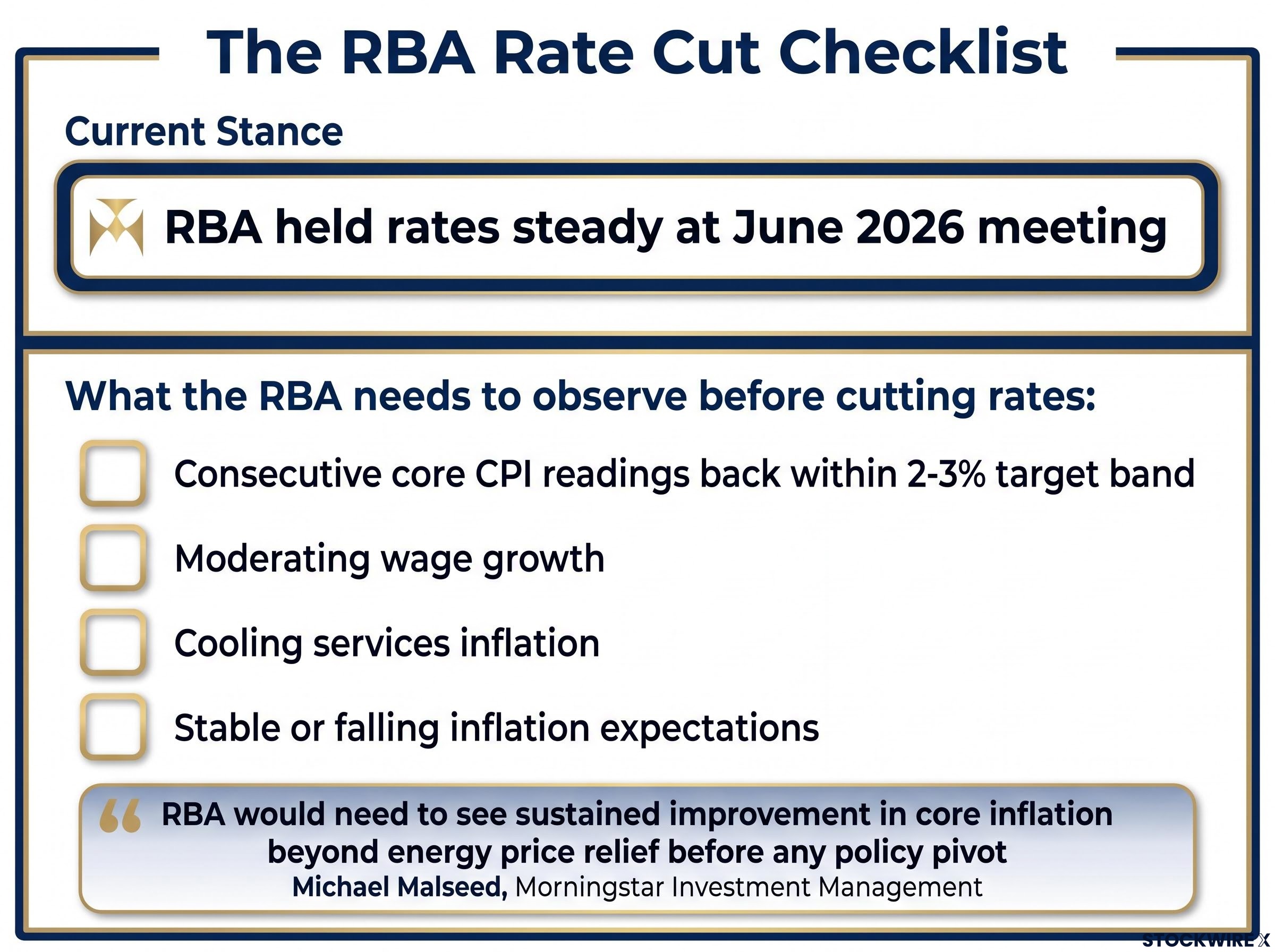

Before considering rate cuts, the RBA would need to observe:

The RBA held the cash rate unchanged at its June 2026 meeting, adopting a data-dependent stance rather than signalling immediate further tightening. The peace deal and falling oil prices arrived in that same week, creating a backdrop that is more favourable than what the board faced when it set the agenda.

The backdrop to the June 2026 hold decision is a period of pronounced global central bank divergence, in which the RBA hiked to 4.35% on 5 May while the Fed, ECB, and Bank of England all held, creating a spread of up to 235 basis points and signalling that Australian inflation was treated as a more acute domestic problem than the energy shock alone could explain.

Lower crude reduces the probability of additional rate hikes by easing headline inflation risk. It does not remove the possibility of further increases in the second half of 2026 entirely.

Michael Malseed, Head of Institutional Portfolio Management at Morningstar Investment Management, observed that the RBA would need to see sustained improvement in core inflation beyond energy price relief before any policy pivot, as reported in Morningstar Australia’s Market Minute during the week of 16 June 2026.

For Australian borrowers, the practical translation is:

The gap between those two columns is where the next several months of monetary policy will be decided.

Three categories of data will determine whether this geopolitical development translates into tangible rate relief. They are listed in the order they are likely to arrive:

Readers who track these three signals are positioned to interpret upcoming news with context rather than reacting to individual data points in isolation.

The Iran-US peace accord and the resulting fall in crude prices are a genuine and meaningful disinflationary development. They buy central banks time, reduce the probability of further hikes, and ease one of the most visible cost pressures Australian households have faced in recent months.

They are not, on their own, sufficient to trigger rate cuts. The months ahead will be shaped by whether lower energy costs filter through into core inflation, wages, and services prices. The RBA and its peers are watching for cumulative evidence across several quarters, not acting on a single week’s price move.

For Australian borrowers, the primary near-term benefit is reduced risk of additional mortgage rate increases. Genuine rate relief remains conditional on the broader disinflation story holding across the measures central banks actually weight in their decisions.

For investors who want to act on the possibility that the disinflation story eventually delivers a policy pivot, our dedicated guide to positioning your ASX portfolio ahead of rate cuts examines which ASX sectors have historically moved first when the RBA eases, covers how REITs, infrastructure, and high-growth technology stocks respond to confirmed versus anticipated cuts, and explains why bank stocks are a more complicated play than they appear in a falling-rate environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking statements regarding rate paths and inflation trends are subject to change based on market developments and economic data.

Falling oil prices reduce petrol, diesel, and household energy costs directly, pulling headline CPI lower within weeks. Indirect relief across transport, food, and manufacturing follows on a 6-12 month lag and depends on whether lower crude prices are sustained.

The Strait of Hormuz handles roughly 20% of global oil trade, and its effective closure since late February 2026 had pushed Brent from around $70 to above $110 per barrel. The Iran-US peace accord announced in the week of 16 June 2026 restored supply expectations, sending Brent down approximately 4% to the low-$80s.

The RBA requires consecutive core CPI readings trending back within its 2-3% target band, moderating wage growth, cooling services inflation, and stable or falling inflation expectations before considering a rate cut, as cheaper oil alone does not confirm sustained domestic disinflation.

Headline CPI includes all consumer prices including volatile food and energy costs, while core inflation measures such as the trimmed mean strip out those volatile components. The RBA focuses on core measures because they better reflect persistent domestic price pressures rather than temporary external shocks like oil price swings.

Investors should monitor tanker traffic and Gulf producer output data for confirmation of physical supply restoration, Australian and global CPI releases to see if fuel relief flows through to core components, and RBA and Fed communications for language shifts signalling reduced inflation risk.