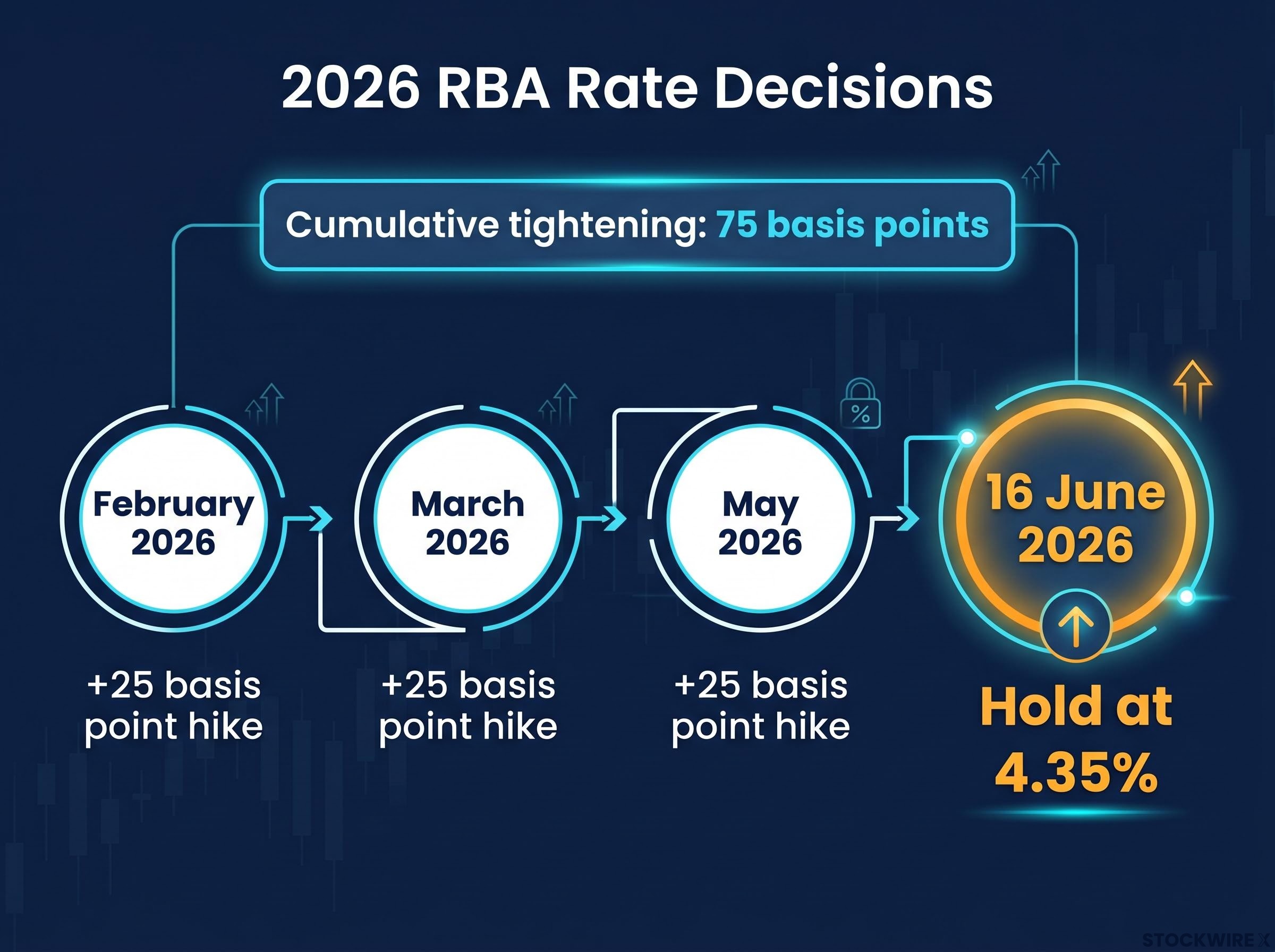

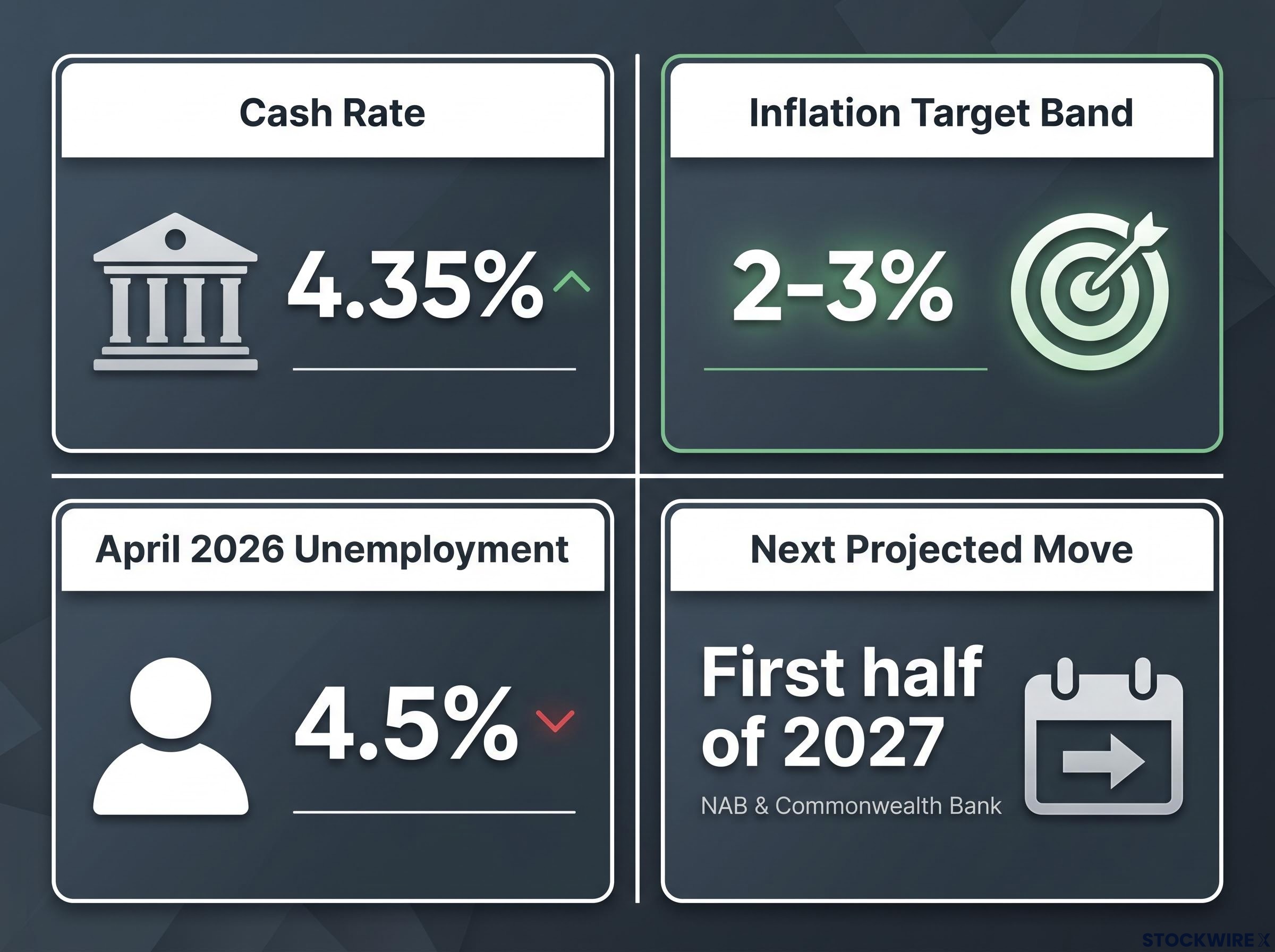

The Reserve Bank of Australia held its cash rate at 4.35% on 16 June 2026, halting a three-hike tightening cycle that added 75 basis points to borrowing costs since February. The decision was unanimous. The Board’s statement, however, was unusually brief, and what it left unsaid may matter more than the hold itself.

With inflation still above the 2-3% target band, household consumption softening, and unemployment jumping unexpectedly to 4.5% in April, the RBA is walking a narrowing line between finishing the inflation fight and letting the economy slow too far, too fast. NAB Group Economics sees no rate relief until at least the first half of 2027. For investors, the question is no longer whether rates stay high. It is whether the economy can absorb this level of restriction without a sharper deterioration than policymakers are publicly acknowledging.

RBA pauses at 4.35% after three straight hikes

The Monetary Policy Board voted without dissent to hold the cash rate at 4.35%, effective 17 June 2026. The decision marks the first pause after three consecutive increases this year:

The June hold sits within a broader context of global central bank divergence, with the Fed, ECB, and Bank of England all holding rates steady through the same period while the RBA completed three consecutive hikes, creating a rate differential of up to 235 basis points that has direct implications for the AUD and for Australian asset valuations relative to offshore alternatives.

- February 2026: 25 basis point hike

- March 2026: 25 basis point hike

- May 2026: 25 basis point hike

- Cumulative tightening: 75 basis points

ASX 30-day interbank futures, as at 15 June 2026, implied a 4.35% rate for the June contract, with virtually no probability of further hikes or meaningful easing priced for the remainder of 2026.

The Board chose not to characterise the overall stance of monetary policy directly, pointing instead to tighter financial conditions and an economy decelerating in line with projections. The brevity of the statement itself stood out. There was no explicit language closing the door on further tightening, a deliberate omission that preserves the Board’s optionality heading into the second half of the year.

NAB Group Economics anticipates no change to the cash rate for the remaining quarters of 2026, with the next rate movement projected to be a reduction in the first half of 2027.

Sally Auld, Chief Economist, NAB Group Economics, 16 June 2026

When big ASX news breaks, our subscribers know first

Why inflation is still running the show at the RBA

The hold confirms what the Board’s language has signalled for months: inflation remains the dominant constraint on policy. The Board’s explicit priority is preventing inflationary pressures, particularly those stemming from elevated oil prices, from becoming embedded in wages and price-setting behaviour.

The RBA’s June 2026 monetary policy decision confirms the Board’s explicit focus on preventing elevated oil prices from embedding into wages and broader price-setting behaviour, a concern that underpins the inflation-first stance reflected in the June statement’s deliberately measured language.

Certain measures of inflation expectations have recently moderated, which is a positive signal. It has not, however, been sufficient to shift the RBA’s stance. NAB views it as premature to anticipate any move toward a more accommodative tone while inflation sits above the target band. Commonwealth Bank economists have reached a similar conclusion, projecting the next move as a cut in the first half of 2027 with a very low likelihood of further hikes.

The primary risk for fixed income and duration positioning through the remainder of 2026 is an upside surprise in core inflation (trimmed mean CPI) during the H2 releases. A renewed acceleration in core measures would re-open the door to a further hike, pushing yields higher before they fall.

For investors managing bond duration or considering term deposits, the inflation constraint defines the floor under yields for the rest of this year. Until the CPI data confirms sustained moderation, the rate plateau holds.

What the RBA did not say, and why it matters

The June statement contained two conspicuous silences. Both carry weight for investors trying to read the Board’s assessment of where the economy actually stands.

- Capacity utilisation: NAB Group Economics identified one of the steepest six-month declines in this measure in roughly 15 years outside of pandemic conditions. The Board did not reference it.

- Housing market implications: The statement acknowledged a shift in housing market momentum but did not detail its broader economic consequences.

The capacity utilisation omission caught NAB off guard. The RBA has historically relied on this indicator to assess output gap dynamics, the degree to which the economy is operating above or below its potential. A sharp fall in capacity utilisation typically signals that businesses are pulling back, that demand is weakening faster than headline GDP figures suggest.

NAB’s interpretation is direct: the omission may signal the economy is slowing more sharply than official projections acknowledge. If that reading proves correct, it has implications for the earnings and growth outlooks investors are currently pricing.

Per capita output contraction has been running alongside positive headline GDP growth for over a year, with corporate insolvencies reaching their highest level since the 1990-91 recession and real wages declining as CPI outpaced wage growth, conditions that help explain why the RBA’s capacity utilisation data has recorded one of the steepest six-month declines in 15 years even as aggregate output numbers appear relatively stable.

NAB anticipates the August 2026 RBA Statement on Monetary Policy will provide a more thorough assessment of both capacity utilisation and housing conditions.

The unemployment surprise adds another layer of uncertainty

The unemployment rate rose unexpectedly to 4.5% in April 2026, though other labour market indicators remained resilient. NAB projects a decline when May figures are released on 25 June 2026.

The binary outcome matters. If unemployment holds at 4.5% or climbs, NAB would view this as a material signal toward a more dovish policy direction and potentially earlier-than-2027 cuts. If the April reading proves temporary, the Board retains room to stay patient.

What “higher for longer” means across your portfolio

The macro picture translates differently across asset classes, and the implications are not symmetrical.

Fixed income offers the clearest tactical opportunity in a peak-rate environment. If NAB’s baseline holds and the first cut arrives in the first half of 2027, today’s 2-5 year government bond yields could look attractive in retrospect. A measured duration tilt, rather than maximum duration, is appropriate given the residual hike risk the Board has preserved. Floating-rate and inflation-linked exposure remain relevant hedges while the RBA’s inflation-first stance persists.

Equities require sector differentiation. Domestic demand-sensitive names face ongoing pressure as household consumption softens. Quality, cash-generative businesses with pricing power are better positioned if growth slows but inflation stays sticky. Financials benefit from higher-for-longer net interest margins but face rising credit risk if unemployment continues to drift upward. Growth stocks face capped multiple expansion under sustained high real rates, making earnings delivery the variable that separates winners from losers.

The stagflation risk framework, combining above-target inflation with rising unemployment and slowing growth, has become the lens through which institutional economists including AMP and Westpac are interpreting the current data, and it maps directly onto the policy trap the RBA is navigating: cutting rates to support employment risks entrenching the same inflationary pressures that three consecutive hikes have not yet fully suppressed.

Property investors should plan for no meaningful rate relief until 2027. Mortgage rates stay elevated, cash flows remain stretched for leveraged investors, and the RBA’s acknowledgement of shifting housing momentum suggests further pressure may be building beneath the surface.

Cash and term deposits at 4.35% offer attractive yields by the standards of the past decade. Locking in 12-24 month terms is sensible for capital-preservation allocations, but an all-cash stance risks reinvestment risk once the easing cycle begins.

For investors who want to move beyond the asset class summary and build a specific portfolio response to the current rate environment, our comprehensive walkthrough of ASX inflation investment strategies covers six ASX-listed ETFs spanning capital preservation, bond income, and quality equity exposure, with dollar cost averaging frameworks and portfolio tilt guidance calibrated to the inflation and rate conditions that have persisted through 2026.

| Investor Type | Core Strategy |

|---|---|

| Income-focused | Secure medium-term bond and term deposit yields; moderate duration tilt with inflation protection |

| Growth-oriented | Prioritise quality equities with pricing power; remain conservative on cyclicals and leveraged names |

| Property investor | Stress-test cash flows at or above current rates through 2027; focus on structural rental demand |

| Tactical trader | Watch 25 June labour data, H2 CPI releases, and the August RBA statement as primary catalysts |

Understanding the RBA’s rate-setting framework

The cash rate is the interest rate on overnight loans between banks, and it is the RBA’s primary tool for influencing borrowing costs across the Australian economy. When the Monetary Policy Board raises the cash rate, the increase flows through to mortgage rates, business loan rates, and deposit rates, tightening financial conditions and slowing demand. When it cuts, the reverse occurs.

The Board operates under a dual mandate: maintaining price stability (targeting inflation within the 2-3% band) while supporting full employment and economic prosperity. The June 2026 decision illustrates the tension between these objectives. Inflation remains above target, which argues for maintaining restriction. Unemployment has risen to 4.5%, which argues for caution.

A unanimous hold after three hikes signals the Board believes the current rate level is doing sufficient work to bring inflation down. The open door on further tightening reflects genuine uncertainty about whether that work is complete.

The cash rate affects investors through three primary channels:

- Borrowing costs: Higher rates increase mortgage repayments and business financing expenses, reducing disposable income and corporate margins

- Asset valuations: Higher discount rates compress the present value of future cash flows, weighing on equity and property valuations

- Currency competitiveness: Rate differentials influence AUD strength, affecting export earnings and international purchasing power

The Board’s language choices after each meeting, what it says and what it omits, function as forward guidance. Investors who understand these signals can position proactively rather than reacting after the market has already moved.

Three dates that will shape the rate outlook before year-end

The macro complexity of the preceding sections distils into three concrete calendar events. Each carries the potential to shift the rate path and force portfolio adjustments.

- 25 June 2026: May labour force data (ABS). April unemployment hit 4.5%. NAB projects a decline in May, but if unemployment holds or rises, it would represent a material dovish signal with implications for the timing of rate cuts.

- H2 2026: CPI and trimmed mean releases. These are the inflation test. Renewed acceleration in core inflation re-opens the hike door. Continued moderation strengthens the 2027 cut baseline.

- August 2026: RBA Statement on Monetary Policy. NAB views this as the forum where the Board will address the capacity utilisation decline, housing momentum shift, and updated growth and inflation forecasts that were absent from the June communication.

If the unemployment rate remains at 4.5% or trends higher, NAB would view this as a material signal toward a more dovish policy direction and potentially earlier-than-2027 cuts.

The pause that still demands active positioning

The base case is settled: 4.35% through 2026, with a first cut projected for the first half of 2027. Market pricing reflects this consensus, with virtually no probability of further hikes or meaningful easing priced for the remainder of this year.

The risk distribution, however, is not symmetrical. The RBA’s silence on capacity utilisation, the unexpected unemployment jump, and the deliberately open-ended statement language all point to an economy where downside risks may be building faster than the Board has publicly acknowledged. Investors who treat this hold as a full stop are reading the wrong signal.

Three near-term data releases will do more to clarify the rate path than any further parsing of the June statement. Portfolios should be structured to remain responsive to those outcomes, not locked into a single scenario. The August 2026 RBA Statement on Monetary Policy is the next major inflection point.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—