The Bank of Japan raised its benchmark overnight call rate to 1.0% on 16 June 2026, a level the country has not seen since September 1995. The decision arrived without Governor Kazuo Ueda in the room, marking the first regular policy meeting held in the governor’s absence.

The 25-basis-point increase, delivered via a 7-1 board vote, represents the most significant milestone yet in Japan’s monetary normalisation cycle. It landed alongside a structured bond purchase tapering schedule designed to complement the rate hike, and against a backdrop of persistent yen weakness that continues to amplify import-driven inflation across the world’s fourth-largest economy.

What follows breaks down the specifics of the decision, the inflationary pressures that forced it, the mechanics of the tapering plan, which investor positions face recalibration, and what the forward path for Japanese monetary policy means for global portfolios.

BOJ lifts rates to 31-year high in 7-1 vote as governor sits out

The key details of the 16 June 2026 decision:

- Policy rate: Overnight call rate raised 25 basis points to 1.0%, effective immediately

- Vote: 7-1, with Board Member Toichiro Asada casting the sole dissent in favour of holding rates unchanged

- Governor absence: Kazuo Ueda did not attend due to a health-related matter, the first time a regular policy meeting has proceeded without the governor

- Historical milestone: 1.0% is the highest BOJ policy rate since September 1995, a 31-year high

31-year rate milestone: The BOJ’s policy rate has not stood at 1.0% since September 1995, when Japan was still several years from the deflationary spiral that would define two decades of monetary policy.

The decision was widely anticipated. At the April 2026 meeting, the board had held at 0.75%, but three members had already dissented in favour of an immediate move to 1.0%. The June vote narrowed that gap to a single holdout in Asada, signalling an institution moving with broad conviction despite the governor’s absence.

BOJ forward guidance was the dominant market focus in the days before the decision, with prediction markets pricing a 95-98% probability of the hike itself while investor attention shifted entirely to what the post-decision statement would reveal about the pace of future increases and the QE exit timeline.

When big ASX news breaks, our subscribers know first

Yen weakness and oil-driven inflation forced the BOJ’s hand

Two forces converged to make the hike feel necessary rather than optional: elevated crude oil prices and a depreciated yen working in tandem through Japan’s import-heavy economy.

The BOJ cited cost pass-through from crude oil as advancing at a relatively rapid pace within business-to-business transactions, with the risk of spreading into broader consumer price increases. The bank specifically named Iran-linked geopolitical tensions as the energy-shock risk it was acting to prevent from spilling into wider CPI.

CPI overshoot warning: The BOJ warned that combined energy and foreign exchange forces could push CPI inflation beyond its established 2% annual target, with underlying inflation at risk of accelerating above that level.

The yen’s role compounded the pressure. USD/JPY settled at 160.22 following the announcement, declining only 0.06%, illustrating that the currency remained near annual lows even after the hike.

Why Japan’s import dependency makes rate hikes an inflation tool

Japan imports the vast majority of its energy supply, including crude oil and liquefied natural gas (LNG). When the yen weakens, the domestic cost of those imports rises in lockstep, feeding directly into producer prices and eventually consumer prices.

This mechanism is not new. The BOJ has cited the interaction of import costs and currency weakness as a recurring driver of inflation risk across multiple policy cycles. In the current environment, with crude elevated and the yen near 160 against the dollar, the feedback loop between currency depreciation and energy costs left the board with limited room to delay.

RIETI research on yen-to-CPI transmission documents the multi-stage pass-through process, from import prices to producer prices and finally to consumer prices, providing empirical grounding for why sustained yen weakness near 160 against the dollar creates compounding inflationary pressure rather than a contained, single-stage shock.

What the bond purchase tapering schedule means for JGB markets

The rate hike was only one lever. Alongside it, the BOJ announced a structured reduction in its monthly government bond purchases, a second, structurally independent tightening mechanism running in parallel.

The tapering parameters are confirmed: monthly Japanese Government Bond (JGB) purchases will decrease by approximately ¥200 billion per quarter through March 2027, after which purchases are intended to stabilise at ¥2 trillion per month. The BOJ retained stated flexibility to modify the pace as conditions require.

The BOJ’s 16 June 2026 policy statement confirms the Policy Board set the uncollateralized overnight call rate at around 1.0 percent by a 7-1 majority, with the dissenting member preferring to maintain the existing rate target.

| Period | Monthly Purchase Target | Implication |

|---|---|---|

| Current (June 2026) | Above ¥2 trillion | BOJ remains a dominant buyer, suppressing yields |

| Q3 2026 to Q1 2027 | Reducing by ~¥200B per quarter | Gradual shift toward market-driven price discovery |

| Post-March 2027 | Stabilised at ¥2 trillion | Higher term premia likely; curve steepening expected |

As the BOJ withdraws as a dominant buyer, price discovery in JGBs shifts toward market participants. The likely consequences include upward pressure on medium- and long-term yields, increased yield volatility, and a tendency toward curve steepening. For fixed income investors, the tapering schedule is as consequential as the rate decision itself: it changes who sets the price of Japanese government debt.

The sovereign yield repricing that began in May 2026 had already sent Japan’s 10-year JGB yield to 2.8%, its highest since October 1996, well before the June rate decision, with the simultaneous surge across Germany, France, Italy, Spain, and the United States confirming that the energy-shock inflation signal was being read as structural rather than transitory by global bond markets.

How Japanese banks, property, and carry traders read this decision

The same rate decision creates distinct winners and losers rather than a uniform market signal.

| Likely Beneficiaries | Likely Headwinds |

|---|---|

| Banks and lenders (wider net interest margins) | Real estate companies (higher funding costs, rising cap rates) |

| Insurance companies (improved reinvestment yields) | Highly leveraged firms (tighter credit conditions) |

| Pension managers (better yen-denominated liability matching) | Domestic demand cyclicals (potential consumption drag) |

Japanese banks benefit most directly. Higher policy rates and a steeper JGB yield curve strengthen net interest margins and improve the economics of maturity transformation, the practice of borrowing short and lending long. Insurance companies and pension managers also stand to gain as higher domestic yields improve reinvestment economics for their yen-denominated liabilities.

On the other side, real estate companies and heavily indebted firms face rising funding costs, tighter credit, and higher capitalisation rates that weigh on asset valuations. The central equity market question remains unresolved: does normalisation validate healthier economic conditions and support a re-rating, or does it constrain growth and compress multiples?

The carry trade dimension extends the impact well beyond Japan. A structurally higher Japanese policy rate erodes the yen’s attractiveness as a cheap funding currency. Any sharp yen appreciation could trigger disorderly unwinds, with the most exposed positions concentrated in:

The carry trade mechanics operating through the yen have a transmission channel that reaches well beyond Japan, with carry-trade liquidation compressing the Australian dollar, AUD/JPY cross rates, and higher-beta equity sectors within hours of any yen appreciation shock, regardless of whether a portfolio holds Japanese assets directly.

- Emerging market FX and local rates, where Japanese and global speculative participation is high

- High-yield credit, which benefited from ultra-cheap global funding conditions

- Emerging market local-currency debt, vulnerable to a reversal in yield-seeking capital flows

Understanding Japan’s monetary normalisation cycle

For readers less familiar with Japan’s monetary history, the significance of 1.0% requires context.

Japan spent much of the past two decades fighting deflation, a persistent decline in prices that discouraged spending and investment. To combat it, the BOJ maintained negative interest rates (where banks were effectively charged to hold reserves at the central bank) and deployed yield curve control, a policy that capped long-term government bond yields at specified levels.

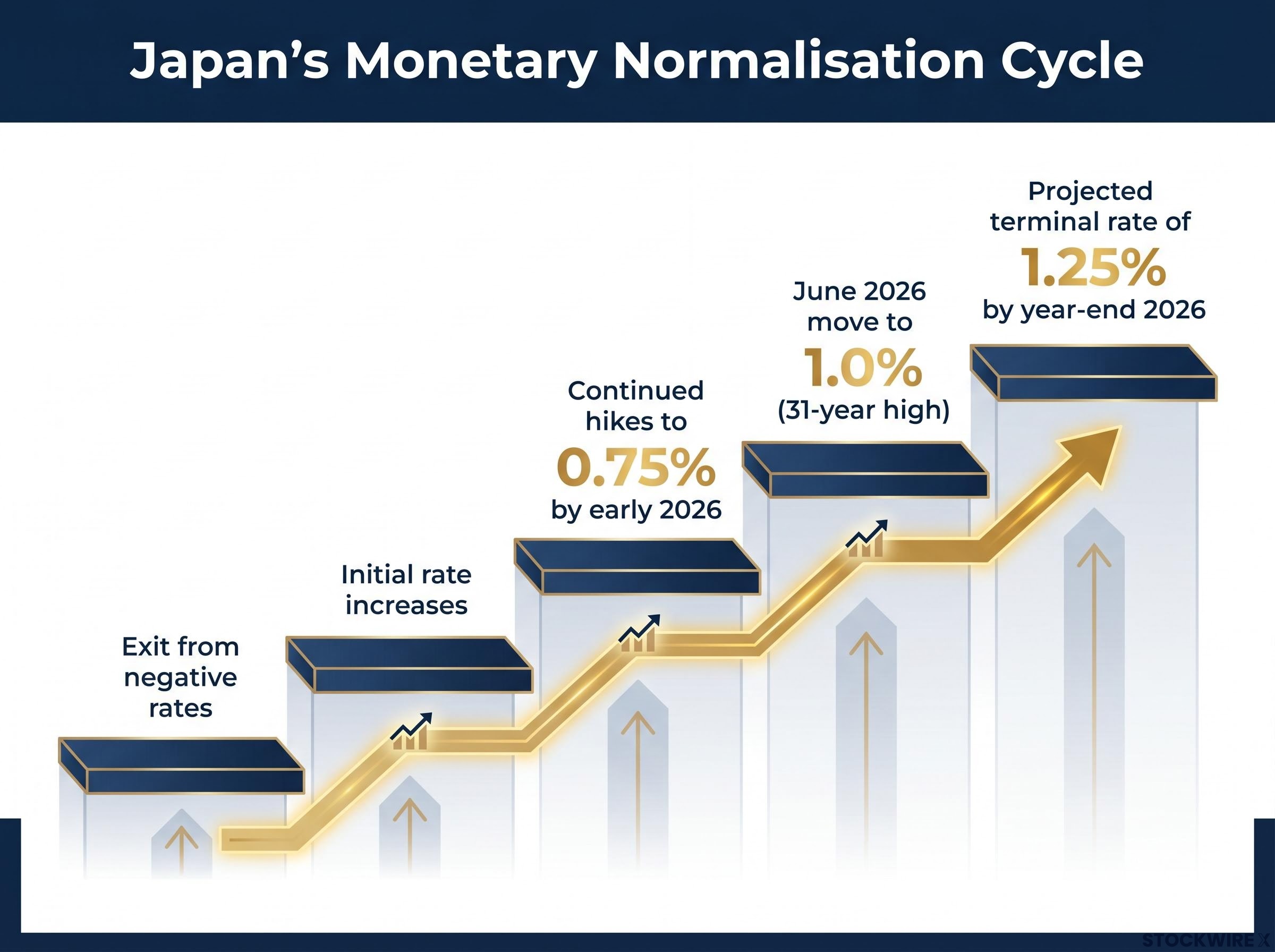

The normalisation path has unfolded in stages:

- Exit from negative rates, ending a policy that had been in place for years

- Initial rate increases, moving gradually from zero toward positive territory

- Continued hikes to 0.75% by early 2026, with the April meeting holding at that level

- The June 2026 move to 1.0%, a 31-year high and a marker of Japan’s return to conventional monetary policy territory

- Projected terminal rate of approximately 1.25% by year-end 2026, based on market consensus

The BOJ’s 2% annual CPI target, which had been persistently undershot for years, is now at risk of being exceeded. That shift from chronic undershooting to overshoot risk is what enabled the current tightening cycle and what continues to drive it.

What the market expects next from the BOJ

Market consensus points to a terminal rate of approximately 1.25% by the end of 2026, with the next move anticipated in Q4 2026. This is market expectation, not confirmed BOJ guidance. The actual pace depends on the inflation trajectory, yen direction, and global rate conditions, particularly the path of US Federal Reserve policy.

Japan’s tightening cycle just became a variable every global investor needs to model

The dual tightening levers, a rate hike to 1.0% and a structured bond tapering schedule, send a reinforcing signal. The BOJ is committing to normalisation as a sustained policy direction, not responding tactically to a single inflation spike.

The global spillover channels are concrete. As domestic yields rise, Japanese investors face reduced incentive to seek yield abroad, potentially tightening demand for foreign bonds in emerging market local-currency debt and some global credit segments. The carry trade unwind risk intensifies as the yen funding advantage structurally narrows.

For investors who want to model the full cascade risk of a disorderly carry unwind, our deep-dive into CTA selling mechanics examines how Goldman Sachs quantified the $100 billion asymmetric selling threat from trend-following funds in June 2026, including the rule-driven algorithm triggers that could compound yen-driven price declines across equity markets faster than any fundamental-driven selloff.

The rate differential versus the Fed and the European Central Bank (ECB) remains the key constraint on yen appreciation. USD/JPY at 160.22 post-decision reflects a market that views the gap as still wide enough to limit yen strength, but that calculus shifts if the Fed cuts or the BOJ accelerates.

Three forward indicators will determine the trajectory:

- BOJ forward guidance on Q4 2026 timing and conditions for the next rate increase

- USD/JPY trajectory relative to the 160 level, with any sustained move lower signalling a shift in carry trade economics

- Crude oil price developments, given the BOJ’s explicit citation of energy-shock risk as a policy driver

Whether or not a portfolio holds Japanese assets directly, the yen carry trade dynamic and Japanese demand for global bonds make this tightening cycle relevant to asset allocation decisions far beyond Tokyo.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including terminal rate projections and anticipated policy timing, are based on market consensus as of mid-June 2026 and are subject to change based on economic conditions and BOJ deliberations.