Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

An Australian investor receives a $20,000 bonus and faces a question with no obvious answer: invest it all today, or spread it across the next 12 months? The dilemma is genuine, and millions of Australians confront some version of it every year. Dollar cost averaging is one of the most discussed strategies in personal finance, yet it remains persistently misunderstood. Some dismiss it as mathematically inferior. Others treat it as universally safer than it actually is.

The reality is more nuanced. The choice between dollar cost averaging and lump-sum investing is not purely mathematical; it is also behavioural. The current Australian market environment, with the RBA cash rate at 4.1%, headline inflation forecast at 4.2% by mid-2026, and elevated ASX volatility, makes the question more practically urgent than it was during the post-GFC bull market.

What follows is a clear explanation of how dollar cost averaging works mechanically, what the evidence actually says about when each strategy wins, and a concrete framework for deciding which approach fits a given investor’s situation, including Australian platform options and tax implications.

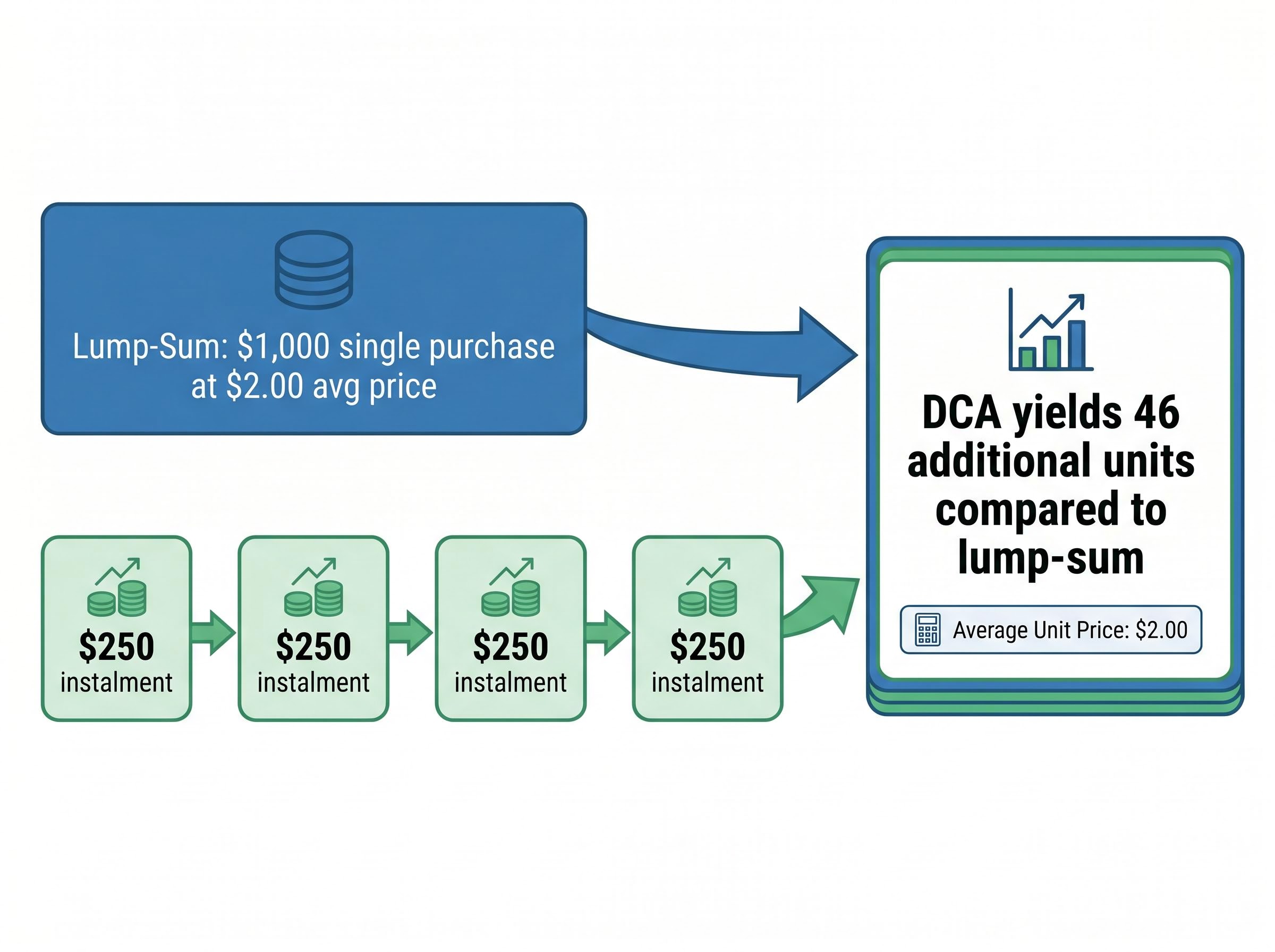

The logic sits at the unit level. A fixed dollar amount invested at regular intervals buys more units when prices fall and fewer units when prices rise. Over time, this produces a smoothed average cost per unit, lower than the simple average of the prices paid.

Consider a practical example. An investor has $1,000 to deploy into an ASX ETF. Rather than buying in one transaction, they split it into four $250 instalments. If the unit price moves across those four purchases, the fixed dollar amount captures more units during the dips and fewer during the peaks.

The arithmetic difference is tangible. In illustrative modelling at an average unit price of $2.00, splitting $1,000 into four equal instalments yields 46 additional units compared to a single $1,000 purchase at the same average price.

That difference matters because it compounds over years. But DCA does not guarantee better returns. It reduces the impact of entry-point timing on the average cost. The distinction is worth holding onto for everything that follows.

Setting up a DCA approach in Australia involves four steps:

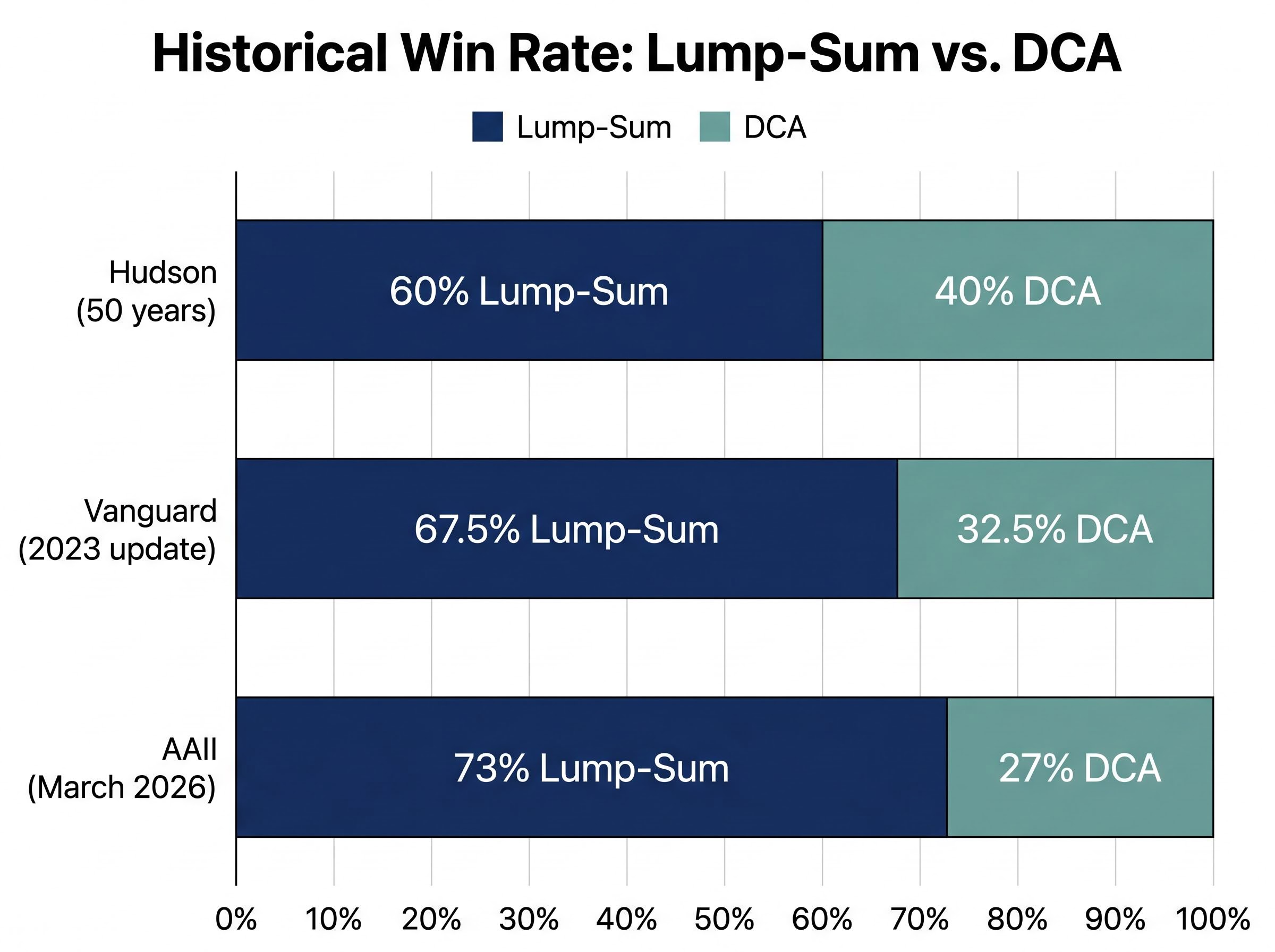

The research points in one direction, and it does so from multiple independent sources. Lump-sum investing outperforms DCA in the majority of historical scenarios, typically 60-75% of the time, because markets trend upward over time and earlier market exposure compounds returns sooner.

Hudson Financial Planning examined 50 years of ASX data and found that lump-sum beat staged investing in approximately 60% of market environments. Vanguard’s 2023 update, incorporating data through 2022 including Australian markets, showed lump-sum winning approximately 67.5% of the time after one year versus a 12-month DCA approach. The American Association of Individual Investors (AAII), in analysis published March 2026 covering rolling 20-year U.S. periods since 1926, put the figure at 73%.

The pattern is consistent. The degree of lump-sum advantage varies by market regime, but no 2024-2025 research has overturned the consensus for ASX conditions.

Then there are the exceptions. During the 2000-2002 tech correction, DCA limited losses to -1.75% annualised compared to -13.84% annualised for lump-sum, according to Morningstar Australia. Sustained downturns and high-volatility environments are precisely where DCA’s smoothing properties earn their keep.

| Measure | Lump-sum | DCA |

|---|---|---|

| Historical ASX win rate (Hudson, 50 years) | ~60% of scenarios | ~40% of scenarios |

| Vanguard 1-year data (2023 update) | ~67.5% of the time | ~32.5% of the time |

| AAII 20-year rolling periods (March 2026) | 73% of the time | 27% of the time |

| 2000-2002 downturn performance | -13.84% annualised | -1.75% annualised |

| 2026 environment verdict | Weaker case (elevated volatility) | Stronger case (rate/inflation uncertainty) |

The weight of evidence favours lump-sum in most historical windows. The behavioural counter-argument, however, is not a concession. It is a separate and well-supported case.

The statistical scoreboard tells one story. The underlying reason tells a more useful one.

Lump-sum wins most of the time because the market’s long-run trajectory is upward. Every day cash sits uninvested while waiting for the next DCA instalment is a day it is not compounding inside the market. Betashares frames the logic directly: lump-sum’s edge derives from having more money working in the market for longer in rising conditions.

The experience of this is concrete. An investor spreading $20,000 across 12 months watches the market rise 3% in the first quarter while $15,000 sits in a savings account earning less than the market returned. That gap is the opportunity cost of DCA in a rising market, not a theoretical concept but a visible drag on returns.

DCA does not eliminate market risk. It redistributes entry-point risk across time. In a steadily rising market, that redistribution is a drag. In a sideways or declining market, it is genuine protection. The distinction matters.

Investors who choose DCA believing it reduces overall risk are solving a different problem than the one they face. The risk being managed is the risk of a single bad entry, not the risk of the market declining over time.

The cost of reactive trading in Australia compounds across four distinct mechanisms: transaction fees, tax drag from forfeiting the 50% CGT discount, timing errors from missing recovery sessions, and opportunity cost from cash held uninvested, with behavioural finance research estimating a combined return drag of approximately 1.5% per annum.

The mathematical consensus holds across multi-decade horizons. The current environment, however, narrows the gap.

The RBA raised the cash rate to 4.1% following hikes in February and March 2026. Headline inflation is forecast to reach 4.2% by mid-2026, with underlying inflation peaking at approximately 3.7%. ASX volatility has been elevated through this period, driven by inflation pressures and ongoing rate uncertainty.

The RBA’s March 2026 monetary policy decision confirmed the cash rate target at 4.10 per cent, with the Board citing persistent underlying inflation and a still-resilient labour market as the primary factors shaping the tightening path through the first half of the year.

Lump-sum outperformance is most pronounced in calm, steadily rising bull markets. The current regime is not that. Elevated volatility, persistent rate uncertainty, and the psychological weight of deploying a large sum into a market that could draw down 5-10% in a quarter all strengthen DCA’s practical case relative to the post-GFC environment that produced much of the historical outperformance data.

Three conditions specifically favour DCA over lump-sum in the current environment:

ASX Q1 2026 trading volumes ran 32% above Q1 2025 levels, a concrete measure of reactive investor behaviour that confirms the elevated volatility environment is not merely a macro abstraction but a pattern visible in actual platform activity across the retail cohort.

The long-run upward trend of the ASX remains intact, preserving the multi-decade case for market participation in either form. The near-term environment simply provides a reasonable empirical basis for choosing DCA rather than treating it as an emotional concession.

The hybrid approach: Deploy a portion of available capital immediately to capture early compounding, then continue with regular automatic contributions. This pragmatic middle ground is particularly relevant for investors receiving a one-time windfall alongside regular income.

Three Australian platforms support automated DCA with low friction, each with a distinct positioning.

| Platform | Auto-invest feature | Minimum investment | Asset access | Key limitation |

|---|---|---|---|---|

| Pearler | Automated recurring purchases for ASX ETFs and index funds | Low | ASX | Limited to ETFs and index funds |

| CommSec Pocket | Recurring DCA purchases, trades from $2 | Low | ASX (themed portfolios) | Relatively low customisation |

| Stake | Fractional shares and recurring investment | Low | ASX and U.S.-listed | Fee structure varies by market |

A cost consideration specific to DCA: brokerage fees accumulate across many small transactions. An investor making 12 purchases per year rather than one is paying 12 sets of brokerage. Comparing per-trade fees relative to the investment amount is a genuine decision factor, and lower-cost platforms become more efficient at smaller regular amounts.

Australian investors setting up recurring purchases have access to several automated DCA platforms beyond the three listed here, including Interactive Brokers and Betashares Direct, each with different fee structures and asset coverage worth comparing before committing to a schedule.

Each DCA purchase creates a separate capital gains tax (CGT) parcel, a distinct record with its own cost base and acquisition date. This has three practical consequences investors should track:

Both DCA and lump-sum strategies can be implemented inside superannuation structures, where the 15% concessional tax rate amplifies the benefit of either approach. The tax advantage of super is independent of which method is used.

Investors with complex tax situations, such as those involving SMSFs, trusts, or multiple asset classes, should consult a registered tax adviser for tailored guidance.

The decision is not binary. It maps to two variables: time horizon and behavioural type.

The most common real-world scenario for Australian investors is not a one-time lump-sum decision at all. Salary and wages arrive regularly, making DCA not a strategic choice but a structural reality. The question then becomes whether to deploy windfalls (bonuses, inheritance, tax refunds) as lump-sums or spread them.

Younger Australian investor cohorts are demonstrating a structural preference for systematic investing strategies, with cohort data showing up to 70% of allocations directed toward broad-market ETFs, a pattern that reinforces the structural reality of DCA for most investors whose primary capital inflows arrive as regular income rather than windfalls.

The core principle across all sources: behaviour and consistency drive long-term outcomes more than entry-point timing. For new investors, establishing the habit of consistent, automated investing through DCA is often more valuable in practice than optimising for theoretical lump-sum outperformance.

Lump-sum is mathematically superior in most historical scenarios. The evidence on this point is convergent and robust. But the gap narrows in the current 2026 Australian environment, where elevated rates, persistent inflation, and ASX volatility make DCA’s risk-mitigation properties more practically relevant than they were during the post-GFC bull run.

The hybrid approach offers a pragmatic synthesis: neither strategy requires choosing between mathematical optimality and emotional sustainability. Deploy a portion immediately, automate the rest, and let compounding do its work across both tranches.

The most consequential decision is not lump-sum versus DCA. It is whether to start investing consistently at all. Time in the market matters more than the method of entry for long-run wealth building.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Dollar cost averaging is an investment strategy where a fixed dollar amount is invested at regular intervals, automatically buying more units when prices are low and fewer when prices are high, producing a smoothed average cost per unit over time.

Historically, lump-sum investing outperforms dollar cost averaging approximately 60-75% of the time on ASX and global markets because markets trend upward and earlier exposure compounds returns sooner, though DCA performs better during sustained downturns such as the 2000-2002 tech correction.

Pearler, CommSec Pocket, and Stake all support automated recurring investment purchases on the ASX, with low minimum investment thresholds and varying fee structures suited to regular small contributions.

Each DCA purchase creates a separate CGT parcel with its own cost base and acquisition date, meaning the 50% CGT discount applies individually to each parcel held for more than 12 months and requires careful record-keeping across all transactions.

With the RBA cash rate at 4.1%, inflation forecast at 4.2% by mid-2026, and elevated ASX volatility, DCA's risk-mitigation properties are more practically relevant now than during the post-GFC bull market, making a hybrid approach (deploying some capital immediately and automating the rest) a pragmatic option for most investors.