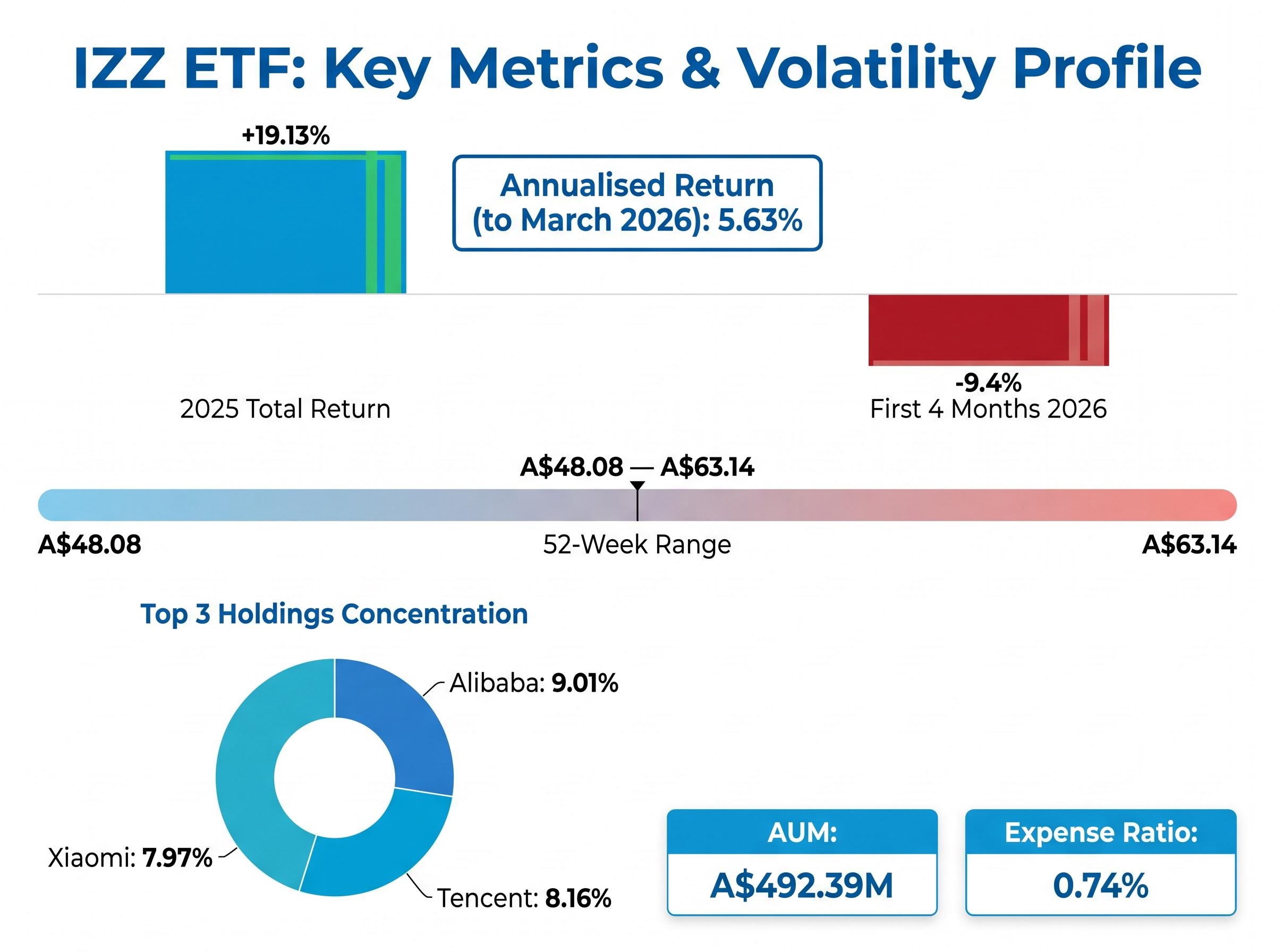

After delivering a 19.13% total return in 2025, IZZ, the ASX’s primary China large-cap ETF, has shed approximately 9.4% in the first four months of 2026. That single reversal captures the core tension Australian investors now face: a structurally compelling long-term thesis interrupted by violent short-term reality.

The debate around China ETF exposure on the ASX has intensified as US global leadership visibly recedes under America First policy settings, the US-China trade war escalates with tariffs reaching 145%, and China posts Q1 2026 GDP growth of 5.0%. For Australian investors carrying heavy US equity tilts, the question of whether to rotate toward Chinese equities is no longer hypothetical.

The shift toward China exposure sits within a broader structural reorientation: home bias in Australian portfolios has visibly weakened across every generational cohort in Q1 2026, with international ETFs overtaking domestic funds as the most purchased category on the Selfwealth by Syfe platform for the first time on record.

What follows is a clear-eyed assessment of what a China ETF allocation actually involves, from the investment thesis and the mechanics of available funds to the structural constraints that make Chinese equity investing unlike any other market exposure.

Why the geopolitical shift is generating real portfolio questions in 2026

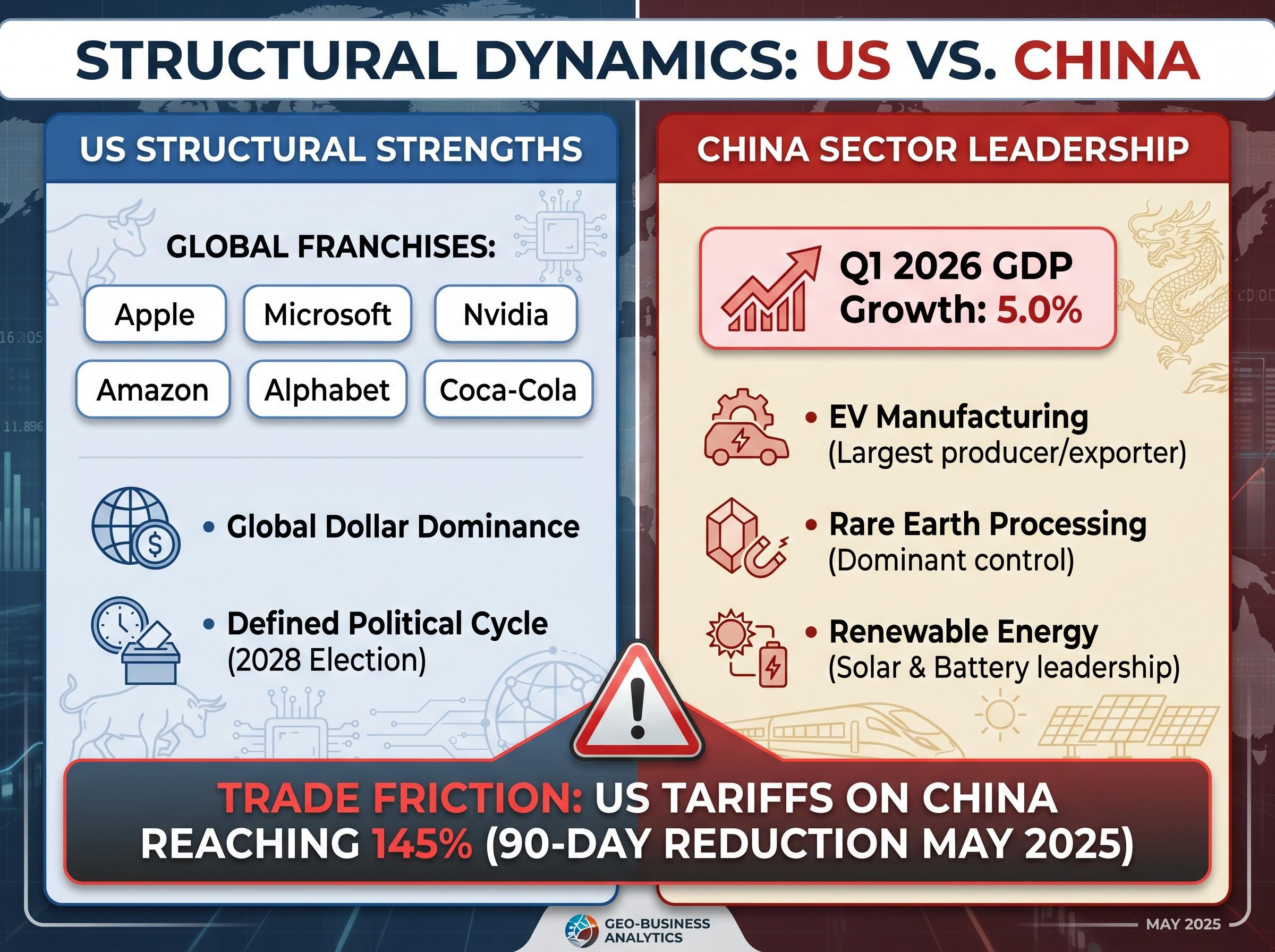

This is not routine market volatility. The US withdrawal from multilateral institutional roles it has held since the post-World War II era represents a category-level shift in global power dynamics. America First policy settings have redrawn trade architecture, with tariffs on Chinese goods escalating to approximately 145% under the Trump administration’s second term before a 90-day reduction was announced in May 2025.

If US influence continues receding, China, as the world’s second-largest economy with publicly stated superpower ambitions, is the most structurally positioned beneficiary. The country holds sector leadership positions that underpin global supply chains:

- Electric vehicle manufacturing: The world’s largest producer and exporter of EVs

- Rare earth mineral processing: Dominant control over refining and processing infrastructure

- Renewable energy production: Leading global capacity in solar panel and battery manufacturing

Q1 2026 GDP growth: 5.0% China’s first-quarter GDP growth accelerated to 5.0%, up from 4.5% the prior quarter, signalling economic resilience despite trade war headwinds.

The question for Australian investors is whether this geopolitical realignment represents a genuine structural reallocation opportunity or a cyclical distraction. The answer demands serious analysis, not a reflexive dismissal.

When big ASX news breaks, our subscribers know first

How China investing actually works for ASX investors: the structural mechanics

Most Australian investors understand how to buy a US or Australian equity ETF. China investing operates under fundamentally different rules, and the differences are not cosmetic.

How ownership works

Non-citizens cannot hold direct ownership stakes in Chinese-listed companies. ASX-listed China ETFs instead use variable interest entity (VIE) structures or hold Hong Kong-listed shares rather than direct mainland equity. The distinction between available exposure types is material:

- H-shares (Hong Kong-listed): IZZ holds large-cap Chinese companies listed on the Hong Kong Stock Exchange. These shares are subject to Hong Kong’s regulatory framework, which provides more familiar investor protections but is itself under increasing mainland influence.

- A-shares (mainland-listed): CETF accesses shares listed on mainland Chinese exchanges in Shanghai and Shenzhen. A-shares have historically been less accessible to foreign investors, carry different volatility characteristics, and operate under a distinct regulatory environment.

The choice between these exposure types determines the regulatory environment, liquidity profile, and risk characteristics an investor takes on.

State-over-shareholder governance: what it means in practice

Chinese companies are legally required to prioritise central government directives over shareholder interests. In practice, this can include restrictions on profit repatriation, mandatory government partnerships, or operational pivots executed with no shareholder vote.

This contrasts directly with OECD-standard corporate governance, where shareholder primacy is the legal baseline. These structural constraints are not theoretical footnotes. They directly affect shareholder rights and capital repatriation in ways that differ from every other major market exposure available on the ASX.

Academic research on VIE structure legal risks identifies contractual validity vulnerabilities, regulatory policy exposure, and imperfect shareholder rights protection as the primary channels through which foreign investors in Chinese equities face losses that have no direct equivalent in OECD-standard corporate governance frameworks.

IZZ under the microscope: what the numbers actually show

The 2025 return of 19.13% made the bull case easy to tell. IZZ rewarded holders who had endured years of underperformance with a meaningful rebound, and inflows reflected renewed interest. The US-listed counterpart, FXI, posted an even stronger 28.93% return over the same period.

Then 2026 arrived. IZZ’s year-to-date decline of approximately -9.4% through late April erased a significant portion of those gains. The trailing one-year total return as of April 2026 stood at -8.12%. Broader Chinese indices told the same story: the CSI 300 fell approximately 5% year to date, while the Hang Seng dropped roughly 3%.

52-week range: A$48.08 to A$63.14 A spread of approximately A$15 between the low and high over 12 months illustrates the volatility profile investors are accepting with this fund.

The longer-term picture is more sobering still. IZZ’s average annual return since inception sits at 0.41%, though the annualised figure to March 2026 is cited at 5.63% depending on the measurement period. Either number forces a harder question than the 2025 headline suggested.

The AUD’s appreciation from approximately 0.6777 to 0.7153 between January and late April 2026 created a measurable performance gap between hedged and unhedged international ETF strategies, a currency dimension that applies directly to IZZ’s unhedged Hong Kong dollar exposure for Australian holders.

| Metric | Value | What it signals | Benchmark comparison | Investor implication |

|---|---|---|---|---|

| Expense ratio | 0.74% | Higher than broad-market ETFs | Typical ASX equity ETF: 0.10-0.30% | Cost drag compounds over long holding periods |

| Holdings | 50 | Concentrated portfolio | Broad EM ETFs: 300-1,500 holdings | Top 3 names (Alibaba 9.01%, Tencent 8.16%, Xiaomi 7.97%) carry meaningful single-stock risk |

| Dividend yield | 2.16% | Moderate income component | ASX 200 yield: approximately 4% | Not an income vehicle |

| AUM | A$492.39M | Sufficient liquidity for retail investors | Largest ASX-listed China fund | Bid-ask spreads manageable at this scale |

| Annualised return (to March 2026) | 5.63% | Modest long-run compounding | S&P 500 long-run average: approximately 10% | Returns have not compensated for the volatility experienced |

The numbers build a clear picture: IZZ is capable of strong short-term performance within a long-run return profile that demands honest assessment of whether the risk justifies the allocation.

The three China ETF options ASX investors actually have

The decision is not simply whether to buy IZZ. Three distinct exposure profiles are available, and they serve different portfolio objectives.

| Fund | Exposure type | Key risk | Best suited for |

|---|---|---|---|

| IZZ | Hong Kong-listed large caps (50 holdings, 0.74% expense ratio) | Concentrated single-stock exposure; Hong Kong regulatory evolution | Investors seeking direct, liquid large-cap China exposure |

| CETF | Mainland A-shares (Shanghai/Shenzhen exchanges) | Mainland regulatory environment; historically higher volatility | Investors seeking differentiated mainland exposure beyond Hong Kong |

| Betashares MSCI Emerging Markets | Diversified EM with significant China weighting | Diluted China-specific upside; broader EM risk factors | Investors wanting China exposure with built-in risk distribution |

No major new pure-China ETF has launched on the ASX in 2025 or 2026, confirming that IZZ and CETF remain the primary targeted options. The framework for choosing between them is straightforward:

- Clarify risk tolerance. A concentrated single-country allocation carries fundamentally different risk from a diversified emerging markets position.

- Determine China conviction level. High-conviction investors with a long time horizon may suit IZZ or CETF. Lower-conviction investors may prefer China as a component within a broader EM fund.

- Choose the vehicle accordingly. The exposure type, not just the country label, determines the risk and return characteristics of the position.

The counterargument: why the US financial system remains the harder bet to fade

Where the US case remains structurally strong

The Warren Buffett principle of never betting against the United States is not a closing argument, but it is a useful starting point. The US corporate ecosystem, represented by global franchises such as Apple, Microsoft, Nvidia, Amazon, Alphabet, and Coca-Cola, has demonstrated a durability of competitive moat that Chinese equivalents have not yet replicated across global markets.

The US dollar’s continued dominance in global trade, despite the Bretton-Woods collapse in the 1970s, serves as a historical data point for how resilient structural financial advantages can be once embedded in the global system. The US financial system remains the central pillar of global capital markets. The 2028 presidential election also creates a defined horizon for potential policy reversal, meaning the current political environment may prove temporary rather than structural.

Where the China bull case has genuine gaps

China’s 5.0% Q1 GDP headline requires qualification. Consumer confidence remained pressured through early 2026, with trade war uncertainty weighing on domestic sentiment. The property sector recovery has been described as uneven and fragile, with increased fixed-asset investment offset by ongoing structural challenges.

China’s Q1 2026 GDP analysis recorded 5.0% year-on-year growth alongside an 11.2% fall in property investment and soft consumer spending, a combination that illustrates why the headline figure requires the qualification the article applies: strong aggregate output does not resolve the sectoral fragility weighing on domestic demand.

China’s corporate governance obligations to the state introduce a structural ceiling on shareholder value creation that does not exist in the same form in US markets. These are not temporary policy risks. They are built into the legal architecture of Chinese business.

- US structural advantages: Global brand penetration, dollar dominance, deep capital markets, corporate governance aligned with shareholder interests, defined political cycles

- China structural constraints: State-over-shareholder governance, ownership restrictions for foreign investors, property sector fragility, consumer confidence headwinds, geopolitical isolation risk

Reasonable, evidence-based investors sit on both sides of this debate. The decision to allocate toward China is not a contrarian insight; it is a genuinely contested call.

The China ETF call in 2026 comes down to one question Australian investors must answer honestly

The decision hinges on a single belief: is the narrative of US power receding structural and long-duration, or cyclical and reversible? These two assumptions lead to opposite portfolio conclusions. Investors who believe the shift is structural will find the China thesis compelling. Those who view it as a cyclical disruption likely to reverse by 2028 or beyond will see little reason to alter their existing US equity allocation.

Investors pursuing international diversification away from ASX concentrated the largest single quarterly flow into global equity ETFs on record in Q1 2026, with A$6.9 billion entering international funds across the Australian market, a data point that signals the rotation this article examines is already well underway rather than anticipatory.

- Assess your view on US power trajectory. If the America First withdrawal from global leadership represents a permanent recalibration, China’s relative positioning strengthens. If it represents a temporary political cycle, the US corporate ecosystem’s competitive advantages reassert themselves.

- Determine appropriate satellite position size. IZZ’s volatility profile, with swings between 19.13% gains and -9.4% drawdowns within 18 months, makes position sizing and time horizon the critical variables. A small satellite position for investors with genuine long-term conviction is a different proposition from a wholesale portfolio rotation.

- Choose the right exposure vehicle for your conviction level. High conviction may warrant IZZ or CETF directly. Lower conviction may suit a broader emerging markets fund with built-in diversification.

IZZ annualised return since inception: 5.63% (to March 2026) The long-run figure provides a grounding reference point against the short-term performance swings that dominate headlines.

According to Vanguard, Australian investors should consider Chinese equities for portfolio diversification in 2026, despite trade war volatility. Motley Fool Australia has echoed caution on short-term volatility while acknowledging long-term growth prospects via ETFs like IZZ.

China ETFs on the ASX are a legitimate tool, not a certainty

China ETFs on the ASX offer a real mechanism for accessing a structurally important economy. The structural constraints of Chinese investing, including state governance obligations, ownership restrictions, and geopolitical volatility, are not incidental risks. They are embedded in the architecture of every position.

IZZ or CETF may serve as satellite positions sized according to genuine conviction, not as reactive plays on geopolitical headlines. Before adding China exposure, investors should review their existing US and global equity allocations to determine whether their portfolio reflects their actual view of the US-China power dynamic.

IZZ, CETF, and broad emerging markets ETFs represent three starting points for further research. The China ETF question is not binary, and the answer sits within each investor’s own assessment of where global power is heading over the next decade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.