For the first time on record, internationally focused exchange-traded funds overtook domestically focused funds as the most purchased ETF category among Australian retail investors during Q1 2026. The milestone, captured in the Selfwealth by Syfe Quarterly Investor Pulse Index published in April 2026, did not arrive in isolation. It landed against a strengthening Australian dollar, an RBA rate hike that dampened trading volumes, and a generational convergence in how Australians of all ages are constructing their portfolios. What follows is an examination of what this data reveals: how each generation is allocating, why international ETFs have finally eclipsed domestic ones, what the macro environment means for hedging decisions, and what the broad alignment in investor behaviour signals about the future of retail portfolio construction in Australia.

The headline finding: International ETFs have overtaken domestic funds

Q1 2026 marks the first period on the Selfwealth by Syfe platform where internationally focused ETFs became the single largest ETF purchase category, surpassing domestic funds. The quarter confirmed a direction that full-year 2025 data had already made visible.

The scale of the shift is difficult to dismiss as a one-quarter anomaly:

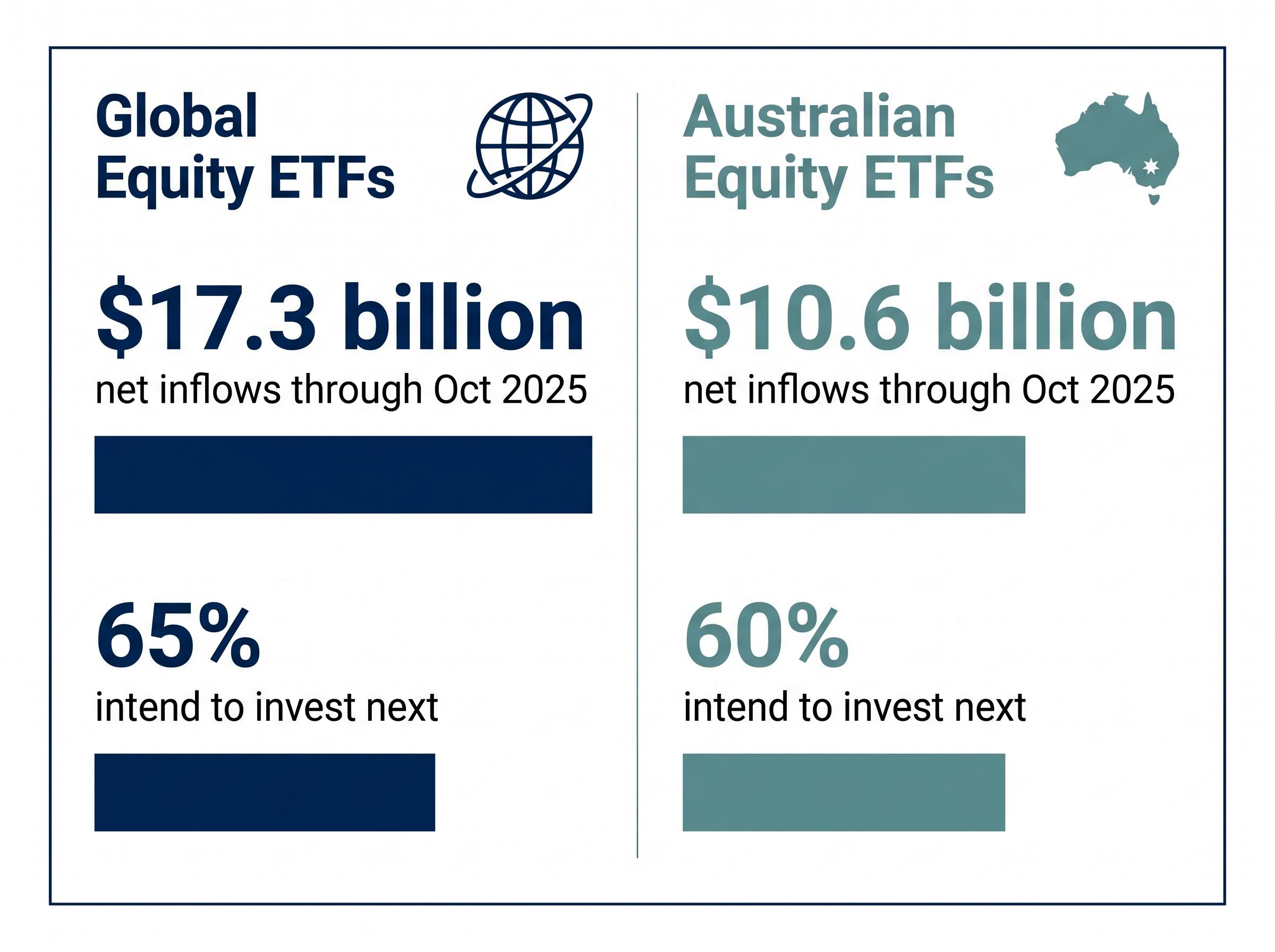

- Global equity ETFs attracted $17.3 billion in net inflows through October 2025, compared with $10.6 billion into Australian equity ETFs over the same period.

- 65% of ETF investors identified global equities as their next intended investment, versus 60% targeting Australian equities.

- The shift is not merely in execution; it is embedded in stated investor intention.

Vanguard’s VGS drew $361 million in single-month inflows during January 2026, a figure that illustrates how concentrated demand for international exposure has become within a handful of products.

The question this raises is not whether Australian investors are diversifying offshore. They are. The question is why it happened now, and whether the structural conditions behind it are durable enough to persist through the next macro disruption.

When big ASX news breaks, our subscribers know first

A generational snapshot: More similar than the headlines suggest

The expected story is one of stark generational division: younger investors in ETFs, older investors in individual stocks. The Q1 2026 data complicates that narrative.

Gen Z and Gen X both hold approximately 50/50 splits between ETFs and individual stocks. Millennials are the most ETF-concentrated cohort, allocating roughly 70% of their portfolios to ETFs. Boomers retain a preference for individual stocks, yet their ETF incorporation is rising, suggesting adoption is not a generationally bounded phenomenon.

| Generation | Approximate ETF Share | Individual Stock Share | Key Behavioural Note |

|---|---|---|---|

| Gen Z | ~50% | ~50% | More disciplined than stereotypes suggest |

| Millennials | ~70% | ~30% | Most ETF-heavy cohort |

| Gen X | ~50% | ~50% | Mirrors Gen Z allocation split |

| Boomers | Lower, rising | Higher | Gradual ETF incorporation underway |

Across all cohorts, 81% of ETF investors plan to increase their ETF holdings in 2026. Total Australian ETF participation reached 2.7 million (up 20% year-on-year), with 411,000 first-time buyers entering the market in 2025 alone.

Where the generations are actually converging

Despite differing allocation percentages, Q1 2026 data shows cross-generational alignment on three decisions: increasing international exposure, reducing domestic concentration, and using ETFs as the primary vehicle for deploying new capital.

Part of this convergence is structural. Lower platform entry barriers and auto-invest features have reduced friction for cohorts that previously found ETF access more cumbersome. The result is that portfolio construction methodology is converging even where risk tolerance and asset preferences differ.

Platform accessibility has been a decisive enabler of the generational convergence visible in Q1 2026 data: lower fees, fractional share access, and auto-invest features have reduced the structural friction that previously kept older cohorts anchored to direct equity holdings and newer investors from building diversified offshore exposure.

Why Australian investors are shedding home-country bias now

Home-country bias describes the tendency for investors to overweight domestic assets relative to their share of global market capitalisation. In Australia, the bias has been historically pronounced: the ASX represents a small fraction of global equity markets, yet Australian portfolios have traditionally concentrated the majority of their equity exposure domestically. That concentration creates a form of risk that ETF investors are now explicitly managing.

Three forces are driving the correction:

The home-country bias correction now underway is not simply a product of improved investor education; it reflects a structural mismatch between where Australian wealth is held and where global equity value creation is concentrated, with the ASX representing well under 2% of total global market capitalisation.

- Structural market size: The ASX’s limited representation of global capitalisation means a heavily domestic portfolio misses the vast majority of global equity returns. This argument has existed for years but is now reaching a broader investor audience.

- Macro-economic pressures: According to Betashares, diversification needs have been amplified by housing affordability constraints and cost-of-living challenges, making offshore exposure feel more urgent rather than merely optimal.

- Platform accessibility: The barriers to international market access that previously sustained home-country bias, including higher fees, currency conversion friction, and limited product availability, have materially declined.

Betashares attributes the accelerating shift to diversification needs amplified by housing pressures and cost-of-living challenges, framing the move as a response to specific Australian economic conditions rather than a passive following of global index trends.

VanEck (2026) has identified global inflection points as a further driver, noting that geopolitical and economic disruptions are reinforcing the case for geographic diversification at the portfolio construction stage rather than as an afterthought. For investors still holding a predominantly ASX-weighted portfolio, the structural logic behind the industry-wide rebalancing is becoming harder to set aside.

What the ETF market looks like when the Australian dollar strengthens

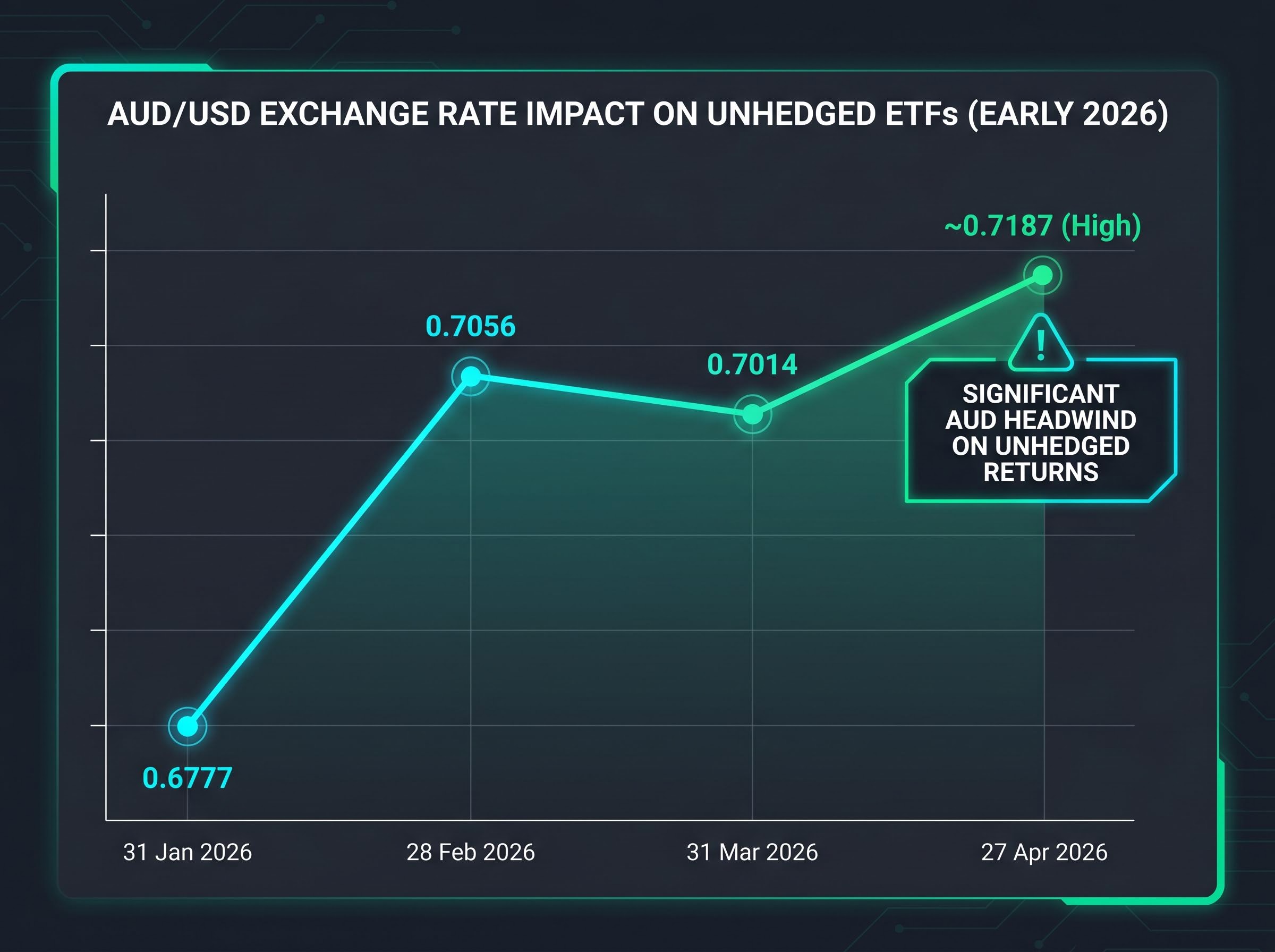

The AUD’s appreciation through early 2026 introduced a complication that the “go global” consensus had not fully priced. From approximately 0.6777 on 31 January 2026 to approximately 0.7153 in mid-to-late April 2026, the currency moved enough to create a measurable performance divergence between hedged and unhedged international ETF strategies.

| Date | AUD/USD Rate | Hedged ETF Impact | Unhedged ETF Impact |

|---|---|---|---|

| 31 January 2026 | 0.6777 | Neutral baseline | Neutral baseline |

| 28 February 2026 | 0.7056 | Shielded from AUD rise | Returns eroded in AUD terms |

| 31 March 2026 | 0.7014 | Continued outperformance | Drag persists despite slight AUD pullback |

| 27 April 2026 | ~0.7187 (high) | YTD outperformance vs unhedged | Significant AUD headwind on returns |

The mechanism is straightforward: when the AUD strengthens, unhedged international ETF returns are reduced in AUD terms even if the underlying assets perform well. Hedged S&P 500 ETFs outperformed their unhedged equivalents on a year-to-date basis over this period, a reversal from the conditions that prevailed while the dollar was weaker.

How the RBA rate hike registered in trading behaviour

Trading activity declined more than 20% following the RBA rate hike in March 2026. That contraction stands in contrast to the doubling of trading volumes observed during the US tariff announcement in April 2025.

The RBA March 2026 monetary policy decision raised the cash rate by 25 basis points to 4.10 percent, a move whose dampening effect on retail trading activity is visible in the more than 20 percent contraction in platform volumes that followed.

The divergence is instructive. Domestic monetary policy appears to generate avoidance behaviour, with investors pulling back from the market. Global macro events generate engagement, with investors leaning in. For those assessing their own hedging exposure, the AUD environment in mid-2026 warrants attention that many international ETF holders may not have given it when the dollar was falling.

What it means that gold demand is cooling while ETF flows accelerate

The gold trade moved through three distinct phases in recent quarters:

- Late 2025: Elevated gold demand, driven by geopolitical instability, pushed gold-related buying activity higher as investors sought defensive positioning.

- Q1 2026: Gold-related buying declined to below 70% of total trades on the Selfwealth by Syfe platform, signalling a cooling in defensive sentiment.

- Current rotation: Capital that was parked in gold-adjacent assets has begun moving toward financial equities and growth-oriented ETFs.

Gold-related buying activity fell to below 70% of total trades on the platform during Q1 2026, a concrete marker of the shift in retail investor positioning from defensive to growth-oriented.

The rotation extends beyond gold. Risk-on flows are visible in Asia technology ETFs, including IKO and ASIA (both with SK Hynix exposure), while copper-focused ETFs attracted a notable single-month inflow spike in January 2026.

Gold retains a portfolio role as an inflation and geopolitical hedge, but the Q1 2026 data characterises that role as cyclical and sentiment-driven. The dominant retail positioning in early 2026 has shifted toward growth, not defence. Tracking where capital rotates tells investors something about prevailing sentiment that price charts alone do not capture.

Defensive asset rotation away from gold and toward financial equities and growth-oriented ETFs reflects a broader reassessment of what hedges actually work in a supply-driven inflationary environment, where traditional bond and gold combinations have failed to provide the capital preservation they historically offered.

The three structural forces now shaping how Australians build portfolios

The data examined across this analysis points to three durable structural forces that are likely to persist beyond any single quarter:

- Geographic diversification as default: International exposure is no longer an advanced portfolio overlay. It is becoming the starting point for new and existing investors alike, as the home-country bias that defined prior decades of Australian retail investing erodes.

- ETFs as the primary construction vehicle: Across all generational cohorts, ETFs have become the instrument of choice for deploying new capital. ETFs now represent 17% of average portfolios, the highest share on record. Australian ETF assets under management grew 31.7% over the past year to March 2026, with a five-year compound annual growth rate of 26.3%.

- Macro-responsiveness as a feature, not a bug: Retail investors are reacting to currency movements, rate decisions, and geopolitical developments with increasing sophistication. That responsiveness creates both opportunity and risk, particularly when tactical decisions (hedging, gold rotation) are conflated with structural ones.

Betashares Australian ETF market data confirms the participation figures cited here, recording 2.7 million investors active in the local ETF market and projecting approximately 300,000 new entrants in 2026 alone, a growth trajectory that underpins the structural rather than cyclical character of this shift.

Betashares forecasts total Australian ETF assets under management exceeding $500 billion by the end of 2028, a projection that, if realised, would place the industry at roughly double its current scale.

Sitting on top of these structural forces are the tactical dynamics: hedging decisions driven by AUD strength, the gold-to-equities rotation, and sector-specific thematic flows. Separating the structural from the tactical is the task facing investors who want to position for the medium term rather than react to the quarter.

An estimated 300,000 new ETF investors are projected to enter the market in 2026, pushing total Australian participation above 3 million. These structural forces are still in their growth phase.

Australian ETF investing in 2026 is a story still being written

The international-over-domestic inflection in Q1 2026 is not a one-quarter event. It is the visible surface of a structural change in how Australian retail investors conceive of portfolio construction, a shift backed by multi-year flow data, generational convergence, and macro conditions that have made offshore diversification feel more rational than domestic concentration.

The unresolved question is whether the discipline observed in Q1 2026, diversification-oriented, cross-generational, thematic rather than reactive, holds through the next major macro disruption. The RBA’s rate hike already revealed that domestic monetary policy can suppress engagement. A sustained AUD rally or a global equity drawdown would test the durability of these positioning choices.

Investors reviewing their own portfolios in mid-2026 may find value in three reference points from this data: the generational benchmarks for ETF allocation, the hedging question raised by AUD strength, and whether their domestic-to-international ratio reflects a considered view or an inherited default.

For investors who recognise the structural case for international diversification but find themselves reacting to each macro event rather than executing a plan, systematic investing approaches like dollar-cost averaging into diversified index products offer a concrete framework for separating structural positioning decisions from tactical noise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.