ASX 200 Posts Four-Day Run as WiseTech Sheds 18% in One Session

1 hr ago

Binary options were once synonymous with offshore fraud and SEC enforcement actions. Now one of America’s largest brokerages is preparing to put them in front of everyday investors.

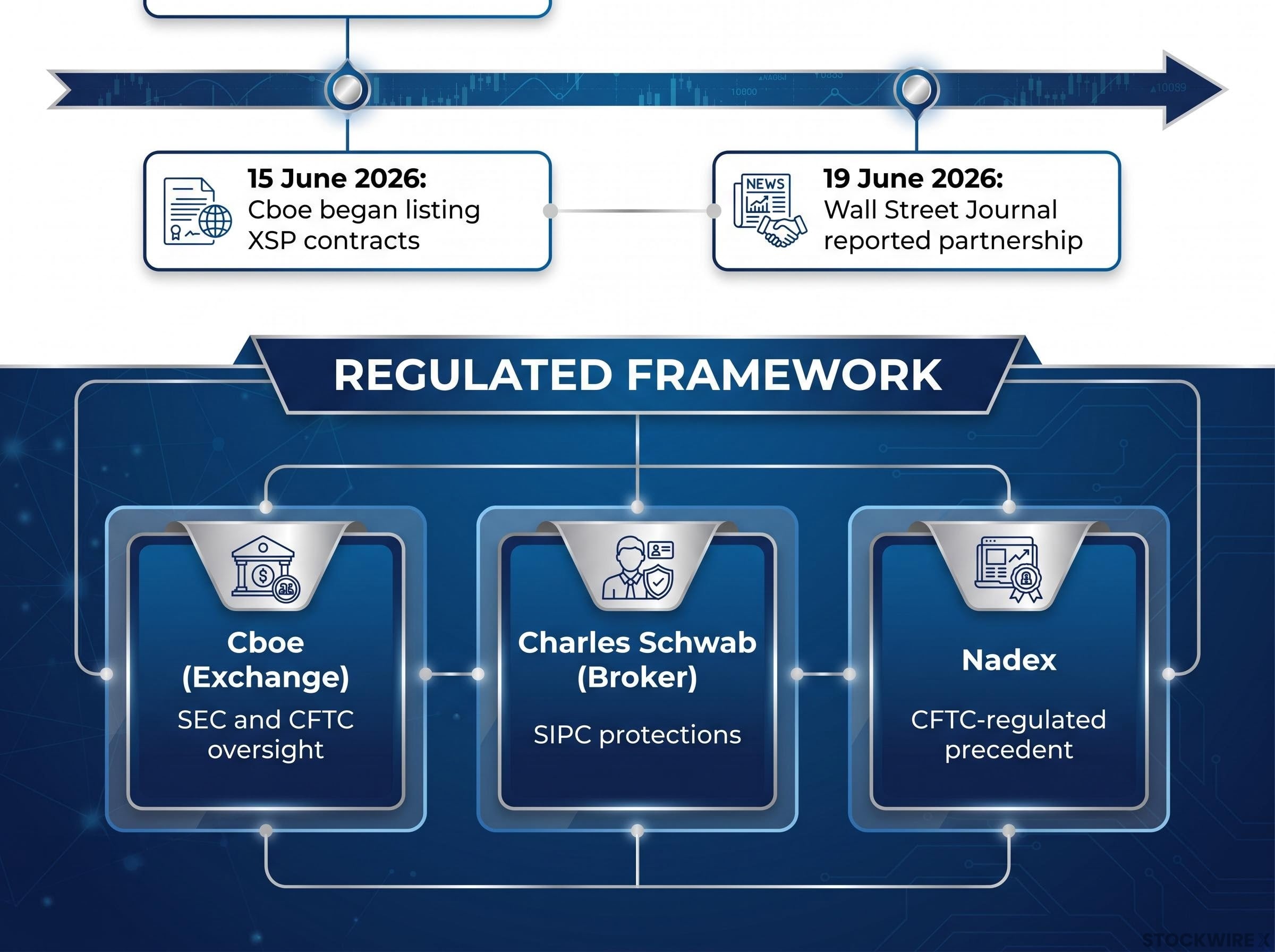

Charles Schwab is partnering with Cboe Global Markets to list S&P 500-linked binary options on its retail platform. Cboe began listing Mini S&P 500 (XSP) binary options on 15 June 2026, and the Wall Street Journal reported the partnership details on 19 June 2026. Schwab customer access is expected in the coming months, meaning these contracts are not yet live in accounts but are close enough to warrant attention.

The launch marks a significant moment in the ongoing expansion of speculative instruments into mainstream retail trading. What follows explains exactly what Schwab is launching, how the contracts pay out, why this version differs from the offshore schemes that made binary options infamous, and what retail investors should understand before considering a trade.

The core facts are straightforward:

What makes this noteworthy is the distribution channel. Schwab’s retail customer base is one of the largest in the United States. Listing exchange-traded binary options through that platform creates a new category of access for ordinary investors, many of whom will encounter the product for the first time inside an account they associate with index funds and retirement savings.

Cboe has positioned these regulated contracts as a way to recapture retail speculative volume that migrated to offshore platforms and prediction markets in recent years, according to the Wall Street Journal.

The contracts are not yet available to Schwab clients. The window between now and the formal rollout is time investors can use to understand what they would be trading.

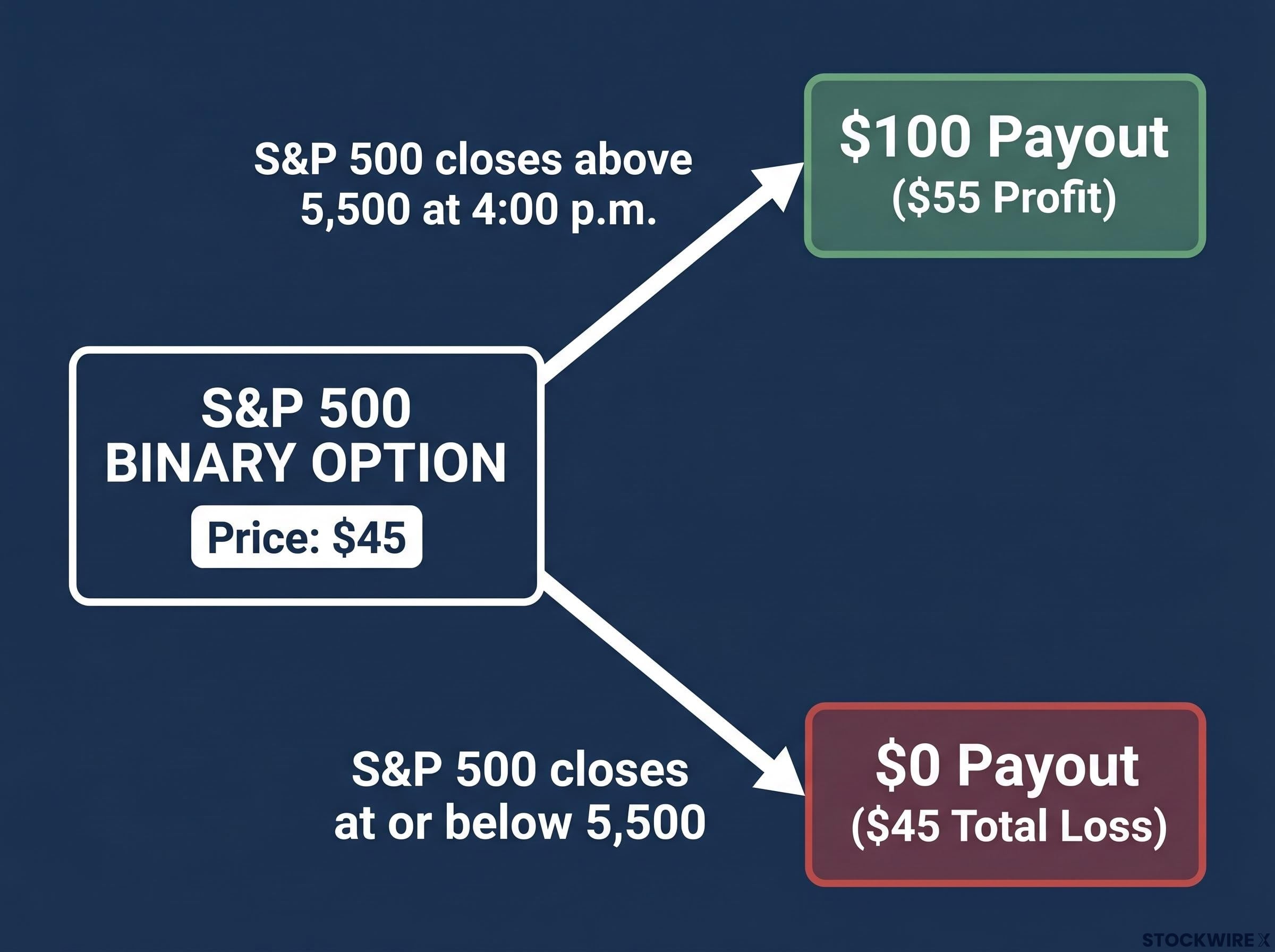

A binary option is a contract that pays a fixed sum if a specified condition is true at expiration, and pays nothing if it is false. There is no partial outcome.

Consider an S&P 500 binary priced at $45. The contract pays $100 if the index closes above 5,500 at 4:00 p.m. on the expiration date. If the condition is met, the holder receives $100, producing a $55 profit. If the index closes at or below that level, the holder receives $0 and loses the entire $45 premium.

Expiration horizons are typically short, often intraday or daily. Cboe has reportedly explored a “Plus Zone” partial-payout feature for near-miss outcomes, though this has not been independently confirmed.

This is where binary options diverge from every other option product a retail investor may already know. With a conventional call option, profit scales with how far the index moves above the strike price. A 200-point surge produces a materially larger gain than a one-point finish above the strike.

With a binary, a one-point win and a 200-point win are economically identical. Both pay exactly $100. A one-point miss and a 200-point miss are equally total losses. Both pay $0.

| Feature | Binary option | Standard call option |

|---|---|---|

| Payout if above strike | Fixed $100 regardless of magnitude | Scales with distance above strike |

| Payout if below strike | $0 (total loss of premium) | $0 (total loss of premium) |

| Does magnitude of move matter? | No | Yes |

| Maximum loss | 100% of premium paid | 100% of premium paid |

The “all-or-nothing” label is commonly used but rarely unpacked. The irrelevance of magnitude is the single most important mechanical fact for anyone encountering binary options for the first time.

The instinct that “binary options” sounds dangerous is historically justified. Offshore platforms offered unregulated contracts, manipulated pricing, obstructed withdrawals, and drew multiple enforcement actions from the SEC and CFTC. Those platforms were the reason the product category became synonymous with fraud.

The Schwab-Cboe product differs in specific structural ways:

These features remove counterparty risk and fraud risk. They do not remove market risk. A legal, fully regulated binary option still produces a total loss of premium on every losing trade. Regulation resolves the question of whether the platform will pay out; it does not change the odds of winning.

CFD trading offers a useful comparison point: between 74% and 89% of retail CFD accounts lose money according to ESMA data, a figure that illustrates how regulatory legitimacy and transparent pricing do not, by themselves, shift the odds toward retail participants in high-frequency speculative instruments.

The concerns extend beyond the product’s legality. Five distinct risk dimensions have been identified across industry and academic commentary:

Hidden costs in speculative instruments follow a consistent pattern across product categories: a 2025 CFA Institute study found retail short sellers lost an average of 18% annually from 2024-2025 primarily because of fee drag and timing errors, not directional error, a finding that applies equally to any instrument where the structural cost of participation is systematically underestimated.

Even proponents of the product concede it is unsuitable for most retail investors. Both advocacy and critique converge on one point: simplicity of the contract does not equate to simplicity of the decision to trade it.

Brokerages and exchanges earn more when clients trade more, yet frequent use of high-risk instruments is rarely aligned with building long-term wealth. This structural tension sits at the centre of the debate over mainstreaming binary options.

Schwab’s move is not an isolated decision. It follows a multi-year pattern of increasingly speculative products migrating onto retail platforms that once focused primarily on stocks and mutual funds.

Three categories of speculative instruments have made this journey in recent years:

Zero-commission trading and app-based access lowered friction. Prediction markets demonstrated demand. Cboe’s stated motivation for the binary options product explicitly cites the need to compete with that growth in a regulated format. Coinbase and Robinhood are among the platforms exploring event contracts and similar instruments, making Cboe’s offering both a defensive and offensive market move.

Cboe’s decision to enter this space was shaped in part by the rapid growth of prediction markets, where quarterly volume reached $26.2 billion in Q1 2026 but roughly 70% of users have lost money, with just 0.1% of accounts capturing the majority of all profits generated since 2022.

When a brokerage launches a new speculative instrument, the question worth asking is who benefits most from increased trading activity in that product, and whether the answer is the platform or the client.

When these contracts appear in Schwab accounts, the following self-assessment can help determine whether they belong in a given investor’s toolkit:

S&P 500 breadth and concentration data are among the inputs a binary trader might consult when assessing short-term directional probability: as of mid-May 2026, the index sat 8.5% above its 50-day moving average while only 47% of constituents traded above theirs, a divergence that illustrates how index-level price action can obscure the underlying fragility relevant to near-term directional bets.

For many investors, working through this list honestly will confirm that conventional alternatives achieve their goal with fewer embedded costs and behavioural risks.

In disciplined, well-capitalised hands, these contracts can serve a defined purpose. For many investors, however, they will function more like a regulated, financial form of gambling than a core investment tool.

The regulatory legitimacy of the Schwab-Cboe binary options product is real and meaningful. Exchange listing and broker-dealer oversight resolve counterparty risk. They do not resolve market risk or behavioural risk, and the all-or-nothing payoff structure ensures that both remain present on every trade.

Investors considering these contracts should understand settlement mechanics, size positions as a small fraction of capital, and assess their motivation and edge honestly before placing a single order. The formal Schwab rollout announcement, expected in the coming months, will provide specific contract terms, margin requirements, and account eligibility criteria.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Charles Schwab is partnering with Cboe Global Markets to offer S&P 500-linked binary options (XSP contracts) on its retail platform. Each contract pays a fixed $100 if the S&P 500 closes above a specified level at expiration, or $0 if it does not, meaning the entire premium paid is lost on a losing trade.

Unlike the unregulated offshore platforms associated with fraud and SEC enforcement actions, the Schwab-Cboe product trades on a major U.S. exchange under SEC and CFTC oversight, with standardised contract terms and customer funds covered by SIPC protections at the broker level. Regulation removes counterparty and fraud risk, but does not change the all-or-nothing market risk on each trade.

Cboe began listing Mini S&P 500 (XSP) binary options on 15 June 2026, and the Wall Street Journal reported the Schwab partnership on 19 June 2026. Schwab customer access is expected in the coming months, meaning the contracts are not yet live in retail accounts at the time of writing.

Key risks include the total loss of premium on every losing trade, gambling-style feedback loops from rapid win-or-lose outcomes, embedded costs in bid-ask spreads that create a negative expected value over time, and behavioural traps such as loss-chasing and overconfidence driven by short-dated expirations.

With a standard call option, profit scales with how far the index moves above the strike price, so a large move produces a larger gain. With a binary option, any finish above the strike pays exactly $100 regardless of magnitude, and any finish below pays $0, meaning the size of the move is entirely irrelevant to the payout.