On 16 June 2026, the ASX 200 logged its fourth consecutive daily gain. That same week, one of the index’s most prominent technology stocks had just shed nearly a fifth of its value in a single session. The tension between those two facts, index resilience and violent stock-level chaos, captures the ASX 200 market wrap for the fortnight spanning roughly 10 to 22 June 2026.

Australian equities were pulled in multiple directions simultaneously. WiseTech Global collapsed 18.4% in one day. Gold and energy names whipsawed as Strait of Hormuz diplomacy repriced the commodity complex. BHP weakened on Chinese demand concerns. The Reserve Bank of Australia held rates steady, supporting bank shares but failing to fully insulate the sector from property-tax policy noise.

What follows unpacks each of those forces, explains why the index held up despite the turbulence, and identifies the watchpoints that will shape ASX performance into the end of the financial year and the second half of 2026.

The index holds its ground despite one of the most turbulent fortnights of 2026

The headline numbers tell an unusually confident story. Consider the index-level milestones from the period:

- A 171-point surge on 12 June 2026, one of the largest single-session gains of the year

- Back-to-back gains of approximately 100 points each on consecutive sessions, reported around 15 June

- Four consecutive sessions of gains running into mid-month

Despite sharp stock-specific shocks and commodity noise, dip-buying appetite in Australian equities remained firm. Demand for exposure at current valuations persisted even as individual names experienced severe dislocations.

That resilience matters, but it can also mislead. A rising index does not mean every position is winning. The fortnight’s internals were far more fractured than the benchmark suggested, and the sector-by-sector picture that follows explains why.

Those sector rotation dynamics were already visible in early June, when institutional capital began closing underweight positions in globally exposed technology and base metals names even as domestic rate-sensitive stocks faced pressure, foreshadowing the fractured internals that defined the mid-June fortnight.

When big ASX news breaks, our subscribers know first

How a single high-multiple stock’s implosion exposed the ASX tech sector’s concentration problem

WiseTech Global (ASX: WTC) lost approximately 18.4% of its market value in a single trading session, making it the standout single-stock event of the fortnight.

The mechanics are familiar to anyone who has held a high-multiple name through a sentiment turn. Elevated expectations sit on top of an already stretched valuation. When a negative catalyst arrives, the gap between price and revised expectations closes violently. Stop-loss orders trigger in sequence, and sentiment contagion spreads to sector peers regardless of whether the underlying issue is shared.

WiseTech’s mid-June plunge fits a pattern that has recurred over the past year. The stock has experienced prior bouts of heavy selling tied to stake-filing headlines and regulatory investigations. Each episode forced risk managers and active fund managers to reassess their tech-sector exposure.

The WiseTech valuation mechanics behind that plunge are worth examining in detail: a stock carrying a trailing PE above 67x entering a period of governance uncertainty and decelerating organic growth at just 7% in 1H26 is precisely the kind of setup where sentiment can reverse faster than fundamentals justify.

The structural insight: when a single marquee name in a narrow sector falls this hard, it moves sector benchmarks and triggers repositioning well beyond its own shareholder register. For ASX technology investors, concentration risk is not theoretical.

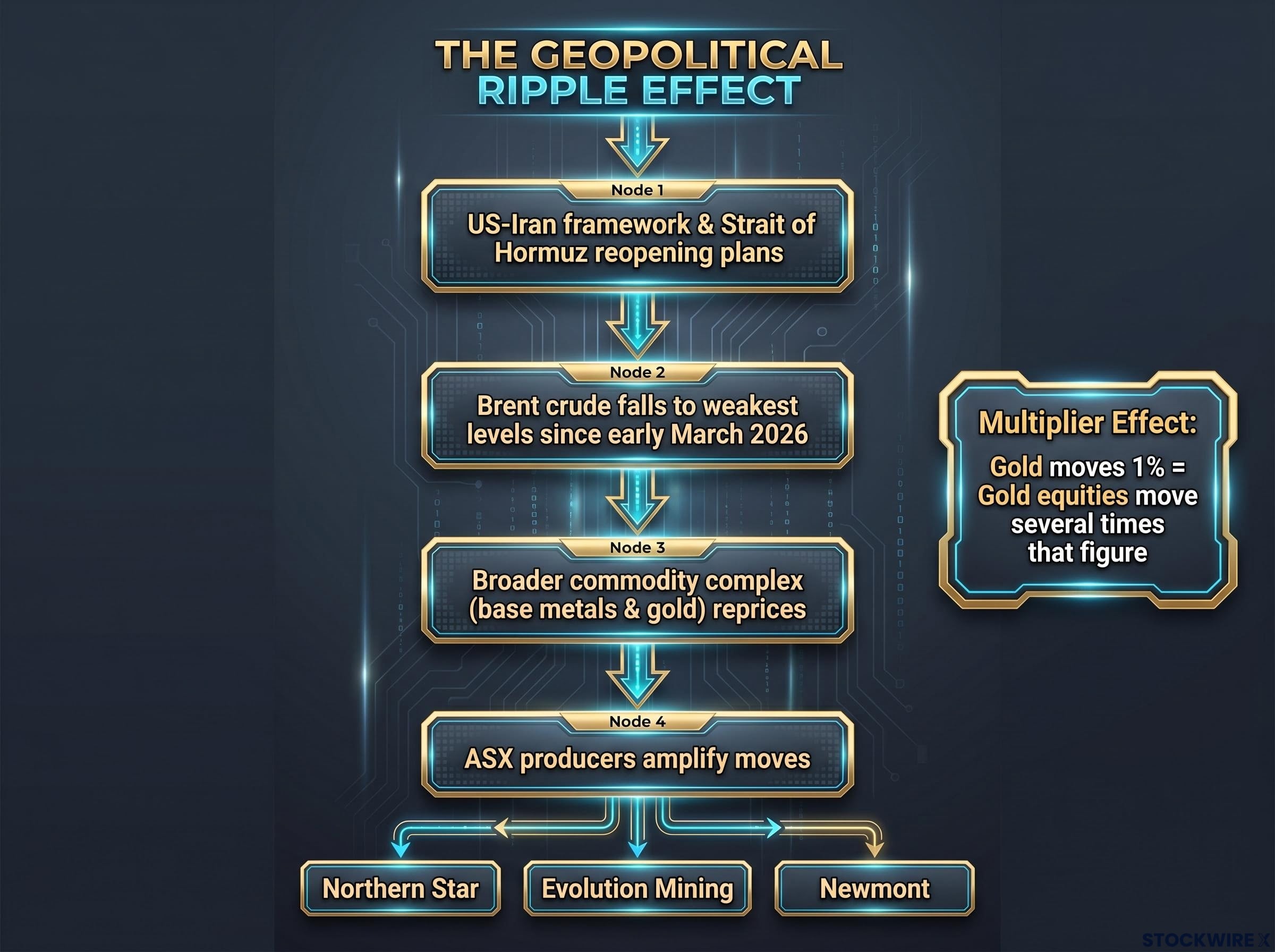

How the Strait of Hormuz reshaped gold, oil, and the commodity complex in a single week

The commodity complex repriced around a single geopolitical catalyst, and the chain of cause and effect moved fast. For readers less familiar with how distant diplomatic developments reach Australian portfolios, the sequence ran as follows:

- A US-Iran framework peace deal and plans to reopen the Strait of Hormuz reduced fears of supply disruption across global energy markets

- Brent crude fell to its weakest levels since early March 2026 as the geopolitical risk premium drained from oil prices

- The broader commodity complex, including base metals and gold, repriced as investors reassessed risk across related markets

- ASX-listed producers in gold, energy, and base metals amplified those moves, producing alternating sessions of sharp gains and heavy losses

The Strait of Hormuz is one of the world’s most significant oil transit corridors. When disruption fears ease, the effect radiates outward from crude oil into refined products, shipping costs, and eventually the earnings expectations of commodity-exposed equities.

Gold equities: amplifiers in both directions

Gold miners structurally amplify the direction of the underlying gold price. When the metal rises 1%, gold equities often move several times that figure; the same holds on the way down. In mid-June, that dynamic produced erratic trading across names including Northern Star, Evolution Mining, and Newmont’s Australian operations, with alternating strong-gain and heavy-loss sessions.

For ASX investors, the broader lesson is structural. Australia’s listed universe is heavily commodities-exposed, meaning geopolitical developments in distant waterways translate directly into domestic portfolio volatility.

BHP, lithium, and the resources complex: heavyweight drag meets a jumpy cycle

BHP’s share price weakness during the fortnight mattered beyond its own shareholders, because its index weight means even a modest percentage decline creates measurable drag on the ASX 200.

ASX 200 concentration risk explains much of why a single large-cap event, whether WiseTech’s 18.4% session decline or a meaningful BHP move on Chinese demand data, can produce index-wide outcomes that feel disproportionate to the number of stocks actually moving.

Two sources of pressure converged. Persistent uncertainty around Chinese steel demand continued to suppress iron ore pricing. At the same time, copper, increasingly central to BHP’s forward strategy, faced its own repricing as investors questioned the pace of the energy transition and the impact of geopolitical supply-chain disruptions.

Lithium stocks added a second layer of resource-sector volatility. The sector remains in a multi-year boom-bust adjustment phase, where earlier surplus supply has produced sharp price swings that now feed directly into large equity moves for ASX lithium producers.

| Factor | BHP | Lithium Sector |

|---|---|---|

| Commodity Exposure | Iron ore, copper | Spodumene, lithium carbonate |

| Key Pressure Point (Mid-June) | Chinese steel demand uncertainty | Boom-bust price cycle volatility |

| Index Weight Implication | Top-3 constituent; moves benchmark | Smaller individually; collective weight rising |

| Forward Watchpoint | Chinese stimulus signals, copper demand | Supply rationalisation, EV adoption pace |

Heading into late June and the end of the financial year, the forward watchpoints for the resources complex include:

- Whether Chinese stimulus signals shift the trajectory for BHP and the bulk miners

- EOFY portfolio repositioning flows and their impact on resource-heavy portfolios

- The copper demand trajectory as energy-transition spending plans firm or falter

Resources collectively represent a large portion of ASX 200 index weight, meaning retail investors with simple index-tracking exposure carry more commodity cycle risk than they may realise.

Banks and CSL: two quieter stories that still moved the needle

The major banks spent the fortnight caught between two simultaneous forces:

- Tailwind: The RBA’s decision to hold the cash rate at 4.35% reduced near-term funding-cost uncertainty and supported net interest margin stability

- Headwind: Renewed property tax reform debate weighed on sentiment, given the sector’s heavy mortgage-book exposure

Bank shares responded positively to the rate hold on a sectoral basis, but did not emerge as clear net winners across the full fortnight. The episode illustrated how quickly competing macro narratives can offset each other for a sector that is sensitive to both monetary policy and fiscal policy signals simultaneously.

CSL offered a quieter counterpoint. The healthcare heavyweight recovered above A$100 per share during the period, reclaiming a price threshold that long-term holders had been watching closely.

For CSL shareholders, the move back above A$100 signalled tentative stabilisation in sentiment toward the ASX’s major global healthcare name, a development that may prove more durable than the noisier swings elsewhere.

Together, banks and CSL represent a substantial slice of the ASX 200. Their combined performance acted as a stabilising counterweight to the volatility in resources and technology, a dynamic relevant to any diversified Australian equity portfolio.

Four themes to watch as the ASX heads into EOFY and the second half of 2026

The fortnight’s action distilled into four unresolved questions, each of which retail investors can track heading into the new financial year:

- WiseTech and tech cohort stabilisation: Can the ASX’s narrow technology sector absorb the positioning shock, or does the sell-off in WTC trigger a broader reassessment of high-multiple holdings?

- Hormuz and US-Iran framework evolution: As diplomatic developments continue, how do gold and energy names adjust to a potentially lower geopolitical risk premium, and what happens if the framework stalls?

- Chinese stimulus signals: Any shift in Beijing’s policy stance will flow directly to BHP, the bulk miners, and lithium producers, making Chinese economic data one of the most consequential inputs for the ASX resources complex.

- RBA forward guidance: How the central bank frames its rate path into the second half of 2026 will shape bank sentiment, mortgage-linked sectors, and the broader appetite for Australian equities among yield-sensitive investors.

Chinese stimulus signals matter to the ASX resources complex not only through commodity pricing but through the portfolio positioning decisions of Australian investors who hold China exposure directly via ETFs, where structural legal constraints and the gap between headline GDP and underlying consumer demand create a far more complicated picture than the 5.0% Q1 2026 growth figure implies.

Commodity-driven volatility is not transitory for the ASX. It is structural, a function of the index’s composition. Yet the four consecutive up sessions and multiple large point-gain days across this fortnight confirmed that demand for Australian equities remains present even amid that volatility.

The ASX 200 enters the new financial year volatile, resilient, and full of unresolved questions

The fortnight’s central tension was real and unresolved: an index that kept climbing even as individual stocks and sectors experienced severe dislocations. That gap between headline performance and stock-level reality is the environment Australian equity investors now operate in.

Position sizing, sector diversification, and a clear understanding of macro and geopolitical linkages are the practical tools for this environment. The structural forces at play, tech concentration, commodity cycles, RBA policy, and global geopolitics, are not fading. They will continue to shape ASX performance through the second half of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.