What PE Ratios Miss: Calculating the Implied Growth Rate

16 hrs ago

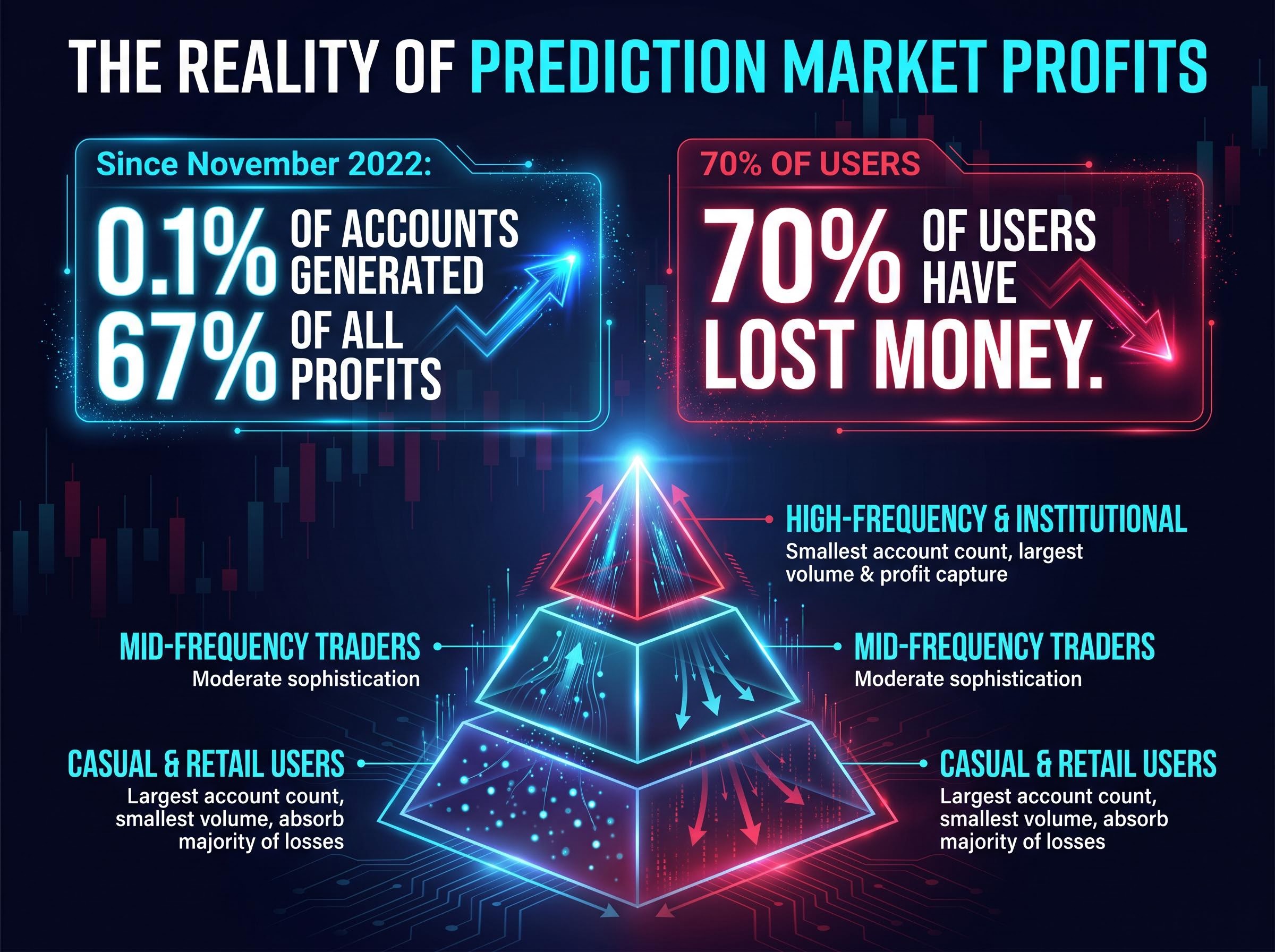

On two of the most widely used prediction market platforms, just 0.1% of accounts have generated 67% of all profits since November 2022. Roughly 70% of users have lost money. Those two figures frame the gap between what prediction markets promise and what most participants actually experience.

Prediction markets have moved from the periphery of finance into mainstream conversation across 2025 and 2026. High-profile election contracts, a unanimous Senate vote banning senators from participating, and Polymarket’s legal relaunch in the United States after a multibillion-dollar acquisition and CFTC approval have all accelerated attention. Monthly trading volumes across the sector now exceed $21 billion, according to TRM Labs.

What follows is a structured walk through exactly how these markets work, what the data says about who profits from them, how accurate their forecasts tend to be, and how to think about them without conflating sentiment tools with investment vehicles.

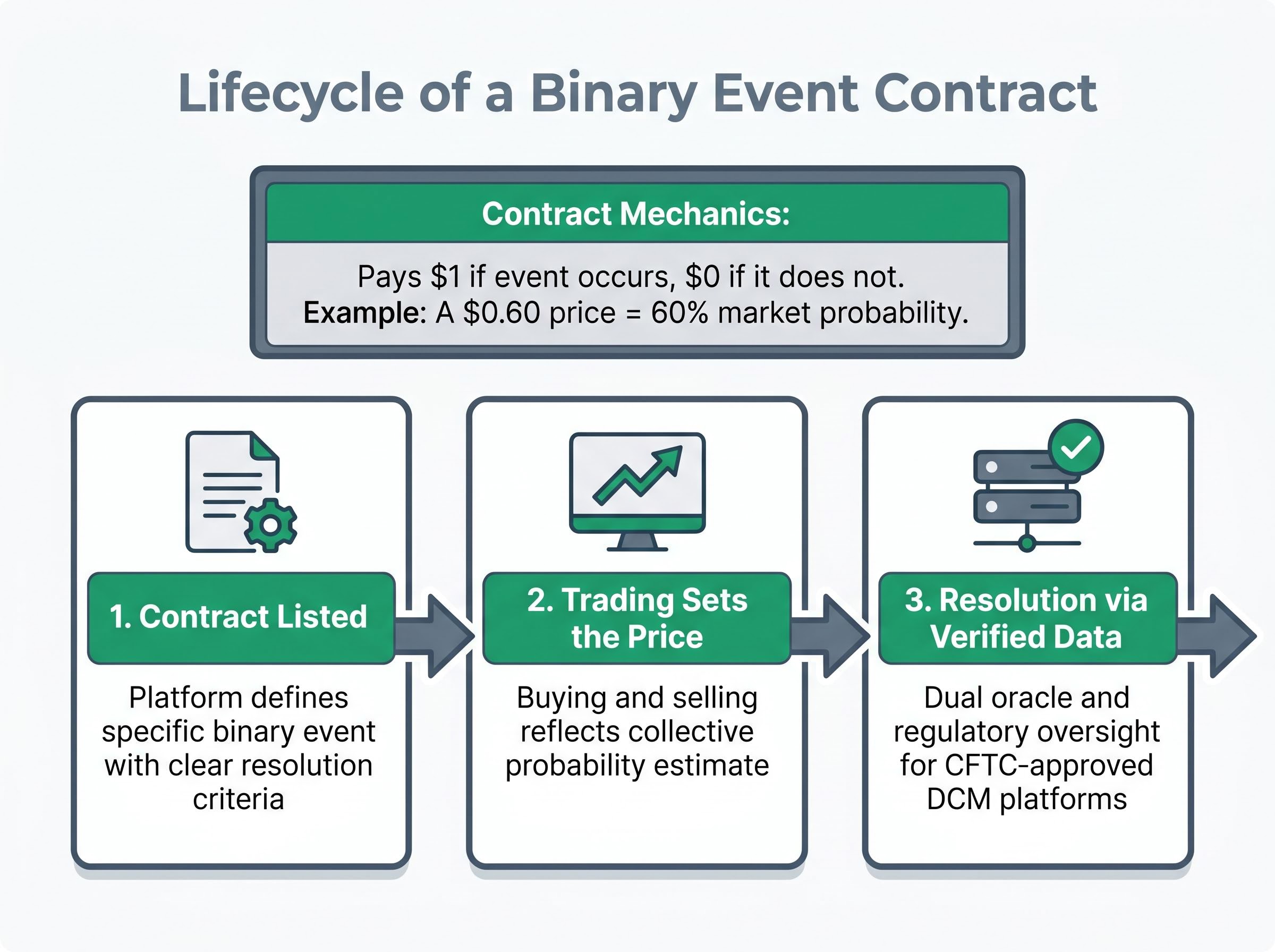

The core instrument is a binary outcome contract. It pays $1 if a specified event occurs and $0 if it does not. The current trading price reflects the collective implied probability assigned by all participants in the market at that moment.

Prices are not set by a centralised oddsmaker. They emerge from aggregate buying and selling pressure among participants, each trading on their own assessment of likelihood. The more participants and the more capital at stake, the more information the price incorporates.

A single contract moves through three stages:

CFTC event contract core principles require DCM-licensed platforms to maintain dual oracle resolution mechanisms and submit to regulatory oversight on market surveillance, the compliance framework that underpins the legitimacy argument proponents make for Kalshi and Polymarket relative to offshore alternatives.

A contract trading at $0.60 means the market assigns 60% probability to that outcome. It does not mean the outcome has a 60% chance of occurring.

That distinction matters. The price reflects what participants are willing to pay, not an objective measure of likelihood. Under CFTC jurisdiction, event contracts are treated as commodity derivatives, not securities. As of 2026, the two primary U.S.-legal retail platforms are Kalshi and Polymarket, with PredictIt remaining active but capped at $850 per user under no-action relief.

For years, prediction markets existed in legal limbo in the United States. The Commodity Futures Trading Commission (CFTC) maintained an enforcement posture that kept platforms either offshore, restricted to academic settings, or operating under narrow no-action letters. The period from 2024 through 2025 reversed that stance.

Polymarket’s path to U.S. legitimacy illustrates the scale of the shift. In July 2025, the platform completed a $112 million acquisition of CFTC-licensed QCX (now QCEX), a designated exchange and clearinghouse. By September 2025, the CFTC granted Polymarket authorisation to relaunch in the U.S. under DCM status. November 2025 brought approval to directly onboard U.S. brokerages and customers, and December 2025 saw no-action relief on recordkeeping requirements extended to multiple platforms.

The capital flowing in confirmed institutional conviction. ICE/NYSE invested $2 billion in Polymarket at an $8 billion valuation in October 2025. By the end of Q1 2026, Polymarket had grown to 1.26 million users, and sector-wide quarterly volume reached $26.2 billion.

The table below summarises the legal standing of the three major U.S. platforms:

| Platform | Legal Status | Key Details | User Limits |

|---|---|---|---|

| Polymarket | Expanded authorisation (DCM via QCEX) | U.S. relaunch September-November 2025; $2B ICE/NYSE investment | No stated cap |

| Kalshi | CFTC-approved DCM since 2024 | Retail event contracts; no major changes post-early 2025 | No stated cap |

| PredictIt | Restricted under no-action relief | Academic-focused; niche positioning | $850 per user |

The Senate responded to the sector’s growth with a unanimous vote banning senators and their staff from participating in prediction markets, a signal that legislators view these platforms as posing conflict-of-interest risks for those with access to non-public policy information.

Separate legislative proposals have targeted insider trading in prediction markets specifically. According to TRM Labs, on-chain analysis documented clusters of coordinated wallet activity spiking volumes ahead of U.S. airstrikes on Iran, providing the evidentiary basis for these proposals. No bills have passed as of May 2026, but the proposals are actively shaping the regulatory environment around what constitutes market manipulation in event contract trading.

The strongest case for prediction markets comes from high-liquidity, public-information events. 2024 U.S. election markets priced outcomes ahead of traditional polling. 2025 Federal Reserve rate cut markets resolved with precision against official data. In both cases, the skin-in-the-game mechanism, where participants backed their views with real capital, produced signals that outperformed conventional surveys.

TRM Labs reported in March 2026 that prediction markets excel as real-time indicators for geopolitics and macroeconomics, outperforming traditional forecasts in high-liquidity conditions. Wedbush noted in January 2026 that high-liquidity event markets demonstrate signalling efficiency comparable to established financial instruments.

Geopolitical event pricing in liquid markets involves probability-weighted adjustments to expected outcomes rather than proportional headline reactions, a dynamic that applies to equity markets and prediction markets alike, though the two instruments surface that information through fundamentally different mechanisms.

The record becomes considerably less impressive under different conditions.

Conditions where prediction markets tend to be reliable:

Conditions that undermine reliability:

Fisher Investments has observed that how people feel and how people behave can diverge significantly. Prediction markets capture expectations, not guaranteed behaviour.

That observation matters. The skin-in-the-game argument assumes participants are betting on what they believe will happen based on superior analysis. In practice, many are betting on what they hope will happen, or what they perceive the consensus to be. The signal is real in some conditions and unreliable in others, and knowing which conditions apply is what separates useful information from noise.

Across two major platforms, 0.1% of accounts generated 67% of all profits since November 2022. Approximately 70% of users have experienced net financial losses.

Retail loss rates in speculative instruments follow a strikingly consistent pattern across asset classes: between 74% and 89% of retail CFD accounts lose money according to ESMA data from Q1 2026, a figure that sits directly alongside the 70% loss rate documented across prediction market platforms.

Just 0.1% of accounts generated 67% of all profits since November 2022. Approximately 70% of users have lost money.

The concentration is structural, not accidental. Prediction market participants sort into three broad cohorts:

The pattern is not unique to prediction markets. Early retail options trading and perpetual futures markets displayed similar profit concentration dynamics before those markets matured. FalconX warned in February 2026 that prediction markets carry speculative bubble risks akin to early perpetual futures environments.

Wedbush’s January 2026 analysis noted that culture markets in particular blur the line between investing and gambling for retail participants. When entertainment and speculation overlap, the informational signal the market generates may be accurate in aggregate while the typical participant’s experience remains a net loss.

Market-level accuracy and individual expected outcomes are two entirely different questions. The market can be right. Most participants can still lose.

Prediction markets represent the latest entry in a long list of retail trading traps where the market-level mechanism functions as designed while the typical participant loses money, a dynamic that runs from short selling through leveraged derivatives to event contracts.

The distinction that matters is between monitoring and participating. A prediction market price carries genuine informational content in specific conditions. Whether that information justifies direct participation is a separate question entirely.

Fisher Investments identifies a quality worth noting: financial commitment creates stronger conviction signals than survey responses. When participants put capital behind their expectations, the resulting price aggregates conviction-weighted views rather than costless opinions. That is a real advantage over traditional polling and sentiment surveys.

TRM Labs frames institutional bets, including ICE’s $2 billion Polymarket investment, as reflecting hedging value over pure speculation. Institutional participants use prediction market data as one input among many, a structurally different relationship than the retail user treating the same platform as a trading venue.

Wedbush’s comparison of prediction market platforms to Robinhood and IBKR as challengers for event-based finance highlights where the product category sits: at the boundary between financial information and entertainment. Regulatory maturation under CFTC oversight has made these platforms more accessible. It has not changed the underlying risk profile for retail traders.

The gambling-versus-investing framing misses the point. Prediction markets are real-time collective expectation instruments. In high-liquidity, public-information conditions, they produce forecasting signals that outperform conventional alternatives. They also operate as a net-loss environment for approximately 70% of participants, with profits concentrated among a fraction of a percent of accounts.

CFTC accommodation and DCM status have made these platforms more legitimate. They have not made them less risky for retail traders. The unanimous Senate vote banning senators from participating acknowledged, at the legislative level, that even those with informational advantages recognised the conflict-of-interest risks these markets create.

With Q1 2026 volumes reaching $26.2 billion, prediction markets are now large enough to warrant serious understanding. The value for most readers lies in using prediction market prices as one input within a broader analytical framework, not as a trading vehicle. Unless a participant possesses the sophistication and speed to compete with the 0.1% capturing the majority of profits, direct trading in these markets carries a demonstrated probability of loss.

Prediction markets are better understood as sentiment instruments than as investment vehicles. Their prices are worth reading. For most participants, they are not worth trading.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Prediction markets are platforms where participants buy and sell binary outcome contracts that pay $1 if a specified event occurs and $0 if it does not, with the trading price reflecting the collective implied probability assigned by all participants at any given moment.

Yes, as of 2025-2026 two major U.S. platforms operate legally: Kalshi holds CFTC-approved Designated Contract Market status, and Polymarket relaunched in the U.S. under DCM status via its acquisition of QCEX, with both subject to regulatory oversight on market surveillance.

Approximately 70% of users across two major prediction market platforms have experienced net financial losses since November 2022, with just 0.1% of accounts generating 67% of all profits.

Prediction markets tend to be most accurate in high-liquidity, public-information conditions, such as U.S. elections and Federal Reserve rate decisions, but their reliability breaks down in low-volume markets, culture events, or situations involving insider information or coordinated trading.

Investors can monitor high-liquidity prediction market prices as one real-time data point alongside conventional analysis, using price shifts as signals worth investigating further rather than conclusions to act on directly, without needing to participate as active traders.