ASX 200 Posts Four-Day Run as WiseTech Sheds 18% in One Session

1 hr ago

For the first time in South Korean corporate history, Samsung Electronics is not the most valuable company in the country. On 22 June 2026, SK Hynix displaced it. SK Hynix shares climbed 3.7% on the session, pushing its market capitalisation to approximately 2,082 trillion won. Samsung fell 1.4% on the same day, slipping below that threshold. The crossing was not a single-session quirk; it was the culmination of a multi-month convergence driven by one product category: high-bandwidth memory (HBM) chips, the components that feed data to the processors powering artificial intelligence. What follows is a breakdown of what caused the overtaking, what HBM is and why it commands premium margins, what the financial divergence between the two companies reveals, and what the milestone means for investors tracking the AI semiconductor supply chain.

Samsung has been South Korea’s most valuable listed company for decades. No domestic rival had come close to displacing it. That changed today.

SK Hynix shares rose 3.7% on 22 June 2026, lifting the chipmaker’s market capitalisation to approximately 2,082 trillion won. Samsung fell 1.4% in the same session, and the two lines crossed. The overtaking had been building for weeks: by early May 2026, SK Hynix had already reached approximately 93% of Samsung’s market cap, narrowing a gap that had once seemed structural.

Anchor figure: SK Hynix market capitalisation at the point of crossing: approximately 2,082 trillion won.

The speed of the convergence sits within a broader repricing of the global memory sector. All three major memory producers crossed the $1 trillion market capitalisation threshold within a three-week window:

The leaderboard change is not a short-term swing. It reflects how rapidly AI-driven demand has reshuffled valuations within a single sector.

Samsung’s trillion-dollar milestone, reached on 6 May 2026, was itself a product of the same HBM-driven repricing wave, with the company’s memory division recording approximately 55% year-on-year revenue growth in Q1 2026 even as its HBM market share sat well below SK Hynix’s position.

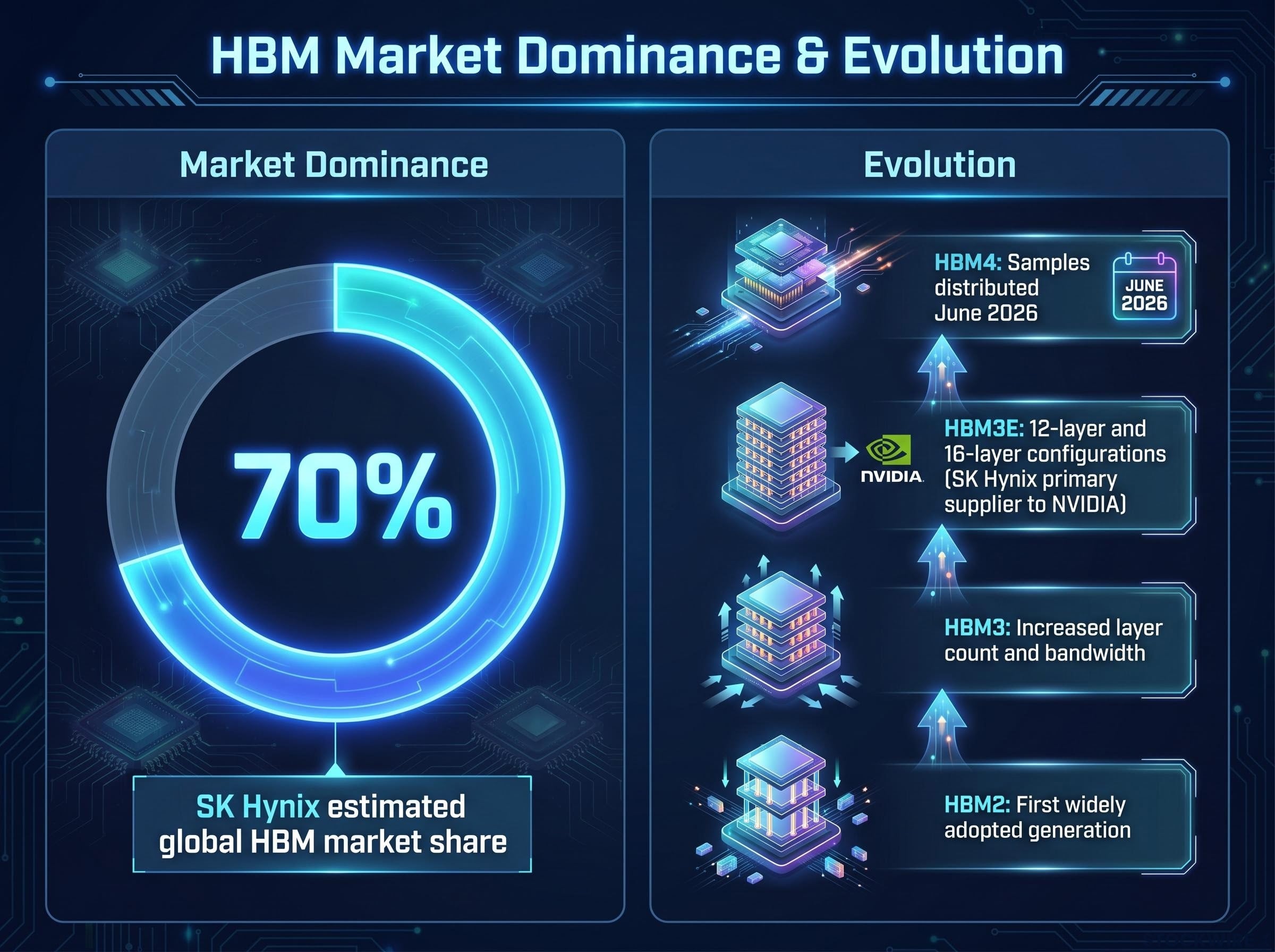

AI systems need processors to compute, but they need memory to feed those processors data. HBM, or high-bandwidth memory, is the category of memory chip designed specifically for that feeding role. It consists of multiple layers of DRAM dies stacked vertically and connected by through-silicon vias (tiny vertical channels that pass data between layers), delivering dramatically higher bandwidth than conventional memory modules.

The product has evolved through successive generations, each increasing stack height and data throughput:

AI training and inference workloads are memory-bandwidth-constrained, meaning the speed at which a GPU can access data limits overall system performance. This makes HBM the binding constraint in the AI accelerator stack, not a commodity input but the component that determines how fast the entire system runs. That bottleneck position is what gives HBM its premium margins and what gives its leading supplier, SK Hynix, the valuation the market now assigns it.

The market capitalisation crossing reflects a profit divergence that was already visible in the 2025 results. SK Hynix recorded a full-year 2025 operating profit of approximately 47.2 trillion won (a record), while Samsung’s semiconductor division reported approximately 43.6 trillion won over the same period, according to research-layer estimates. It marked the first time SK Hynix had outearned Samsung’s chip arm on an annual basis.

| Metric | SK Hynix | Samsung (Semiconductor Division) |

|---|---|---|

| 2025 operating profit | ~47.2 trillion won (est.) | ~43.6 trillion won (est.) |

| Primary memory product focus | HBM (high-margin, AI-optimised) | Broader DRAM and NAND mix |

| HBM generation leadership | HBM3E primary supplier; HBM4 samples distributed | Working to close HBM technology gap |

The structural reason for the gap is product mix. SK Hynix’s revenue is heavily weighted toward HBM, which carries materially higher margins than the commodity DRAM and NAND that compose a larger share of Samsung’s semiconductor revenue. Research-layer estimates indicate SK Hynix’s DRAM revenue share reached 36.2% globally, exceeding Samsung’s share in recent periods. Samsung has been working to close the HBM technology gap, but has not yet recaptured design wins at the leading edge of the product cycle.

The profit comparison confirms what the share prices are pricing in: technology leadership and product mix, not production volume, now determine where margin flows in the memory industry.

The SK Hynix overtaking is part of a broader pattern. All three major global memory producers crossed the $1 trillion market capitalisation threshold within weeks of each other in May 2026:

South Korea now hosts multiple $1 trillion companies in a single sector, a first outside the United States. The concentration reflects the country’s structural position in global AI infrastructure supply chains, where memory production is geographically concentrated in ways that logic chip fabrication is not.

Market context: The KOSPI index is up an estimated 95% year-to-date in 2026, following an estimated 76% gain in 2025, with memory stocks leading the rally (research-layer estimate).

The simultaneous trillion-dollar milestone across all three memory majors signals that the market views HBM demand as a sustained structural condition rather than a speculative spike. Hyperscaler capital expenditure growth has created a demand floor for HBM that investors are pricing as durable, with direct implications for how memory exposure is categorised in AI-focused portfolios.

SK Hynix holds an estimated 70% of the global HBM market (research-layer estimate, not independently confirmed). The question now is whether that lead extends or narrows. Four variables will determine the answer:

HBM4 supplier qualifications for NVIDIA’s Vera Rubin platform were confirmed in early June 2026, with all three major memory producers clearing certification simultaneously for the first time, though SK Hynix is estimated to hold 60-70% of volume allocations, reflecting its earlier entry into the qualification process.

Samsung’s semiconductor division has been working to close the HBM technology gap, but no specific timeline for a leading-edge qualification win has been confirmed in verified reporting. If Samsung secures a major HBM design win, particularly with NVIDIA, the market share and margin dynamics that underpin SK Hynix’s valuation premium could compress. Conversely, if SK Hynix extends its lead into HBM4 production at scale, the gap could widen further.

Investors who monitor HBM product cycle transitions, Samsung’s qualification progress, and hyperscaler capital expenditure guidance will have earlier signals of whether SK Hynix’s premium is expanding or compressing.

The displacement of Samsung by SK Hynix is not primarily a story about two Korean companies. It is a story about how AI infrastructure spending is restructuring where margin and valuation accumulate across the semiconductor industry. The companies positioned at the binding constraints of the AI buildout, whether in memory, interconnects, or advanced packaging, are the companies attracting premium valuations.

Semiconductor supplier profitability relative to the hyperscalers funding the AI buildout has become one of the defining financial dynamics of 2026, with Goldman Sachs projecting that major hyperscalers will spend approximately $770 billion on capex, equivalent to roughly 100% of their operating cash flow, while the companies supplying memory and packaging components capture structurally superior margins.

Value creation arc: SK Telecom acquired SK Hynix in 2012 for approximately $3 billion (research-layer estimate). On 22 June 2026, SK Hynix’s market capitalisation reached approximately 2,082 trillion won, representing one of the largest corporate value creation trajectories in recent semiconductor history.

That arc, from mid-tier memory producer to trillion-dollar AI infrastructure supplier in 14 years, illustrates how component specialisation compounds over long cycles when it aligns with a durable demand shift. For investors evaluating the AI supply chain, the SK Hynix story offers a framework: the next decade’s outsized returns may come not from the companies building AI models, but from the companies supplying the components those models cannot run without.

For investors who want to act on Korean semiconductor exposure, our dedicated guide to investing in South Korean stocks covers the practical mechanics of accessing KOSPI-listed names via international brokers and MSCI Korea ETFs, the KRX daily price limit rules that can affect exit timing, and the Corporate Value-Up reform programme that is reshaping governance and payout structures across Korean blue chips.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial figures cited from research-layer estimates have not been independently confirmed and are subject to revision.

High-bandwidth memory (HBM) is a type of chip made from multiple layers of DRAM stacked vertically and connected by tiny vertical channels, delivering far greater data throughput than conventional memory. AI training and inference workloads are memory-bandwidth-constrained, making HBM the component that determines how fast the entire system runs and giving its leading suppliers premium pricing power.

SK Hynix overtook Samsung because its revenue and profits are heavily weighted toward HBM chips, which carry materially higher margins than the broader DRAM and NAND mix that makes up a larger share of Samsung's semiconductor revenue. SK Hynix's role as NVIDIA's primary HBM3E supplier and its early distribution of HBM4 samples have reinforced its technology leadership position in the eyes of investors.

SK Hynix holds an estimated 70% of the global HBM market according to research-layer estimates, and is reported to hold 60-70% of volume allocations for NVIDIA's next-generation Vera Rubin platform after all three major memory producers cleared HBM4 certification simultaneously in early June 2026.

International investors can access KOSPI-listed names such as SK Hynix through international brokers that offer direct Korean exchange access or via MSCI Korea ETFs, though investors should be aware of KRX daily price limit rules that can affect exit timing and the ongoing Corporate Value-Up reform programme reshaping governance across Korean blue chips.

The key risks include Samsung securing a major HBM design win with NVIDIA or another accelerator customer, which would shift market share dynamics, and SK Hynix's concentrated commercial dependency on NVIDIA as a single customer. Micron's HBM capacity expansion also affects overall market supply and pricing across the sector.