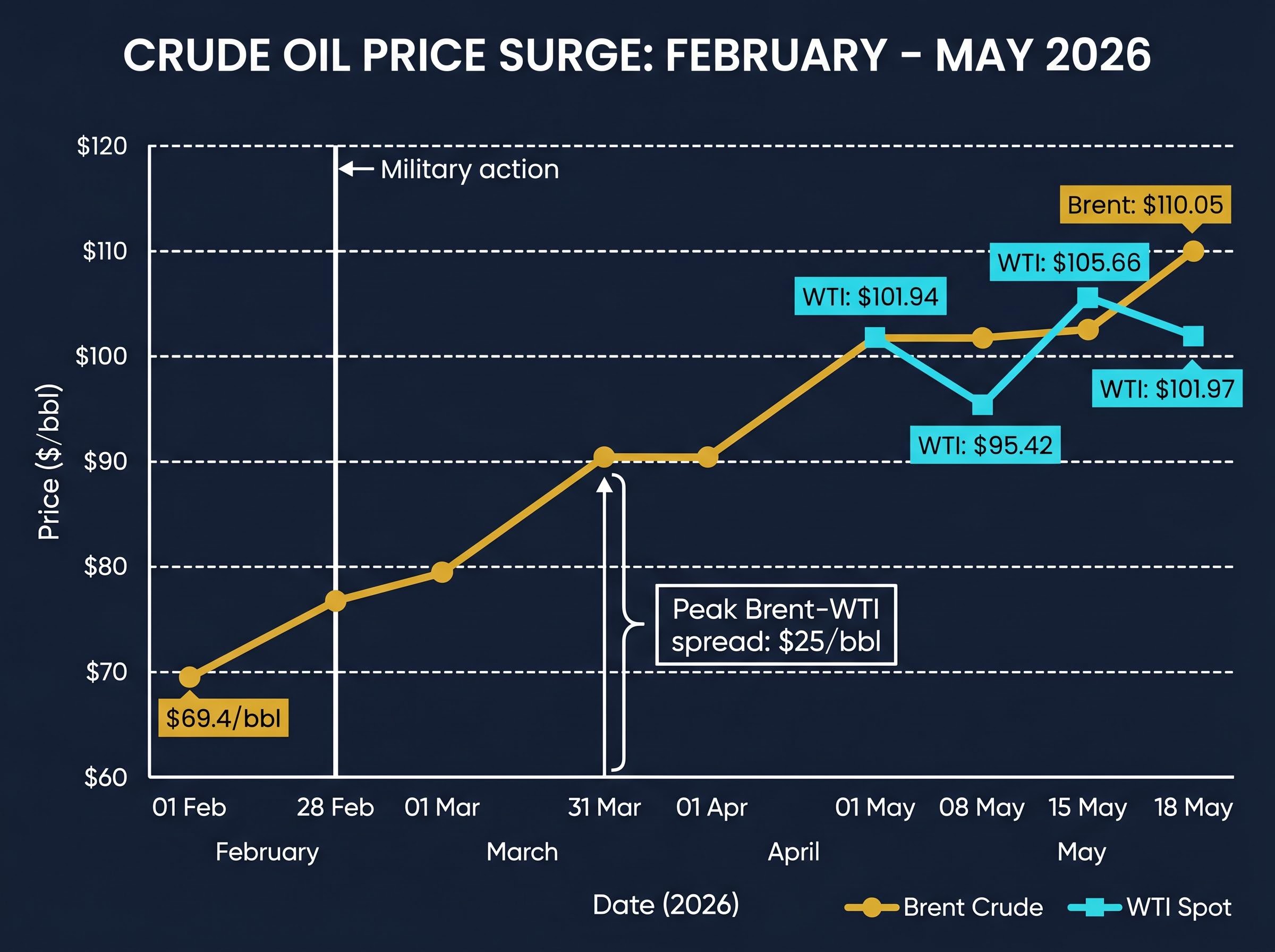

Brent crude sat at $69.4 per barrel in February 2026. By 18 May, it was trading above $110. One waterway, and one military action, accounts for most of that gap.

On 28 February 2026, military action in the Middle East triggered what the U.S. Energy Information Administration (EIA) has since characterised as a de facto closure of the Strait of Hormuz, the narrow passage through which approximately one-fifth of the world’s oil supply flows. The closure has persisted for nearly three months, producing one of the sharpest crude oil price surges in recent history. What follows is an analysis of the geopolitical mechanics behind the disruption, why the Strait of Hormuz holds singular leverage over global energy markets, what the verified price data reveals about supply shock dynamics, and what investors and consumers should understand about their current exposure to sustained elevated energy prices.

Why a single waterway can move global oil markets by 57%

The Strait of Hormuz is not merely an important shipping lane. It is structurally irreplaceable. No other maritime route, pipeline network, or overland alternative can absorb the volume of crude that transits this passage on a daily basis. That structural fact is what converts a geographically confined military action into a global commodity shock.

Three features explain why no workaround exists:

- Volume share: Approximately 20% of global oil supply passes through the strait, according to reporting by Investing.com on 18 May 2026. No other single chokepoint carries this proportion of global crude flows.

- Absence of bypass alternatives: Most Gulf exporters lack pipeline infrastructure capable of rerouting significant volumes overland. The strait is the exit.

- Iranian geographic control: The waterway runs along the Iranian coast, giving Iran asymmetric interdiction capability that no other regional actor can neutralise quickly.

EIA, Today in Energy (7 April 2026): The EIA characterised the situation as a “de facto closure of the Strait of Hormuz” following military action on 28 February 2026.

The arithmetic is direct. Brent crude averaged $69.4 per barrel in February 2026, according to INSEE data published on 27 March 2026. By 18 May, Brent had risen above $110 per barrel, a roughly 57% increase in approximately 11 weeks. The price move is not disproportionate. It is the mechanical consequence of removing one-fifth of global supply from reliable transit.

When big ASX news breaks, our subscribers know first

From $70 to $110: tracing the price mechanics of the supply shock

The headline figure, 57%, tells part of the story. The Brent-WTI spread tells the rest.

Following the 28 February military action and the subsequent de facto Hormuz closure, crude prices climbed sharply through Q1 2026. But the two global benchmarks did not climb in parallel. According to the EIA’s 7 April 2026 report, the Brent-WTI spread peaked at $25 per barrel on 31 March 2026 and averaged $11 per barrel across March. That gap is the analytical signal: the disruption was concentrated in seaborne, internationally traded crude. Brent, the global waterborne benchmark, absorbed the full force of the supply shock. WTI, anchored by strong U.S. crude inventories and plans to release crude from the Strategic Petroleum Reserve (SPR), rose more slowly.

The SPR release plans, noted by the EIA as a price-moderating factor during Q1, helped cap WTI’s ascent. But they did not stabilise it. WTI spot data from FedPrimeRate.com shows the benchmark remained volatile through mid-May: $101.94 on 1 May, a dip to $95.42 on 8 May, and a rebound to $105.66 by 15 May. That sequence is not a market finding equilibrium. It is a market repricing risk week by week.

| Date | Brent (approx.) | WTI Spot | Notable Development |

|---|---|---|---|

| February 2026 | $69.4/bbl | ~$69-70/bbl | Pre-conflict baseline (INSEE) |

| 31 March 2026 | Peak spread | Brent-WTI spread: $25/bbl | Widest Brent-WTI gap; Q1 surge peak (EIA) |

| 1 May 2026 | ~$106-110/bbl | $101.94 | Elevated prices persist into Q2 |

| 8 May 2026 | ~$106-110/bbl | $95.42 | Mid-month dip; market uncertainty |

| 15 May 2026 | ~$106-110/bbl | $105.66 | Sharp rebound; volatility continues |

| 18 May 2026 | $110.05 (+0.72%) | $101.97 | Escalation signals over preceding weekend |

As of 18 May 2026, Brent stood at $110.05 (up approximately +0.72%) and WTI at $101.97, according to Investing.com. The spread has narrowed from its March peak, but the price level has not. The disruption is ongoing.

The Strait of Hormuz: how a chokepoint becomes a geopolitical weapon

A maritime chokepoint is a narrow passage through which shipping traffic must transit because no practical alternative route exists. Several such passages exist globally, including the Suez Canal and the Malacca Strait. The Strait of Hormuz differs from all of them in one respect: the sheer volume of oil that depends on it, combined with the fact that a single state controls the coastline on one side.

Iran’s geographic position along the strait’s northern shore gives it asymmetric interdiction capability. This has been a focal point of geopolitical risk across multiple decades of Iran-U.S. tensions. But the current conflict has moved the risk from theoretical to operational.

How de facto closure works without a formal blockade

The EIA’s use of the phrase “de facto closure” in its 7 April 2026 report is analytically significant. It describes a market reality, tanker traffic disrupted, without requiring confirmation of a formal naval blockade. The mechanism operates in three stages:

The EIA’s ‘de facto closure’ framing captures the economic reality, but the physical picture is more layered: a triple lock on Hormuz transit, combining U.S. naval blockade operations, Iranian toll enforcement on non-U.S. and non-Israeli vessels, and the near-total withdrawal of commercial war-risk insurance coverage, has made the strait commercially impassable through at least three independent mechanisms simultaneously.

- Threat of interdiction raises war risk insurance premiums. When underwriters price the possibility of missile strikes, drone attacks, or mine contact into tanker insurance, premiums escalate sharply.

- Elevated insurance costs make transits commercially unviable. Tanker operators face a cost calculation: if the premium to transit the strait exceeds the margin on the cargo, the route is effectively closed by economics rather than ordnance.

- Tanker diversion or anchoring creates effective supply reduction. Even without a single vessel being struck, the reallocation of tanker traffic away from the strait removes barrels from the market as surely as a physical obstruction would.

The EIA’s characterisation of “de facto closure” is the primary-source evidence that this mechanism has operated in the current conflict. Readers who understand the distinction will not misread a partial diplomatic thaw as a return to normal commercial shipping. The insurance market, not the military situation alone, determines when the route reopens in practice.

Escalation signals the market cannot ignore

The 0.72% rise in Brent on 18 May looks modest in isolation. It is less modest in context.

Over the weekend preceding 18 May 2026, three specific events signalled that the conflict’s geographic reach is expanding rather than contracting:

- A drone strike targeted a UAE nuclear power plant, according to Investing.com reporting on 18 May 2026

- Saudi Arabia intercepted three separate drones during the same period

- U.S. President Trump publicly called on Iran to move toward a durable peace agreement, a statement that implicitly confirms an existing ceasefire is under strain rather than holding

U.S. President Trump publicly called on Iran to move quickly toward a durable peace agreement, signalling that the current ceasefire framework is not operating as intended.

The drone incidents are particularly significant because they extend the conflict’s footprint beyond the strait itself. A strike on a nuclear facility and multiple interceptions over Saudi territory indicate that the threat environment has broadened. The Brent price movement on 18 May should be read as a market assessment of conflict trajectory, not a routine daily fluctuation. The question has shifted from “how high has oil gone” to “whether the conditions for sustained elevation remain intact.”

The cross-asset repricing from the blockade extends well beyond crude futures: ECB Chief Economist Philip Lane explicitly linked the oil shock to potential rate hikes on 13 May 2026, Asian equity markets registered broad declines on 18 May with the Hang Seng falling approximately 1.7% and the ASX 200 down approximately 1.6%, and China’s April retail sales growth of just 0.2% year-on-year introduced a stagflationary undercurrent that compounds the supply-driven inflation the crude price itself is generating.

What the price surge means for consumers, businesses, and economies

$110 Brent does not stay inside commodity trading screens. It moves through supply chains.

The transmission channels from elevated crude prices to consumer-facing costs are well established. A 57% increase in Brent, and a roughly 45% increase in WTI (from approximately $70 in February to $101.97 on 18 May), flows through the economy via four primary pathways:

- Retail fuel prices: Pump prices track crude with a short lag, compressing household transport budgets

- Airline and logistics surcharges: Fuel represents a significant share of operating costs for carriers; sustained crude above $100 typically triggers surcharge adjustments

- Industrial input costs: Energy-intensive manufacturing, petrochemicals, and heating face margin pressure that is either absorbed or passed through

- Central bank tightening risk: Prolonged elevated energy costs generate persistent inflation pressure that complicates monetary policy positioning

The inflationary dimension compounds the direct cost effects. Market concern that prolonged elevated energy costs could generate inflationary pressures sufficient to prompt central bank tightening was reflected on 18 May 2026 in higher bond yields across global sovereign debt markets, according to Investing.com.

The NBER research on oil price shocks, led by James D. Hamilton, documents the consistent historical linkage between crude supply disruptions of this magnitude and downstream recessionary pressure, a pattern that gives the current transmission channels from $110 Brent to consumer-facing costs their full macroeconomic weight.

Oil-import-dependent economies face a further layer of exposure. Crude is priced in U.S. dollars. A weaker domestic currency against the dollar amplifies the domestic price of every imported barrel, making the shock asymmetric across geographies. Economies running current account deficits funded by energy imports are most exposed.

The structural tension beneath the price: surplus fundamentals vs. geopolitical shock

J.P. Morgan Global Research projects Brent crude averaging approximately $60 per barrel for the full year of 2026. The bank characterises this as a bearish forecast grounded in soft supply-demand fundamentals: global oil demand is expected to grow by 0.9 million barrels per day in 2026, but supply growth outpaces that figure. J.P. Morgan states that “voluntary and involuntary production cuts will be needed to prevent excessive inventory accumulation” to stabilise prices around the $60 level.

That forecast is not incorrect. It is the pre-disruption structural baseline that the Hormuz closure has overridden.

| Structural Baseline (J.P. Morgan) | Current Geopolitical Reality (18 May 2026) |

|---|---|

| Brent forecast: ~$60/bbl average | Brent spot: $110.05/bbl (~83% above forecast) |

| Supply-demand: Global surplus expected | ~20% of global supply in disrupted transit |

| Key risk: Overproduction requiring cuts | Key risk: Sustained Hormuz closure |

| Policy implication: Production discipline | Policy implication: Emergency supply response, inflation management |

The $50 gap between J.P. Morgan’s structural view and the current spot price is, in effect, the quantified cost of the Hormuz disruption. Two competing forces now sit in direct tension: an underlying market that the bank’s analysts see as oversupplied, and an acute geopolitical constraint that has removed the waterway through which that surplus would normally reach buyers. How and when that tension resolves depends on a single variable: whether the Strait of Hormuz returns to normal commercial operation, and over what timeline. That variable remains unresolved.

The Hormuz premium will not unwind until the conflict does

Rarely can the difference between a $60 oil market and a $110 oil market be traced to a single identifiable mechanism with this degree of precision. The $40-50 premium embedded in current Brent above J.P. Morgan’s structural baseline is a Hormuz premium. It will persist as long as the strait remains commercially impaired.

That creates a two-sided risk for energy market participants. A rapid diplomatic resolution, one that restores normal tanker traffic and normalises war risk insurance premiums, could produce a sharp downside correction toward levels closer to J.P. Morgan’s structural view. Further escalation, of the kind signalled by the weekend’s drone incidents and the strain on the existing ceasefire, could push Brent materially higher.

The Hormuz risk premium has a structural persistence that market participants frequently underestimate: even in a best-case diplomatic resolution, VLCC daily hire rates tracking approximately $110,000 per day and the IEA’s two-year supply chain recovery timeline mean the premium decompresses gradually rather than snapping back to the $60 structural baseline J.P. Morgan’s model reflects.

The single clearest analytical frame for tracking resolution is commercial traffic through the Strait of Hormuz. When tanker transits normalise and insurance premiums fall, the Hormuz premium unwinds. Until then, it does not.

EIA and International Energy Agency (IEA) energy market updates, alongside diplomatic developments relating to the Iran-U.S. ceasefire, remain the primary indicators for how this situation develops. Monitoring those sources provides the most direct signal of whether $110 oil is a temporary ceiling or a new floor.

Investors who need to model the duration of elevated prices beyond the immediate conflict will find our full explainer on the 2027 supply normalisation timeline useful: it covers Saudi Aramco CEO Amin Nasser’s warning that supply normalisation may extend into 2027, the 880 million net barrel supply deficit accumulated since the closure began, and why the 400 million barrel IEA emergency release covers only approximately four weeks of the weekly shortfall created by the strait’s closure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.