Why AI Makes Markets Safer Daily but Riskier in a Crisis

1 hr ago

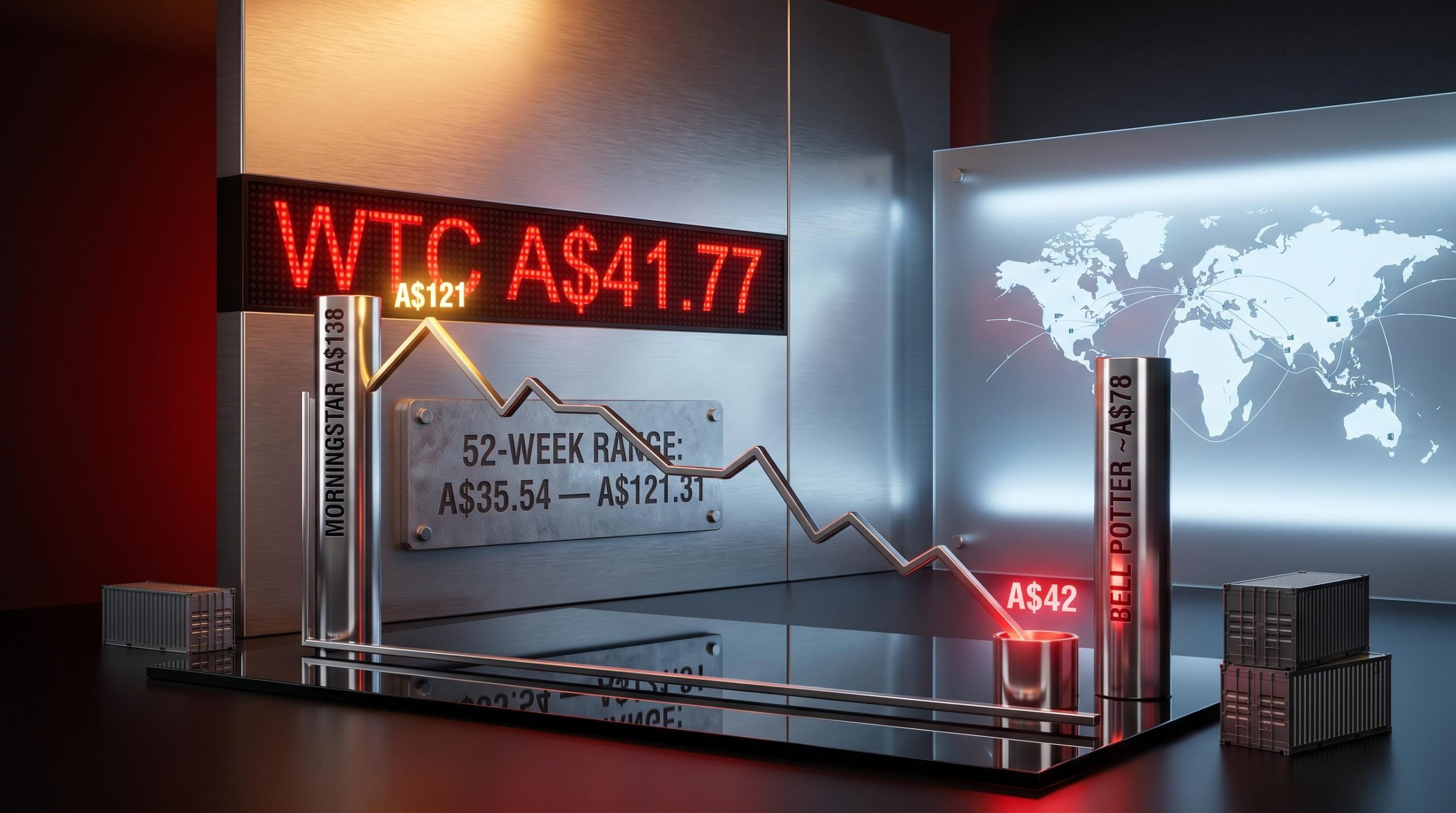

WiseTech Global shares have fallen approximately 58% from their January 2026 highs to trade near A$42 in May 2026. The 52-week range of A$35.54 to A$121.31 tells the story in two numbers: a peak that priced in compounding dominance, and a trough that prices in something close to distress. The question facing ASX-focused investors is whether that collapse reflects a business in genuine trouble or a temporarily mispriced monopoly.

Two distinct forces drove the selloff: a governance crisis originating in 2024 involving co-founder Richard White, and the margin compression triggered by the August 2025 acquisition of e2open. A sector-wide software selloff compounded both. The result is a share price that Morningstar now assesses as trading at a 70% discount to fair value, while Bell Potter’s more conservative target still implies roughly 70% upside from current levels.

What follows unpacks the case for and against treating WiseTech at current prices as a buying opportunity, examining the organic business quality, the acquisition overhang, the governance risk, and the valuation spread between analyst targets.

No single cause explains the full magnitude of WiseTech Global’s decline. Three compounding forces, each operating on a different timeline, drove the stock from its January 2026 highs to its current price near A$42, a one-year decline of 56.06%.

The three catalysts, in sequence:

The sector-wide software selloff that amplified WiseTech’s company-specific pressures sits within a broader global software repricing, one that saw approximately $2 trillion in market capitalisation erased from US software names in early 2026 as institutional capital rotated toward AI-native infrastructure and consumption-based pricing models.

“Down 45% year to date, WiseTech’s ongoing governance concerns and the sector-wide software selloff has created a compelling opportunity.” — Morningstar, 16 April 2026

Separating these causes matters because each carries a different recovery timeline. Governance risk has been partially restructured. Integration costs are temporary by nature. Sector sentiment is cyclical. Investors who conflate all three into a single “broken business” narrative may be pricing in permanent impairment where the evidence points to temporary dislocation.

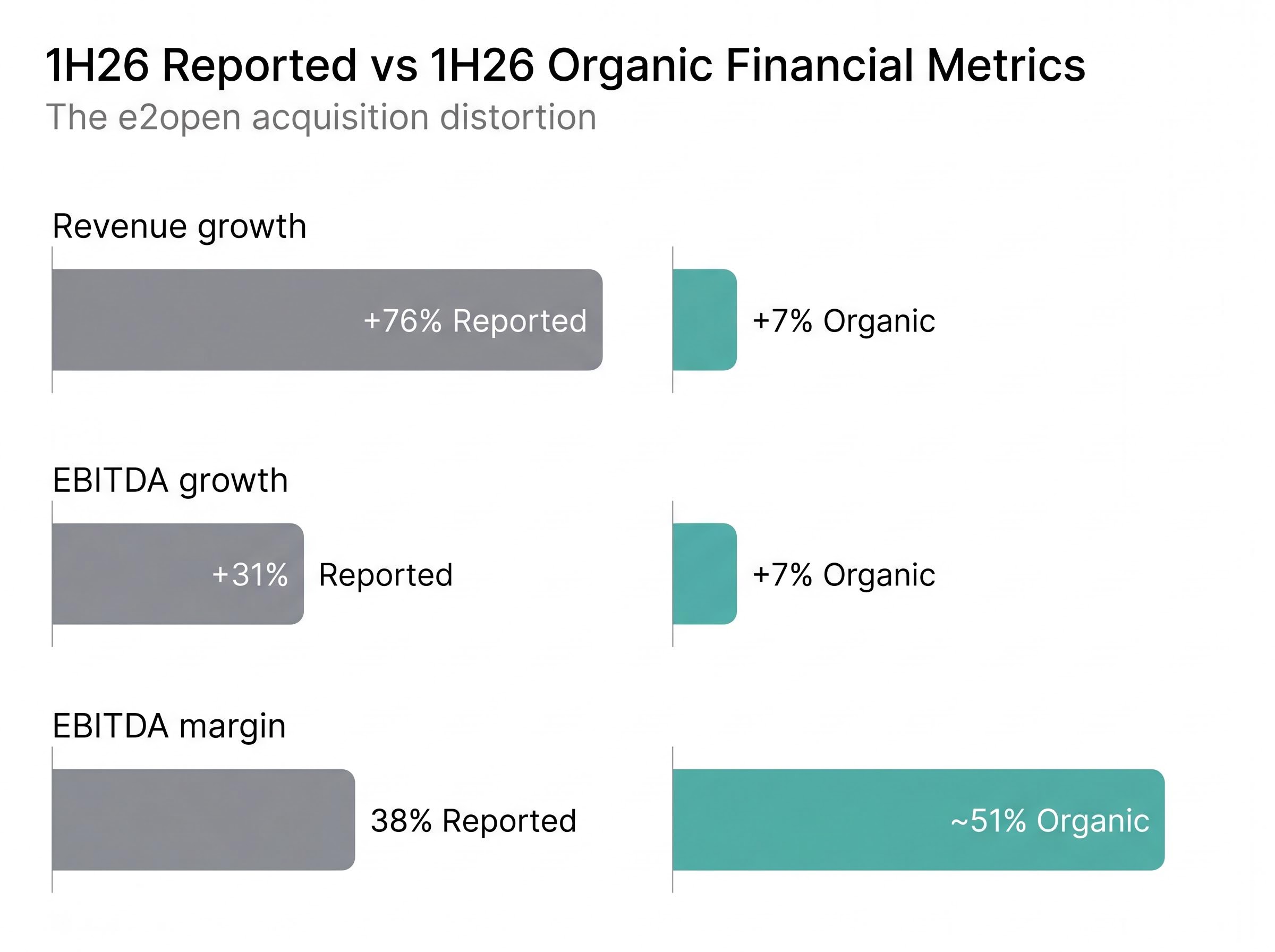

Headline numbers in 1H26 painted two very different pictures depending on whether the reader looked at reported or organic results.

| Metric | 1H26 Reported | 1H26 Organic |

|---|---|---|

| Revenue growth | +76% | +7% |

| EBITDA growth | +31% | +7% |

| EBITDA margin | 38% | ~51% |

The reported figures are inflated by five months of e2open consolidation. The organic figures reflect the actual trajectory of the core business. Both matter, but only the organic column reveals the platform’s underlying health.

That platform retains a near-monopoly market position. CargoWise is used by 24 of the 25 largest global freight forwarders and 46 of the top 50 third-party logistics providers. Morningstar’s assessment as of 16 April 2026 was blunt: “No competitors of note” in the logistics software segment. FY24 total revenue reached A$1,042 million, and net profit grew from A$108 million to A$263 million between 2021 and the most recent full-year period.

Platform penetration is a stock; growth rate is a flow. The first is a structural advantage that changes slowly. The second is a cyclical and strategic variable that can shift quarter to quarter.

Organic revenue growth of 7% in 1H26 represents a meaningful deceleration from the company’s historical average of 27.1% per year since 2021. That gap warrants scrutiny. Revenue drivers in 1H26 included large global freight forwarder rollouts, price increases, and a new commercial model launched in December 2025. Whether these prove sufficient to re-accelerate organic growth is the single most important question for investors evaluating the business at current prices.

e2open’s acquisition, completed on 4 August 2025, makes WiseTech look simultaneously better by revenue and worse by margin than the underlying business actually is.

The key financial impacts, in order:

The R&D acceleration is part of a broader AI transformation programme that includes a workforce reduction of up to 2,000 roles across key teams, a structural cost base reset that management expects to generate material margin benefits from FY27 onward as the headcount changes flow through reported results.

The margin compression is a structural feature of consolidating a lower-margin business, not evidence of deterioration in the CargoWise product itself. Acquiring and integrating complementary platforms into CargoWise is WiseTech’s stated and historically consistent strategy.

FY26 EBITDA guidance of A$550 million to A$585 million implies a full-year margin of 40% to 41%, an improvement from the 38% seen in 1H26 as integration costs are absorbed. The market reacted to the guidance announcement on 25 February 2026 with an approximately 10% share price gain, despite the guidance sitting below prior analyst consensus.

That margin trajectory, from 38% in the first half toward 40% to 41% for the full year, is a meaningful signal for investors focused on the direction of margin recovery rather than current-period snapshots.

Australian investors accustomed to evaluating banks on dividend yield or miners on book value need a different lens for a capital-reinvesting software company. Three metrics form the core of that framework:

Applied to WiseTech’s actual numbers, these metrics tell a specific story:

| Metric | Current / Recent Actual | 3-Year Forward Forecast |

|---|---|---|

| Revenue growth | +7% organic (1H26) | 15.4% p.a. (consensus) |

| Earnings growth | +30% NPAT (most recent FY) | 30.1% p.a. (consensus) |

| EPS growth | — | 27.83% p.a. (consensus) |

| Return on equity | 12.8% | 19.32% |

Consensus forecasts from 16 analysts project revenue reaching A$1,414 million in FY26, A$1,582 million in FY27, and A$1,780 million in FY28, according to Simply Wall St data as of 6 May 2026.

The trailing PE ratio of 67.63 (Yahoo Finance, 8 May 2026) appears elevated in isolation. For a company forecast to grow earnings at 30.1% per annum, however, the PE ratio is less informative than the relationship between the current multiple and the forward earnings trajectory. A stock trading at 67 times trailing earnings but growing those earnings at 30% per year re-rates quickly if the growth materialises. The risk sits in the word “if.”

ASX tech premium multiples across Pro Medicus, TechnologyOne, and Xero sit in a similar 56-68x trailing earnings range, and the November 2025 selloff that sent TechnologyOne down approximately 17% on sector sentiment rather than earnings deterioration illustrates precisely the asymmetric downside risk that WiseTech’s own de-rating amplified.

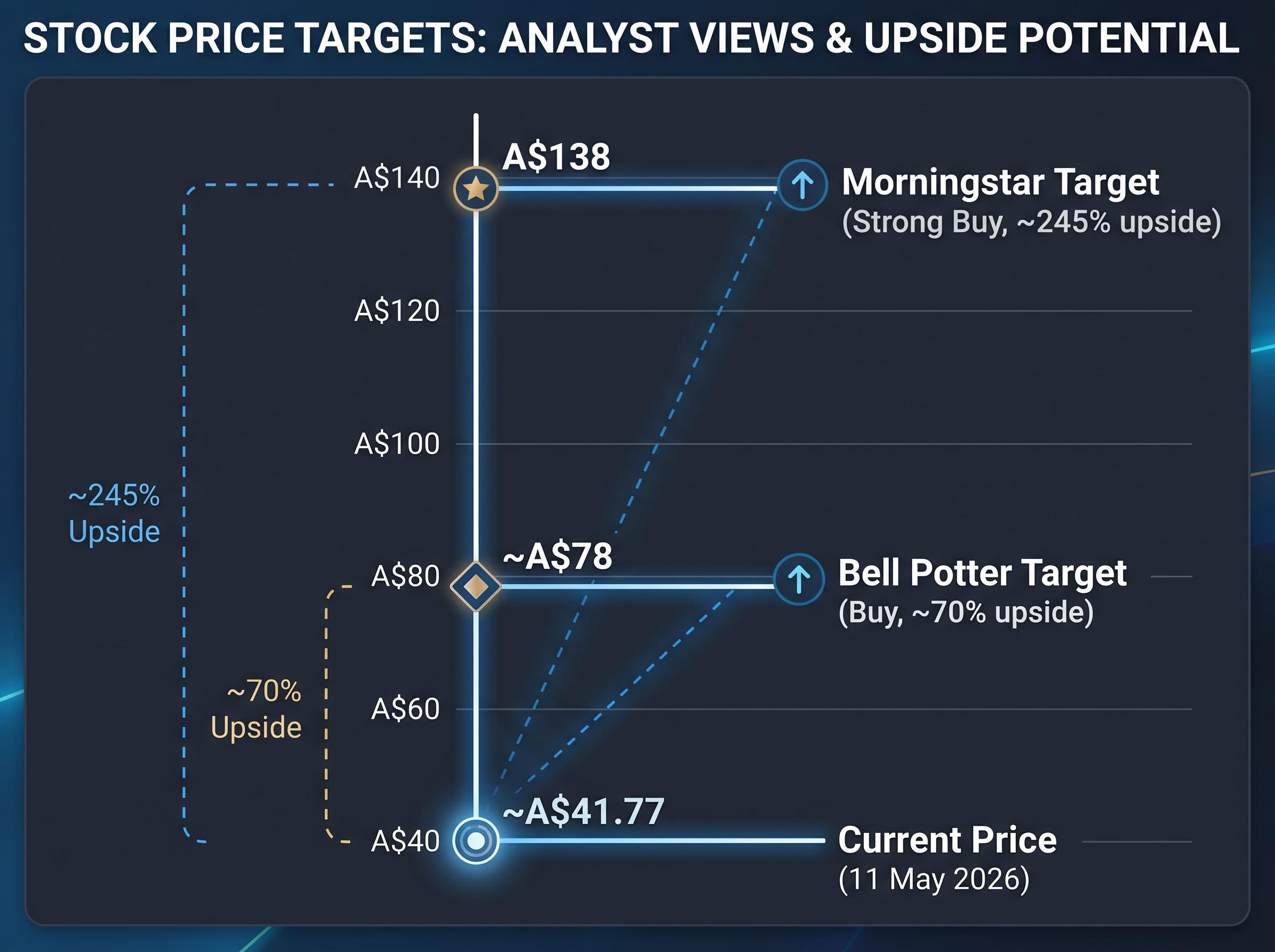

Two publicly available analyst views frame the current valuation debate:

| Analyst / Source | View | Fair Value Target | Reference Price | Implied Upside |

|---|---|---|---|---|

| Morningstar (16 April 2026) | Wide Moat, Strong Buy | A$138 | A$39.96 | ~245% |

| Bell Potter via Motley Fool (6 May 2026) | Buy | ~A$78 | ~A$45.75 | ~70% |

Both targets sit well above the current share price of approximately A$41.77 (Yahoo Finance, 11 May 2026). The market capitalisation stands at A$14.09 billion as of 8 May 2026.

Morningstar confirmed its wide moat rating alongside a high uncertainty designation. The share price jumped approximately 10% on the 25 February 2026 half-year results announcement, despite below-consensus guidance, suggesting the market briefly re-engaged with the underlying earnings quality before broader selling pressure resumed.

The A$60 spread between these two targets is not noise. It reflects materially different assumptions about three variables: how quickly organic CargoWise growth recovers from 7% toward historical rates, how fast the e2open margin drag lifts, and how much residual discount the governance overhang warrants.

Morningstar’s A$138 assumes strong organic recovery and minimal lasting governance discount. Bell Potter’s A$78 appears to embed greater caution on both fronts. Neither is unreasonable given current data.

The more useful observation for investors: even the conservative target implies a material margin of safety from current levels. The disagreement is about magnitude of upside, not direction.

Analyst optimism requires a counterweight. Three risks stand between the current share price and the recovery those targets imply.

Multiple compression risk is the mechanism through which WiseTech’s forward P/E contracted from approximately 86x to 34x between October 2025 and April 2026 even as FY27 EPS estimates rose nearly 29%, a divergence that illustrates how sentiment-driven de-ratings can produce buying opportunities in businesses whose earnings trajectory has not materially changed.

The ASX continuous disclosure obligations under Listing Rules 3.1, 3.1A, and 3.1B require immediate market notification of any information a reasonable person would expect to have a material effect on share price, meaning leadership transitions of the kind WiseTech navigated in early 2025 carry specific and enforceable disclosure timelines.

Morningstar rates WiseTech’s uncertainty as High while simultaneously confirming a wide moat. Both assessments can be simultaneously true: the business may be structurally dominant and the near-term outcome may be genuinely uncertain.

FY26 full-year EBITDA guidance of A$550 million to A$585 million, approximately 13% below prior consensus, underscores that the recovery path is not yet reflected in reported numbers. It remains forecast, not fact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Owning WiseTech at approximately A$42 is a bet on three things resolving favourably:

The bull case rests on a wide-moat business with no named competitors, 24 of 25 largest freight forwarders as customers, and consensus earnings growth of 30.1% per annum. The bear case rests on a stock that remains expensive on current earnings at a PE of 67.63, with organic growth that has materially decelerated and a governance history that introduced uncertainty into what was previously a straightforward compounder.

Analyst targets ranging from approximately A$78 to A$138 against a share price of approximately A$41.77 suggest both camps see value. The disagreement is about how much, and how quickly it surfaces.

Three compounding forces drove the decline: a governance crisis involving co-founder Richard White that surfaced in 2024, margin compression from the August 2025 acquisition of e2open, and a broad sector-wide selloff in global software equities that amplified both company-specific concerns.

CargoWise is WiseTech Global's core logistics software platform, used by 24 of the 25 largest global freight forwarders and 46 of the top 50 third-party logistics providers, giving the business a near-monopoly position that Morningstar described as having no competitors of note.

WiseTech's organic EBITDA margin was approximately 51% in the first half of FY26, but consolidating e2open's lower-margin operations compressed the reported EBITDA margin to 38%; full-year FY26 guidance implies a partial recovery to 40%-41% as integration costs are absorbed.

Based on a consensus of 16 analysts, WiseTech is forecast to grow earnings at approximately 30.1% per annum over the next three years, with revenue projected to reach A$1,780 million by FY28, according to Simply Wall St data as of May 2026.

Morningstar set a fair value target of A$138 per share as of April 2026, implying around 245% upside from its reference price, while Bell Potter's more conservative target of approximately A$78 still implies roughly 70% upside from the share price at the time of publication.