The big four bank shares just posted their steepest weekly declines of 2026, and the sell-off has made their dividend yields more attractive than they have been in months. Over the five trading days to 30 April 2026, Commonwealth Bank fell 3.24%, ANZ dropped 2.6%, NAB shed 1.9%, and Westpac slipped 0.8%, all against a broader ASX 200 retreat of roughly 2%. The timing creates a tension that income-focused investors are already weighing: most broker coverage is cautious, with Morgans holding sell ratings on all four banks, yet the pullback has mechanically lifted entry yields at a moment when the RBA cash rate sits at 4.10%. This analysis cuts through the sell ratings to identify which of the big four currently offers the strongest case for income investors, comparing dividend yields, franking credits, grossed-up returns, and the one bank still attracting bullish analyst targets.

Why the big four sold off and why income investors are watching closely

The declines were sector-wide rather than stock-specific. All four banks sold off alongside the ASX 200’s roughly 2% retreat, with CBA leading the fall at -3.24% and Westpac holding up best at -0.8%.

Five-day price performance to 30 April 2026:

- CBA: -3.24%

- ANZ: -2.6%

- NAB: -1.9%

- Westpac: -0.8%

For income investors, the arithmetic works in a specific way when prices fall. A bank paying the same dividend at a lower share price delivers a higher yield on entry. That is not a guarantee of value, but it is the mechanism that makes the current pullback worth examining rather than dismissing.

The structural context matters here too. The big four collectively hold more than 75% of the Australian domestic banking market, giving them a concentration of deposit funding and mortgage origination that smaller income plays cannot replicate. Price weakness across banks of this scale is a yield-entry question before it is a capital-risk question.

When big ASX news breaks, our subscribers know first

What the dividend numbers actually show after franking credits

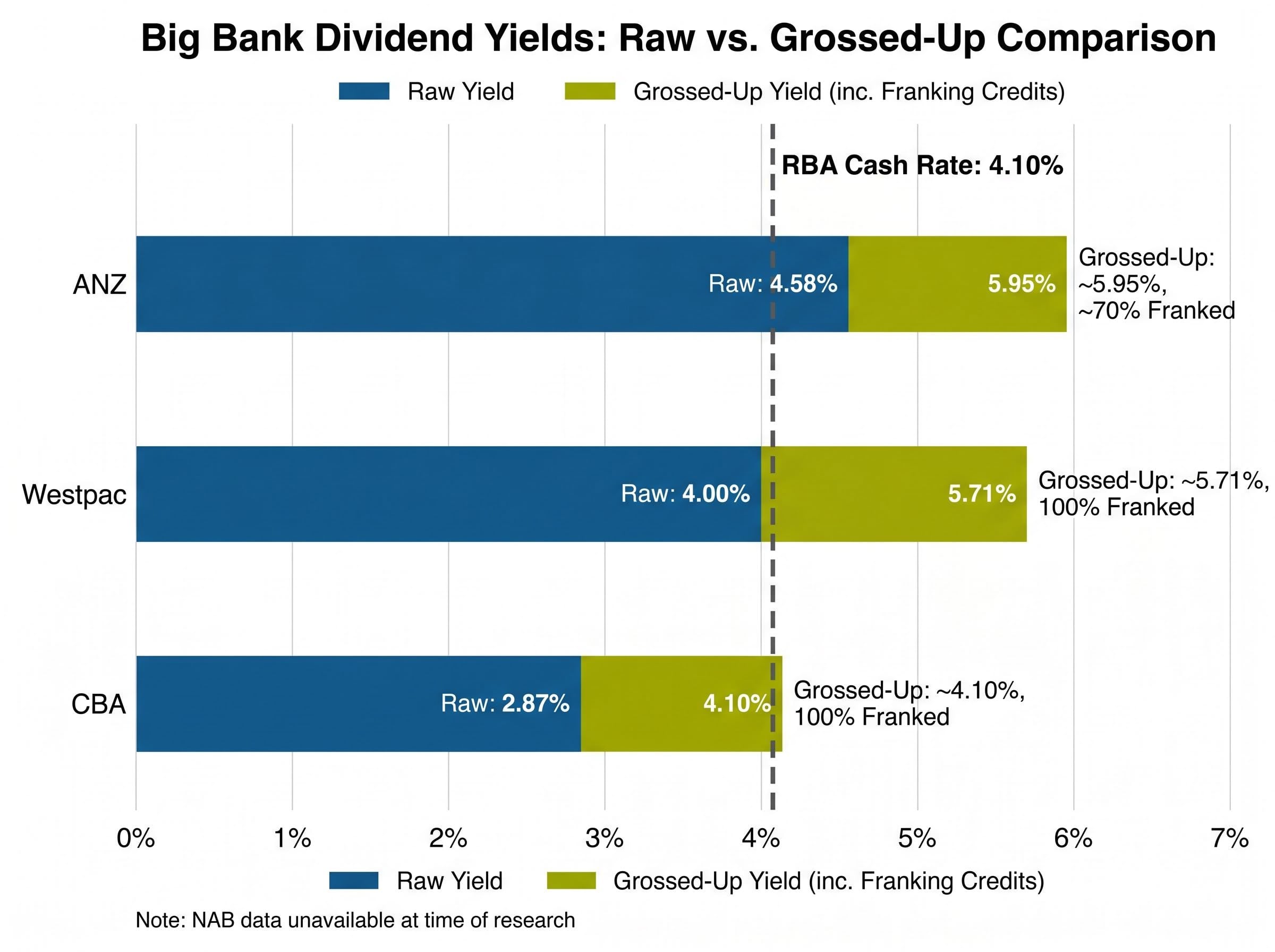

Raw dividend yields tell part of the story. For Australian tax-resident investors, the franking credit attached to each dividend changes the real income comparison materially.

The table below presents the confirmed yield and franking data for three of the four banks. NAB data was unavailable at the time of writing.

| Bank | Share Price | Raw Yield | Franking Level | Grossed-Up Yield |

|---|---|---|---|---|

| ANZ | $36.74 | 4.58% | ~70% | ~5.95% |

| CBA | $173.42 | 2.87% | 100% | ~4.10% |

| Westpac | $38.38 | 4.00% | 100% | ~5.71% |

| NAB | Data unavailable at time of research | |||

ANZ leads on raw yield at 4.58%, though its approximately 70% partial franking means a portion of the dividend carries no franking credit. The grossed-up yield of roughly 5.95% reflects this blend. Westpac yields 4.00% raw, but its 100% franking level lifts the grossed-up figure to approximately 5.71%, making it more competitive on an after-tax basis than the raw number suggests. CBA trails at 2.87% raw, grossing up to around 4.10%.

For context, Westpac’s FY25 final dividend of 77 cents per share (fully franked) is confirmed. The commonly cited total annual figure of $1.54 should be treated with caution, as only the final dividend has been verified against live data.

Income benchmark: At a grossed-up yield of approximately 4.10%, CBA’s income return currently matches the RBA cash rate of 4.10%. Both ANZ and Westpac offer grossed-up yields that sit meaningfully above the risk-free rate, at 5.95% and 5.71% respectively.

The franking distinction matters most for investors in lower marginal tax brackets, where the full franking credit can offset tax owed on other income. Partially franked dividends, such as ANZ’s, still carry a credit on the franked portion but deliver less tax benefit per dollar of income received.

The compounding effect of franking credits on total return is more pronounced for CBA than its headline yield suggests; a two-year holding period to April 2026 produced an estimated 72% total return against a 52.5% price gain, with fully franked dividends and reinvestment accounting for the gap.

The ATO guidance on franking credit refunds confirms that eligible Australian resident individuals can receive the full value of attached franking credits as a tax offset or cash refund, which is the mechanism that lifts ANZ’s and Westpac’s grossed-up yields materially above their headline cash figures.

Understanding P/E multiples and what valuation means for income investors

A price-to-earnings (P/E) multiple measures how much investors are paying for each dollar of a company’s annual profit. A stock trading at 18x earnings costs $18 for every $1 of profit the company generates, while a stock at 28x costs $28 for the same dollar. For income investors, a lower P/E can indicate that the entry price leaves more room for the dividend yield to compound over time, though it does not guarantee value on its own.

On this measure, the gap between the big four is wide. ANZ trades at 18.38x earnings. Westpac sits at 19.38x. CBA commands 28.11x, a premium of more than 50% over ANZ on a P/E basis. NAB data remains unverified.

Why CBA commands a premium and what income investors should make of it

CBA’s 28x multiple reflects its position as Australia’s largest bank by market capitalisation, its digital infrastructure lead, and the market’s confidence in its earnings consistency. That premium is a quality signal, not an income signal. On a grossed-up basis, CBA’s yield of approximately 4.10% sits level with the current RBA cash rate, meaning risk-free alternatives are currently competitive with CBA’s income return.

P/E should not be used as a standalone buy signal. Three factors require scrutiny beyond the multiple:

- Earnings quality: whether reported profits are recurring or boosted by one-off items

- Payout ratio: the share of earnings paid as dividends, which determines how sustainable the yield is

- Credit exposure: the composition of each bank’s loan book and its vulnerability to rising arrears

The absence of NAB from this comparison is a genuine analytical limitation. A full four-bank valuation picture is not possible with the data currently available.

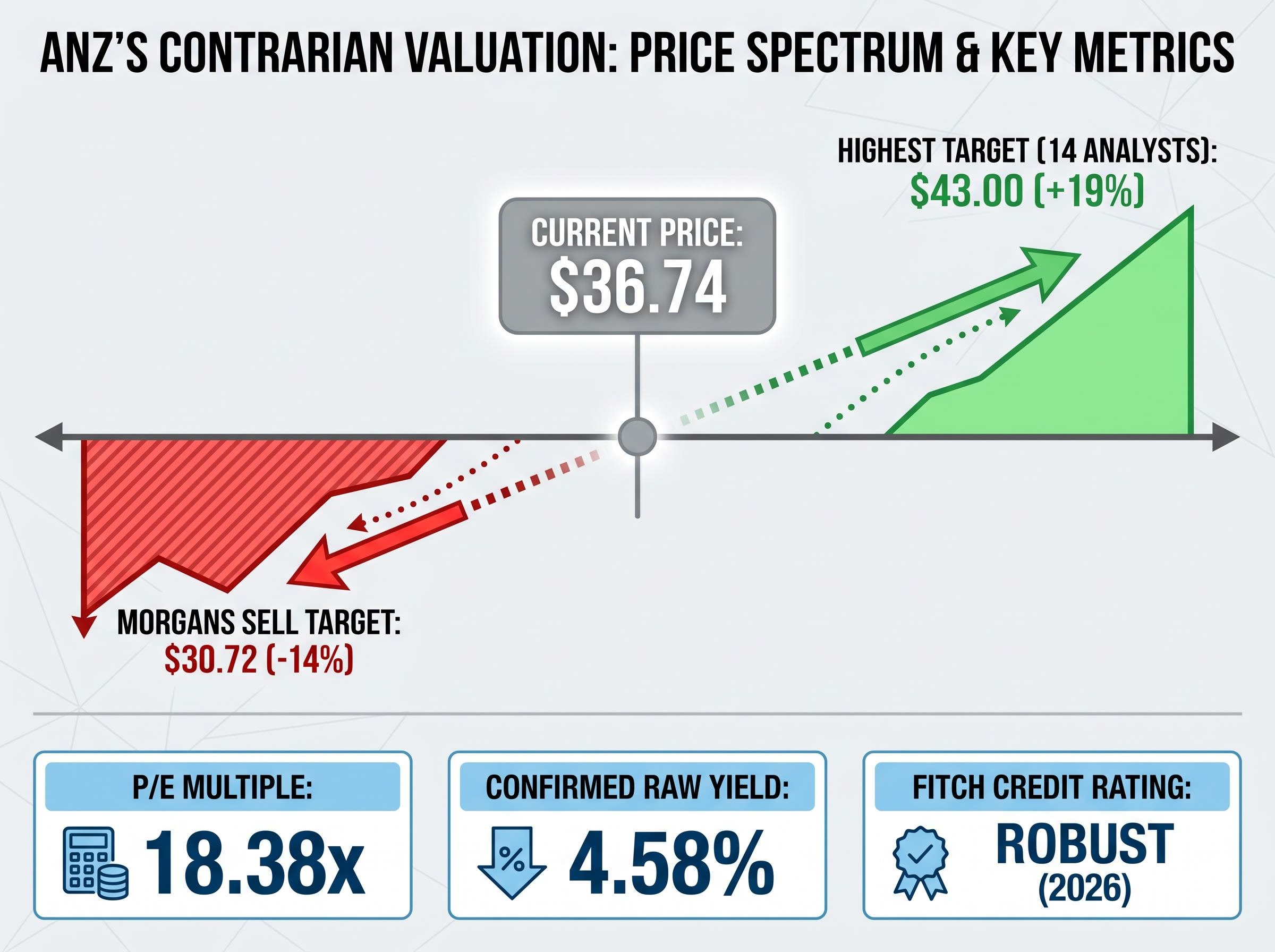

ANZ as the contrarian income pick: where the analyst upside case comes from

The dominant broker position on ANZ is not encouraging.

Morgans holds a sell rating on ANZ with a price target of $30.72, implying approximately 14% downside from the current price of $36.74.

That is not a fringe call. Morgans has sell ratings across the sector, with targets of $124.26 on CBA (approximately 28% downside) and $34.06 on Westpac (approximately 12% downside):

- CBA: Morgans sell, target $124.26 (approximately -28%)

- Westpac: Morgans sell, target $34.06 (approximately -12%)

- ANZ: Morgans sell, target $30.72 (approximately -14%)

Yet the range of analyst opinion on ANZ is wider than on the other three. According to TradingView data, among 14 analysts covering ANZ, the highest price target is $43, implying approximately 19% upside from $36.74. That spread, from $30.72 to $43, signals that the market has not settled on a verdict.

ANZ’s combination of the highest confirmed raw yield (4.58%), the lowest confirmed P/E (18.38x), and the widest analyst upside target makes it the most differentiated income-plus-value proposition among the big four. Fitch Ratings affirmed a robust credit rating for ANZ in 2026, providing a counterweight to the Morgans downside case. The contrarian opportunity is real, but so is the risk embedded in that $30.72 target.

ANZ’s net interest margin expanded 2 basis points to 1.56% in Q1 2026, a directionally positive signal for income sustainability that partially explains why the bullish end of the 14-analyst range holds a $43 target even as Morgans anchors the bear case at $30.72.

Westpac’s dividend growth trajectory and the case for patient income investors

Where ANZ offers a single-year yield and valuation argument, Westpac’s income case unfolds over a longer horizon. The appeal is not the current 4.00% yield alone; it is the projected growth path for the dividend itself.

Forward estimates point to Westpac paying $1.605 per share in FY26 and $1.64 per share in FY27. At the current share price of $38.38, those projections imply rising yields year on year, with each payment expected to carry 100% franking.

| Period | Dividend Per Share | Implied Yield at $38.38 | Note |

|---|---|---|---|

| FY25 Final | $0.77 | N/A (half-year only) | Confirmed, fully franked |

| FY25 Total | $1.54 | ~4.01% | Cited in source data; total unconfirmed |

| FY26 (Projected) | $1.605 | ~4.18% | Forward estimate |

| FY27 (Projected) | $1.64 | ~4.27% | Forward estimate |

Westpac reported FY25 net profit of $6.91 billion, and the bank has reportedly extended its share buyback programme through November 2026. A growing dividend supported by buyback activity signals confidence in capital generation.

Westpac’s Q1 FY26 profit of $1.9 billion, representing 5% growth on the H2 FY25 average, provides the underlying earnings support for the projected dividend path, though the authoritative confirmation point for the FY26 interim dividend and updated NIM trajectory is the 5 May 2026 half-year results announcement.

Two caveats apply to this data:

- The total FY25 annual dividend of $1.54 is cited in research sources but only the 77-cent final dividend is independently verified

- The buyback extension through November 2026 requires confirmation via Westpac investor relations or ASX announcements

Morningstar holds a neutral outlook for the big four in FY2026, which tempers any aggressive growth assumptions. For income investors planning to hold for two to three years, however, a fully franked dividend on a rising path compounds the income case in a way that a single-year yield snapshot cannot capture.

Income appeal is real, but these risks deserve a place in the analysis

The income case for ANZ and Westpac rests on current yields, franking benefits, and forward dividend projections. Those figures do not exist in isolation. Four risk dimensions are directly relevant to big four bank income investors in the current macro environment:

- Credit quality under higher rates: With the RBA cash rate at 4.10% and a potential peak of 4.85% flagged, mortgage arrears and business loan stress could rise across all four banks’ lending books

- Housing market mortgage book exposure: All four banks carry significant Australian residential mortgage portfolios, and elevated rates increase the probability of borrower distress

- APRA regulatory requirements: Capital adequacy rules may constrain future dividend growth or buyback programmes if credit conditions deteriorate

- NIM sensitivity to RBA rate movements: Net interest margins benefit from higher rates in the short term, but the timing and pace of any rate normalisation will affect earnings trajectories differently across the four banks

The APRA capital adequacy standards require authorised deposit-taking institutions to maintain minimum capital ratios and operate within buffer ranges, and a deterioration in credit conditions could activate those buffers in ways that restrict dividend distributions or curtail buyback programmes across the sector.

Fitch Ratings affirmed robust credit ratings for ANZ, NAB, and Westpac in 2026, providing a baseline of institutional confidence. A KPMG analysis expected around 5 May 2026 may offer additional comparative insight for investors tracking the sector.

This analysis works with verified data for three of the four banks. A complete comparative picture requires NAB yield, franking, and valuation data, alongside broader broker consensus from sources such as Bloomberg Terminal or FactSet.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Where the income opportunity sits and what to watch next

The data points in different directions depending on what an income investor prioritises. ANZ offers the highest confirmed raw yield (4.58%), the lowest confirmed P/E (18.38x), and the widest analyst price target range, making it the strongest contrarian income-plus-value case. Westpac offers 100% franking, a growing dividend trajectory through FY27, and $6.91 billion in underlying profit to support that path.

Both sit well above CBA on an income basis. At its current premium valuation, CBA’s grossed-up yield matches the risk-free rate rather than exceeding it.

Four developments will either confirm or challenge these income theses in the months ahead:

- The KPMG major bank analysis expected in early May 2026

- Any RBA rate decisions that shift NIM guidance across the sector

- NAB’s dividend and franking disclosure, which remains a data gap in any complete big four comparison

- Westpac’s confirmation of the buyback extension through November 2026

For income investors who can tolerate the risk dimensions outlined above, the current pricing of ANZ and Westpac delivers a higher entry yield than the CBA premium valuation affords. The question is not whether the income is attractive. It is whether the macro risks justify the entry.