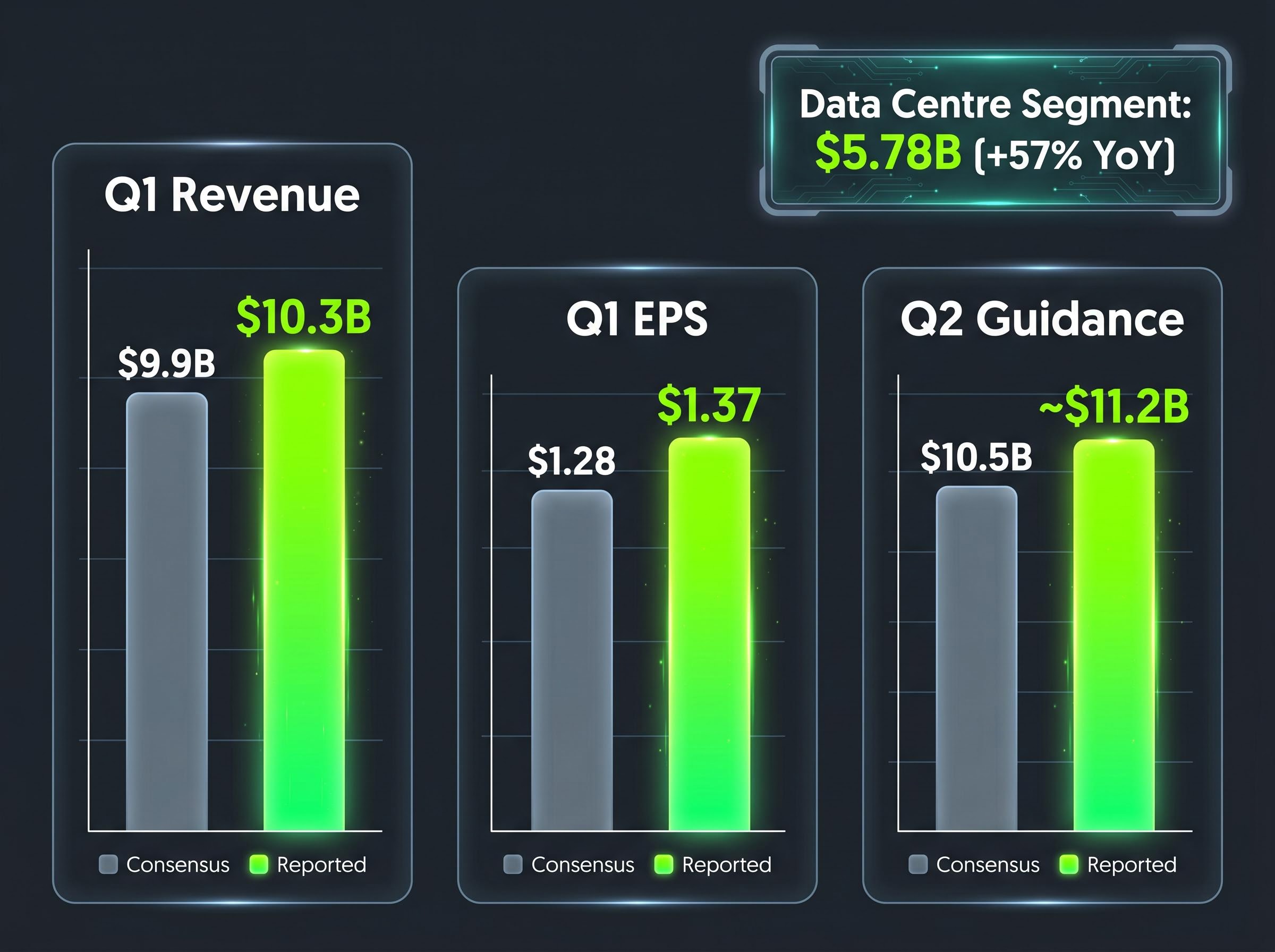

AMD posted $10.3 billion in first-quarter revenue on 10 May 2026, beating the Wall Street consensus of $9.9 billion and triggering the stock’s largest single-day surge in over two years. The shares climbed more than 18% in a session that saw Bernstein nearly double its price target to $525 and Goldman Sachs raise its own to $450, both framing the results as evidence of a structural re-rating rather than a cyclical beat. The reaction landed at a moment when the market is actively sorting which semiconductor companies carry genuine artificial intelligence exposure from those riding temporary momentum. What follows breaks down what AMD actually reported, why two of Wall Street’s most-watched analysts are modelling earnings through 2028, where the bear case retains teeth, and what the second-quarter guidance implies for the rest of 2026.

AMD’s Q1 2026 numbers: what the company actually reported

The beat was not concentrated in a single line item. Total revenue of $10.3 billion cleared the $9.9 billion consensus by $400 million, while non-GAAP earnings per share of $1.37 exceeded the $1.28 estimate by 7%.

AMD’s Q1 2026 earnings press release confirms total revenue of $10.3 billion, non-GAAP EPS of $1.37, and Q2 guidance of approximately $11.2 billion, with Data Centre segment revenue rising 57% year over year as the primary driver of the outperformance.

The Data Centre segment drove the outperformance, delivering $5.78 billion in revenue, up 57% year over year. Within that figure, Instinct MI350 GPU revenue reached approximately $2.1 billion, representing 120% year-over-year growth.

Second-quarter guidance compounded the signal. AMD projected approximately $11.2 billion in Q2 revenue against a Street estimate of $10.5 billion, a gap wide enough to force model revisions across the sell side.

| Metric | Q1 2026 Reported | Consensus Estimate | Beat/(Miss) |

|---|---|---|---|

| Total Revenue | $10.3B | $9.9B | +$0.4B |

| Non-GAAP EPS | $1.37 | $1.28 | +$0.09 |

| Data Centre Revenue | $5.78B | N/A | +57% YoY |

| Q2 Revenue Guidance | ~$11.2B | $10.5B | +$0.7B |

Q2 server CPU outlook: AMD management guided for greater than 70% year-over-year growth in server CPU revenue for Q2 2026, a figure that, if delivered, would mark an acceleration from an already elevated growth rate.

The scale of the beat across revenue, earnings, and forward guidance explains why the market responded with an 18% move rather than a modest relief rally.

When big ASX news breaks, our subscribers know first

What agentic AI means for AMD’s long-term thesis

The quarterly numbers tell one story. The reason Bernstein is modelling AMD earnings per share above $14 in 2027 and approaching $20 in 2028 tells another.

AMD revised its AI accelerator total addressable market (TAM) estimate to $120 billion through 2030, up from a prior estimate of $100 billion, implying a compound annual growth rate of approximately 35%. The company is targeting roughly 25% share of that market. The revision is driven by agentic AI, a category of artificial intelligence in which autonomous software agents perform multi-step tasks (code generation, logistics routing, enterprise search) without continuous human direction, expanding inference workloads well beyond earlier generative AI use cases.

AMD’s positioning rests on two pillars: the ROCm open software ecosystem, which offers developers an alternative to NVIDIA’s proprietary CUDA platform, and native compatibility between EPYC server CPUs and Instinct GPUs, which simplifies infrastructure deployment for hyperscalers already running x86 architectures.

Enterprise deployments moving from pilot to production

The TAM revision carries more weight when matched against named customers with production-stage commitments:

- Microsoft is deploying MI350 GPUs for approximately 20% of Azure AI inference workloads via Copilot agentic workflows.

- Oracle is running MI350 clusters for agent-based cloud services, citing a 1.8x throughput improvement versus prior-generation MI-series hardware.

- Meta is testing an EPYC plus Instinct combination for Llama 4 agent training workloads.

These represent revenue-stage relationships, not letters of intent. The distinction matters because it gives Bernstein’s forward earnings models a commercial foundation rather than a pipeline-based assumption.

Why Goldman Sachs and Bernstein upgraded: the structural re-rating argument

Two of Wall Street’s most closely followed semiconductor analysts issued upgrades on the same day, but their reasoning diverges in instructive ways.

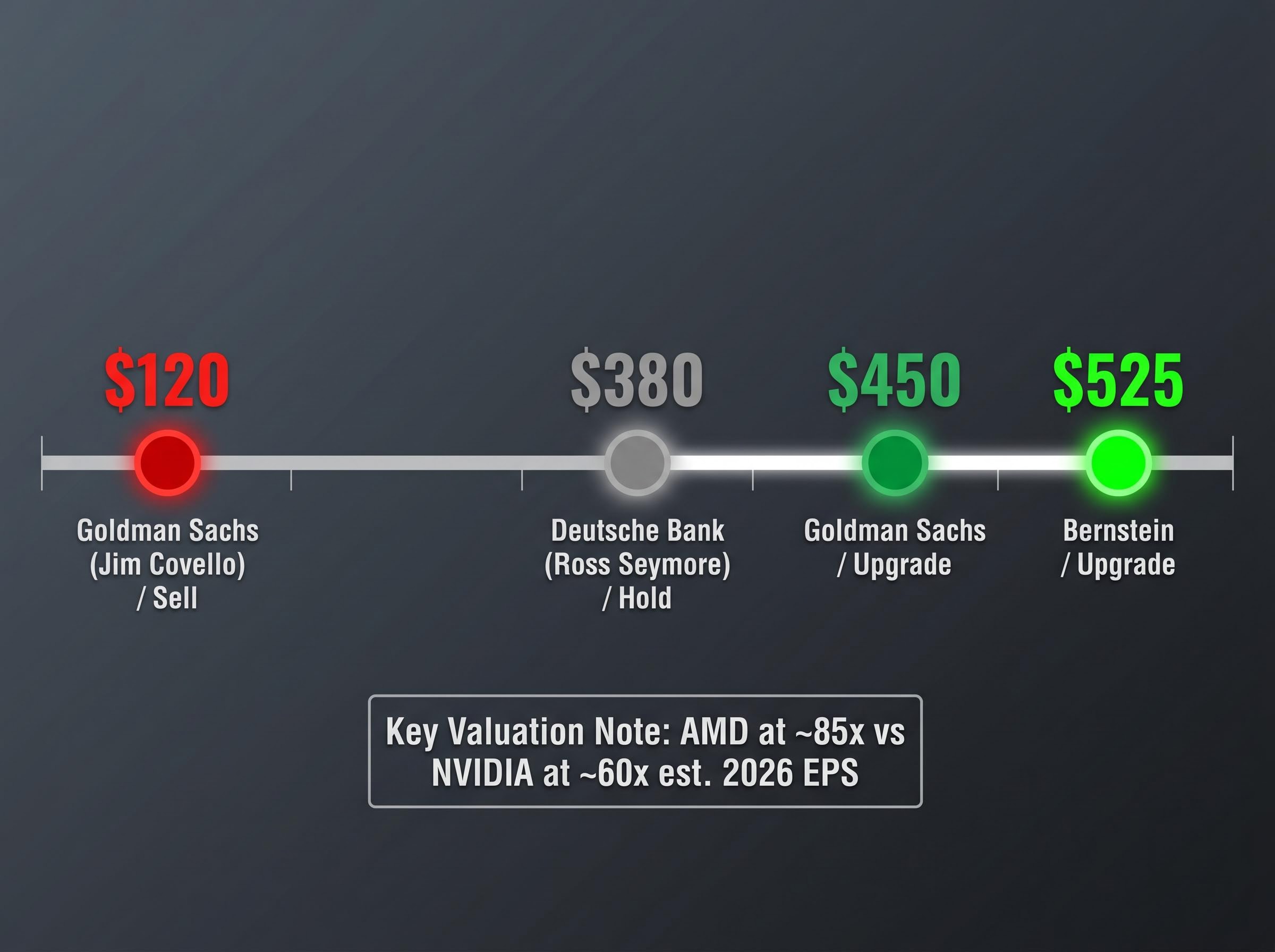

According to reported analyst commentary, Bernstein analyst Stacy Rasgon raised the firm’s price target, framing AMD as now meriting recognition for executing on its underlying story rather than simply riding market momentum. The upgrade is anchored in forward earnings models projecting non-GAAP EPS above $14 in 2027 and approaching $20 in 2028, driven by the 35% CAGR TAM projection and sequential data centre revenue growth implied by Q2 guidance.

According to reported analyst commentary, a Goldman Sachs analyst took a different path, raising the target to $450. That thesis centres on a structural CPU tailwind: agentic AI workflows require significant server-side orchestration, and AMD’s x86 compatibility positions it as a disproportionate beneficiary of that demand.

The distinction matters. Bernstein is primarily making an earnings credibility argument. Goldman is primarily making a hardware architecture argument. When two independent analytical frameworks converge on the same directional conclusion, the structural case is harder to attribute to sentiment alone.

The commercial foundation for Bernstein’s forward earnings model extends beyond quarterly results: a $60 billion Meta chip supply agreement covering five years of MI300X and MI325X GPU shipments beginning H2 2026 provides contractually anchored revenue visibility that analysts have described as de-risking a significant portion of AMD’s 2027 revenue line.

| Analyst | Prior Target | New Target | Primary Upgrade Driver | Key Risk Cited |

|---|---|---|---|---|

| Bernstein (Stacy Rasgon) | N/A | $525 | Forward EPS credibility; 35% TAM CAGR | Execution on MI400 ramp |

| Goldman Sachs | N/A | $450 | Structural CPU tailwind from agentic AI | NVIDIA GPU dominance persisting |

The bear case: why Goldman’s sell-side colleague disagrees

A separate Goldman Sachs team, led by analyst Jim Covello, maintained a Sell rating with a price target of $120 on the same day.

Goldman Sachs (Jim Covello), Sell, price target $120: The starkest contrast on Wall Street, Covello’s target implies more than 70% downside from the post-surge price.

The scepticism is not reflexive. It rests on three specific, enumerable concerns:

- Valuation: AMD now trades at approximately 85x estimated 2026 earnings per share, compared with approximately 60x for NVIDIA (based on analyst estimates; NVIDIA’s Q1 FY2027 results had not yet been reported as of 10 May 2026). That premium implies a sustained earnings growth rate that multiple analysts have flagged as aggressive.

- Competitive positioning: AMD’s estimated share of the combined GPU market sits at approximately 8%, up from roughly 5% the prior year. NVIDIA retains dominant market share, and supply chain constraints for the MI400 (targeted for H2 2026 launch) could cap near-term gains.

- Customer and regulatory concentration: The top five customers account for approximately 40% of AMD revenue, and China export restrictions continue to limit the addressable market for advanced AI accelerators.

Positioning AMD within the broader AI hardware landscape requires understanding where its GPU and CPU offerings sit relative to competing architectures: the GPU flywheel against the custom ASIC model debate, which pits Nvidia’s general-purpose accelerator dominance against Broadcom’s locked-in hyperscaler contracts, defines the competitive environment AMD is entering as it pushes toward 25% GPU market share.

The BIS export license review policy effective January 15, 2026 requires case-by-case evaluation of advanced computing semiconductors shipped to China and Macau, a framework that directly constrains the addressable market for AMD’s highest-performance AI accelerators in one of the world’s largest data centre markets.

Deutsche Bank analyst Ross Seymore offered a similar note of caution, maintaining a Hold rating and raising the price target modestly to $380 while flagging that a 50%+ compound annual growth rate appears unsustainable over a multi-year horizon.

The 18% single-day move is significant. So is the fact that the bear case is not a fringe position.

How AMD’s EPYC server CPU fits into the AI infrastructure stack

The stock debate can obscure a simpler question: why are server CPUs being re-rated alongside GPUs in an AI spending cycle?

In a modern AI server rack, GPUs handle the parallel computation required for training and inference, processing thousands of calculations simultaneously. CPUs perform a different function: orchestrating data flow, managing memory, and routing inference outputs to their destinations. In an agentic AI workflow, CPU-side orchestration becomes more demanding as the number and complexity of autonomous agent tasks increases.

The sequence works roughly as follows:

- The GPU inference layer processes the AI model’s core computation, generating a response or decision.

- The CPU orchestration layer manages task routing, memory allocation, and inter-agent communication.

- The output routing layer delivers results to the requesting application or triggers the next agent task in the chain.

AMD’s EPYC processors dominate the x86 server CPU category, and according to reported analyst commentary a Goldman Sachs analyst cited this positioning as the primary reason for the upgrade: hyperscalers already running x86 infrastructure face lower switching costs when scaling agentic AI workloads on AMD hardware. ROCm 6.0 was cited by AMD management as enabling agentic inference optimisation when paired with EPYC CPUs.

What 70% server CPU growth in Q2 signals about hyperscaler purchasing

The Q2 guidance figure of greater than 70% year-over-year server CPU revenue growth is not a projection from an external analyst. It came from AMD management.

If sustained, that growth rate would shift the composition of AMD’s Data Centre revenue meaningfully toward CPU by the end of 2026, reducing the segment’s dependence on GPU cycles alone. The three largest named customers, Microsoft, Oracle, and Meta, have each disclosed capital expenditure commitments to AI infrastructure that imply multi-quarter purchasing runways rather than one-off procurement events.

AMD’s structural moment: what the next 12 months need to deliver

The bull case and the bear case share one thing in common: both depend on execution milestones that have not yet occurred. Three in particular will determine whether the re-rating is durable:

- MI400 supply chain execution (H2 2026): Multiple analysts have flagged production constraints for AMD’s next-generation GPU. A delayed or limited ramp would weaken the share-gain narrative at a moment when NVIDIA remains the default choice for hyperscaler GPU procurement.

- Q2 and Q3 revenue delivery: The $11.2 billion Q2 guidance, if met, would mark the second consecutive quarter of guidance beats. Sequential data centre growth through the second half of the year is the minimum threshold for the structural thesis to hold.

- 2027 EPS trajectory: Bernstein’s model projects earnings per share above $14 in 2027. The gap between that figure and the current $1.37 quarterly run rate is wide enough that any deceleration in the Data Centre segment would compress the timeline significantly.

The long-term bull case in one number: Bernstein’s model projects AMD earnings per share approaching $20 in 2028, a figure that, if achieved, would justify a valuation well above today’s post-surge price.

Short interest stood at approximately 6.2% of float heading into the earnings release, with covering activity accelerating post-beat. Implied volatility on near-term options ranged from 75-85% across most strikes as of today, reflecting a market that is pricing significant movement in either direction over the coming quarters.

The 18% single-session gain did not land in isolation: it triggered a sector-wide semiconductor rally that saw Samsung reach a $1 trillion market cap and SK Hynix gain 11% in the same session, a breadth of reaction that reflects the market pricing in supply-chain-wide confirmation of AI hardware demand rather than a single-company re-rating.

If AMD’s multiple compresses back toward 60x without earnings growth sufficient to justify the current price, the Goldman Sachs $120 Sell target implies material downside. If Bernstein’s forward models prove achievable, the stock has room to grow into its valuation. The next two earnings cycles will begin to resolve that gap.

For investors trying to calibrate how much of AMD’s post-surge price reflects genuine earnings growth versus multiple expansion, our full explainer on AI chip valuation comparisons examines Nvidia trading 39% below its average analyst price target alongside Broadcom’s 106% AI revenue growth, with dissenting views from Seaport Research on structural limits to AI industry growth that apply equally to AMD’s 2027-2028 earnings projections.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and earnings projections, are subject to change based on market developments and company performance.