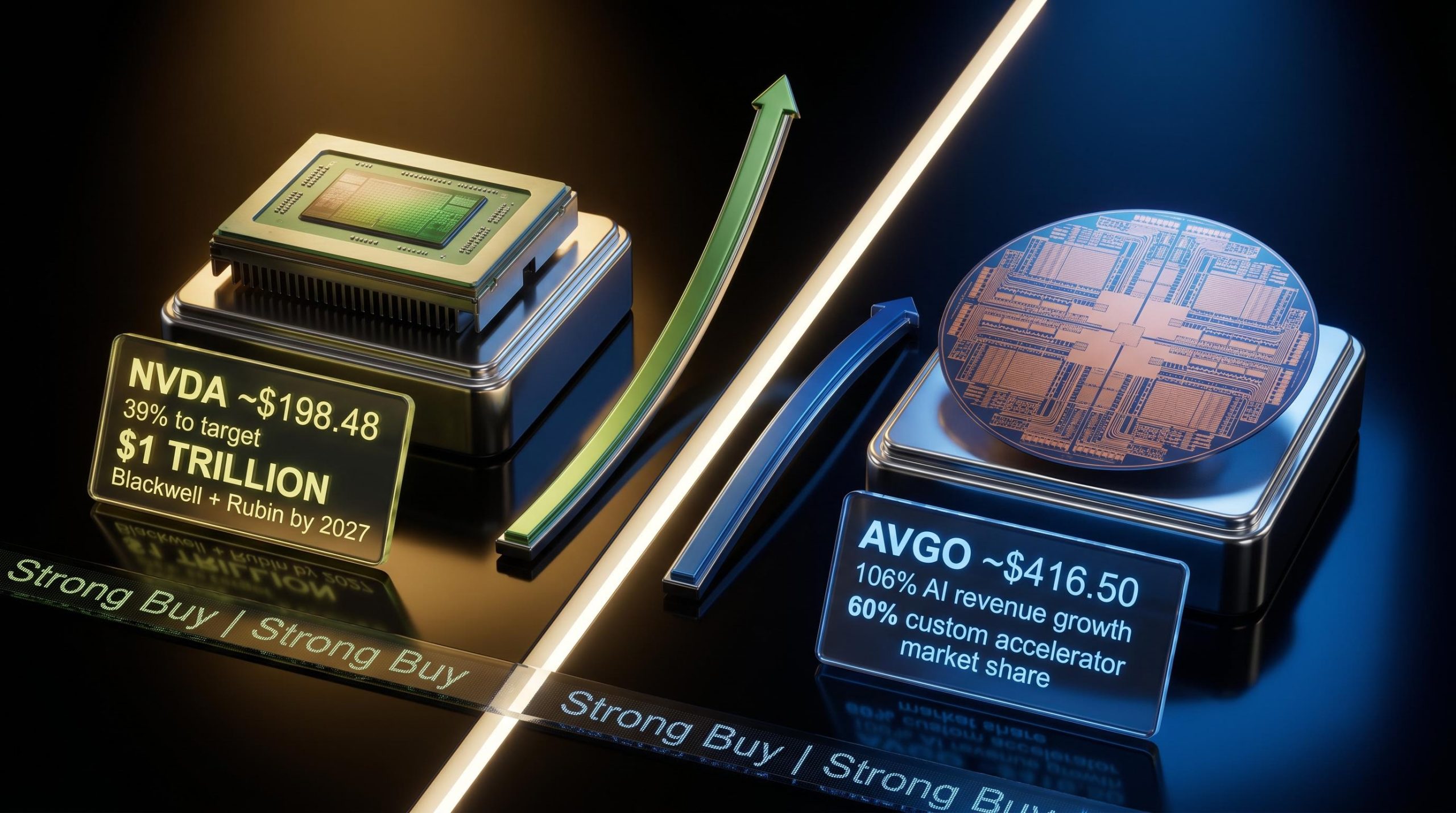

Nvidia trades at roughly 39% below its average analyst price target. Broadcom trades at roughly 11% below its own. Both carry Strong Buy consensus ratings from Wall Street, and both are identified by Zacks as top earnings growers for 2026. Yet the two companies represent fundamentally different bets on how AI infrastructure spending will flow over the next two years.

As of early May 2026, Broadcom has posted 106% year-over-year AI chip revenue growth in Q1 FY2026, while Nvidia CEO Jensen Huang has projected at least $1 trillion in combined Blackwell and Rubin revenue by end-2027. The comparison is live, consequential, and requires more than a headline-level reading. What follows walks through the architecture divide, the current financials, the valuation spread, what analysts are actually saying, the risks that could break each thesis, and a framework for matching each stock to a specific investor profile.

How Nvidia and Broadcom are solving AI differently

The investment case for each company starts with a structural question: how should AI compute be delivered at scale? Nvidia and Broadcom have arrived at opposite answers, and the divergence shapes everything from margin profiles to customer concentration.

Nvidia’s CUDA moat: why software locks in hardware

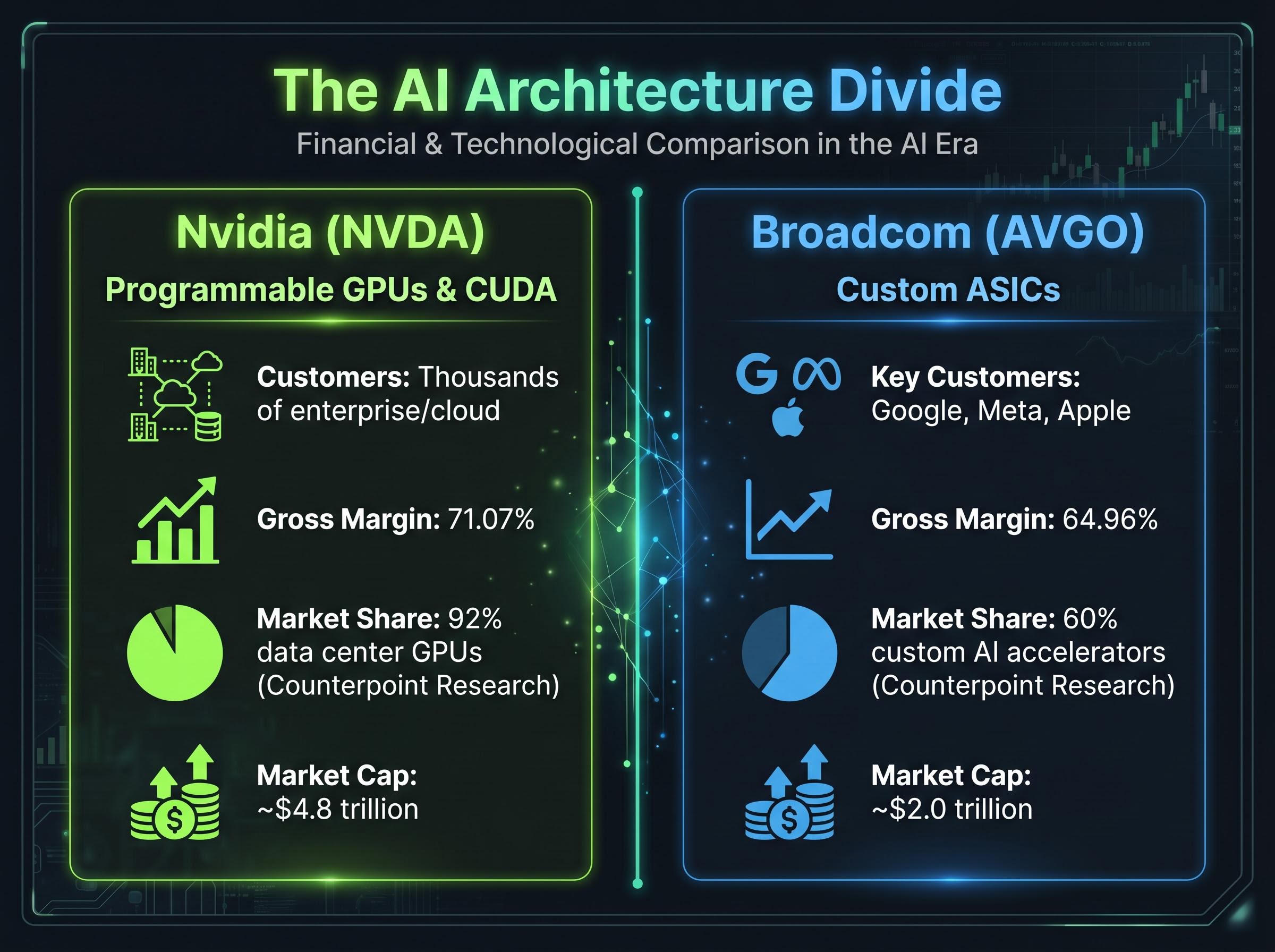

Nvidia builds programmable GPU accelerators optimised for flexibility across both training and inference workloads, unified by the CUDA software ecosystem. CUDA functions as the established AI infrastructure standard, cited by Raymond James and New Street analysts as a structural reason consensus estimates may be conservative. Application developers, AI frameworks, and enterprise tooling are all standardised around it, creating switching costs that extend well beyond the chip itself. Nvidia commands a market capitalisation of approximately $4.8 trillion.

Broadcom’s hyperscaler partnerships: efficiency at scale

Broadcom takes the opposite approach. The company designs custom application-specific integrated circuits (ASICs), chips engineered for individual hyperscaler clients such as Google, Meta, and Apple, trading flexibility for efficiency and lower total cost at scale. Broadcom holds approximately 60% market share in custom AI accelerators, according to Counterpoint Research, and commands a market capitalisation of approximately $2.0 trillion. CEO Hock Tan has cited growing agentic and generative AI adoption as sustaining demand for this model.

The investor implication breaks down across four dimensions:

- Flexibility: GPUs serve a broad range of AI workloads; ASICs are optimised for specific ones

- Customer base: Nvidia sells across thousands of enterprise and cloud customers; Broadcom’s revenue concentrates among a handful of hyperscalers

- Margin profile: Nvidia’s gross margin (71.07%) reflects software ecosystem pricing power; Broadcom’s (64.96%) reflects hardware customisation at volume

- Switching costs: CUDA locks in developers and frameworks; ASIC relationships lock in multi-year co-design partnerships

GPU exposure is a bet on the breadth of AI infrastructure demand. ASIC exposure is a bet on the depth of hyperscaler customisation. Every data point that follows lands differently depending on which side of that divide an investor sits.

When big ASX news breaks, our subscribers know first

Recent results: where the growth numbers actually stand

Both companies reported strong recent quarters, and the numbers reveal two distinct growth profiles rather than a single AI narrative.

Nvidia’s Q4 FY2026 results (ended 25 January 2026) showed GAAP earnings per share of $1.76, up 35% year over year, with adjusted EPS of $1.62. The headline forward signal came from Jensen Huang’s projection of at least $1 trillion in combined Blackwell and Rubin revenue by end-2027, a figure that Raymond James and New Street both cite as grounded in inference demand running ahead of schedule.

Forward-looking signal: Jensen Huang has projected at least $1 trillion in combined Blackwell and Rubin architecture revenue by end-2027. Analysts at Raymond James view current consensus estimates as potentially conservative, with inference demand catalysts arriving ahead of schedule.

Broadcom’s Q1 FY2026 delivered total revenue up 29% year over year, with AI chip revenue surging 106% year over year. Non-GAAP diluted EPS came in at approximately $2.10, up roughly 30% year over year.

Both companies were identified by Zacks as top earnings growers for 2026 driven by AI demand. This is not a one-winner comparison.

| Metric | Nvidia (NVDA) | Broadcom (AVGO) |

|---|---|---|

| Latest EPS growth (YoY) | 35% (GAAP) | ~30% (non-GAAP) |

| AI revenue growth (YoY) | Not separately disclosed | 106% |

| Gross margin | 71.07% | 64.96% |

| Market cap | ~$4.8 trillion | ~$2.0 trillion |

What the valuation gap is actually telling investors

Forward price-to-earnings multiples are often read as a simple cheap-versus-expensive verdict. In this case, the spread between the two stocks reveals something more specific: what each price already assumes about growth, and how much room remains if those assumptions prove correct.

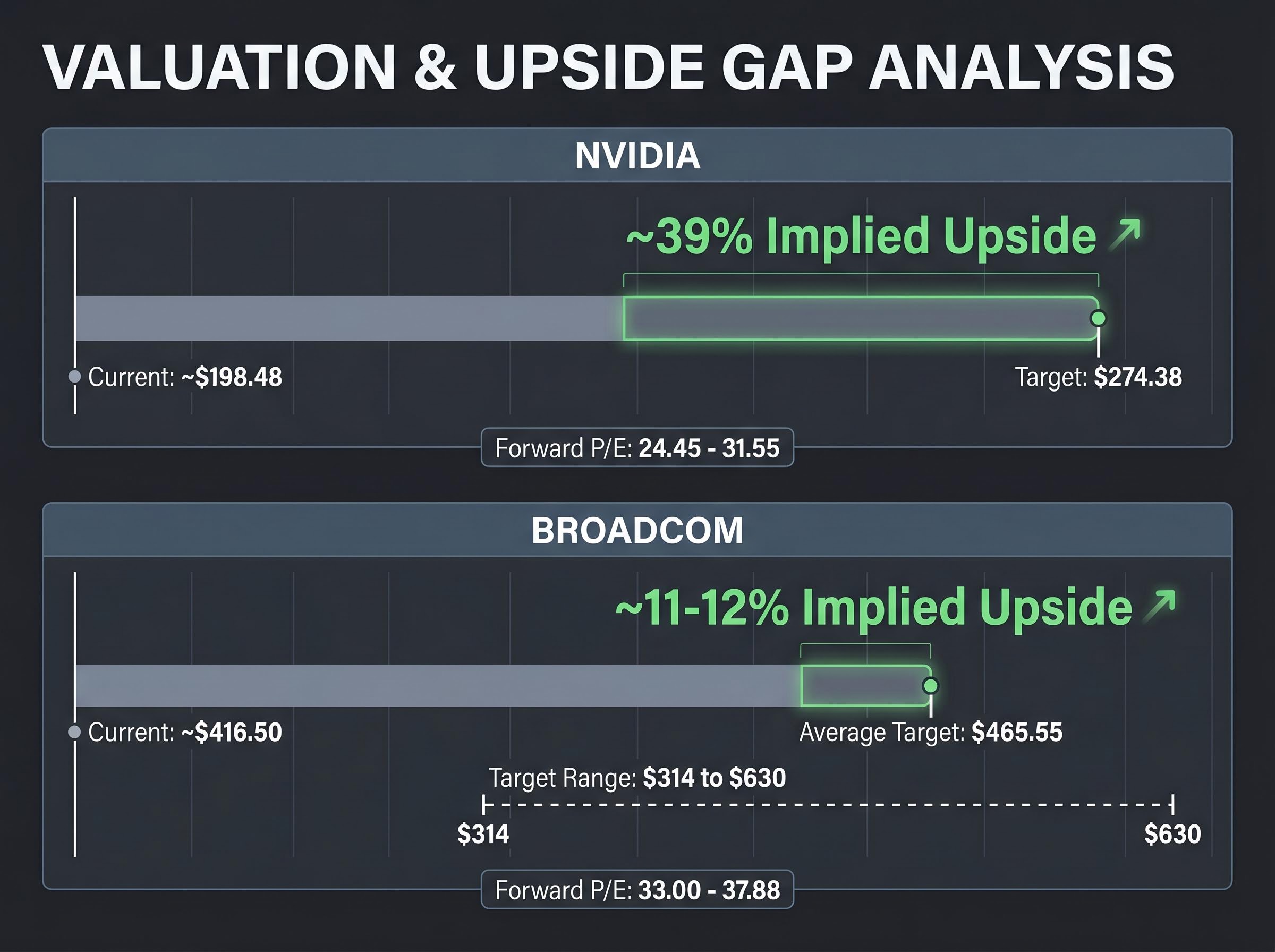

Nvidia trades at a forward P/E of approximately 24.45-31.55. Broadcom trades at approximately 33.00-37.88. The instinct is to read the lower multiple as cheaper, but the context matters. Nvidia’s larger revenue base dilutes its per-unit growth rate, compressing the multiple even as absolute dollar growth remains enormous. Broadcom’s premium reflects concentrated growth expectations from a narrower custom-chip market, where a single hyperscaler contract can move the revenue trajectory materially.

The price-to-target spread sharpens the picture. Nvidia trades at approximately $198.48 against an average analyst target of $274.38, implying roughly 39% upside. Broadcom trades at approximately $416.50 against an average target of $465.55, implying roughly 11-12% upside. The dispersion in Broadcom’s analyst targets is itself a signal: the high target sits at $630, the low at $314, a range wide enough to reflect genuine disagreement about ASIC trajectory.

| Metric | Nvidia (NVDA) | Broadcom (AVGO) |

|---|---|---|

| Current price | ~$198.48 | ~$416.50 |

| Average analyst target | $274.38 | $465.55 |

| Implied upside | ~39% | ~11-12% |

| Forward P/E range | 24.45-31.55 | 33.00-37.88 |

| Analyst consensus | Strong Buy (39 ratings) | Strong Buy (29 Buys, 2 Holds) |

Three inferences stand out from this valuation gap:

- Nvidia offers a wider margin of safety relative to consensus targets, meaning the stock has more room to re-rate even if growth merely meets expectations

- Broadcom’s premium multiple prices in sustained high growth from a concentrated customer base, leaving less room for disappointment

- The wide analyst target dispersion on Broadcom ($314 to $630) suggests the market has not converged on a single ASIC growth narrative the way it has around Nvidia’s GPU trajectory

What Wall Street analysts are saying right now

The consensus view on both stocks is bullish, but the distribution of conviction, and the identity of the dissenters, tells a more nuanced story.

S&P Global survey data from April 2026 shows 56 out of 59 analysts assigning Nvidia a Buy or Strong Buy rating. For Broadcom, 44 out of 47 analysts rated the stock Buy or Strong Buy. The three most consequential recent analyst actions shape the current positioning:

- Raymond James analyst Simon Leopold raised his Nvidia price target to $323 from $291, maintaining Strong Buy, citing updated estimates for $1 trillion in cumulative GPU sales through 2027 and inference demand catalysts arriving ahead of schedule

- New Street analyst Pierre Ferragu added Nvidia to its 2026 best ideas list, projecting a $1 trillion run-rate by end-2027 (approximately double consensus), with strong earnings beats expected through 2026-2027

- Seaport Research downgraded Broadcom to Neutral on 8 April 2026, citing AI industry limits, a meaningful shift from its prior Buy stance

New Street’s Pierre Ferragu has described retail sentiment around Nvidia’s guidance as reflecting a “misplaced lack of enthusiasm,” suggesting the growth trajectory may be materially underappreciated by non-institutional investors.

The dissenting view deserves specific attention. Seaport Research analyst Jay Goldberg maintains a Sell rating on Nvidia with a $140 price target, citing competitive pressures from custom silicon. His firm’s simultaneous downgrade of Broadcom to Neutral creates a structurally consistent position: that AI industry growth may be approaching limits that constrain both architectures, even if ASICs increasingly pressure GPU economics. It remains a minority view, but one with internal coherence worth monitoring.

The risks each company still carries

Both stocks carry Strong Buy consensus ratings, but the specific failure modes for each thesis differ in character and timing.

Nvidia: where the bull case could break down

- ASIC share erosion: Broadcom’s 60% custom accelerator market share and 106% AI revenue growth demonstrate that hyperscalers are willing to invest heavily in alternatives to GPUs for specific workloads; sustained ASIC growth could gradually narrow Nvidia’s addressable market

- Hyperscaler in-house silicon: Google TPUs and Amazon Trainium represent ongoing efforts by Nvidia’s largest customers to reduce dependence on third-party GPU supply, creating structural pressure even if near-term share erosion remains modest

- Seaport’s competitive pressure thesis: Jay Goldberg’s $140 target versus the consensus average of $274.38 represents a live dissenting view that financial arrangements between hyperscalers and chip suppliers may compress GPU economics more than bulls expect

Broadcom: where the bull case could break down

- Valuation multiple contraction: A forward P/E of 33-38x prices in sustained high growth; if AI chip revenue growth decelerates from 106% toward more normalised levels, the multiple could compress materially before earnings catch up

- Customer concentration: Google, Meta, and Apple represent the bulk of Broadcom’s custom accelerator book; the loss or deferral of a single major contract could disproportionately affect the revenue trajectory

- Seaport’s Neutral downgrade: The 8 April 2026 downgrade signals a possible AI industry ceiling that, if validated, would constrain the total addressable market for custom ASICs regardless of Broadcom’s competitive position within it

The analyst target dispersion on Broadcom ($314 to $630) is the widest in this comparison set, reflecting genuine disagreement about whether ASIC demand is a secular shift or a cyclical surge within the current AI buildout phase.

Which AI chip stock fits which investor

Five sections of data, valuation, and analyst positioning converge on a framework rather than a single answer.

Nvidia is the higher-upside, lower-current-multiple option. It suits investors seeking broad AI infrastructure exposure with meaningful price-to-target room (approximately 39% to consensus), who accept the risk that GPU competition from ASICs and in-house hyperscaler silicon could accelerate. A Strong Buy consensus from 39 analysts and the $1 trillion Blackwell and Rubin revenue projection underpin the bull case.

Broadcom is the lower-upside, higher-multiple option. It suits investors who want exposure to the efficiency-driven ASIC trend and are comfortable paying a premium for demonstrated 106% AI revenue growth, accepting that narrower upside to target (approximately 11-12%) leaves less margin for error. Broadcom also offers a dividend yield of 0.60%, a modest but relevant differentiator for income-oriented portfolios.

| Investor Profile | Preferred Fit | Key Upside Driver | Key Risk to Monitor |

|---|---|---|---|

| Growth-focused | NVDA | 39% upside to target; $1T revenue projection | ASIC and in-house silicon share erosion |

| Value-conscious | NVDA | Lower forward P/E (24-31x) vs. AVGO | Seaport’s $140 bear case |

| Income-supplementing | AVGO | 0.60% dividend yield; stable hyperscaler contracts | Customer concentration risk |

| Broad AI diversification | Both | GPU + ASIC capture breadth of AI spend | AI industry growth ceiling (Seaport thesis) |

The case for holding both is straightforward:

- GPU and ASIC markets are not zero-sum; the strongest AI infrastructure buildout scenarios benefit both architectures simultaneously

- Owning both hedges against the risk that one architecture captures a larger share of incremental spend than currently projected

- Both companies are identified by Zacks as top 2026 earnings growers, suggesting near-term earnings momentum is shared

Two different roads to the same AI destination

Nvidia and Broadcom are not competing for the same investor dollar in the same way. They represent structurally different exposures to AI infrastructure spending, and the right allocation depends on what an investor is trying to achieve.

Three findings from this analysis carry the most weight. First, Nvidia’s wider price-to-target gap (39% versus 11-12%) and $1 trillion forward revenue narrative offer more re-rating room, but that room exists partly because the market has not yet fully priced in the inference demand acceleration that Raymond James and New Street see arriving. Second, Broadcom’s 106% AI chip revenue growth and 60% custom accelerator market share demonstrate that the ASIC model is capturing real hyperscaler spend at scale, even as its premium valuation leaves less cushion. Third, the consensus Wall Street view holds that both can win in an AI infrastructure supercycle, with Seaport Research the primary dissenting voice arguing for structural limits.

The two near-term data points most likely to shift this comparison are the Vera Rubin architecture launch timeline and Broadcom’s next earnings report. Both bear watching through the second half of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.