BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

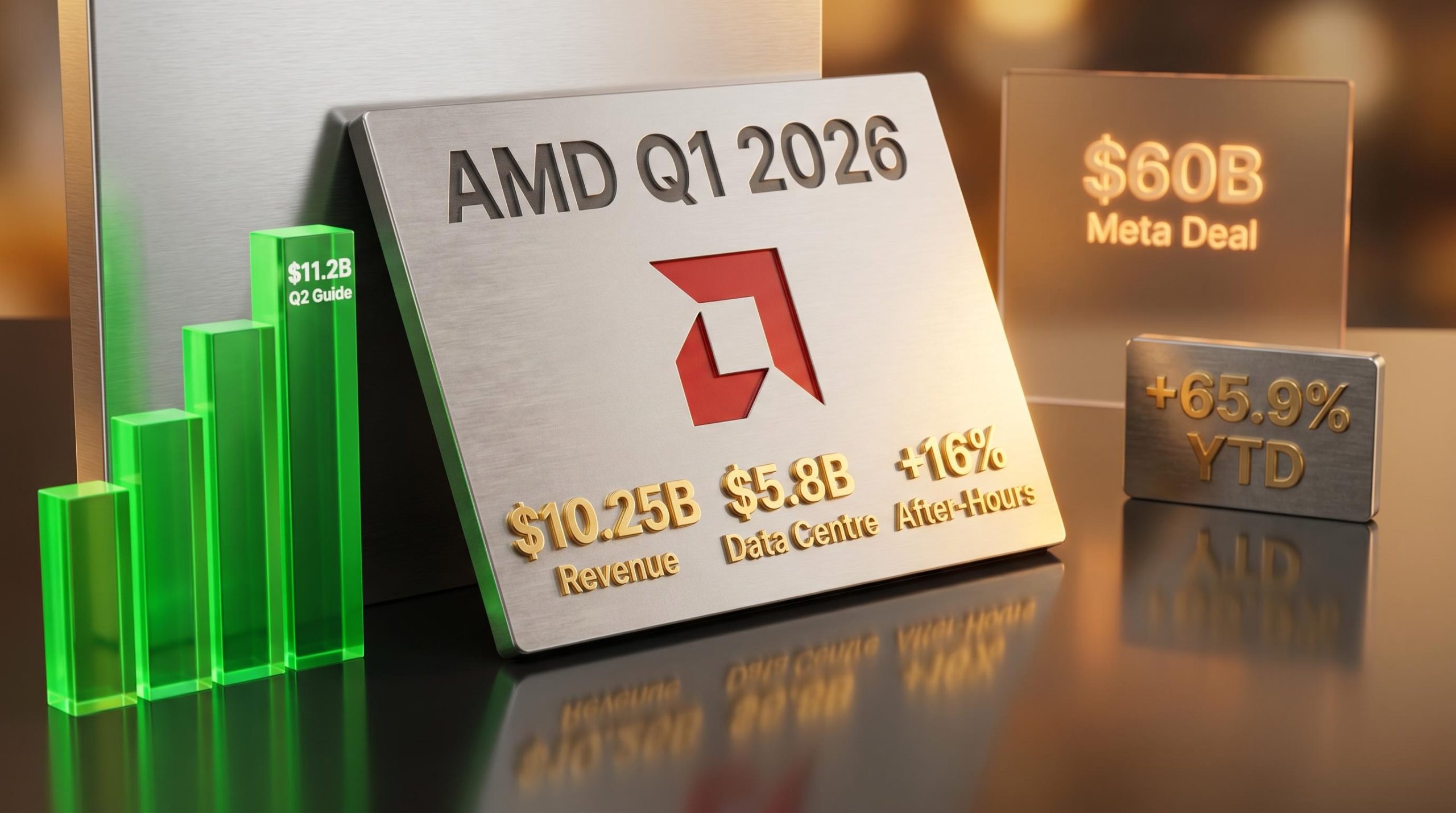

AMD shares surged approximately 16% in after-hours trading on 5 May 2026, the largest single-session move following an earnings release in over two years. The company posted quarterly revenue of $10.25 billion and forward guidance of $11.2 billion that left Wall Street’s consensus figures looking conservative.

The results arrive as investors scrutinise which semiconductor companies are genuinely converting AI infrastructure spending into durable revenue growth rather than benefiting from a temporary demand spike. AMD’s Q1 numbers, released the evening of 5 May, provide the clearest evidence yet that the company is executing consistently across both its GPU and CPU businesses. What follows breaks down the headline financials, identifies the data centre engine driving the outperformance, explains what Q2 guidance implies for full-year momentum, and situates the $60 billion Meta supply deal as a concrete de-risking signal for investors tracking AMD’s multi-year trajectory.

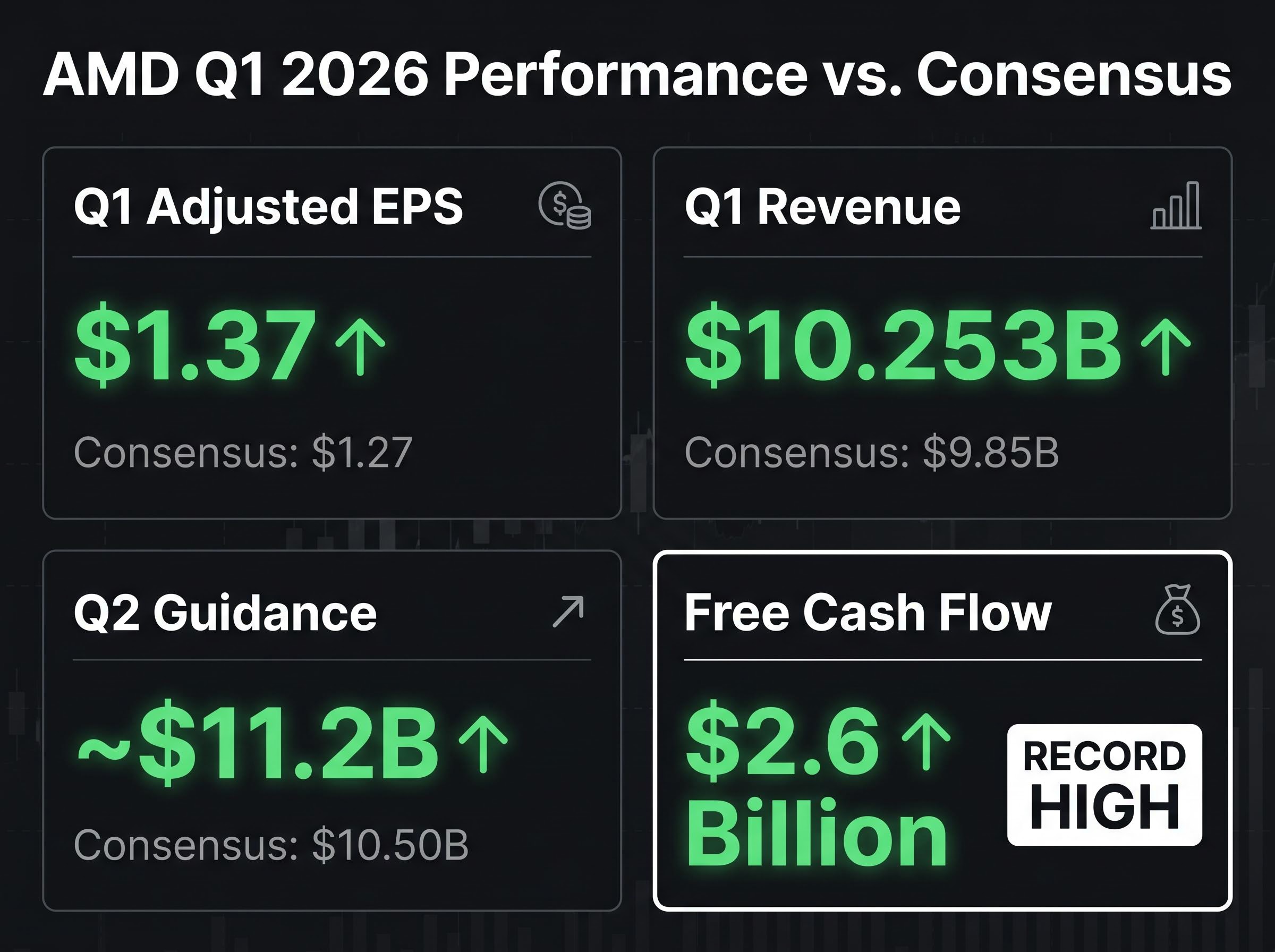

This was not a narrow beat. Adjusted earnings per share came in at $1.37 against a consensus estimate of $1.27, a $0.10 margin that represents nearly 8% upside to expectations. Revenue of $10.253 billion cleared the $9.85 billion analyst estimate by roughly 4%, marking 38% year-on-year growth.

The figure that signals operating quality rather than top-line scale alone sits further down the income statement.

Record free cash flow of $2.6 billion confirms that margin expansion is accompanying AMD’s revenue surge, not being sacrificed for it.

After-hours trading pushed the stock to approximately $413.41, a move that reflected the market pricing in not just the backward-looking results but the forward guidance that accompanied them.

| Metric | Q1 2026 Actual | Analyst Consensus | Beat |

|---|---|---|---|

| Adjusted EPS | $1.37 | $1.27 | +7.9% |

| Revenue | $10.253B | $9.85B | +4.1% |

| Q2 Guidance | ~$11.2B | $10.50B | +$700M |

The single most consequential number in the release is $5.8 billion in data centre revenue, representing 57% year-on-year growth. That segment now accounts for approximately 57% of AMD’s total quarterly revenue, meaning its trajectory effectively sets the floor for the company’s overall growth rate.

Two interlocking drivers produced the result. MI300X GPU demand at hyperscaler scale continued to accelerate, while EPYC server CPU deployments expanded simultaneously. The customer evidence is specific:

CEO Lisa Su stated during the earnings call that the EPYC plus Instinct combination delivers better total cost of ownership than competing configurations in large language model inference benchmarks, a claim aimed directly at procurement teams weighing AMD against Nvidia’s Blackwell generation.

EPYC server CPU share gains in enterprise and cloud represent a complementary growth driver, not a secondary one. Su updated AMD’s CPU total addressable market forecast to 35% annual growth, projecting the market will exceed $120 billion by 2030, up from the 18% growth estimate provided in November. Agentic AI workloads are expanding CPU demand alongside GPU demand, and Intel’s ongoing competitive pressure from EPYC suggests these share gains are structural rather than cyclical.

AMD guided Q2 revenue to approximately $11.2 billion (plus or minus $300 million). The analyst consensus sat at $10.50 billion, meaning guidance cleared expectations by roughly $700 million.

The arithmetic makes the magnitude concrete. Implied sequential growth from Q1 is approximately 9.1%. Implied year-on-year growth is approximately 50.6%. Both figures indicate that management expects the Q1 acceleration to continue rather than moderate.

Lisa Su projected more than 70% year-on-year server revenue growth in Q2, the specific mechanism underlying the guidance beat.

Forward guidance is where earnings reports either sustain a stock rally or cut it short. The after-hours re-rating was anchored in the Q2 outlook, not just backward-looking results. A $700 million guidance beat gives the market confidence that the demand curve AMD is riding has months of runway ahead of it.

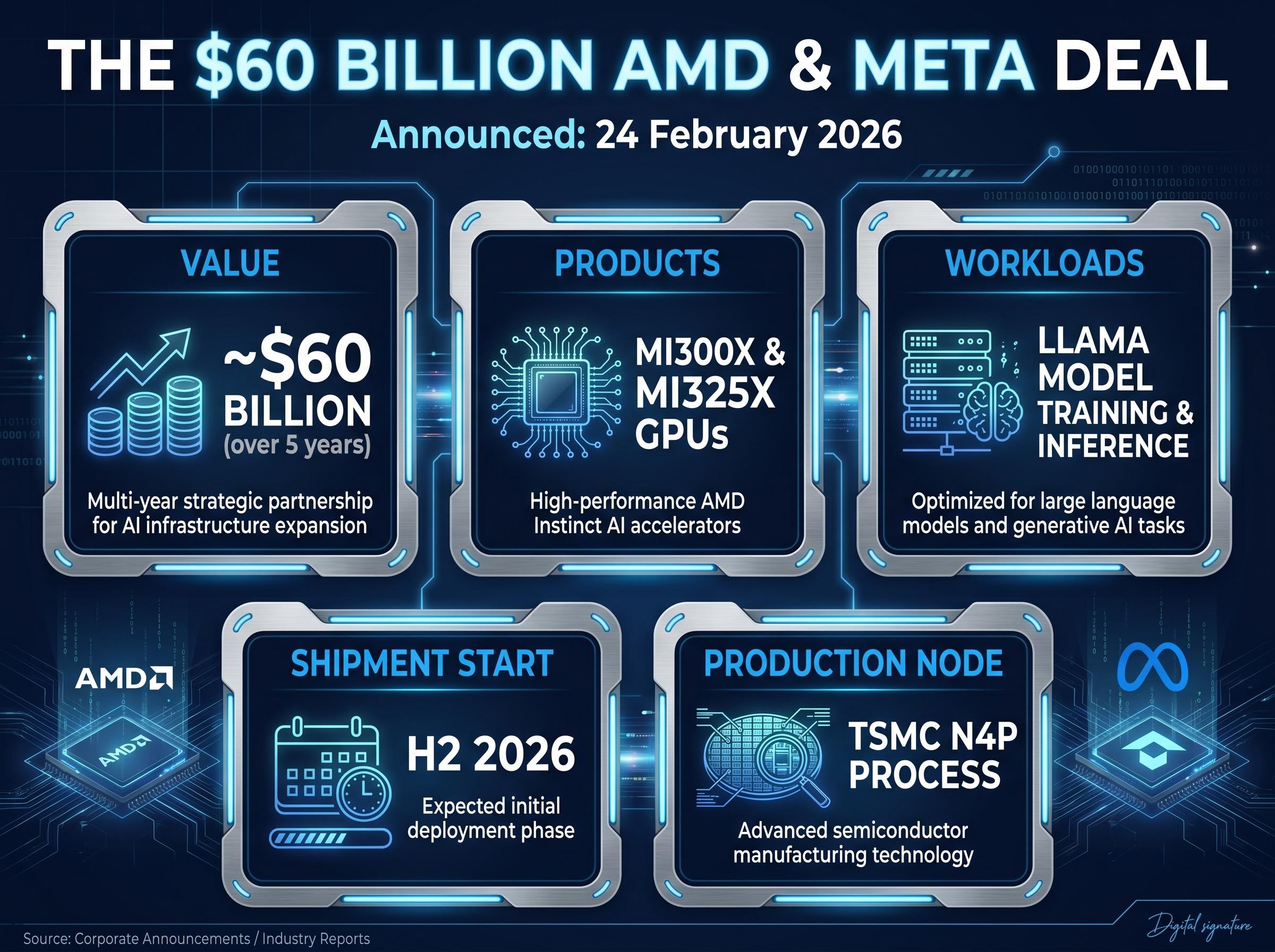

The $60 billion Meta chip supply agreement was announced on 24 February 2026, not on the earnings call. What 5 May provided was confirmation that shipments remain on schedule, reinforcing the deal’s role as a multi-year revenue anchor rather than a headline partnership.

The deal’s parameters frame its scale:

Goldman Sachs characterised the agreement as de-risking a significant portion of AMD’s 2027 revenue. JPMorgan framed it as validation that AMD has reached approximately 20% AI GPU market share.

The AI monetisation timeline from infrastructure deployment to cloud revenue materialisation spans multiple years, a dynamic that helps explain why AMD’s contractually anchored Meta deal carries disproportionate analytical weight: it converts uncertain future demand into scheduled shipment obligations, compressing the typical gap between capex commitment and recognised revenue.

For investors assessing earnings durability beyond a single quarter, the Meta deal provides a tangible demand floor. Hyperscalers are actively building AMD into their AI infrastructure architecture at the largest procurement scale, and that commitment is contractually locked rather than implied.

The market’s running verdict on the competitive shift underway is visible in year-to-date equity performance. AMD has gained 65.9% through 5 May 2026. Nvidia has gained 5.4%. The S&P 500 has returned 6.1%.

Semiconductor equities converting hyperscaler procurement into durable revenue growth are the central beneficiary of the AI hardware capex cycle, with infrastructure spending projected to consume up to 90% of major tech firms’ operating cash flow by 2027, a concentration that creates both exceptional tailwinds and meaningful concentration risk for investors holding hardware suppliers.

| Index / Company | YTD Performance (as of 5 May 2026) |

|---|---|

| AMD | +65.9% |

| Nvidia | +5.4% |

| S&P 500 | +6.1% |

CFO Jean Hu noted during the earnings call that data centre growth was partly enabled by Nvidia supply constraints at hyperscale, with customers actively seeking alternative GPU capacity. The context matters: Alphabet, Microsoft, and Meta all reported results in the prior week, reaffirming or increasing AI infrastructure capital expenditure and validating the demand environment that AMD is supplying into.

Wedbush analyst Dan Ives described the data centre results as further validation of the AI investment thesis, reiterating a $500 price target.

The client and gaming segments contributed $3.61 billion in combined revenue (+23% year-on-year), providing a secondary growth lane. AMD itself flagged potential near-term softness tied to rising memory component costs, a risk worth monitoring in coming quarters.

IDC semiconductor market growth projections place AI infrastructure spending as the primary driver pushing the global semiconductor market past the trillion-dollar threshold, a macro tailwind that directly enlarges the addressable pool AMD is competing for across both GPU and EPYC CPU product lines.

A 57% year-on-year growth figure in data centre revenue carries more weight than it might in a consumer business, and understanding why requires a brief look at how hyperscaler chip procurement works.

GPU revenue (from products like the MI300X) is driven by training and inference workloads. Deals tend to be large, lumpy, and high-margin, structured around specific AI model deployments. CPU revenue (from EPYC processors) is stickier and more predictable, tied to ongoing infrastructure refresh cycles. In practical terms, GPUs accelerate the matrix mathematics underlying AI model training and inference; EPYC CPUs handle orchestration, memory management, and non-AI compute surrounding those workloads.

The procurement cycle at hyperscaler scale follows a general sequence:

This is why Su’s TCO claim carries strategic weight. At hyperscaler scale, procurement decisions are not made on peak benchmark performance alone; they are made on cost per inference, power efficiency, and software ecosystem maturity.

AMD’s updated CPU total addressable market forecast (to exceed $120 billion by 2030 at 35% annual growth) reflects the expanding role of CPUs in AI-adjacent workloads. Agentic AI applications require substantial CPU compute alongside GPU acceleration, and Intel’s competitive weakness in server processors means AMD’s EPYC share gains appear structural. The GPU roadmap (MI350 available 2025, MI400 available 2026, MI500 targeted 2027) ensures that the competitive proposition improves annually rather than resting on a single-generation win.

Three signals define the Q1 report: data centre revenue at $5.8 billion (up 57%), Q2 guidance of $11.2 billion clearing consensus by $700 million, and the $60 billion Meta deal providing multi-year demand visibility. Together, they explain why approximately 38 analysts hold Buy ratings against just 5 Holds.

The risks are real and worth stating plainly:

Investors weighing AMD’s execution record against the risk register should also factor in generative AI profitability concerns that sit upstream of AMD’s customer base: escalating inference costs are putting pressure on hyperscaler unit economics, and a procurement deceleration driven by unprofitable AI application deployment would flow directly into chip supplier order books regardless of competitive positioning.

The question the next quarter will answer is whether $11.2 billion is a conservative floor or a stretch target. The Meta supply anchor, the hyperscaler capex commitments, and the EPYC share gains all suggest the former. Execution over the next 90 days will determine whether the market agrees.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AMD reported Q1 2026 revenue of $10.253 billion, beating the analyst consensus of $9.85 billion by roughly 4%, with adjusted EPS of $1.37 against a consensus estimate of $1.27, and record free cash flow of $2.6 billion.

AMD guided Q2 2026 revenue to approximately $11.2 billion (plus or minus $300 million), which cleared the analyst consensus of $10.50 billion by roughly $700 million and implies approximately 50.6% year-on-year growth.

Announced on 24 February 2026, the agreement covers approximately $60 billion in MI300X and MI325X GPU supply over five years to support Meta's Llama model training and inference infrastructure, with shipments scheduled to begin in H2 2026.

AMD's data centre segment generated $5.8 billion in revenue in Q1 2026, representing 57% year-on-year growth and accounting for approximately 57% of the company's total quarterly revenue.

Through 5 May 2026, AMD shares had gained 65.9% year to date, significantly outperforming Nvidia's 5.4% gain and the S&P 500's 6.1% return over the same period.