US Strikes 60 Iran Targets as Brent Crude Breaks $80

17 hrs ago

Three of enterprise software’s most recognised names, IBM, ServiceNow, and Salesforce, each shed meaningful market capitalisation in premarket trading on 9 July 2026. The catalyst was a report that Starbucks had begun constructing its own AI-powered software tools, raising the prospect that a major enterprise customer was moving away from third-party vendors.

The report landed on a sector already sensitive to AI-driven demand erosion throughout 2026. The premarket moves reflect not just a single news item but an investor community actively repricing a structural question: what happens to enterprise software vendors when their largest customers start building rather than buying?

Here is the distinction that matters. What Starbucks is actually doing, what the market feared it was doing, and why the gap between the two matters less than the broader structural dynamic now sitting underneath enterprise software valuations. That separation shapes how you read the next earnings cycle for every major software name.

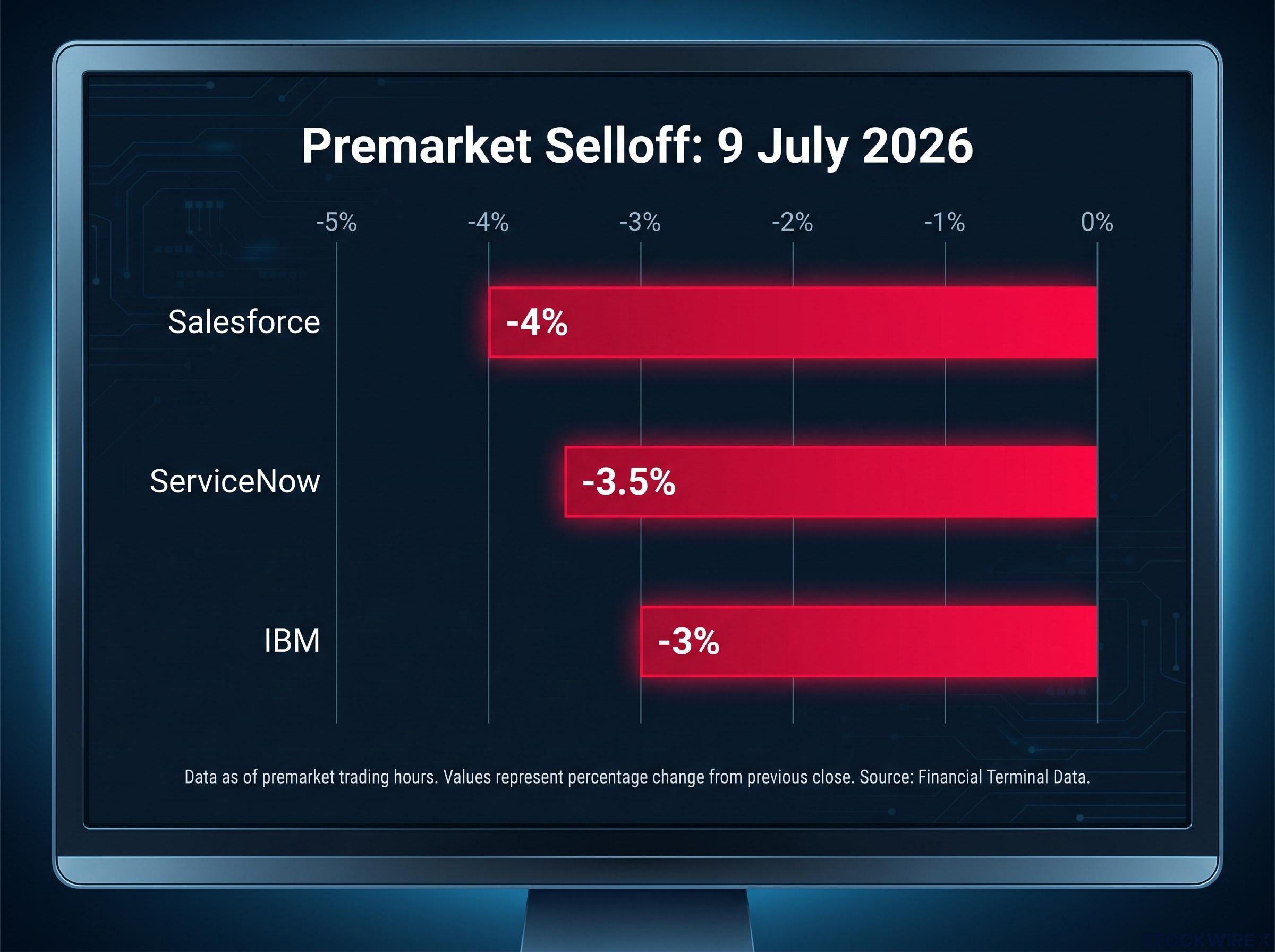

The premarket damage on 9 July 2026 was swift and concentrated.

| Stock | Premarket Move | Date |

|---|---|---|

| IBM | –3% | 9 July 2026 |

| ServiceNow | –3.5% | 9 July 2026 |

| Salesforce | –4% | 9 July 2026 |

According to Investing.com reporting by Sam Boughedda, the moves followed coverage of Starbucks reportedly constructing its own AI-driven software, with investors reading the news as a signal that major enterprises are shifting toward homegrown solutions rather than continuing to purchase them from established vendors.

The speed of the reaction is itself a data point. Three major-cap stocks moved 3-4% before the open on a single suggestive report.

Important caveat: No public reporting confirms that Starbucks is replacing CRM platforms such as Salesforce, abandoning workflow platforms such as ServiceNow, or dismantling core IBM software relationships. The stock moves reflect investor sentiment about a plausible scenario, not a documented corporate decision.

That distinction matters. Enterprise software valuations are now sensitive enough to AI displacement narratives that a single unsubstantiated story can reprice billions of dollars of market capitalisation before most investors have finished their morning coffee.

The 9 July moves sit within a broader software sector selloff that has pushed more than 75% of software application companies into negative year-to-date territory in 2026, with Morningstar formally downgrading the economic moats of Salesforce and ServiceNow in April citing generative AI as a structural threat to switching costs.

Starbucks is deploying AI across four documented systems, all focused on store-level operations rather than enterprise platform replacement:

The platform partner for every documented AI initiative is Microsoft. Not a displacement of Salesforce, ServiceNow, or IBM. The actual evidence points toward hyperscaler consolidation, where a major enterprise deepens its relationship with a cloud platform provider, rather than a broad retreat from enterprise software vendors.

Early results sit firmly at the store-operations layer. Starbucks reports that 80% of in-cafe orders are now completed in under four minutes, a metric tied to the company’s broader operational turnaround narrative.

That is meaningful operational progress. It is also a different category entirely from the enterprise software infrastructure (customer relationship management, IT service management, enterprise resource planning) that IBM, Salesforce, and ServiceNow primarily serve. The market conflated the two on 9 July. The evidence does not support that conflation.

Starbucks did not just build AI tools. It also abandoned one.

The AI-powered Automated Counting tool, part of the NomadGo system using computer vision for inventory management, was deployed across more than 11,000 North American locations beginning approximately September 2025. By approximately May 2026, it was gone.

“Effective immediately, Automated Counting will be discontinued.” — Starbucks internal communications

Publicly, Starbucks cited a desire to “standardise inventory counting” and emphasised daily replenishment and supply chain improvements instead.

A company willing to deploy, scale, and then publicly abandon an AI tool across 11,000 locations is demonstrating something the displacement narrative often glosses over: enterprise AI failure is a real outcome, not a theoretical risk. That changes the probability distribution on how many other in-house enterprise AI projects will reach durable scaled deployment. Some will succeed. Some will end up back at manual counting.

Enterprise AI pilot failure rates run at an estimated 70-80% across large organisations, with poor data integration cited as the primary cause, a base rate that makes the Starbucks inventory miscounting outcome far more representative of sector-wide experience than the displacement narrative implies.

The investor concern is structurally legitimate, even if the 9 July trigger lacked substantiation.

AI-assisted development tools, including code copilots, low-code builders, and domain-specific agents, are genuinely lowering the cost and time required for large enterprises with strong engineering teams to build custom internal software. Those tools shorten development timelines, reduce initial build costs, and allow companies to tailor solutions to proprietary data and workflows that off-the-shelf platforms cannot match.

That is the case for why the moat around enterprise software vendors has narrowed. It is real, and it is directionally supported by the trajectory of AI development tooling throughout 2026.

Narrowed is not the same as gone, and the distinction is worth understanding.

AI agents executing multi-step enterprise workflows depend on systems of record for authoritative data, a structural dependency that makes incumbent platforms infrastructure for AI deployment rather than obvious targets for displacement, particularly where deep compliance configurations and integration layers have accumulated over years.

AI solutions also risk amplifying existing process or data dysfunction rather than resolving it. The Starbucks inventory miscounting failure illustrates exactly this: computer vision applied to a messy physical environment produced results worse than manual counting.

The honest investor position is this: the moat is narrowing, not gone. What that means for you is that renewal rates and net revenue retention in upcoming earnings cycles are the metrics to watch, rather than treating today’s premarket move as either confirmation or dismissal of a structural shift.

IBM, Salesforce, ServiceNow, and Microsoft are all investing in AI-native versions of their platforms, positioning themselves as the lower-friction path for enterprises seeking AI capabilities within existing systems. If enterprises adopt AI primarily within vendor platforms rather than building competing alternatives, the incumbents are absorbing the threat rather than being displaced by it.

The four metrics worth tracking in upcoming earnings cycles, in priority order:

| Signal | What It Would Confirm |

|---|---|

| Declining renewal rates | AI-driven DIY is producing real customer churn, not just investor anxiety |

| Softening net revenue retention | Existing customers are spending less, consistent with partial self-sufficiency |

| Rising pilot discontinuation ratio | Enterprise AI builds are failing at scale, potentially reinforcing vendor demand |

| Strong vendor AI platform adoption | Incumbents are successfully absorbing the AI threat within their own ecosystems |

Until those metrics surface in earnings calls, the 9 July moves are best read as sentiment rather than confirmation.

The market reaction was real. IBM, ServiceNow, and Salesforce each lost 3-4% before the opening bell, and the underlying structural concern about AI-enabled enterprise self-sufficiency is legitimate and building.

But the specific Starbucks-to-vendor displacement story that triggered the selloff lacks substantiation. What Starbucks is building sits at the operational edge, demand intelligence, order sequencing, barista support, not at the enterprise platform layer where these vendors generate their revenue. And the one AI system Starbucks scaled most aggressively was abandoned within nine months.

What the 9 July premarket session demonstrated is how quickly AI-driven enterprise self-sufficiency narratives can move major-cap software stocks, regardless of whether the triggering evidence holds up. You now have the framework to separate confirmed structural shift from sentiment-driven pricing. The metrics that will tell you whether the risk has graduated from emerging concern to confirmed headwind are renewal rates and net revenue retention. Watch for those in the next earnings cycle.

For investors wanting to model the valuation context behind the 9 July moves in more depth, our full explainer on SaaS valuation compression examines how the sector reached 9.5x EV/Sales, a full standard deviation below historical norms, despite Q1 2026 revenue growth hitting a three-year high.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The AI threat is the possibility that large enterprises will use AI-assisted development tools to build custom internal software instead of purchasing platforms from established vendors, narrowing the switching-cost moat that has historically protected companies like Salesforce, ServiceNow, and IBM. Morningstar formally downgraded the economic moats of Salesforce and ServiceNow in April 2026 citing generative AI as a structural threat.

All three stocks dropped 3-4% before the open after reports that Starbucks was building its own AI-powered software tools, which investors read as a signal that major enterprises were shifting toward homegrown solutions rather than buying from established vendors. No public reporting confirmed that Starbucks was replacing any of these specific platforms.

Starbucks is deploying four AI systems, Deep Brew, SmartQ, Green Dot Assist, and NomadGo Inventory AI, all focused on store-level operations such as order sequencing and barista support, with Microsoft as the platform partner for every documented initiative. These operate at the operational edge rather than at the enterprise platform layer where IBM, Salesforce, and ServiceNow generate their revenue.

Starbucks deployed its AI-powered Automated Counting tool across more than 11,000 North American locations from approximately September 2025, but discontinued it by approximately May 2026 after frequent miscounting and mislabelling, including confusing types of milk, and reverted to manual inventory counting.

The four metrics to track in upcoming earnings cycles are renewal rates on large enterprise contracts, net revenue retention, the ratio of durable scaled AI deployments to quiet discontinuations, and vendor AI platform adoption rates within existing enterprise accounts. Softening renewal rates or net revenue retention would be the first hard evidence that AI-driven in-house building is producing real customer churn rather than investor anxiety.