Nvidia Slips 2% Premarket as DeepSeek Targets Inference Chips

11 hrs ago

Twelve Federal Reserve officials voted unanimously to hold interest rates steady on 17 June 2026. Then, in the same set of projections, they split almost evenly on whether rates should go higher, stay flat, or fall by year-end.

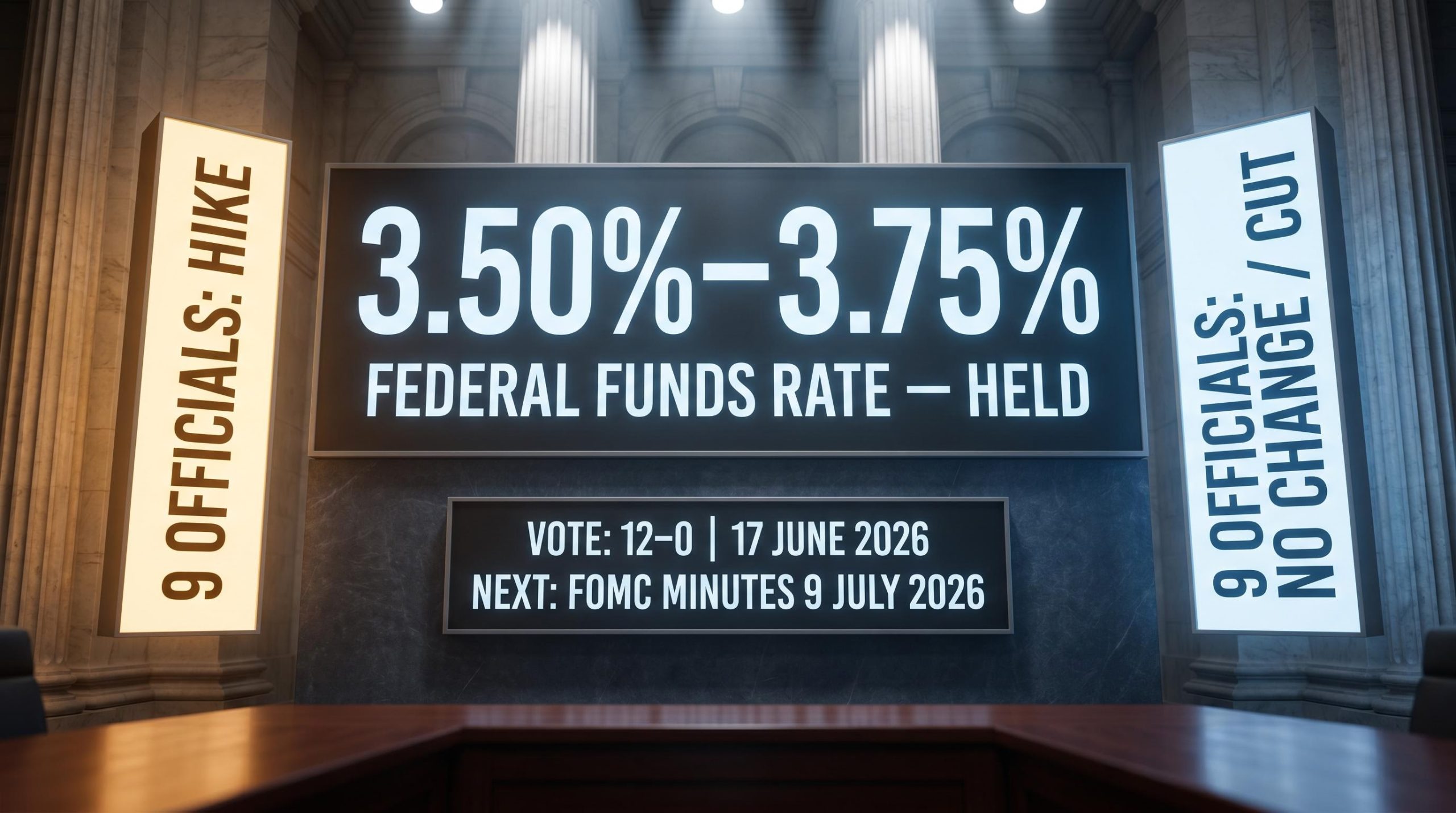

That contradiction sits at the centre of Kevin Warsh’s first meeting as Fed Chair. The decision itself, a fourth consecutive hold at 3.50%-3.75%, was clean. The outlook was anything but. With FOMC minutes scheduled for release on Wednesday, 9 July 2026, this is a live story: markets will parse every sentence for clues about where the committee lands next.

Here is how to separate what the June meeting actually tells you about the path of Federal Reserve interest rates from what it does not, and why that distinction matters before the minutes arrive.

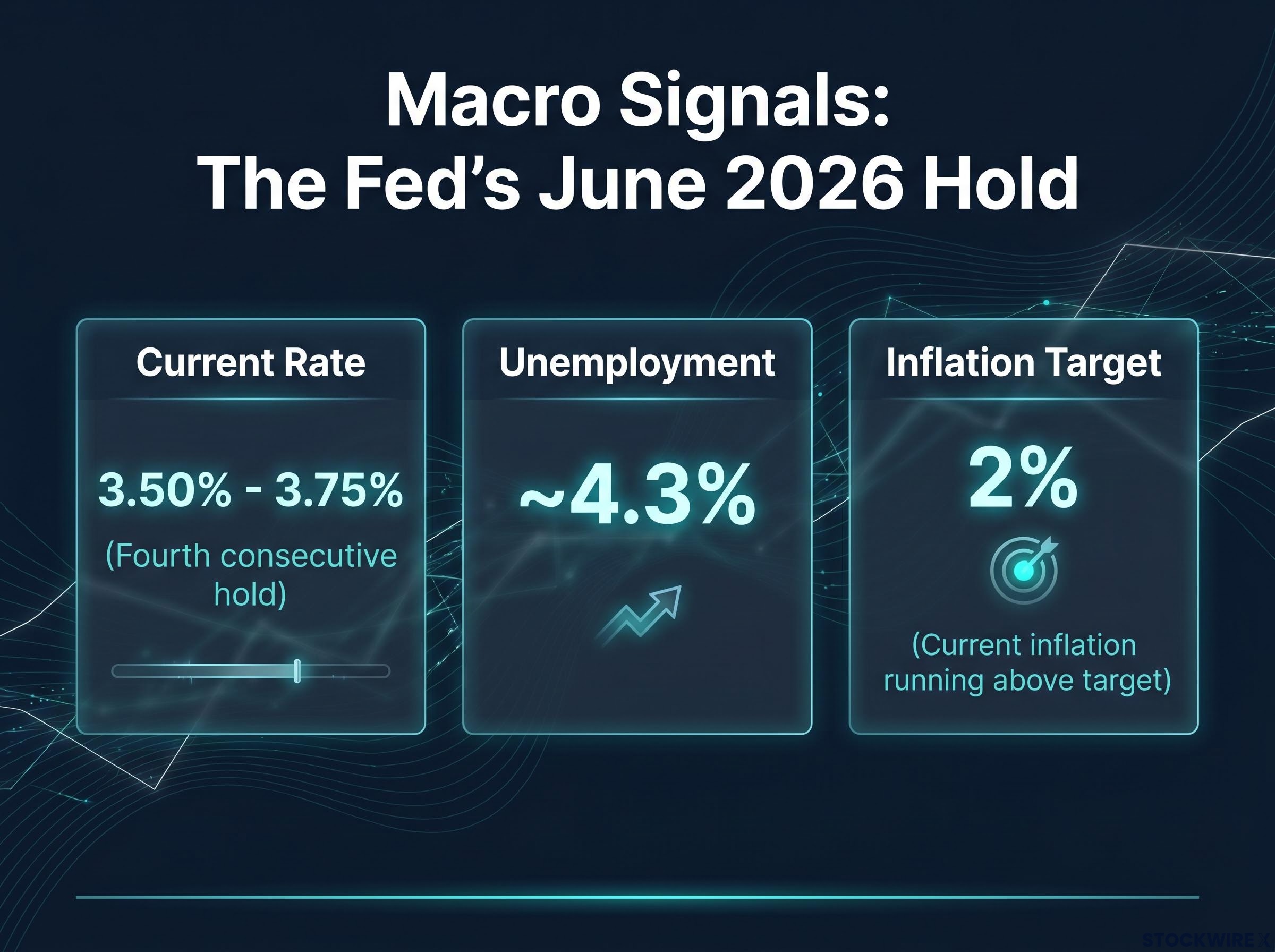

The headline is simple. The federal funds rate held at 3.50%-3.75% on a 12-0 vote at the 16-17 June 2026 meeting, marking the fourth consecutive hold. Every voting member agreed this was the right call for right now.

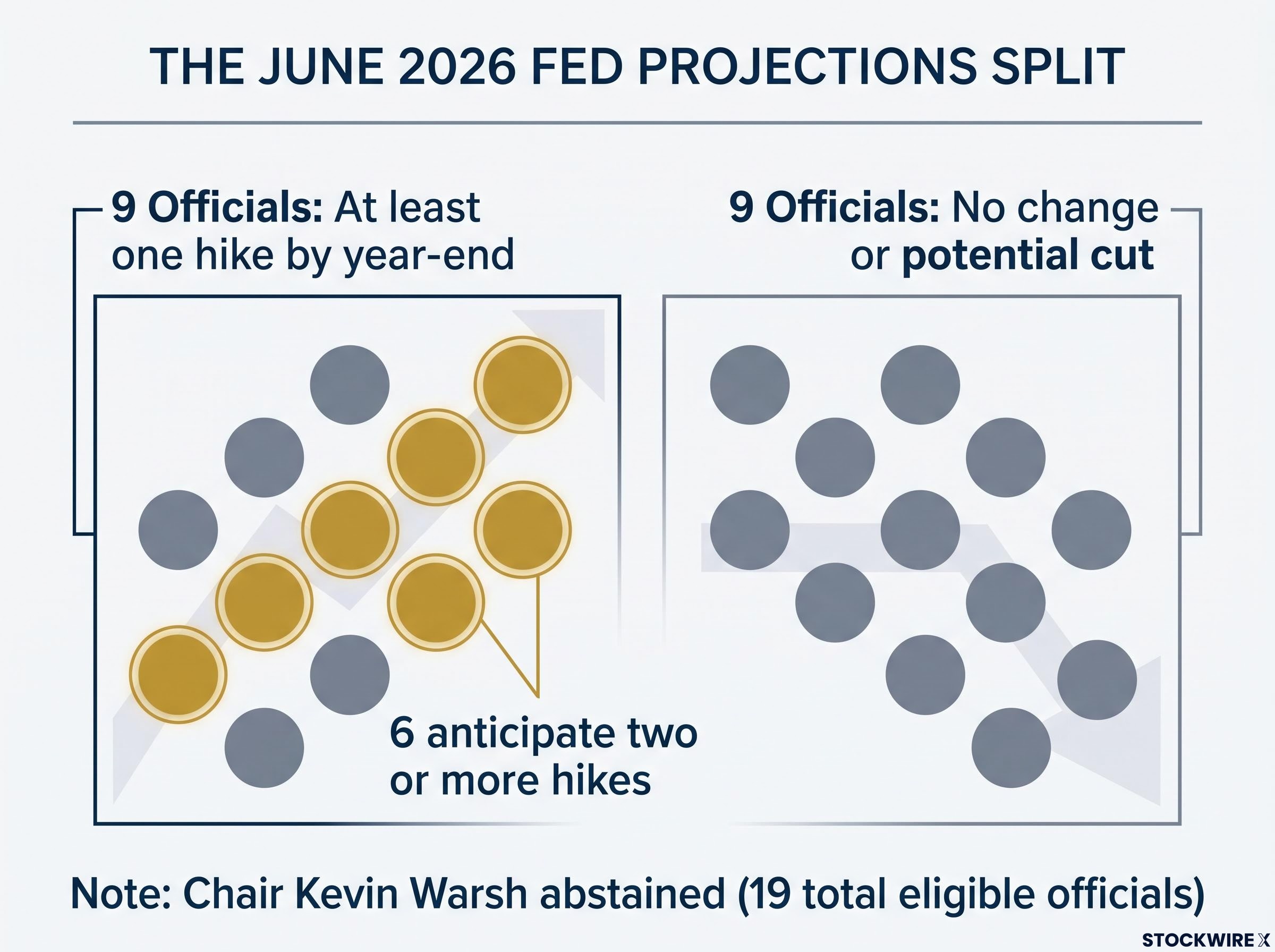

The projections told a different story. Of the 18 officials who submitted dot plot forecasts, those views divided sharply: nine judged that rates should rise by at least one increment before year-end, and six of that group pencilled in two or more hikes. The remaining nine saw no further moves, or even a reduction, as the more appropriate outcome.

The split in one number: nine officials see at least one hike by year-end; nine see no change or a cut. That is as close to a coin-flip as the Fed’s internal compass gets.

The median 2026 rate projection (excluding Warsh, who abstained) rose to approximately 3.75%-3.80%, up from approximately 3.375%-3.40% in March. The policy statement itself was unusually brief, containing no forward guidance, a deliberate choice under Warsh rather than an oversight.

The 130-word policy statement Warsh produced represents a reduction of more than 60% from the 341-word April statement and comes within two words of the all-time modern low set under Greenspan in January 2002, a comparison that frames just how structurally different this communication overhaul is from incremental adjustments made by prior chairs.

| Category | Officials (June) | Median Rate Projection, June (ex-Warsh) | Median Rate Projection (March) |

|---|---|---|---|

| At least one hike by year-end | 9 | ~3.75%-3.80% | ~3.375%-3.40% |

| At least two hikes by year-end | 6 | ||

| No change or potential cut | 9 |

The 12-0 vote tells you the Fed is unified on what to do today. The dot plot tells you there is no shared roadmap for the rest of 2026. Hold both facts simultaneously rather than treating the unanimous vote as a signal of future cohesion.

Of the 19 officials eligible to submit projections, 18 did. The one who did not was the Chair.

Warsh deliberately excluded himself from the Summary of Economic Projections (SEP), the quarterly collection of individual rate forecasts that produces the dot plot. At his press conference, he confirmed that nine participants judged at least one rate increase by year-end would be appropriate, but he offered no indication of where his own view sits. His language centred on the committee’s “capability and commitment” to restore price stability.

That abstention is not an absence. It is a signal. Warsh’s communication choices at this meeting form a coherent pattern:

Together, these choices suggest Warsh intends to lead differently from his predecessors. A Fed Chair who declines to place a dot means markets cannot use the Chair’s own projection as an anchor for rate expectations. For you, that shifts the calculus: weight incoming economic data more heavily and Chair signals less heavily than in recent years. The dot plot becomes a distribution of views, not a centre-of-gravity forecast.

The end of forward guidance is not merely a stylistic preference; Warsh launched five internal task forces at the June meeting, including one specifically reviewing the dot plot’s future role, and the two-year Treasury yield surged 18 basis points intraday on 18 June as markets absorbed the full weight of a policy communication regime that no longer provides a buffer between data releases and rate expectations.

Four meetings without a rate change (including February, April, and June 2026) often gets read as the Fed signalling it is done. That reading is usually wrong, or at least incomplete.

Historically, extended hold periods tend to mean the Fed believes it is near an appropriate plateau for current conditions, not that it has reached a terminal rate. Future moves from a plateau are typically data-driven adjustments, not the start of a rapid new cycle. The common inference that consecutive holds guarantee the next move is a cut rather than a hike has no reliable historical basis.

The macro conditions producing this pause are specific. The Fed’s own language describes economic activity “expanding at a solid pace” while inflation remains above 2%. Unemployment sits at approximately 4.3%. Energy prices remain elevated and are contributing to the inflation picture in ways that rate adjustments alone cannot fully address.

The energy supply shock driving the headline-core inflation divergence operates through two distinct channels: the direct effect of crude prices on gasoline and utilities, which hit quickly, and an indirect transmission through logistics, agriculture, and manufacturing supply chains that operates on a 6-12 month lag and had not yet fully appeared in the June CPI data the committee was reading.

That combination, resilient growth plus above-target inflation, is exactly the environment where the Fed historically parks rates and watches. It is not a wind-down posture. The three macro signals worth monitoring:

The committee’s “unambiguous and unanimous” commitment to 2% inflation restoration means the bar for either a hike or a cut is economic data that clearly justifies the move. Four holds in an environment of resilient growth and above-target inflation means the Fed is watching the data, not winding down. If you are positioning for rate relief because hikes have paused, you are working from an incomplete model.

The minutes from the 16-17 June meeting land on Wednesday, 9 July 2026, following the standard three-week release lag. Before they arrive, it is worth understanding what you are actually reading.

| Likely to find in the minutes | Unlikely to find in the minutes |

|---|---|

| How officials weighted inflation, labour market data, and credit conditions | A binding policy path for September or December 2026 |

| Discussion of risk balances (tilted toward inflation risk vs growth risk) | Resolution of the dot plot split |

| How much weight different members placed on near-term data vs medium-term projections | A single authoritative signal on the next rate move |

A structural limitation worth noting: FOMC minutes are edited summaries rather than word-for-word accounts of what was said. The document is prepared and reviewed before publication, which means significant nuance or dissenting reasoning can be stripped out entirely. What remains reflects the themes the committee collectively decided warranted inclusion, not a complete record of the debate.

The minutes will tell you what the Fed collectively thought mattered most at a specific moment in June. They will not tell you what the Fed will do in September. Treating them as a forward roadmap is a structural misread of what the document actually is. Investors who understand that architecture before they read are less likely to overreact to language that sounds decisive but reflects only one snapshot in a data-dependent process.

Fisher Investments characterises monetary policy as one of many market-influencing variables, with no guaranteed or predetermined market effect. That framing matters here.

The practical point: monetary policy is one variable among many, and equity returns have no simple, stable relationship with the absolute level of short-term interest rates. Growth, corporate margins, global risks, and sector trends can matter at least as much as incremental rate changes.

Trading around Fed language is a structurally difficult proposition. Markets generally price broadly expected policy moves well in advance. The committee itself is not unified about the path ahead, which means noise is high relative to signal. Rebuilding or rebalancing a portfolio solely around Fed guesses introduces risk without a reliable payoff.

The constructive alternative comes down to three principles:

For a long-term investor, the most important implication of this divided Fed is not which way rates move next, but that there is no edge in trying to front-run a committee that itself lacks consensus. Discipline around fundamentals is more valuable than Fed-watching precision.

For readers wanting to understand the structural case for why Fed-watching precision rarely pays off, our dedicated guide to Fed policy limitations covers the long and variable lags in monetary transmission, the distinction between nominal and real effects, and the historical episodes where Fed actions destabilised as powerfully as they stabilised.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The 9 July minutes may shift market pricing modestly in either direction if they reveal unexpected emphasis on inflation risks or growth concerns. That is normal. It is not a reason to reposition.

What the minutes cannot change is the fundamental division inside the committee, the data-dependent uncertainty, or the appropriate investor posture. The core takeaway from Warsh’s first meeting is not a rate forecast but a posture: the Fed is unified on its destination (2% inflation) and divided on the road.

The forward-looking question is not “when will the Fed cut or hike?” It is “what economic data would need to arrive between now and September to shift the committee’s internal consensus?” The September 2026 meeting is the next significant decision point, and the bar for a dramatic pivot remains high given the committee’s unanimous inflation commitment.

Three variables are worth monitoring between now and then:

After the minutes, your job is not to update a rate forecast. It is to note whether the internal debate shifted materially toward hawks or doves. That shift, not the minutes language itself, is what actually changes the probability distribution for September.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Federal Reserve held the federal funds rate at 3.50%-3.75% at its 16-17 June 2026 meeting, marking the fourth consecutive hold and a unanimous 12-0 vote.

Nine officials projected at least one rate hike by year-end and nine projected no change or a cut, a near-perfect 50-50 split that signals the committee has no shared roadmap for the rest of 2026.

Warsh deliberately abstained from submitting a dot plot projection to avoid anchoring market expectations to a Chair-endorsed rate path, a deliberate shift that means investors can no longer use the Chair's own dot as a centre-of-gravity forecast.

The minutes will show how officials weighted inflation, labour market data, and credit conditions, but they will not resolve the dot plot split or provide a binding policy path for September or December 2026.

With the committee split and data-dependent, investors are better served monitoring inflation prints and labour market reports as the direct rate drivers, rather than repositioning around Fed statements that reflect a committee without internal consensus.