Asian Chip Stocks Split: SK Hynix Falls 4.3%, Hon Hai Gains

1 min ago

The assumption most investors carry right now about artificial intelligence and enterprise software goes something like this: AI can rebuild any SaaS product faster and cheaper than the incumbent can defend it. The prototyping evidence looks convincing. Code assistants can generate working applications in hours. Foundation models can replicate interfaces, automate workflows, and produce functional software at a fraction of the historical cost.

The uncertainty is real, and it is already priced in. SaaS multiples in mid-2026 are being evaluated against a disruption thesis that treats every enterprise software company as a potential casualty. Billions of dollars in market capitalisation sit on one side or the other of a single question: does AI replace these platforms, or does it need them?

The trillion-dollar SaaS selloff of February 2026 crystallised the disruption thesis into a market event, as institutional capital rotated away from established software vendors toward pure-play generative AI names, compressing multiples across the sector regardless of individual company fundamentals.

Here is the analytical lens you need before making that call. This piece works through the actual mechanism of AI’s impact on enterprise software, covering which platforms are structurally protected, which face genuine displacement risk, and what the distinction means for how you assess SaaS investments today.

The ability to prototype software quickly using AI tools is real. Nobody disputes that. But the leap from “AI can build a version of this” to “an enterprise will replace its system of record with that version” skips over everything that actually determines whether large organisations switch core infrastructure.

Box CEO Aaron Levie has drawn this distinction directly: building a functional prototype with AI tools is categorically different from the governance and accountability requirements of production enterprise software. Enterprise systems of record are not evaluated on whether they technically function. They are accountable to regulators, auditors, supply chains, and legal obligations.

What these systems must satisfy:

Switching costs are organisational, legal, and operational: retraining staff, redoing audits, rewriting integrations, revalidating compliance. RBC Capital Markets characterised vertical SaaS platforms with deep domain expertise and regulatory knowledge as “likely to be viewed as ‘AI-proof’ (for now),” precisely because replicating that embedded context is far harder than rebuilding a feature. AI-generated code also carries higher rates of subtle logic and security errors, requiring more human review, not less. The gap between building something and trusting something is the entire argument.

A system of record is a platform that holds authoritative data other systems, regulators, auditors, and customers depend on. When your ERP stores the financial transactions your auditors sign off on, or your healthcare platform holds the patient records your compliance team certifies, that platform is not just software. It is the single source of truth for an entire organisational chain.

Regulated and high-stakes workflows, in healthcare, finance, insurance, and the public sector, create a fundamentally different risk calculus for switching decisions. The question is never “can we find a better product?” It is “can we afford the regulatory, operational, and legal cost of switching, and can we guarantee the new system meets every obligation the old one does?”

Years of configurations, certifications, and organisation-specific workflows compound that cost. RBC Capital Markets’ analysis positions industry-specific platforms with regulatory knowledge and hard-coded workflows as having a moat that is harder to replicate than rebuilding an interface.

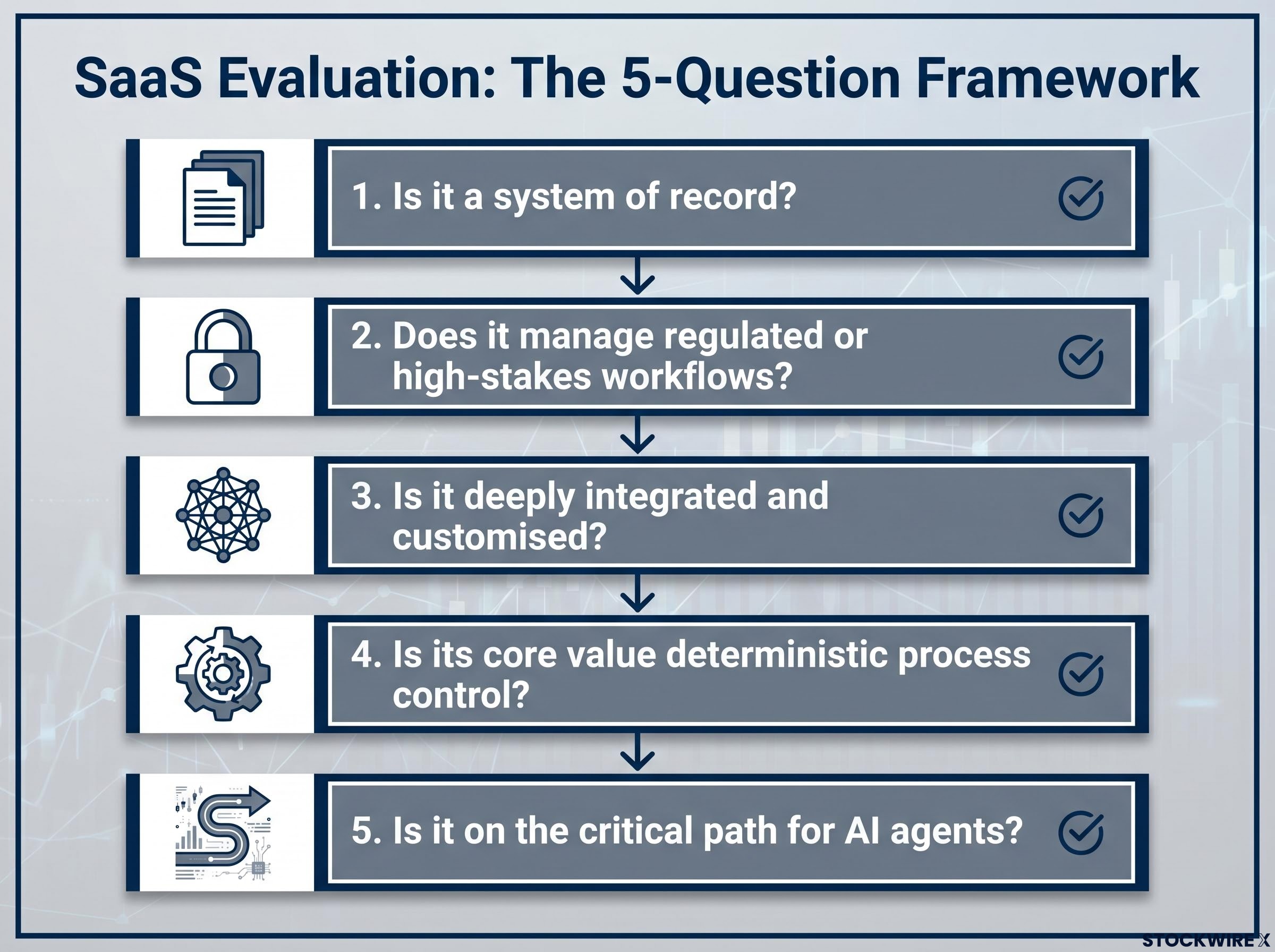

A five-question framework gives you a practical way to evaluate any SaaS company against this standard:

The categories facing genuine displacement risk look structurally different. Software that mainly provides surface-level information retrieval, basic content generation, or lightweight automation without deep workflow integration overlaps directly with what foundation models already do well.

| System of record characteristics | Displacement-risk characteristics |

|---|---|

| Holds authoritative data regulators and auditors depend on | Presents or retrieves generic, widely available information |

| Manages regulated workflows with legal or financial consequences | Automates tasks easily expressed as prompts or simple scripts |

| Deeply integrated with years of custom configurations and certifications | Minimal integration depth; operates as a standalone layer |

| Provides deterministic process control with audit trails | Provides generic Q&A or content generation without structured governance |

| Required by AI agents as a data source to execute workflows | Functionality replicable by foundation models out of the box |

If you can apply this distinction to every SaaS company you evaluate, you have a framework that separates durable platforms from vulnerable ones.

The disruption narrative runs in one direction: AI threatens enterprise software. The data runs the other way.

AI agents executing multi-step tasks are only useful when they operate on authoritative, real-time data. In large organisations, that data lives in four places:

Enterprise AI adoption failure rates tell the same story from the demand side: an estimated 70-80% of enterprise AI pilots fail or stall, with poor data integration cited as the primary cause, which is precisely why the platforms holding authoritative, integrated data are positioned as infrastructure rather than displacement targets.

Levie made the dependency explicit: for AI agents to carry out useful work inside enterprise environments, they must be able to read data from existing systems while operating within defined permission boundaries, data access rules, and the kind of deterministic workflow structures that prevent agents from making unauthorised changes to core business records. The Anthropic Claude integration launching within Slack, with Box as an accessible data source, is real-world evidence that AI intelligence layers are being built on top of existing infrastructure rather than replacing it.

The deterministic and non-deterministic divide: Enterprise SaaS provides rule-based, predictable workflows with strict access controls and audit trails. AI agents provide probabilistic reasoning, synthesis, and natural language interfaces. They are complementary layers, not competing ones. AI sits on top of systems of record to interpret and orchestrate; it does not remove the need for those systems to store, validate, and execute authoritative transactions.

Box has reported increased platform usage as AI agents access stored documents and data. According to RBC’s analysis, vertical SaaS vendors are positioned to provide both the raw data and the domain-specific context needed to train models for particular industries. Every enterprise AI deployment that succeeds makes the underlying system of record more entrenched, not less. That is the opposite of what most disruption narratives predict, and it has direct valuation implications: if AI adoption accelerates demand for incumbent platforms, AI is a demand driver for these companies, not a competitive threat.

Traditional SaaS pricing has been seat-based: per user, per month. That model fits human users. It does not fit AI agents and background automation that generate far more platform activity than people do but occupy zero seats.

Levie identified this shift directly, describing the monetisation of agentic AI usage as likely to move toward consumption-based pricing, where revenue aligns with actual usage: API calls, data volume, transactions processed.

Per-seat pricing displacement is already measurable in the field: one documented enterprise case reduced a SaaS analytics product from 20 seats to 3 via natural language AI interfaces, achieving a 90% reduction in software spend and demonstrating how quickly consumption-based models can erode the revenue base of vendors still tied to headcount pricing.

Levie on the pricing shift: As AI agents proliferate within enterprise customers, the value they generate maps to consumption, not headcount. Platforms already moving toward consumption models are positioned to capture that revenue directly.

The industry is already moving. According to OpenView Partners data, approximately 61% of SaaS companies had adopted some form of usage-based pricing by 2023, up from 49% in 2020. The directional trend toward consumption models has continued into 2025-2026.

| Model | Fit for AI agents | Revenue consequence |

|---|---|---|

| Seat-based | Poor: AI agents do not occupy seats but generate high platform activity | Usage growth from AI agents goes unmonetised under per-user contracts |

| Consumption-based | Strong: revenue scales with API calls, data volume, and transactions regardless of user type | AI-driven usage translates directly to incremental revenue at high margins |

Because the compliance and security infrastructure already exists, the marginal cost of additional AI-driven usage is low. That means high incremental margins on every additional API call or data query an AI agent runs through the platform. For investors, this is the mechanism that converts the structural resilience argument into a revenue growth thesis. It separates a defensive case (“AI will not kill this”) from a growth case (“AI will actually accelerate this”).

The theoretical argument for AI as a demand driver is one thing. The empirical data is another, and it is arriving.

The Google Cloud “The ROI of Generative AI” report found that 74% of enterprises using GenAI report positive ROI. Among those with GenAI in production, 86% report revenue growth of 6% or more annually. That data, reflecting surveys through 2024-2025, tells you that enterprise AI adoption is sustaining software spending, not displacing it.

The Google Cloud enterprise AI ROI survey, covering global business leaders through 2024-2025, found that 74% of enterprises using GenAI report positive ROI, with 86% of those in production reporting annual revenue growth of 6% or more, a data set that directly contradicts the displacement narrative.

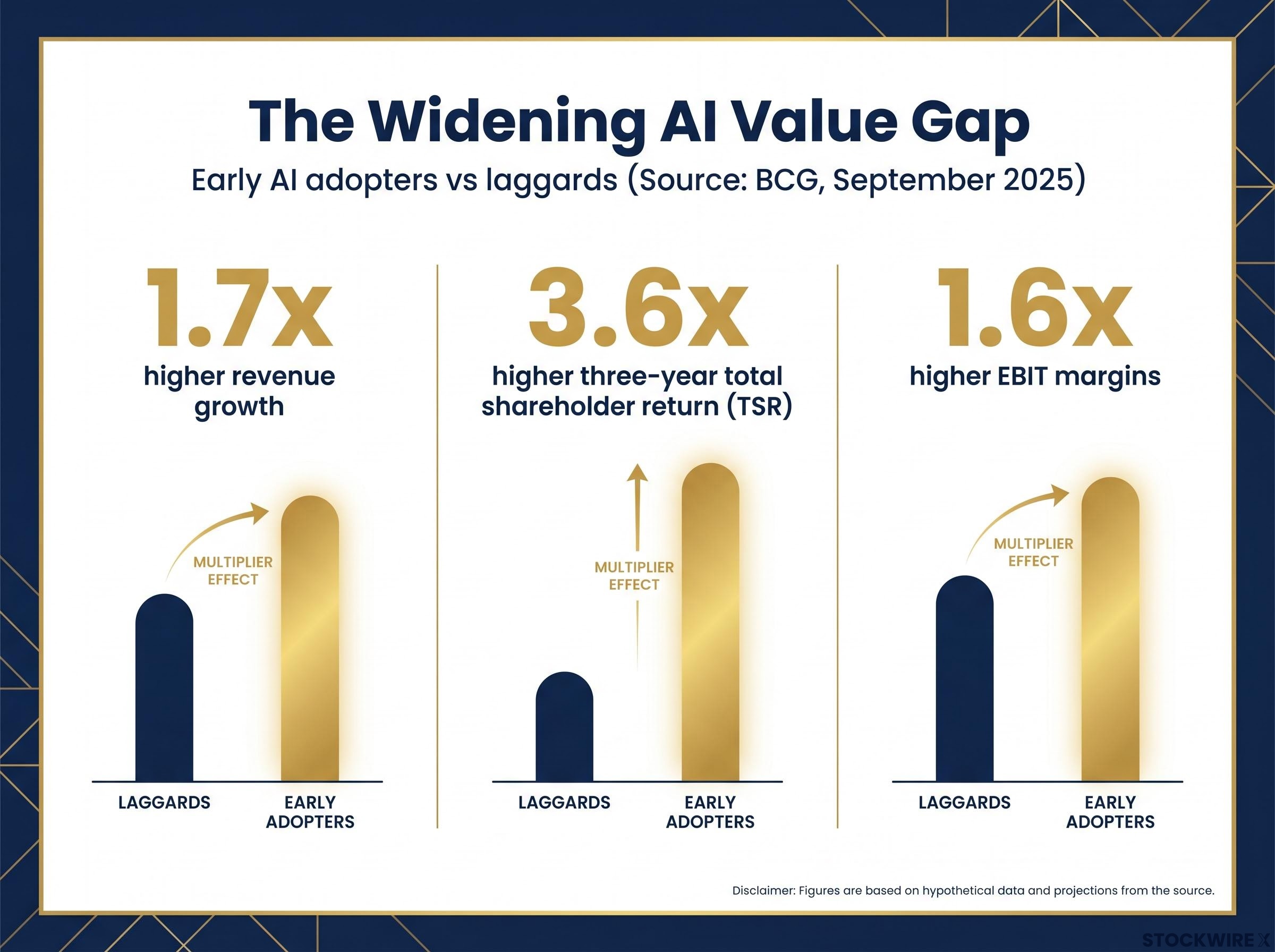

The BCG “The Widening AI Value Gap” study, published in September 2025, sharpens the picture further. Early AI adopters outperform laggards across every financial metric that matters:

The BCG TSR premium: Early AI adopters delivered 3.6x higher three-year total shareholder return than AI laggards. That tells you the platforms enabling enterprise AI workflows are not just defensively stable; they are attached to the companies generating the highest returns in the market right now.

In discussion of how the market is pricing enterprise software with strong AI-driven dynamics, HubSpot was cited as a concrete reference point: trading at roughly 2.5x annual revenue while delivering approximately 30% annual revenue growth. That combination of growth rate and multiple, in an enterprise software company positioned on the critical path for AI-enabled customer workflows, gives you a live reference point for how the market is pricing the beneficiary cohort.

The right question for investors assessing SaaS multiples is not “will AI hurt this platform” but “is this platform on the critical path for enterprise AI deployments.” The answer determines whether the company is a beneficiary of the AI boom or a casualty of it.

Economic moat ratings for AI positions have become the institutional standard for separating structural winners from thematic rally beneficiaries: at mid-2026 prices, the Morningstar US Technology Index has shrunk its discount to fair value from 25% to just 7%, meaning the margin of safety that existed in March 2026 for undifferentiated AI exposure has largely been spent.

The core argument runs through five layers. For platforms that are systems of record with regulatory entrenchment, AI is structurally more likely to drive usage and revenue than to enable replacement. AI agents depend on these platforms for authoritative data. Consumption-based pricing converts that dependency into direct revenue. And the empirical data on enterprise AI ROI confirms that adoption is accelerating spending, not cannibalising it.

The distinction matters for how you categorise your holdings. Systems of record with the five characteristics sit in the beneficiary cohort. Platforms offering generic retrieval or lightweight automation without deep workflow integration carry genuine displacement risk.

Levie’s broader conviction reinforces the frame: enterprise is the only viable path to building a large independent company in software, and he expects the same concentration to hold for AI revenue. With Box sitting at roughly $4 billion in market capitalisation and Dropbox at roughly $6 billion, these two companies illustrate the scale of the enterprise-first segment, where the pricing evolution toward consumption models is not guaranteed but directionally well supported.

Here is the five-question framework as a decision tool you can apply to every SaaS company you evaluate:

The investor who leaves this analysis asking “is this platform on the critical path for enterprise AI” rather than “will AI replace this platform” has a materially sharper evaluative frame for the SaaS category in 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

A system of record is a platform that holds authoritative data that other systems, regulators, auditors, and customers depend on, such as an ERP storing financial transactions or a healthcare platform holding certified patient records. Because organisations cannot afford the regulatory, operational, and legal cost of switching these platforms, they carry far higher switching costs than ordinary software tools.

AI is structurally more likely to drive usage and revenue for regulated SaaS platforms than to enable their replacement, because AI agents require authoritative, real-time data that lives inside existing systems of record. RBC Capital Markets described vertical SaaS platforms with deep regulatory knowledge as likely to be viewed as AI-proof precisely because replicating embedded compliance context is far harder than rebuilding a feature.

Platforms offering surface-level information retrieval, basic content generation, or lightweight automation without deep workflow integration face the most genuine displacement risk, because their core functionality overlaps directly with what foundation models already do out of the box. The contrast is with systems of record that hold authoritative data and manage regulated workflows with legal or financial consequences.

Consumption-based pricing aligns revenue with API calls, data volume, and transactions processed rather than per-seat headcount, which means AI agents generating high platform activity translate directly into incremental revenue for incumbents. According to OpenView Partners data, approximately 61% of SaaS companies had adopted some form of usage-based pricing by 2023, up from 49% in 2020.

BCG's September 2025 study found that early AI adopters delivered 3.6x higher three-year total shareholder return than AI laggards, alongside 1.7x higher revenue growth and 1.6x higher EBIT margins. That data directly contradicts the displacement narrative and supports the case that platforms enabling enterprise AI workflows are attached to the companies generating the highest returns in the market.