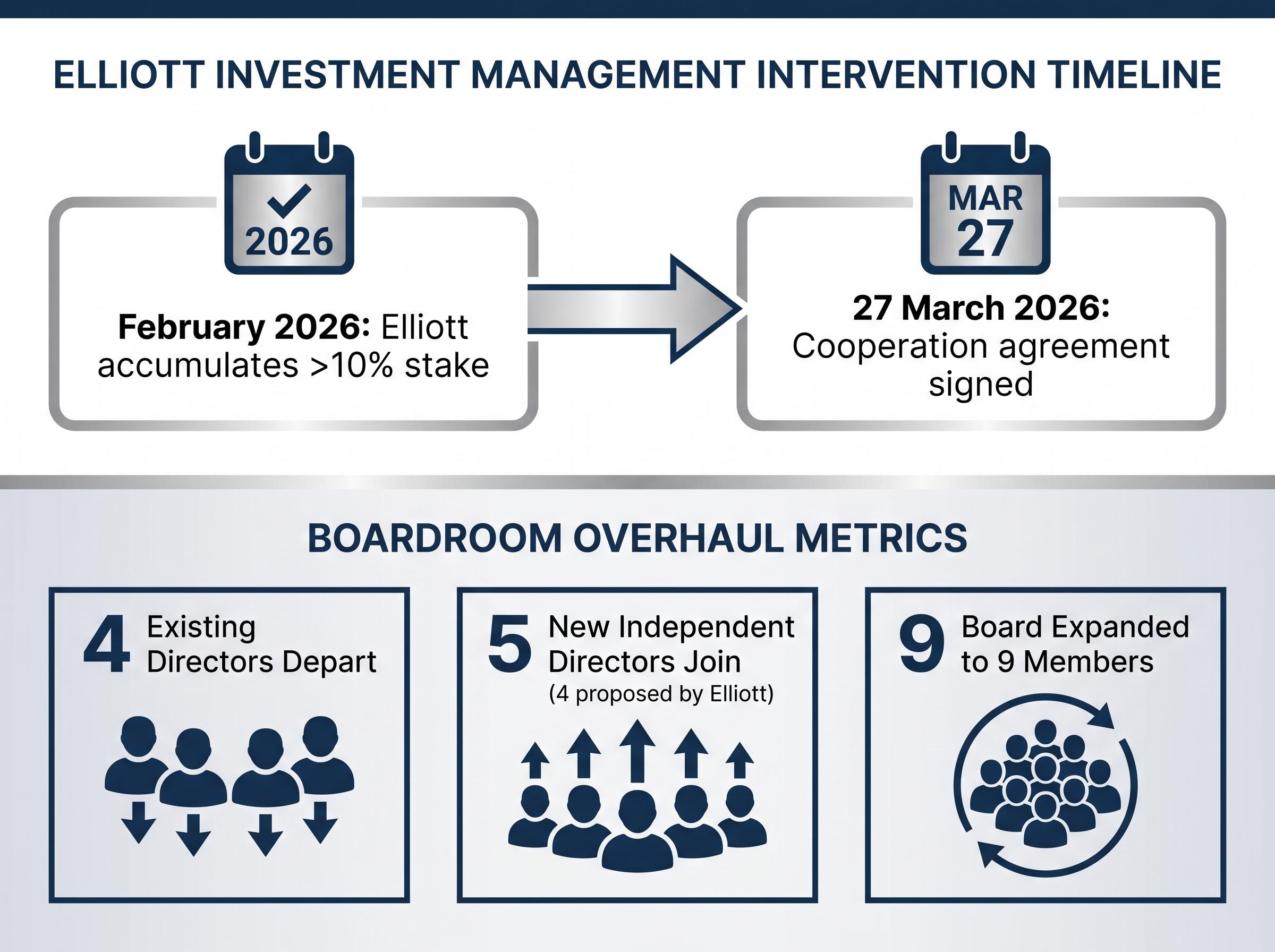

In late March 2026, Elliott Investment Management executed one of the swiftest corporate interventions in recent hospitality history. The firm signed a comprehensive cooperation agreement with Norwegian Cruise Line Holdings, ending a quiet but aggressive accumulation phase.

The financial institution leveraged a massive equity stake to fundamentally rewrite the cruise operator’s leadership structure in a matter of weeks. Activist investing as a strategic approach relies on this exact mechanism, where outside capital forces internal corporate changes rather than passively trading shares. By acquiring enough voting power, outside funds can mandate strategic pivots that existing executives might otherwise avoid.

This intervention provides a real-time educational model for how institutional shareholders address severe corporate underperformance. The Norwegian situation demonstrates the specific mechanics behind these boardroom takeovers, giving retail investors the vocabulary needed to parse Wall Street headlines. Understanding these corporate actions allows shareholders to identify when a lagging stock might become a target for systemic restructuring.

The Catalyst for Intervention: A Half-Decade of Lost Value

Hostile or aggressive corporate moves are the direct mathematical consequence of prolonged shareholder value destruction. According to market data, over the five-year measurement window ending 23 April 2026, Norwegian Cruise Line Holdings saw its equity valuation plummet by 37.8%.

According to market data, during the exact same duration, the broader S&P 500 benchmark generated an 84.3% positive return. This massive disparity highlights the severe opportunity cost for long-term investors who held the stock through multiple operating cycles. In the public markets, prolonged underperformance essentially acts as an open invitation for institutional agitators to step in and demand accountability.

While this broader market benchmark provided strong aggregate returns over the last five years, severe underlying vulnerabilities and macroeconomic warning signals suggest these index-level gains may face significant pressure in the coming quarters.

Five-Year Performance Contrast According to market data, between April 2021 and late April 2026, Norwegian Cruise Line Holdings suffered a 37.8% decline in equity value, severely lagging the 84.3% gain recorded by the S&P 500 over the same period.

The valuation metrics further explain the company’s vulnerability to outside pressure. Company data shows a recent compression of the firm’s trailing earnings multiple, falling to ~13.6 year-to-date. Readers need to understand that these interventions do not happen randomly or without mathematical justification. Institutional funds specifically target companies where the gap between current market value and potential operational value grows too large for existing management to defend.

When big ASX news breaks, our subscribers know first

How Outside Capital Forces Change (The Activist Playbook)

When a company severely lags the broader market, outside institutions use concentrated capital to force open the doors of a closed boardroom. This financial strategy works by accumulating enough voting power to demand systemic changes, moving beyond the passive approach of simply buying and holding shares. The primary goal is to correct management failures, optimise capital allocation, and extract hidden value from underperforming assets.

A standard corporate campaign follows a highly specific chronological timeline:

- Quiet Accumulation: The institution purchases shares on the open market, carefully building a position just below regulatory reporting thresholds to avoid driving up the share price prematurely.

- Public Disclosure: The fund crosses the legally mandated ownership threshold, requiring a public filing that details their exact stake and signals their intentions to the broader market.

- Strategic Demands: The new major shareholder presents a formal list of required changes to the board, often involving executive turnover, cost reductions, or strategic reviews.

- Settlement and Execution: Existing management agrees to a cooperation pact, granting the outside fund board seats to avoid the massive expense and public scrutiny of a shareholder vote.

Legal frameworks like the SEC beneficial ownership reporting rules dictate that investors must publicly disclose their positions once they cross the five percent threshold, a mechanism that officially alerts the market to an impending activist campaign.

The Leverage of a Ten Percent Stake

Elliott Investment Management followed this operational playbook precisely by accumulating an equity position exceeding 10% of outstanding NCLH shares in February 2026. Hitting a double-digit ownership threshold provides the critical mass needed to credibly threaten a proxy fight.

This mathematical leverage forces existing management to negotiate directly rather than risk losing control in a public shareholder vote. The timeline from the initial February disclosure to the swift 27 March cooperation agreement took just weeks. This rapid resolution highlights the immense pressure a concentrated equity block creates within a publicly traded company.

Boardroom Overhaul: Leadership Changes at Norwegian Cruise Line

The immediate result of the 27 March agreement was unprecedented structural turnover within the central governing body of the cruise operator. Four existing directors departed the company immediately upon the signing of the cooperation pact. In their place, the company installed five new independent directors, officially expanding the committee to nine members.

Elliott proposed four of these five new members, granting the fund massive influence across the newly configured board. This intervention focuses on precise operational surgery rather than mere financial engineering or balance sheet manipulation. Activist funds meticulously select operators who possess the exact skills needed to fix specific business flaws identified during their research phase.

The new leadership group represents a deliberate shift away from legacy cruise insiders, injecting highly specific industry DNA into the company. The newly appointed directors bring specialised turnaround credentials:

A former British Airways executive with extensive experience in aviation turnarounds and large-scale cost efficiency programmes. An operations executive with a deep background in theme park management and guest monetisation from Six Flags. * Additional independent members holding specialised backgrounds in corporate finance, strategic planning, and hospitality restructuring.

By installing these specific directors, the outside fund creates a direct mechanism for ensuring its strategic mandates are executed from the inside. The board no longer functions as a passive oversight body, but rather as an active implementation team.

The Operational Mandate: Extracting Profit from Every Passenger

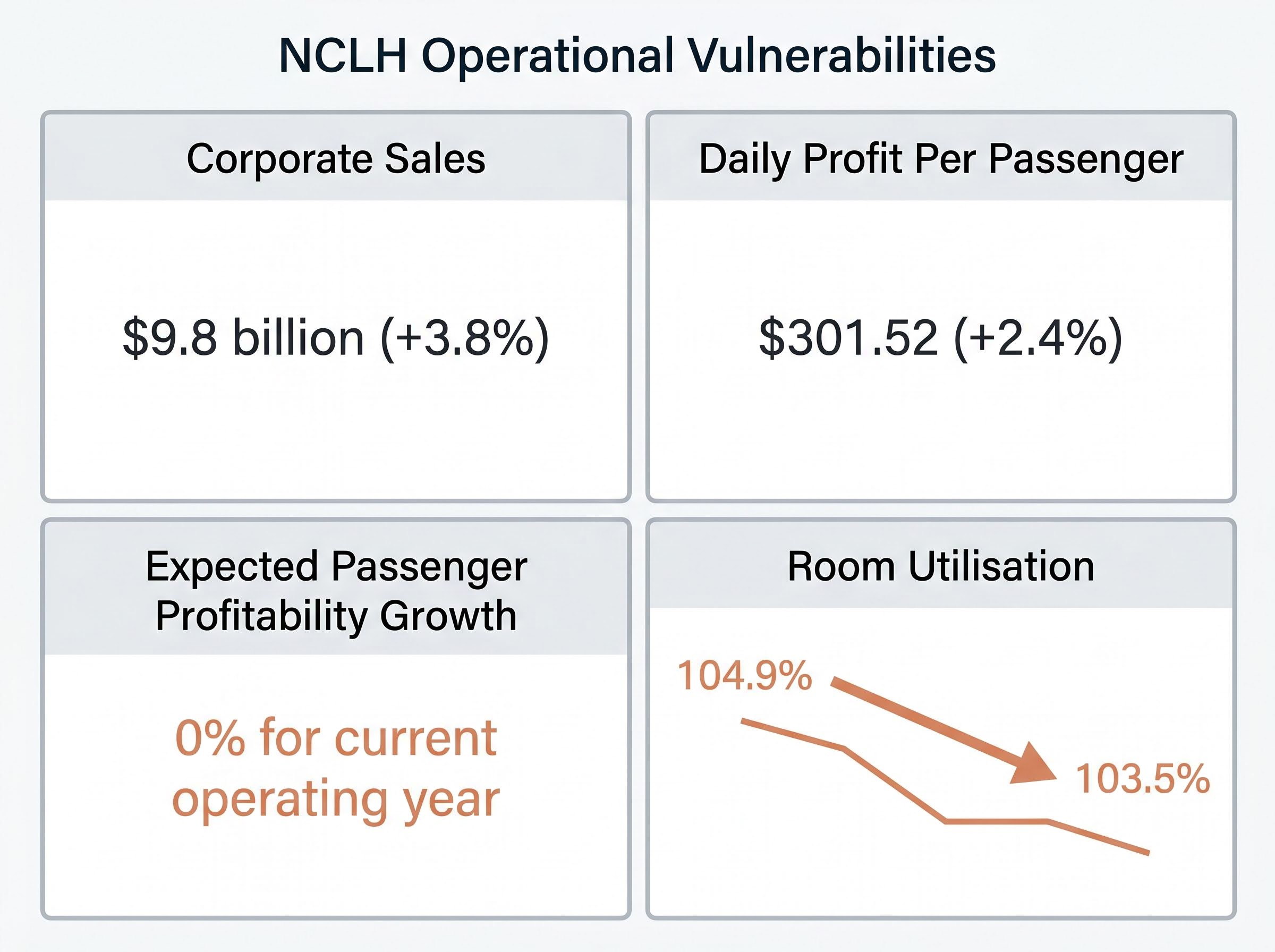

With the boardroom drama settled, the new leadership faces the unglamorous reality of cruise unit economics. The fundamental operational mandate requires extracting more margin from existing assets to close the financial performance gap with industry peers. Recent financial disclosures reveal specific operational vulnerabilities that the newly configured board must address immediately.

According to company data, corporate sales expansion reached 3.8%, hitting $9.8 billion when excluding currency fluctuations. However, according to company data, daily profitability generation per passenger advanced just 2.4% to $301.52, failing to keep pace with broader inflation metrics. More concerning for investors, corporate executives anticipate zero growth in core passenger profitability for the current operating year.

The new board will likely implement aggressive corporate expenditure reductions and an overhaul of promotional campaigns to improve these baseline metrics. By breaking down the unit economics of a cruise cabin, investors gain a practical understanding of how high-level corporate governance directly impacts day-to-day business operations.

Addressing the Utilisation Squeeze

According to company data, a primary operational red flag is the recent drop in standard double-occupancy room utilisation, which fell to 103.5% from a prior 104.9%. In an industry defined by massive fixed costs, falling utilisation directly degrades baseline profitability and indicates weakening pricing power.

The theme park and aviation backgrounds of the new board members connect directly to this specific capacity challenge. Their prior corporate experience centres entirely on maximising yield per available seat and cabin. The outside fund clearly appointed these individuals to deploy their yield-management skill sets across the lagging cruise fleet.

For investors looking to understand how macroeconomic input costs threaten these recovery efforts, our detailed coverage of oil price recession risks examines how surging fuel expenses systematically compress operating margins across the travel sector.

Wall Street’s Verdict and the Forward Outlook

As of late April 2026, the market is pricing in the high stakes of this turnaround attempt. Norwegian currently lags significantly behind its two primary competitors in core valuation metrics, highlighting the exact gap the new board must close. The upcoming 4 May earnings report serves as the first major public test for the newly structured company.

| Cruise Operator | Late April 2026 Stock Price | Forward P/E Ratio |

|---|---|---|

| Norwegian Cruise Line (NCLH) | $18.19 | ~12.5 |

| Royal Caribbean (RCL) | $265.84 | 15.36 |

| Carnival (CCL) | $26.94 | 12.02 |

The analyst community maintains a generally optimistic but cautious stance following the boardroom shakeup. Consensus ratings show a “Strong Buy” with a median price target implying roughly 35% upside from late-April levels. Analysts anticipate Q1 2026 revenue between $2.35 billion and $2.36 billion, alongside earnings per share of $0.14 to $0.16.

This cautious optimism reflects the reality that operational execution must occur against a backdrop of underlying consumer spending constraints, as households increasingly draw down savings to fund discretionary purchases.

However, some financial institutions remain reserved regarding the timeline of the recovery. Both UBS and Susquehanna recently cut their price targets to $22.00 and $20.00 respectively. These adjustments reflect the understanding that while the board has changed, the structural execution risks associated with a fleet-wide operational overhaul remain substantial.

Navigating the Next Chapter of Corporate Accountability

The intervention at Norwegian Cruise Line stands as a clear example of capital markets self-correcting when management fails to deliver adequate returns. Elliott Investment Management successfully weaponised its capital to replace an underperforming governance structure with highly specialised operators.

When these institutional agitators assume control, they typically implement aggressive restructuring programs designed to yield the positive long-term effects of hedge fund activism, focusing on sustained operational efficiency and optimized capital allocation.

While the boardroom battle was won swiftly in March 2026, the actual operational turnaround and margin recovery will take time to manifest in the company’s share price. The new directors face a complex task in reversing declining room utilisation and flat passenger profitability.

This case study serves as a stark warning to other underperforming boards across the broader hospitality sector. When public companies fail to maximise the value of their assets during periods of market expansion, concentrated capital will eventually step in to force the issue.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.