The Maths Behind Stock Picking’s $402,000 Retirement Cost

3 hrs ago

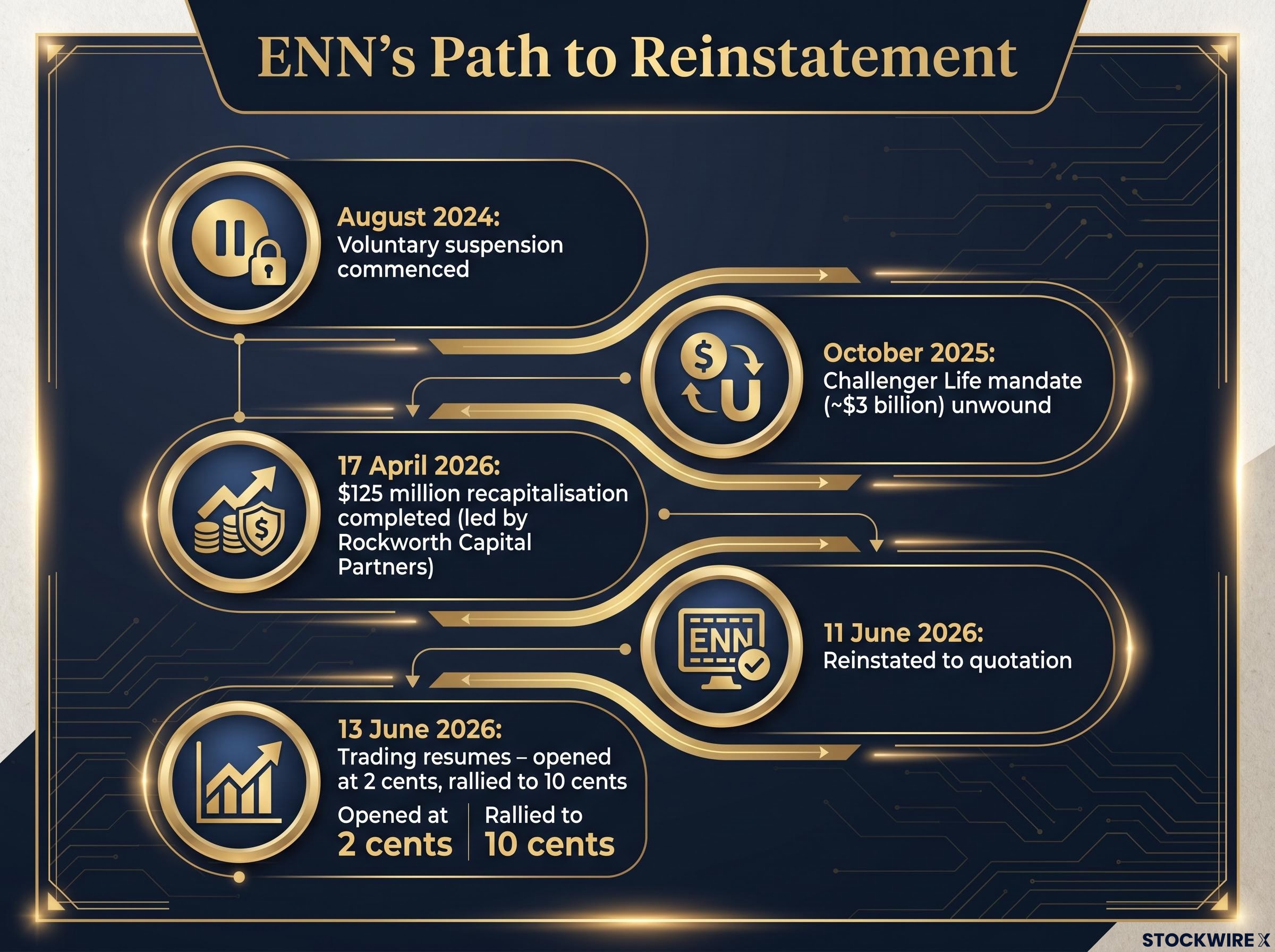

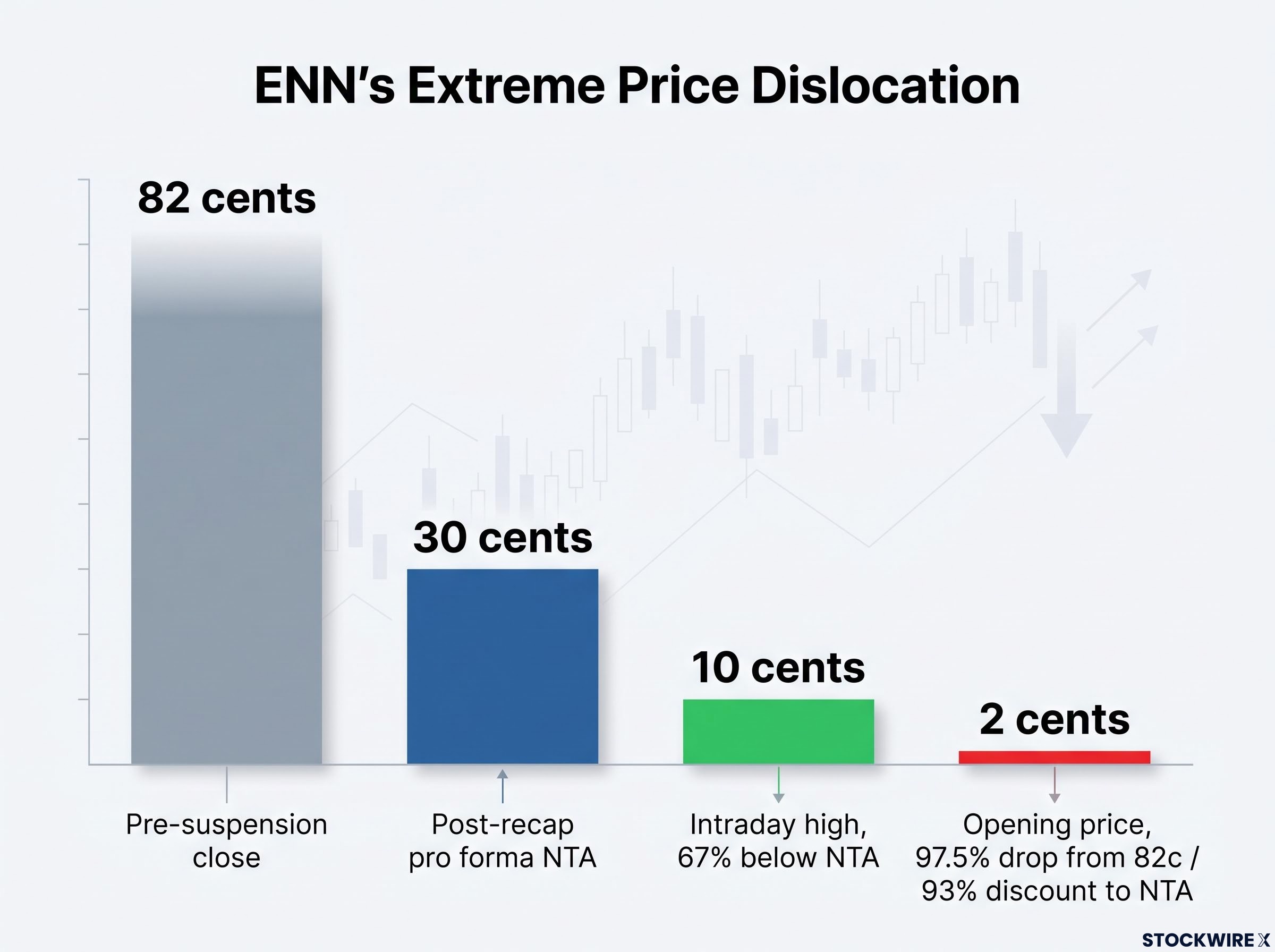

On Friday 13 June 2026, Elanor Investors Group (ASX: ENN) opened at 2 cents per share after nearly two years in suspension. That represented an immediate 97.5% collapse from its last traded price of 82 cents. Within roughly one hour, the stock had surged to approximately 10 cents, a gain of around 400%. Yet even after that violent rebound, ENN was still trading approximately 67% below its stated net tangible asset value of 30 cents per security. This sequence was not a glitch. It was the predictable result of specific structural forces that operate whenever a heavily indebted, recapitalised listed company returns to trading after a prolonged suspension, and these mechanics are poorly understood by most retail investors. This article unpacks exactly what happened with ENN and why, explaining the forces behind the opening crash, the rapid rebound, and the persistent discount to NTA. Readers will come away with a framework for interpreting price action in reinstated or restructured stocks and a set of practical disciplines for managing the real risks involved.

Elanor Investors Group is a real estate funds management and investment platform that accumulated excessive leverage during its expansion, with peak gearing reaching approximately 80%, funded partly by high-cost short-term bridge finance. The group’s financial deterioration accelerated in October 2025 when the Challenger Life mandate, a roughly $3 billion portfolio, was unwound. Combined with ongoing operating losses, this forced the company to request a voluntary suspension from the ASX in August 2024 while it sought to stabilise its balance sheet.

ASX Guidance Note 16 on trading halts and voluntary suspensions sets out the conditions under which a listed entity may request suspension from quotation under Listing Rules 17.1 and 17.2, including the requirement that reinstatement be conditional on the company meeting its continuous disclosure obligations and demonstrating a current prospectus or equivalent disclosure document where required.

The eventual solution was a $125 million recapitalisation led by Rockworth Capital Partners, completed on 17 April 2026. The group was reinstated to quotation on 11 June 2026, with trading resuming the following day.

The price action on reinstatement day told the story of the restructuring in compressed form.

| Metric | Value |

|---|---|

| Suspension commenced | August 2024 |

| Recapitalisation completed | 17 April 2026 |

| Reinstatement to quotation | 11 June 2026 |

| Recapitalisation size / lead partner | $125 million / Rockworth Capital Partners |

| Last pre-suspension close | Approximately 82 cents |

| Opening price on reinstatement | 2 cents (approximately 97.5% below prior close) |

| Post-recap pro forma NTA (diluted) | 30 cents per security |

| Intraday high (within approximately 1 hour) | Approximately 10 cents (approximately 400% from open) |

| Intraday high versus NTA | Approximately 67% below NTA |

A 2-cent opening price against a 30-cent post-recap NTA: an approximately 93% discount to stated asset value at the first trade.

The numbers are stark. An 82-cent stock reopened at 2 cents, rallied 400% to 10 cents within an hour, and was still worth barely a third of its balance-sheet value. Each of those moves has a specific mechanical explanation.

Many retail investors who held ENN through the suspension may still be anchoring to that 82-cent prior close, interpreting the current price as a loss to be recovered. That framing is a structural error, because the legal and financial reality of their holding has been fundamentally transformed.

A debt-for-equity recapitalisation involves new capital providers injecting cash or converting debt into equity in exchange for a large ownership stake, typically under terms that are preferential relative to existing holders. In ENN’s case, Rockworth Capital Partners led the $125 million recapitalisation, and the post-recap pro forma NTA settled at 30 cents per security on a diluted basis (accounting for warrants issued as part of the transaction). That 30 cents was calculated on the new, enlarged and reshaped equity base, not the old one.

The ENN recapitalisation structure involved three distinct capital tiers: $70 million in senior secured Loan Notes, $55 million in Perpetual Notes, and 30 million warrants exercisable at one cent, each carrying different priority and return profiles that directly shaped the dilution experienced by ordinary securityholders.

The four structural changes a recapitalisation introduces are worth cataloguing directly:

After a major recapitalisation, the entity emerging from the process is operating under a different capital structure with a different risk-reward profile. Treating the pre-suspension price as a benchmark for where the stock “should” trade is one of the most common and most costly errors retail investors make in these situations.

ENN’s 2-cent opening print looked disconnected from reality. It was, in a sense, but not because the market was behaving irrationally. The opening price reflected the specific mechanics of who was selling, why they were selling, and how few buyers were willing to stand in front of them.

Price discovery mechanics explain why the opening auction print in a volatile reinstatement often represents the worst price of the entire session: when a concentrated wave of market-sell orders hits a thin book at the same moment, the clearing price reflects the sellers’ urgency rather than any rational assessment of the underlying security’s value.

Three categories of forced or near-forced sellers accumulate during a prolonged suspension:

Distressed and special-situations traders look at the gap between a 2-cent opening price and a 30-cent NTA and see asymmetric optionality. Even if the NTA is optimistic, the downside from 2 cents may be limited compared with the potential upside. These are not investors betting on a full recovery; they are traders pricing the probability that the stock is worth more than the panic print suggested.

As these buyers meet a now-thinner stream of sellers, the price snaps back. That is how ENN moved from 2 cents to approximately 10 cents, a roughly 400% move, in just over an hour. The speed of the rally reflected the severity of the initial dislocation, not a sudden improvement in fundamentals.

Even at 10 cents, ENN remained approximately 67% below its stated NTA. The intraday rally was a partial correction of a structural dislocation, not evidence that value had been restored.

Net tangible asset value (NTA) is a balance-sheet measure: total assets minus liabilities, divided by the number of securities on issue. For property-heavy businesses like ENN, the asset valuations feeding into NTA are based on periodic independent appraisals rather than guaranteed sale prices.

A large and persistent discount to NTA in a post-restructuring situation is not automatically a mispricing. The market is often discounting several distinct layers of risk:

Value traps are the most relevant risk category for post-reinstatement situations: a stock can screen as cheap on NTA, carry an apparently large margin of safety, and still destroy capital if the underlying business is structurally impaired rather than temporarily mispriced.

NTA is a starting point for analysis, not a floor for the share price. Only after interrogating the quality of the underlying assets, the terms of the new capital structure, and the credibility of the turnaround plan should an investor consider whether the discount compensates adequately for the risks.

Applied to ENN specifically: a business with peak gearing of approximately 80%, an approximately $3 billion mandate loss, and an extended period of operating losses was trading at 10 cents against a 30-cent NTA. That 67% discount reflected real, identifiable uncertainties about whether the post-recap business could rebuild its funds management platform and sustain asset values, not an oversight by the market.

The 2-cent opening print on ENN’s reinstatement was not just an abstract data point. For any holder who had lodged a market sell order before the opening auction, it was the price they received for their shares, at the exact moment of maximum dislocation.

A market order instructs the broker to sell at whatever price is available. In a normal trading session with reasonable liquidity, the execution price will be close to the displayed bid. In a volatile reinstatement with a thin order book and concentrated forced selling, a market order exposes the holder to an extreme low print.

A limit order sets a minimum acceptable price. A holder who set a limit of, say, 8 cents would not have been filled at the 2-cent open, but could have been filled as the price recovered toward 10 cents within the hour. The trade-off is real: a limit order may not execute immediately, or at all, if the market never reaches the specified price. But that outcome is preferable to being sold at 2 cents when the stock subsequently trades at 10 cents within sixty minutes.

Three steps for managing order type risk on a reinstatement day:

In illiquid, volatile reinstatements, order type selection is one of the highest-impact decisions a retail holder can make. It is often overlooked in the focus on price direction.

The spectacle of a 400% intraday rally from a 2-cent base makes for attention-grabbing headlines, but it is a distraction from the slower, harder question that will determine whether ENN holders recover meaningful value: can the business actually rebuild?

ENN’s suspension lasted approximately 22 months. The recapitalisation stabilised the balance sheet, but the group was still working to rebuild its funds management platform after the Challenger Life mandate loss and an extended period of operating losses. Even after the intraday rally, ENN sat at approximately 10 cents versus a 30-cent NTA, a persistent 67% discount. Closing that gap, if it closes at all, will be measured in quarters and years, not hours.

Prolonged suspensions signal structural problems, not temporary hiccups. The old share price is not a recovery benchmark. And big percentage moves from a very low base reflect the severity of the dislocation, not the size of the fundamental opportunity.

Before treating any post-recap, post-suspension stock as a value opportunity, an investor should be able to answer four questions:

These are not factors to note in passing. They are questions that must be answered with conviction before capital is committed.

The ENN episode will recur in different forms. Heavily indebted listed companies, prolonged suspensions, debt-for-equity recapitalisations, and violent reinstatement price action are recurring features of Australian equity markets. The specific numbers will change; the mechanics will not.

The lessons are portable. Extreme opening moves in reinstated stocks are structurally driven by forced selling, not random panic. NTA is a starting point for analysis, not a price floor. Pre-suspension share prices become irrelevant after a major recapitalisation. And order type decisions matter more in these situations than most investors realise.

Classifying price dislocations before acting on them is the analytical step most retail investors skip: the same percentage drop in two different stocks can represent an irrational overreaction in one case and early evidence of structural impairment in the other, and conflating the two is how speculative recoveries become permanent capital losses.

Before trading any reinstated or restructured stock, understand the new capital structure, interrogate the NTA, and choose your order type deliberately. The discipline to resist the pull of headline price moves is what actually protects capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and post-restructuring outcomes are subject to material uncertainty.

When a suspended stock is reinstated, forced sellers including managed funds, margin loan accounts, and retail holders who have waited for the halt to lift often flood the opening auction with market sell orders, driving the opening price far below any rational assessment of the company's underlying value. The price frequently recovers sharply once that concentrated selling wave clears.

A debt-for-equity recapitalisation involves new capital providers injecting cash or converting debt into equity in exchange for a large ownership stake, which massively dilutes existing securityholders and makes the pre-suspension share price irrelevant as a recovery benchmark. The post-recap net tangible asset value per security becomes the correct analytical starting point, not the old traded price.

ENN's 2-cent opening print reflected a concentrated wave of price-insensitive sellers, including mandated fund exits and margin-loan liquidations, meeting a thin pool of cautious buyers in the reinstatement auction, not an accurate assessment of the company's balance sheet. The opening price reflected seller urgency rather than the underlying asset value, which is why the stock recovered to approximately 10 cents within an hour.

Investors should avoid market orders before the opening auction clears on a reinstatement day, because in a volatile reinstatement with concentrated forced selling the execution price can be at the extreme low of the session. Setting a limit order at a minimum acceptable price, informed by the post-recap NTA and the expected range of forced selling, protects against being filled at the worst possible print.

A large discount to net tangible asset value after a restructuring is not automatically a mispricing; the market is typically discounting valuation risk on assets, preferential rights held by new capital providers, unproven earnings power, and lingering seller overhang. The NTA is a starting point for analysis rather than a price floor, and the discount only represents a genuine opportunity if the underlying assets are sound and the turnaround plan is credible.