Two Index Changes on 29 June, Two Very Different Flow Stories

9 hrs ago

Bank of America published a semiconductor outlook today that makes one of the more striking claims in recent Wall Street research: according to the bank’s analysts, what took the chip industry roughly half a century to achieve in cumulative revenue, AI will replicate in just five years, adding the next $1 trillion to semiconductor sales.

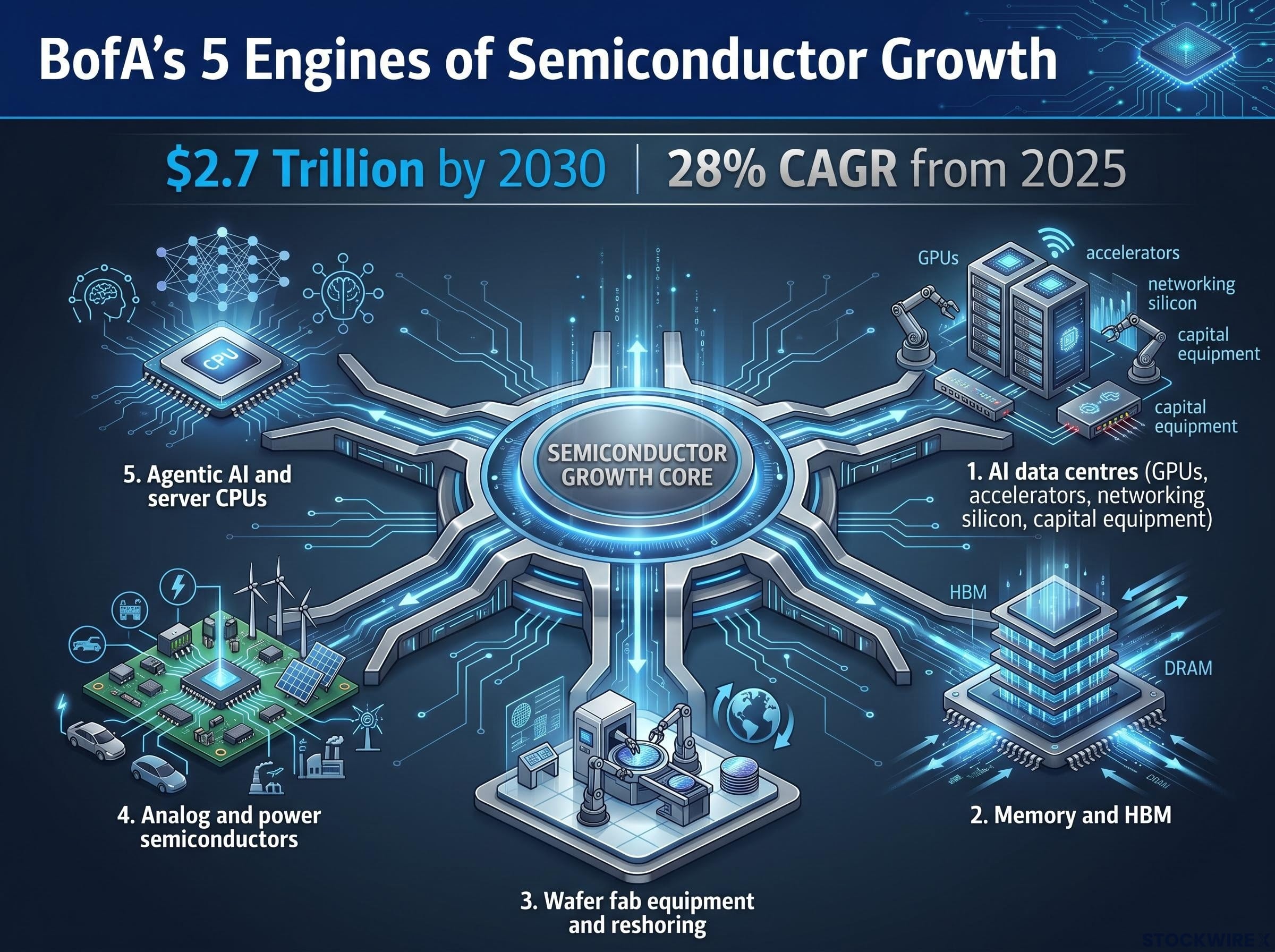

The note, authored by analyst Vivek Arya and published 23 June 2026, lifts BofA’s semiconductor industry revenue forecast to $2.7 trillion by 2030, a figure that works out to a 28% compound annual growth rate (CAGR) from the 2025 baseline. That is not a modest revision. It repositions semiconductors from a cyclical hardware category into something closer to a multi-decade structural build, powered by five distinct AI-driven demand engines operating simultaneously.

What follows breaks down each of those five engines, surfaces the most actionable data points, examines where BofA’s thesis is strongest and where it carries the most execution risk, and identifies which stock-specific price target revisions reflect the most conviction. If you are constructing or adjusting semiconductor exposure, the interaction between these five segments matters more than any single name.

The revision itself is substantial. BofA’s previous forecast had the semiconductor industry reaching $2.3 trillion by 2030. The updated figure of $2.7 trillion carries a 28% CAGR from 2025, a pace that stands out for an industry that needed around five decades to cross its first $1 trillion revenue threshold.

What separates this call from a straightforward GPU bet is its architecture. BofA’s thesis is deliberately multi-segment, and the diversification is both its greatest strength and its most important dependency. Unlike prior chip cycles driven by a single product category (PCs, smartphones, crypto mining rigs), this one requires simultaneous broad-based AI adoption across enterprise and infrastructure to fully materialise. Accepting the full $2.7 trillion number means believing that five distinct demand engines fire at once.

The scale of hyperscaler AI capex commitments, with Amazon, Microsoft, Alphabet, and Meta collectively spending $130 billion in Q1 2026 alone against full-year 2026 guidance reaching $725 billion, sets the demand floor that BofA’s five-engine thesis is built on top of.

Those five engines are:

For 2026, BofA’s forecast points to memory chip revenue growth of close to 300% on a year-over-year basis.

Nearly 300% year-over-year memory chip revenue growth projected for 2026, driven by high-bandwidth memory demand from AI accelerators.

That figure is exceptional even in a segment known for violent swings. Memory has historically been the semiconductor industry’s most volatile subsector, with rapid capacity additions and spot pricing producing margin collapses that wiped out years of gains in a single downturn. BofA’s thesis is that this cycle is structurally different.

The mechanics behind that claim centre on HBM (high-bandwidth memory), a specialised memory type designed to sit directly alongside AI accelerator chips and feed them data at the speeds their workloads demand. Manufacturing HBM is significantly more complex than producing standard DRAM, and multi-year ramp timelines mean new capacity cannot be brought online quickly. BofA anticipates supply constraints persisting through 2028.

Micron is BofA’s clearest single-stock expression of the HBM thesis, with the most aggressive price target revision in the entire note: from $950 to $1,500.

Two structural factors underpin the durability argument. First, long-duration supply contracts between HBM producers and hyperscaler customers provide multi-year demand visibility and reduce the spot-pricing exposure that historically triggered margin collapses. Second, HBM manufacturing complexity means the supply response to high prices is measured in years, not quarters.

The risk is straightforward: how quickly can Samsung and SK Hynix bring additional HBM capacity online? If competing supply arrives faster than BofA anticipates, the pricing power that supports the 300% growth projection compresses. That supply response timeline is the single most important variable for investors sizing memory exposure.

For investors wanting to model the specific supply mechanics behind BofA’s 2028 constraint timeline, our full explainer on HBM supply constraints walks through SK Hynix’s inventory data, the 6-8% DRAM wafer start growth rate against 70% projected HBM demand growth, and the 2027-2028 window where competing capacity arrivals could compress the pricing environment BofA’s Micron call depends on.

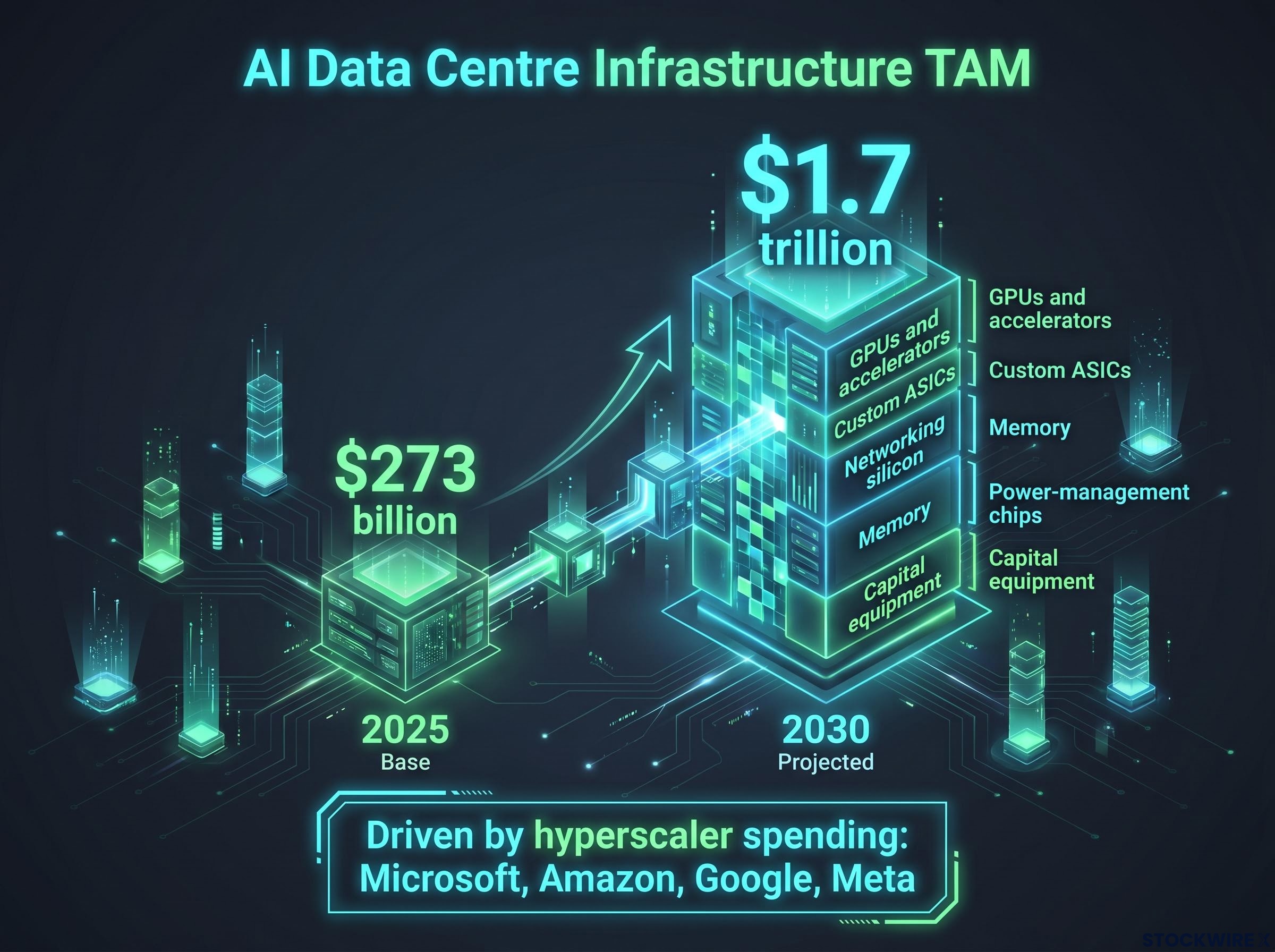

According to BofA’s projections, the AI data centre systems market will scale from a $273 billion base in 2025 to around $1.7 trillion by 2030. The gap between those two numbers is where the investment case lives.

A TAM is the total revenue opportunity available to all companies in a given market if every potential customer purchased. What matters here is what composes it. The AI data centre TAM is not a single product line. It encompasses:

Current hyperscaler AI spending from Microsoft, Amazon, Google, and Meta is already historically large, but BofA characterises it as early relative to long-term anticipated demand. The 2025 baseline is framed as a floor, not a midpoint.

Marvell saw its price target lifted from $240 to $365, with BofA pointing to AI networking and connectivity demand as the primary driver within this broader infrastructure build.

The implication of a TAM expanding from $273 billion to $1.7 trillion is that current infrastructure spending, while already at record levels, represents a fraction of where the addressable market could settle. That gives investors a reference point for evaluating whether sector valuations are running ahead of or behind the underlying demand curve, a more useful framing than current price multiples alone.

BofA has meaningfully revised upward its wafer fab equipment (WFE) spending outlook, which tracks total global expenditure on the machinery used to produce semiconductor chips. The bank now expects WFE spending to reach $250 billion by 2028, compared with a previous estimate of $203 billion, and sees scope for that figure to climb as high as $292 billion by 2030.

The profitability asymmetry between hyperscalers and their semiconductor suppliers is most visible in wafer fab equipment spending: SEMI forecasts three consecutive record years rising from approximately $133 billion in 2025 to $156 billion in 2027, with depreciation as a share of hyperscaler revenue climbing from 7% in 2022 to roughly 12% by 2027, compressing buyer margins while equipment makers capture structurally improved pricing power.

Two forces drive the upgrade simultaneously. First, each new generation of leading-edge chip manufacturing requires more process steps per wafer, which means more equipment per unit of output. Second, government-backed reshoring programmes, most notably the CHIPS Act in the United States, are funding domestic fab construction that would not be economically viable without subsidy support.

The named beneficiaries sit at the intersection of both forces:

| Company | Previous Target | Revised Target | Primary Driver |

|---|---|---|---|

| Applied Materials | $540 | $720 | Higher WFE spending projections |

| Lam Research | $330 | $480 | Higher WFE spending projections |

| KLA Corporation | $210 | $317 | Higher WFE spending projections |

Equipment makers are the one segment in BofA’s thesis that carries structural support from both AI demand and government policy simultaneously. That dual backstop means the investment case does not collapse entirely if AI capex growth moderates, a different risk-return profile from pure-play GPU or memory names.

The policy leg of this thesis carries specific risks worth tracking. CHIPS Act funding requires political continuity; shifts in budget priorities or changes in administration could reduce the subsidy runway. If geopolitical tensions around Asia-centric supply chains ease, the urgency behind domestic fab construction diminishes. And several domestic fab projects face questions about whether they remain economically viable without ongoing government support.

CHIPS Act programs status reporting from the federal oversight body tracks funding disbursements, fab construction milestones, and subsidy conditionality, providing investors with the most direct window into whether the policy leg of the equipment thesis is advancing or stalling.

None of these risks are predictions of failure. They are watchpoints. The equipment thesis is strongest when both the technology-complexity driver and the policy driver operate in tandem; investors should monitor what happens if one weakens.

Two segments in BofA’s framework receive less investor attention than GPUs or memory, but they represent the thesis’s most durable, longer-duration layers.

Rising AI data centre power density creates structural demand for analog and power-management semiconductors, the chips that convert, distribute, and regulate electrical power within server racks. BofA does not provide an explicit revenue forecast for analog, but frames the segment as offering steadier, less hype-driven earnings than GPU-exposed names. As AI racks pull increasing power loads, analog suppliers capture a growing share of infrastructure economics without the narrative volatility that accompanies accelerator stocks.

The second quieter layer is agentic AI. BofA puts the server CPU opportunity tied to autonomous, task-oriented AI deployments at roughly $170 billion, covering both x86 (Intel, AMD) and ARM-based server platforms. CPUs remain central for orchestration, logic, and memory management alongside GPUs and accelerators, reframing them as AI beneficiaries rather than casualties of the accelerator-first architecture shift.

Intel’s price target was revised from $135 to $160, partly on this basis.

The execution risk in the agentic AI thesis is real. The $170 billion TAM requires autonomous AI systems to move from enterprise pilots to widespread deployment, a transition subject to:

These two segments offer AI exposure less sensitive to narrative momentum around model training and hyperscaler capex announcements. For investors who want sector participation without full concentration in the highest-volatility names, they are worth examining, but the agentic AI TAM does not materialise unless enterprise deployment moves beyond controlled pilots.

Investors who want to stress-test BofA’s $170 billion agentic CPU TAM against independent modelling will find our deep-dive into the server CPU market forecast useful: Citi’s 18 May 2026 model projects $131.5 billion by 2030 driven by a newly defined agentic CPU segment growing at a 185% CAGR, with specific Intel and AMD market share projections, price targets, and an honest assessment of the assumptions underpinning the growth rate.

The full set of BofA’s price target revisions, published 23 June 2026 by analyst Vivek Arya, tells a story about where the firm’s highest conviction sits:

| Company | Previous Target | Revised Target | Key Driver | Rating |

|---|---|---|---|---|

| Micron | $950 | $1,500 | HBM demand; structurally limited supply capacity to 2028 | Buy |

| Applied Materials | $540 | $720 | Higher WFE spending projections | Buy |

| Lam Research | $330 | $480 | Higher WFE spending projections | Buy |

| Marvell | $240 | $365 | AI networking and connectivity growth | Buy |

| KLA Corporation | $210 | $317 | Higher WFE spending projections | Buy |

| Intel | $135 | $160 | Growing server CPU addressable market; foundry business outlook | Buy |

| Axcelis Technologies | $130 | $156 | Pending merger with Veeco | Underperform |

Micron’s revision is the largest in percentage terms and reflects BofA’s highest-conviction near-term call, tied directly to the HBM supply constraint thesis.

The pattern across the table tells you where BofA’s strongest conviction sits: memory and equipment rather than software-adjacent or connectivity names.

Axcelis Technologies is the outlier. BofA lifted the price target from $130 to $156 while holding its Underperform rating in place, on the basis that the shares appear fully valued even once potential earnings benefits from the company’s pending merger with Veeco are taken into account. A higher price target does not automatically mean a buy recommendation.

Investors do not have to accept the full $2.7 trillion forecast to find actionable ideas here. The more useful exercise is deciding which of the five engines has the most near-term structural support and sizing exposure accordingly.

Memory and equipment carry the strongest near-term foundations. HBM supply constraints are observable today, long-duration contracts provide earnings visibility, and equipment demand benefits from both AI manufacturing intensity and policy-backed reshoring. Agentic AI and analog represent longer-duration, higher-conditionality exposure where the TAM depends on enterprise deployment velocity and sustained power-density growth.

Even a partial materialisation of the five-engine thesis would represent a significant industry expansion relative to current consensus. The productive question is not whether the entire thesis is correct, but which segments are most likely to underdeliver, and where you are overweight if they do.

The key watchpoints to track over the coming quarters:

The 28% CAGR at the centre of BofA’s thesis is the metric most likely to be scrutinised first if any of these watchpoints flash warning signs. BofA’s framework gives you a structured way to disaggregate semiconductor exposure rather than treating the sector as a monolithic AI trade, and that disaggregation is where the real portfolio construction value sits.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections are subject to market conditions and various risk factors.

Bank of America forecasts the global semiconductor industry will reach $2.7 trillion in revenue by 2030, representing a 28% compound annual growth rate from the 2025 baseline, driven by five AI-related demand segments including data centres, HBM memory, wafer fab equipment, analog power chips, and agentic AI server CPUs.

HBM, or high-bandwidth memory, is a specialised memory type designed to sit directly alongside AI accelerator chips and feed them data at the speeds AI workloads require; its manufacturing complexity means supply cannot be ramped quickly, and BofA expects supply constraints to persist through 2028, supporting the pricing power behind its nearly 300% year-over-year memory revenue growth projection for 2026.

BofA analyst Vivek Arya raised price targets on Micron (from $950 to $1,500), Applied Materials (from $540 to $720), Lam Research (from $330 to $480), Marvell (from $240 to $365), KLA Corporation (from $210 to $317), and Intel (from $135 to $160), with all six carrying Buy ratings.

CHIPS Act subsidies are funding domestic fab construction in the United States that would not be economically viable without government support, giving equipment makers like Applied Materials and Lam Research a dual demand backstop from both AI manufacturing intensity and policy-backed reshoring, though the thesis is vulnerable to shifts in political will or budget priorities.

Wafer fab equipment spending tracks total global expenditure on the machinery used to manufacture semiconductor chips; BofA revised its WFE forecast up to $250 billion by 2028, from a prior estimate of $203 billion, with scope to reach $292 billion by 2030 as each new generation of leading-edge chip manufacturing requires more process steps and equipment per unit of output.