Global equity markets are currently exhibiting a profound detachment from the severe geopolitical realities unfolding across the Middle East in late April 2026. This market correction risk actively threatens retail and institutional portfolios as active military conflicts dictate unprecedented supply chain disruptions. Despite active hostilities, survey participants maintained optimistic market outlooks in mid-April 2026, according to American Association of Individual Investors data.

This elevated reading sits in stark contrast to the optimism rate recorded just prior to the sudden outbreak of overseas hostilities. Investors require a clear analytical breakdown to understand why both institutional and retail traders are mispricing these severe physical hazards. Automated systems and human sentiment alike are ignoring the structural damage to global energy flows. This widening divergence between bullish positioning and military escalation creates a highly fragile environment for capital allocation heading into the second half of the year.

Analysing the Disconnect Between Valuation Targets and Volatility

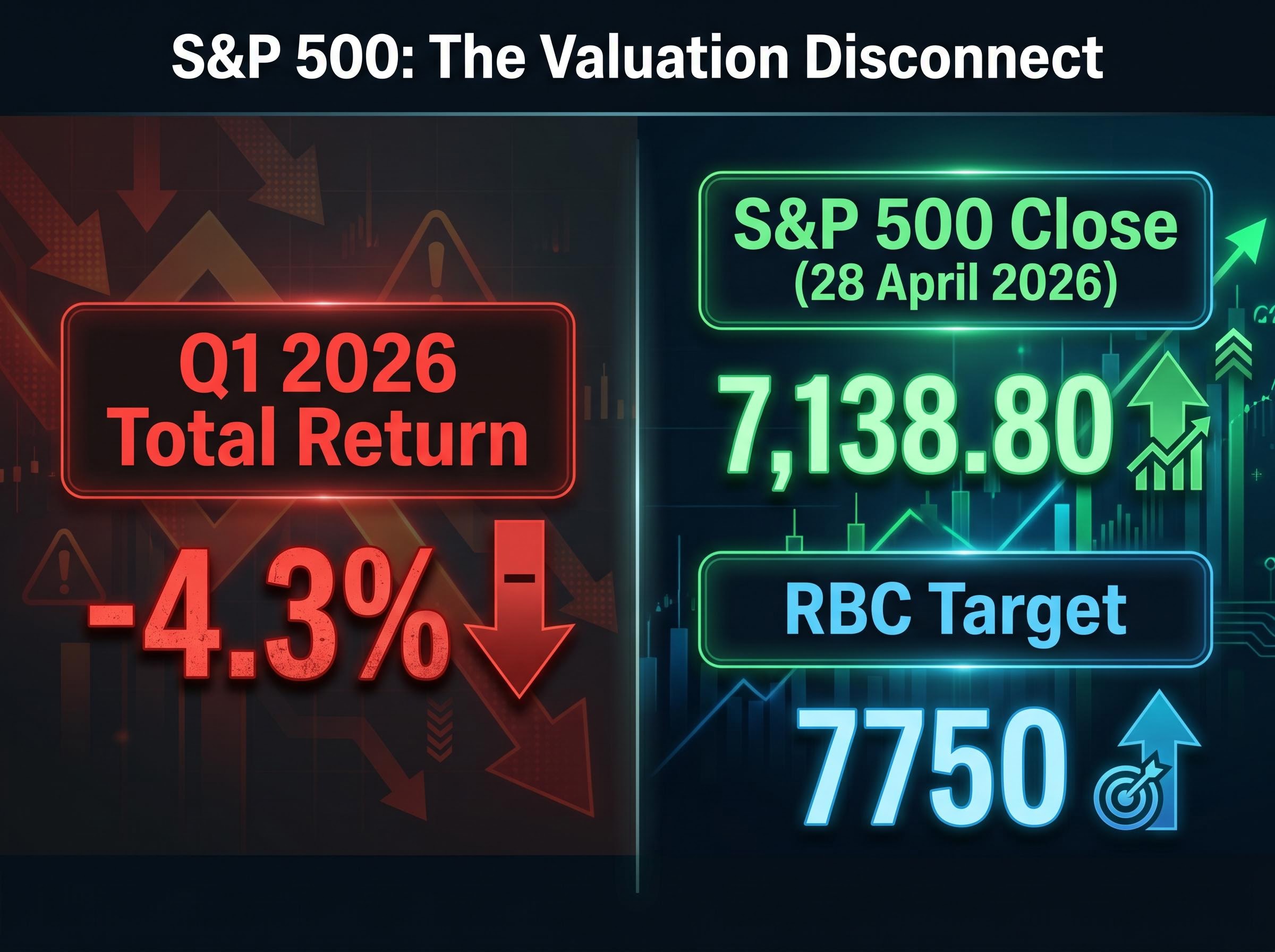

The resilience of US equities continues to defy the negative momentum established earlier in the year. Major indices have sustained an upward trajectory, achieving unprecedented peaks despite a highly negative first quarter. The S&P 500 closed at 7,138.80 as of 28 April 2026, effectively shaking off the fundamental pressures of a broader supply shock.

Looking beyond absolute index levels to historical warning signals reveals a precarious setup where similar past peaks amid commodity shocks led to steep double-digit equity drawdowns.

This optimism directly contradicts the actual performance recorded just weeks prior. The Q1 2026 total return for the S&P 500 was negative 4.3%, while small-cap performance showed the Russell 2000 returning between 0.6% and 3.1%. The broad-based selloffs witnessed in March 2026 ignored normal sector rotations, signalling structural stress that institutional banks are now selectively overlooking.

Prominent analysts continue to issue optimistic targets despite ongoing volatility and a noticeable drop in bond trading. RBC holds an S&P 500 target at 7750, implying quantitative funds are pricing in valuation room for transient dips rather than systemic corrections. Morgan Stanley strategist Mike Wilson explicitly advises a buy-the-dip approach based on projected earnings growth, a sentiment echoed by historical resilience models at J.P. Morgan.

Conversely, analysts like David Goldman warn of persistent volatility and urge geopolitical prudence as financial professionals bypass physical market constraints.

Market Technician Insight “The disconnect we are measuring today suggests financial professionals are bypassing structural supply concerns in favour of historical momentum metrics,” said Craig Johnson, chief market technician.

| Metric | Pre-Conflict Status | April 2026 Status | Market Impact |

|---|---|---|---|

| S&P 500 Positioning | Cautious allocation | Targeting 7750 | Elevated valuation risk |

| Retail Sentiment | Bullish | Bullish | Contrarian indicator triggered |

| Volatility Pricing | Standard hedging | Buying the dip | Underpriced tail risk |

When big ASX news breaks, our subscribers know first

The Algorithmic Blindspot: Why Trading Models Fail to Price Geopolitics

Quantitative funds dictate modern market momentum, yet these systems possess a fundamental vulnerability regarding qualitative military developments. Volatile geopolitical events remain notoriously difficult to accurately price into automated trading algorithms. These systems evaluate risk by analysing historical correlations, volatility patterns, and statistical precedents.

When military posturing disrupts physical supply chains, algorithms lack the necessary historical data to model the outcome accurately. They are structurally designed to process quantifiable inputs like earnings reports or interest rate decisions, not fast-moving negotiations or sudden naval blockades. Consequently, quantitative funds are currently pricing in valuation room for standard market dips rather than structural corrections.

The BIS Quarterly Review on financial markets highlights how sudden geopolitical shocks frequently trigger price discovery failures across commodity sectors, further complicating the ability of automated models to assess qualitative risks.

This automated behaviour means the current market elevation is partially artificial. It is driven by systems that require historical precedent to function, rather than forward-looking geopolitical analysis.

Assessing the Quantitative Vulnerabilities

Algorithms structurally fail to capture military escalation threats for three specific reasons:

They require extensive historical datasets to weight probability, which unprecedented conflicts cannot provide. They rely on numerical inputs and struggle to interpret qualitative rhetoric from military or political leaders. * They are programmed to buy historical support levels, treating fundamental supply shocks as routine technical dips.

This mechanical adherence to past patterns creates a dangerous lag in market pricing. Retail investors must recognise when equity valuations are being driven by blind algorithmic momentum rather than fundamental safety.

Maritime Logistics and the Physical Constraints on Global Energy

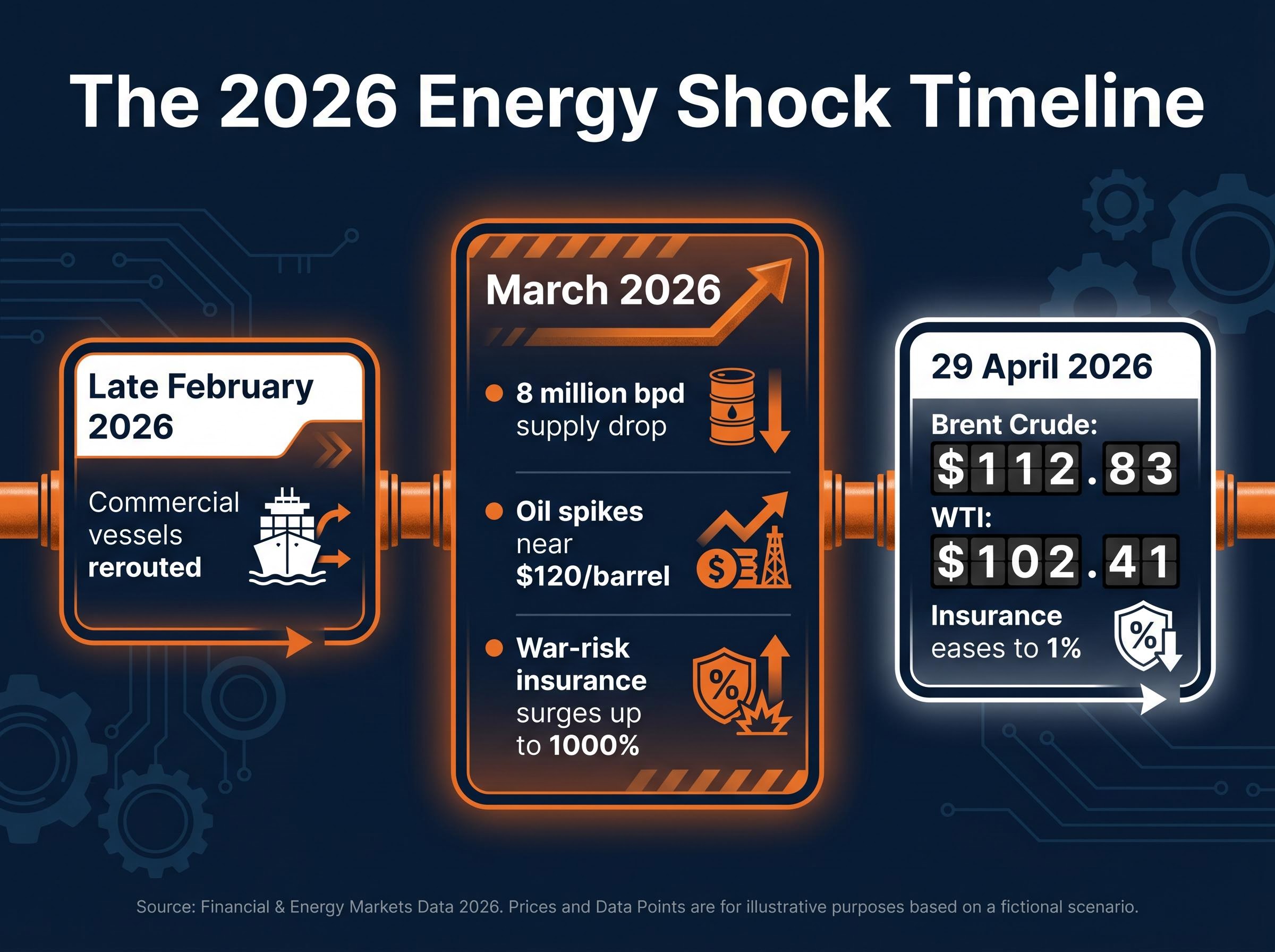

The analytical focus must shift from Wall Street algorithms to the physical reality of the Strait of Hormuz. Tangible threats to global supply chains present a hard ceiling that automated pricing models cannot ignore indefinitely. Energy costs have experienced severe escalation since the initial conflict began in late February 2026.

Global oil prices spiked near $120 per barrel intramonth in March 2026, driven by an 8 million barrels per day supply drop. Prices remained highly elevated as of 29 April 2026, with Brent crude standing at $112.83 per barrel and WTI trading around $102.41 per barrel. Active military posturing has created a fundamentally uninsurable environment for global maritime logistics.

The official EIA analysis of Hormuz closures confirms that such severe production outages mandate the incorporation of a substantial risk premium into baseline crude forecasts.

War-risk maritime insurance premiums surged up to 1000% before easing to 1% from previous highs of 2.5%. This extreme premium volatility reflects the underlying physical danger to tanker infrastructure.

The chronological escalation of maritime threats reveals the trajectory of this physical constraint:

- In late February 2026, initial skirmishes prompted immediate rerouting of commercial vessels away from primary transit corridors.

- By March 2026, physical infrastructure damage resulted in a sudden 8 million barrels per day supply reduction.

- The United States explicitly threatened to strike Iranian vessels and block operational ports to enforce compliance.

- President Donald Trump issued a definitive statement regarding a potential total blockade of the Strait of Hormuz.

Abstract international conflicts directly translate into measurable commodity price shocks. Portfolio managers monitoring these physical leading indicators can accurately track the true cost of global instability.

The Illusion of Consumer Resilience and Federal Reserve Paralysis

A severe contradiction exists between elevated consumer transaction volumes and the rapid deterioration of household purchasing power. Soaring energy costs are quietly fracturing the domestic economic foundation beneath current retail expenditure metrics. The national average for regular gasoline increased by $1.00 in a single month, acting as a highly regressive tax on daily consumption.

This burden forced the personal savings rate down to 4.0% as of February 2026. Consumers are actively draining their accumulated capital to maintain baseline spending levels. A distinct demographic divergence in spending patterns has emerged, where wealthier households are statistically masking the acute financial distress of lower-income demographics.

Federal Reserve Policy Paralysis

Central bank officials find themselves backed into a corner by this energy-driven inflation. The CPI rose to 3.3% year-on-year in March 2026, directly restricting monetary intervention. The FOMC held rates at 3.50% to 3.75% in March, unable to implement cuts while supply shocks inflate core metrics.

The forward trajectory appears equally constrained by these inflationary pressures. The central bank’s dot plot showed 7 of 19 officials expecting absolutely no rate changes through the end of 2026. Goldman Sachs issued distinct warnings of a potential mild recession in the second half of 2026, cutting their GDP growth forecast to 1.5%.

Economic Analysis “Current consumption levels are being temporarily sustained by savings depletion, a mechanism that mathematically cannot persist in a sustained high-energy-cost environment,” according to UBS chief global economist Paul Donovan.

These metrics prove that the foundation supporting current corporate earnings estimates is actively eroding.

Readers interested in the precise mechanisms threatening these economic forecasts will find our deep-dive into US recession risk transmission, which outlines how sustained $110-plus oil translates into corporate margin compression and elevated domestic unemployment probabilities.

Quantifying the Catalysts for an Imminent Repricing

The intersection of macroeconomic paralysis and geopolitical instability provides distinct, measurable triggers that will eventually force an equity repricing. Historical reactions to sustained energy shocks present a clear statistical probability of a severe downturn. Analysts estimate a 20% to 30% chance of a 10% or greater S&P 500 correction occurring in Q2 2026.

Institutional models are actively mispricing geopolitical risk by assuming the Strait of Hormuz will reopen rapidly, a highly optimistic scenario that ignores the escalating physical destruction of regional maritime infrastructure.

These cascading pressures will ultimately override the historical optimism programmed into algorithmic trading models. Abstract macroeconomic fear becomes actionable risk management when traders monitor specific physical and economic thresholds.

The following specific geopolitical and economic catalysts would force automated systems to sharply reprice the market:

Global crude oil remaining sustained above the $110 per barrel threshold, acting as the definitive trigger for a mild domestic recession. Broadened military engagements that result in permanent, physical destruction of Middle Eastern loading terminals. * Additional logistical blockades that trap neutral commercial vessels, forcing marine insurance syndicates to withdraw coverage entirely.

When these concrete events materialise, the transition from market apathy to panic will be rapid. Automated systems will pivot from buying historical dips to executing aggressive algorithmic liquidations.

The Inevitable Collision Between Algorithmic Optimism and Global Conflict

Current equity valuations are constructed upon a fragile foundation of geopolitical willful ignorance. Relying on quantitative targets and historical resilience models is highly dangerous during periods of unprecedented military and energy supply disruptions. The mechanisms that drove market peaks in early 2026 are fundamentally disconnected from the physical realities dictating global commerce.

This profound detachment requires immediate defensive portfolio posturing throughout Q2 2026 and Q3 2026. Investors must prioritise capital preservation strategies and physical commodity hedges before the algorithmic pricing gap violently closes.

Sophisticated market participants are already deploying institutional hedging strategies to reduce duration exposure and increase cash positions ahead of what they view as an inevitable valuation correction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.