Why Governance and Communication Drive Post-IPO Value

7 hrs ago

Most investors frame the choice between NDQ and VAS as a technology bet versus a domestic index bet. That framing misses the point. These two ETFs are not competing answers to the same question; they are instruments designed for different jobs, and the right decision depends on what you are actually trying to build. One is a concentrated global growth vehicle anchored in the companies reshaping digital infrastructure. The other is a broad domestic income engine reflecting the structure of the Australian economy. Choosing between them, or choosing to hold both, is a portfolio construction decision that starts with self-knowledge, not a performance table. What follows is a structural breakdown of how each fund works, what investor profile each serves, and why the most coherent answer for many Australians is a deliberate allocation to both.

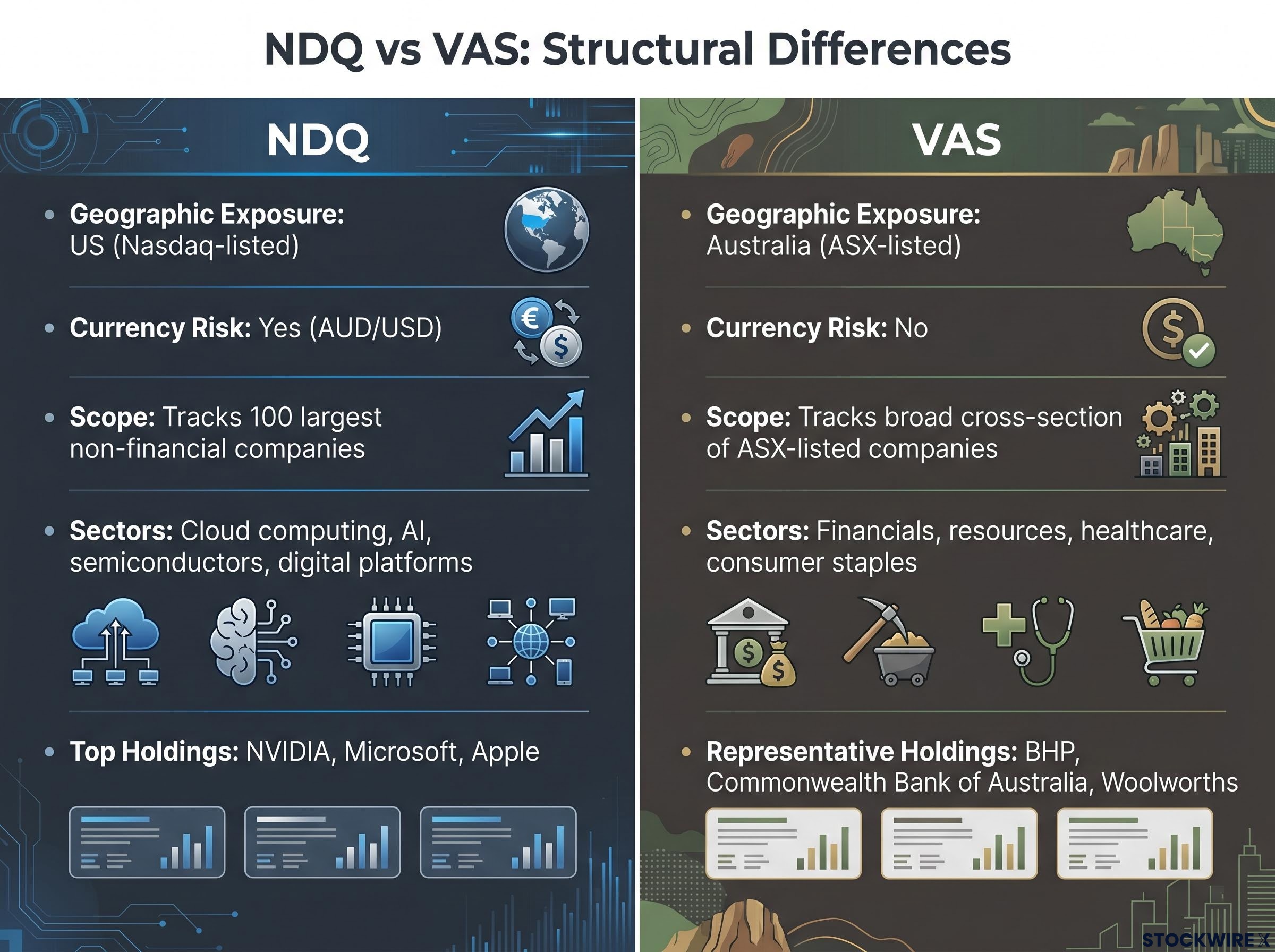

The Betashares Nasdaq 100 ETF (NDQ) tracks 100 of the largest non-financial companies listed on the Nasdaq exchange. Its holdings are concentrated in cloud computing, artificial intelligence, semiconductors, and digital platforms. NVIDIA, Microsoft, and Apple sit at the top of the fund, and the performance of a relatively narrow group of mega-cap technology names drives the bulk of returns.

The Vanguard Australian Shares Index ETF (VAS) tracks a broad cross-section of ASX-listed companies. Its representative holdings include BHP, Commonwealth Bank of Australia, and Woolworths, and its sector weight is anchored in financials, resources, healthcare, and consumer staples.

These are not different flavours of the same thing. They are different in kind.

ETF ownership mechanics matter more than most investors realise: when you buy a single unit of VAS or NDQ, you hold a proportional claim over every underlying company in the index, not a direct shareholding in any of them, and that structure has practical consequences for how dividends are distributed, how capital gains are handled, and how concentration risk actually behaves at the portfolio level.

| Dimension | NDQ | VAS |

|---|---|---|

| Geographic exposure | US (Nasdaq-listed) | Australia (ASX-listed) |

| Sector focus | Technology and innovation | Broad domestic economy |

| Concentration level | High (tech-heavy) | Broadly diversified |

| Currency risk | Yes (AUD/USD) | No |

The sector contrast tells you these funds are not competing substitutes. They are designed for different market exposures, and recognising that difference is the starting point for any allocation decision.

NDQ’s investment thesis rests on capital growth. The fund gives you concentrated exposure to the companies most positioned to capture structural megatrends: AI, cloud computing, semiconductor demand, and the digitalisation of global commerce. These businesses reinvest heavily rather than paying large dividends, which means NDQ’s yield is low and the return profile is weighted toward long-term price appreciation. There are no franking credits, because the underlying companies are US-listed and have not paid Australian corporate tax.

VAS’s thesis rests on income and tax efficiency. Dividend payments are deeply embedded in the ASX’s culture, driven largely by major financials and industrials whose earnings consistently flow back to shareholders, often with franking credits attached.

Franking credit entitlements vary significantly depending on an investor’s tax rate, account structure, and age, with SMSF members in pension phase able to receive the full credit as a direct ATO cash refund rather than a tax offset, a distinction that changes the real after-tax return on VAS distributions in ways that a face yield comparison with NDQ will never capture.

What are franking credits? Franking credits are tax credits attached to dividends paid by companies that have already paid Australian corporate tax on their profits. When you receive a franked dividend, you are not taxed twice on the same earnings. For Australian tax residents on lower or moderate tax rates, or those in retirement-phase superannuation, franking credits can meaningfully increase the effective after-tax value of a dividend, often beyond what the face yield number suggests.

The ATO’s dividend imputation system establishes the precise rules governing how franking credits are calculated, attached to dividends, and claimed by resident shareholders, with the framework explicitly designed to prevent Australian corporate profits from being taxed twice at both the company and individual level.

Because NDQ holds US-listed companies that do not pay Australian corporate tax, its distributions carry no franking credits at all. This is not a minor technical detail for Australian investors; it changes the real return comparison.

Understanding both cases on their own terms prevents the common mistake of dismissing either fund because it underperforms on a dimension it was never designed to optimise.

Risk tolerance is not a personality trait you declare on a questionnaire. It is a financial and emotional capacity that gets tested when markets fall, and the test results matter more than the self-assessment.

NDQ is a concentrated technology and growth fund. It has experienced significant drawdowns during rate hike cycles and periods of broader market stress. VAS, composed of mature, cash-generative businesses across a diversified sector base, has historically produced more moderate price movements. The difference is not accidental; it is structural.

Technology and growth stocks are particularly sensitive to rising interest rates. The mechanism is straightforward: higher rates increase the discount rate applied to future earnings, which compresses the present value of companies whose profits are expected to arrive years or decades from now. NDQ’s holdings are concentrated in exactly these long-duration earnings streams.

VAS holdings, including banks, miners, and consumer staples, are less exposed to this valuation dynamic. Some may even benefit from rate environments that reflect a strong economy. The result is that during rate-driven selloffs, NDQ can fall materially harder than VAS.

The practical implication runs deeper than the numbers.

If you would sell a fund that drops 30-40% in a rate-driven selloff, NDQ’s long-term return potential is academic. The fund only delivers on its growth thesis for investors who hold through the drawdowns. Selling at the bottom destroys the compounding that makes the volatility worth enduring.

This is the most common and costly mistake individual investors make: choosing a fund based on past returns without honestly assessing whether they can stay invested through the volatility required to earn those returns.

The prior sections described what each fund does and what it demands. This section tells you where to place yourself.

NDQ may suit you if:

VAS may suit you if:

The superannuation angle deserves particular attention. Many Australian investors already hold significant domestic equity exposure through their super fund, often in portfolios that look structurally similar to VAS. If that describes your situation, NDQ is not competing with VAS for the same allocation. It is filling a gap that your existing super exposure leaves open, adding international technology exposure that the ASX underrepresents.

The comparison itself can be misleading if it pushes you toward an either/or conclusion. For many investors, the most analytically sound position is a deliberate allocation to both.

The rationale is structural complementarity. NDQ and VAS operate in different geographies, different sectors, different currencies, and respond to different economic drivers. When global technology sells off during a rate cycle, Australian banks and miners may hold steady or benefit. When commodity prices fall and weigh on VAS, technology demand may continue to grow independently. This is not a guarantee of smooth returns, but it is the basis of genuine diversification: holding assets that do not move in lockstep.

ETF portfolio construction for Australian investors involves more than selecting the right individual funds; the proportional split between growth and defensive assets, the interaction between domestic and international exposures, and the management of concentration risk at the total portfolio level are each variables that asset allocation decisions must account for before any individual fund is selected.

VAS provides the income and domestic stability layer. NDQ provides the growth and international technology layer. The combination reduces your dependence on any single market.

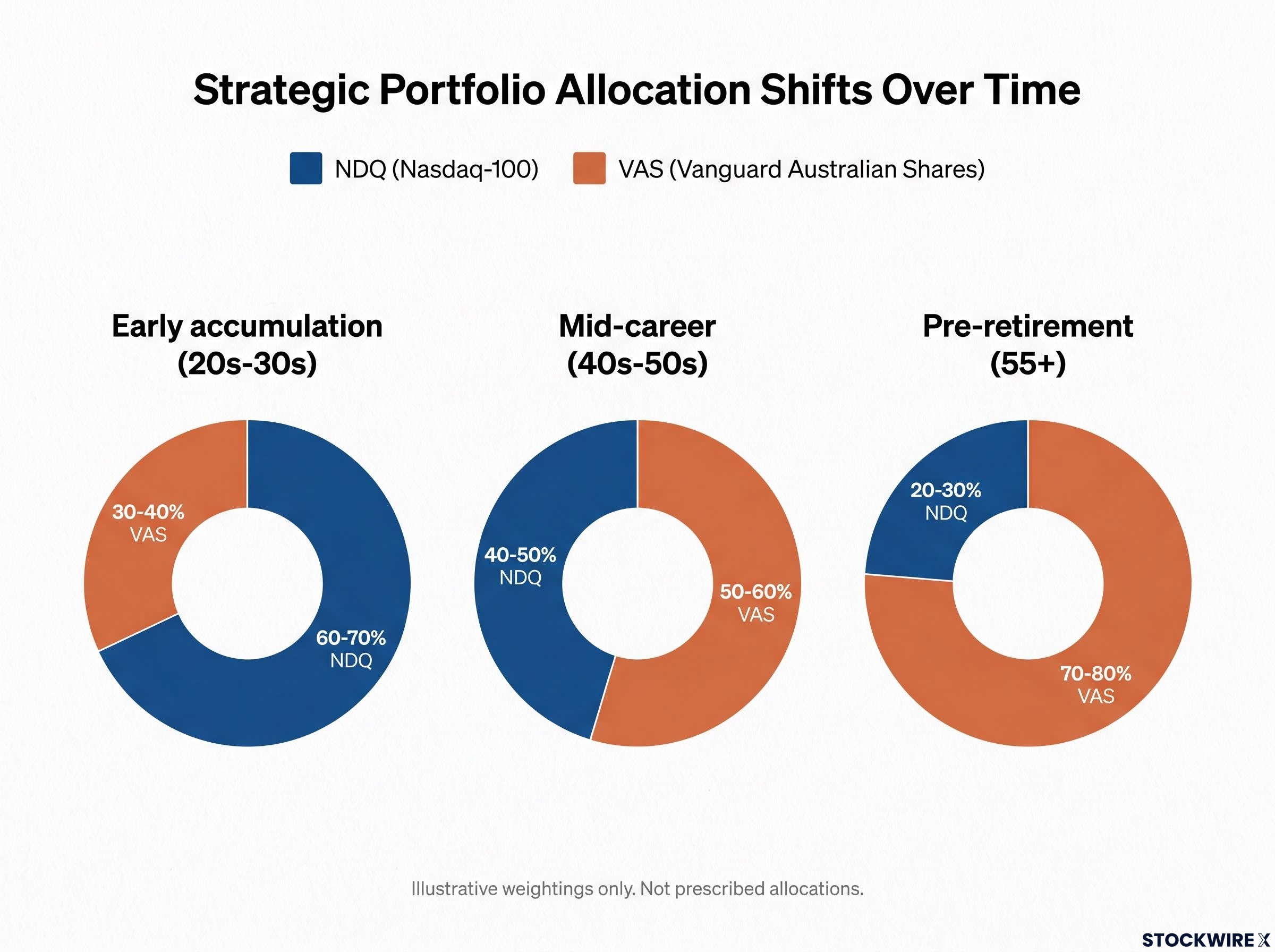

The weighting question is where it becomes personal. Your age, income needs, risk tolerance, tax situation, and existing super exposure all shape the right split.

| Investor profile | Illustrative NDQ weighting | Illustrative VAS weighting | Rationale |

|---|---|---|---|

| Early accumulation (20s-30s) | 60-70% | 30-40% | Long horizon favours growth tilt; VAS provides stability base |

| Mid-career (40s-50s) | 40-50% | 50-60% | Balancing growth with increasing income needs |

| Pre-retirement (55+) | 20-30% | 70-80% | Income and franking credits prioritised; NDQ retained for growth |

These weightings are illustrative, not prescribed allocations. Individual circumstances, existing super exposure, and financial goals should determine any actual split.

The weighting question is not a formula. It is a mirror: the right split reflects what you are actually trying to achieve with your non-super investment capital at this stage of your life.

NDQ is a high-conviction global growth vehicle concentrated in the companies reshaping technology infrastructure. VAS is a diversified domestic income engine built on the mature, cash-generative businesses that anchor the Australian economy. Neither is universally superior.

The decision that matters is not which fund performed better over the last year or the last decade. It is which fund, or which combination, aligns with your time horizon, your income needs, your risk tolerance, your tax position, and what your superannuation already covers. The answer is always downstream of those personal realities.

The reader who finishes this analysis should feel better equipped to have a more informed conversation with a financial adviser, not to bypass that conversation entirely.

For investors who want a systematic method for evaluating NDQ against other technology-focused options before deciding on an allocation, our full explainer on comparing AI and technology ETFs walks through a five-criteria screening framework covering concentration risk, value-chain positioning, cost, liquidity, and currency exposure, with worked examples showing how sub-sector tilt alone drove a 70 percentage point performance gap in 2026.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

NDQ tracks the 100 largest non-financial Nasdaq-listed companies, concentrating exposure in global technology and innovation, while VAS tracks a broad cross-section of ASX-listed companies weighted toward financials, resources, and consumer staples, making them instruments designed for different portfolio jobs rather than competing substitutes.

No. Because NDQ holds US-listed companies that have not paid Australian corporate tax, its distributions carry no franking credits, which meaningfully changes the real after-tax return comparison with VAS for Australian investors, particularly those in retirement-phase superannuation.

Technology and growth stocks are sensitive to rising rates because higher discount rates compress the present value of companies whose profits are expected years or decades into the future, and NDQ is concentrated in exactly these long-duration earnings streams, whereas VAS holdings like banks and consumer staples are less exposed to this valuation dynamic.

Yes, and for many Australian investors holding both is the most coherent approach, since NDQ and VAS operate in different geographies, sectors, and currencies and respond to different economic drivers, providing genuine diversification rather than overlapping exposure.

The article suggests a growth-tilted split of roughly 60-70% NDQ for investors in their 20s-30s, shifting toward a more balanced 40-50% NDQ in mid-career, and moving to a predominantly VAS allocation of 70-80% for pre-retirees who prioritise income and franking credits, though individual circumstances should determine any actual weighting.